House prices continued falling in July with the national median price declining 2.2% to $753,000 from $770,000 in June. It was also down by the same amount compared to July last year, according to the Real Estate Institute of New Zealand (REINZ).

However the fall in Auckland was much greater, with Auckland's median price declining $80,000, or 7.8%, to $950,000 in July from $1,030,000 in June.

The biggest monthly drop in Auckland was in its central suburbs, which includes suburbs such as Herne Bay, Ponsonby, Grey Lynn, the CBD, Parnell, St Heliers, Epsom, Remuera, Mt Eden and Mt Albert, where the median price declined by $182,000 between June and July, dropping from $1,250,000 in June to $1,068,000 in July (-14.6%).

That suggests the biggest falls in prices have been at the top end of the market.

Wellington's median price declined by $28,000 in July and the Canterbury median declined by $36,000.

See the interactive graph below for the full regional median price trends.

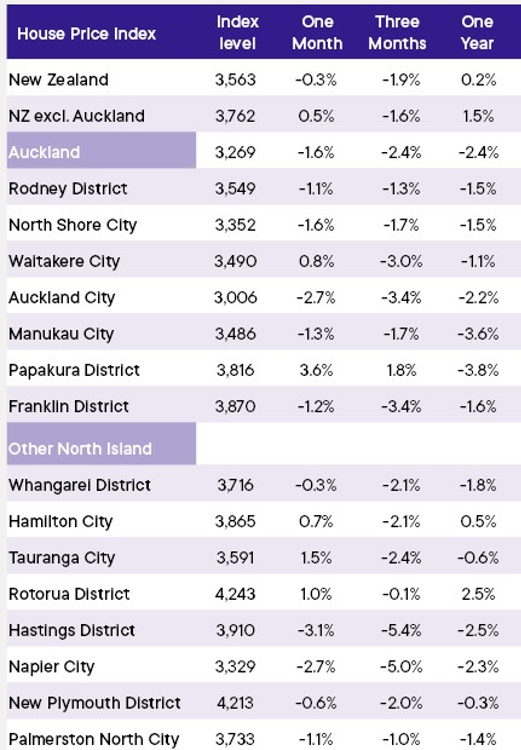

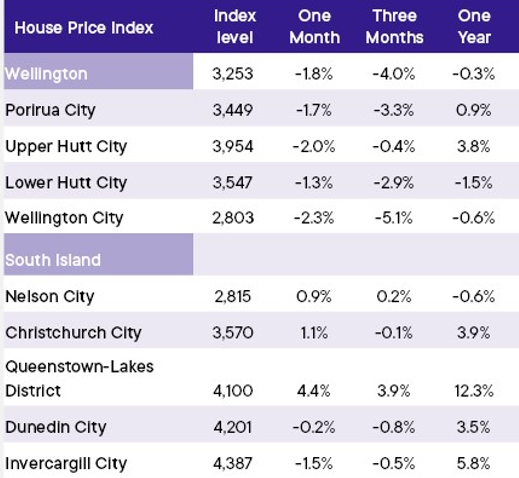

The REINZ's House Price Index, which is adjusted to account for changes in the mix of properties sold each month, declined by -0.3% nationally in July compared to June and was down by -1.9% over the three months to June.

The table below shows the change in the HPI in the main urban districts around the country over the year to June.

The ongoing decline in prices follows falls in vendors' asking prices, as reflected in the most recent reports by property websites Realestate.co.nz and Trade Me Property.

However the decline in asking prices appears to have been to the benefit of buyers, encouraging more of them to commit to a purchase.

A total of 5806 residential properties were sold throughout the country in July, up 19.7% compared to June and up 14.5% compared to July last year.

In Auckland, the effect lower asking prices had on sales was even more evident, with 1805 residential sales in July, up 21.5% compared to June and up 5.5% compared to July last year.

See the second interactive graph below for the full regional sales volume trends.

The jump in sales in July pushed down the total stock of residential properties on the market from 31,745 in June to 30,556 in July, but that was still up by a whopping 32% (+7466) compared to July last year, suggesting buyers will continue to have plenty of stock to choose from and will still have the upper hand when it comes to negotiating a price.

- The comment stream on this story is now closed.

Median price - REINZ

Select chart tabs

Volumes sold - REINZ

Select chart tabs

NZ House Price Index - July 2024

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

283 Comments

Ouch Auckland and Wellington.

Looks like delayed report does in fact mean bigger drop.

Like the super yacht that sank, our housing market is sinking too.. hope there are sufficient life jackets

This is why a 3 month average with the next 2 is so important, I don't see AKL down 7.8% for 3 months in a row....

Aucland Chart looks like a classic Dead Cat Bounce

Team DGM - what a time to be alive!

Comes down to fundamentals which the spruikers tend to deflect

You should check for a pulse first, you DGM's can never be too sure.

Damn. Imagine house prices fall a lot further... smart kiwi kids start to stay to rais ea family and become teachers and police and start productive businesses.. our economy shifts to productive business we all have more money to spend and the rich poor divide narrows.

Vs the few get richer, society starts to break down and all the smart kids leave.

Who is the DGM? Lol

Please don’t get me wrong, its an epic idea to want to create a pathway for young people to prosper in NZ…but I’m just at a loss how house prices continuing to fall a lot further gets us there…how does the rest of the economy look in your future, how are the government paying for all the new teachers and police officers…if you’ve got the solution then please my man share it!! 🙌🙌

perhaps incentivise investment in the productive economy and disincentivise investment in (or at least tax) the financialisation of housing, especially land value appreciation.

To give a more extreme example of overfinancialisation than typically seen in NZ, last time I visited China in 2019, a typical apartment in inner Tianjin cost the equivalent of $1m NZD, with max $20k rental revenue, covering roughly 1/3 of the holding costs, with no land ownership option. Scaling that up, China's housing is many trillions of dollars in debt, all in hope of capital gains, many with insufficient revenue to cover carrying costs.

how are the government paying for all the new teachers and police officers

By simply paying for them? Reducing spend on landlord and wealth subsidies, increasing tax on things like capital gains.

The govt is not and can never be broke, the nonsense that we can't afford these things is simply that, nonsense. The trade off will be a lower standard of living in terms of consumables, which is where we're going regardless. So why not ditch the private debt for non-productive enterprise and actually look to get something (a service) in place of money instead.

I'm going to throw it out there and assume we want to continue having young people in the pipeline?

As a 30yo with a long term partner, no kids and no house we will have to choose between kids or a secure roof over our heads with the way things stand. We live frugal lives and are much luckier than most with our financial situation, but still can't make the finances work. I suspect most our age are in the same boat, hence the plummeting birth rate.

If we could buy a more affordable home, we might have kids, pay for holidays, more food, meals out, clothes, child services. I might even feel more inclined to buy the expensive local products. Right now there's little buy in from me, if my partner weren't so close with family we'd be out of here.

How does the economy look in your future? With wealthy old folks yearning for their overseas children while they receive inadequate care from cheap imported labour. How are the government paying for the aged care and hospitals when the working population are sending their spare $$$s overseas rather than spending locally? At least the teachers and police will be cheap imported labour too, not sure we'll love the cheap option when it's failing to keep us safe.

Agree completely with your comment Jake.

One question, which party does your cohort vote for? Do they vote?

Maybe they don't care, from my limited exposure to useful 20 somethings the plan is often just get qualified and get out.

What does voting matter? No party has the right mix of policies (TOP gets somewhat closer but has no charisma or presence)

Disagree, TOP had very good policies for renters rights/housing/housing demand (good immigration policy) in the first couple of elections. Remained head and shoulders above others with the LVT tax switch last election although dropped the immigration policy unfortunately.

If you see the reply from Jake below, the point is this group are largely not voting 'sensibly' if housing affordability is driving them away.

I went TOP last time, act time before. Mrs was NZ first last time and Labour prior.

Most friends yoyo between the 2 main parties as unfortunately too many young folks can't take a few hours every 3 years to do some reading.

I've voted TOP the last three elections.

Thanks for adding weight to my suspicions. It's a bit hard to change anything on the housing front by voting for the status quo.

@Jake94 I hear you, I'm early 40's with three sons in their early teens...I am aware of how things are and I am bloody scared for what their future holds. But ole mate saying "lower house prices will fix it" is stupid. Lower house prices will make houses cheaper 💡...but the pathway to getting house prices to fall a whole heap more...jeez, that's probably a pretty untidy picture...it'll be damn hard to buy that house without a job eh 🤦🏻♂️

I truly think that we need to make lending more affordable to get things moving, to get the economy moving it will take rate cuts...but we also have an opportunity here, there will be a lag in these cuts taking effect so over the next 6-12 months hopefully we can squeeze a bit more out of house price decreases then we need to aim to keep prices there for as long as possible, use tools like LVRs and DTIs to try to cap growth, get the government doing some JVs with developers building modest, but modern warm/dry 2 and 3 bedroom houses to improve availability of lower priced homes, maybe even with rent to own opportunities, keep the OCR at a sustainable lower NIR creating more affordable mortgages so that we can have steady longterm growth in our economy which hopefully brings steady longterm wage growth with it...over a few years if wages go up/house prices stay the same/lending becomes more affordable...maybe, if these stars align then we can get affordability to a happier place.

Just simply having this narrative of "lower house prices will fix it" worries me....we only have lower house prices because our CB engineered a recession and its turning out to be a pretty gnarly one...to get house prices a lot lower, what is the true cost to the country?

Also, sh*t, now that the RBNZ who are responsible for these significant decreases have changed from a raising rates mindset to a lowering rates mindset...you would have to think there is just as much likelihood that they will be responsible for potential significant increases? We need to look at how use other tools and what else can we do now...or the sh*tty boom bust cycle continues.

I hope you and your partner can get a home, and the chance to raise a family in that home mate. Let's hope that opportunity is also there for my boys in 20 years as well.

You simply prefer the definition of Affordability as "Lower Price of Dept" as opposed to "Lower price of Asset" . Your thinking is in line with pre-2022 peack narrative. Everyone got the idea by now that it was the whole reason why we got into trouble in the first place. RBNZ popped that bubble , and last week has thrown a bone of 0.25% cut so people who desperately sharing your views don't lose hope that things will go back to "normal". However , ^^^Higher For Longer^^^ is still the thing . Budget accordingly !

The Auckland chart is looking as classic bubble if you widen the chart to all years. And the next stop is under 800k if not close to 670k to match 2013 year

Haha ok champ…unfortunately history proves that boom/bust cycles are “normal” and if we’re not careful then we will back to “normal” at some point over the coming couple of years…I’m “desperately sharing” views on how we can keep prices lower sustainably🤦🏻♂️

I thought you made some pretty valid points tbh.

yeap , could not agree more with you , however the key words in your message is "over the coming couple of years". So now is still "Bust stage"

Yes - flat in nominal terms and decline in real (wage adjusted) terms would be beneficial to younger generations. To get there we'll need to lower our trade deficit and increase govt spending into our economy, on service, such as nurses and police force as you mentioned, and on infrastructure.

This is the number one concern with our current govt suggesting a surplus is even possible, if we go there we will see the economic destruction and asset price decline you're suggesting will destroy our economy. We've spent decades shifting the burden onto the private sector, we will need to start shifting back. The private sector has proven inadequate at providing useful investment into the economy, mostly due to the regulations set out by the RBNZ in terms of risk weighting held against residential property.

We cannot run an economy on paying older generations large amounts of money on the hopes that they will reinvest that money back into our economy because too often those windfall gains are spent offshore on imports and luxury vacations rather than invested in working local occupations.

I think you’ve nailed the situation that’s been playing out Jake.

We’ve just lived through peak boomer which was all about ensuring we used policies to ensure that generation retired with peak wealth at any cost (monetary and fiscal policies have all been catered towards this over recent decades) with no care how this would impact those in their 20s-30’s. Gen X have generally done well by living in the shadows of the boomer generation and sharing the financial tailwinds with them (think of those now in their late 40s and 50’s. Later stage millennials and Genz (those under 35) have been setup to carry the risk (and pain) of the excessive benefits transferred to the generations above them. Ie the housing wealth of those 45+ is only because of the high debt saddled on new FHBs recently entering the market (an asset is offset by another’s liability).

But the peak boomer period is coming to an end. They are losing democratic power as they die and will in the coming 5 or so years be outnumbered by their millennial children who will then be the largest voting demographic in the country. Change is ahead.

A really good book on this is ‘The forth turning’ or watch any of Neill Howes interviews on YouTube (author of the book/generational theory).

Way too much generalisation

It's what's happened though. Whether those who have benefited from it personally advocated for these types of policies is another story. The big issue is that many are not willing to accept or concede these economic tailwinds had a lot more to do with their accumulation of wealth, than just plain old hard work.

those police officers and teachers need to BUY HOUSE to live somewhere in Auckland as well , so the falling price is better than even 10% salary increase. Simple math

AKL fell 80k that's a years salary right there.

must be a coincidence, when house prices is down, economy is in recession.

parents lost their jobs, so will the kids.

Dad's always angry unless he's drunk, alcohol must be the cure.

"Here's to alcohol: the cause of, and solution to, all of life's problems"" - Homer Simpson

and yet you wish alcohol vanishes once for all, even though it has been existing since agriculture existed, and will always stay as long as human exists.

I said what now? Careful you don't get blisters trying to shovel words into people mouth like that.

Truth hurts for specu land. Down down in ponzi town.

Waiting for Orr on his white horse.

No surprises really. I expect the downturn to continue considering the headwinds in the economy. It will be interesting to see how it goes over spring and summer when peak selling season, but still doesn’t look flash.

Agree - it will decline further or remain stable for next 4 months

It's always best to look at these Ponzi data sets emotion-free. What's quite interesting with this data set is comparing the magnitude of change between the 3 month vs 12 months - near-term falls are directionally larger than longer term falls. Make of it what you will but subjectively any notion of a symbiotic relationship between house price, the wealth effect, and general economic vitality measures seems to be in effect.

Problem is that if people start believing their net worth is falling $17K per month, it's not good psychologically for consumption. And we need those wallets to be open. Because if they're not, the Ponzi starts to cannibalize itself - like an animal eating its own limbs.

Exactly - the collective needs to believe the bottom is in. That happened March last year, proven wrong.

I have a deal for you, sign up now to lose $250 cashflow per week so that you can lose $17k equity per month.

Prices halve every ten years, don't be a DGM, get in quick.

Buy buy buy. Support those poor speculators.. all watching Duval owners having to sell their lambos and live on 2k a week. And seeing their future play out.

"It's always best to look at these Ponzi data sets emotion-free"

So you're into comedy now J.C. that's a good one 😂.

Good post of course, but it will fly way over the heads of the masses who cheer for a collapse of house prices, like they cheer for their favorite sports team.

Who would not want to buy their dream home at a cheaper price?

At a cheaper price…then don’t buy now…the apocalyptic collapse is still coming…or so I’ve heard…many many times on here 😂

If you want to buy a home, and can afford to buy it, and intend on owning it for five plus years then buy it 🤷🏻♂️

Or if u think prices will fall .. just rent or goto oz for a bit. Relax enjoy life and buy it for $200k less in 2 years time. You can then retire 5 years earlier.

Auckland down $400k+ from the peak..... Am I reading that right? Still not a crash guys. /s

It's not a crash because it didn't drop 400K in a day and if it did drop 400K in a day it would only be a crash for that day, the next day crash would be over and it would be prices going up again.

In NZ it can never ever be a crash.

Lol

it’s a crash

Yeah it’s such an idiotic but widespread sentiment. “If it’s for the long term, just massively overpay. It doesn’t matter. Drop 100k on a Toyota Corolla. It’ll last you years.”

I for one am happily sat on the sidelines watching more and more suitable properties fall into my price range each month. If i'd listened to people like you i'd currently be stuck in some shoebox townhouse in negative equity right about now..

"If i'd listened to people like you i'd currently be stuck in some shoebox townhouse in negative equity right about now.. "

If you were in that situation, how do you think you would feel about being in negative equity?

Negative equity “about now”…if you’d brought that shoebox to try and make a quick buck on capital gains then hey sh*t happens and you made a poor decision…if you brought it as a home and you believe you will still be in negative equity in five years then I think you must’ve brought a really really sh*t place 😂

Except that the shoebox's were selling for 900k plus in 2021. Now there are nice detached 3 bedrooms on a decent section selling for that price point. By ignoring the 'advice' of buy now if you can afford it, I will end up with a much nicer house and with a smaller mortgage..

It’s been happening for two years. Where you been?

"Who would not want to buy their dream home at a cheaper price?"

See, J.C.'s point flew right over your head.

IT Guy sold at the top of the market - just after you bought. So who's the clever one?

I sold in the last week of Oct 2021 and got nuts money from a developer who had not even seen the place (up 384% and I spent about 20k on it...). It would have been worth more without a house on it. The bath had a shower curtain over, it was that old, windows rotting. they paid mid 3's for it, Its lost so much value they had to sell their Takapuna house and move into it, They are down about 1.25mil so far. I guess the numbers no longer stack up for 5-6 units on it, and you can buy in the local area a reasonable place on 800 sq m now for about 1.8-2.25 Meanwhile I moved to the country, which we can subdivide, swapped 800 sqm for 157,000 sq m.

I tell you what I will do for you Yvil and Z, I will ring a bell on here when I think its the bottom to help you out. Clearly your market compass is spinning like the little propeller on your cap.

Of all the flexes I've seen on interest, I think this is one of the biggest.

I thought you said that the old st heliers place was a shitter you had as an investment, you bought the country house a couple years before the other was sold. Really hope you didnt have to pay brightline

No I was living in the old shitter for 11 years, I bought the country one on condition I had 28 days to sell the shitter. In the middle of a housing boom ... 28 days... and got more for the old one , even after RE fees of like 60k... banking a difference. no brightline at all involved.

It was only the risk of the auction and marketing. I could walk away if the sale price did not meet my reserve.

The old shitter is a great suburb, it was Glendowie, my kids went to Churchill park school, it was great for kids growing up but it needed a 1.8-2mil house on it to correctly Capitalise up at the time, and I did not want that size mortgage, it served its purpose, raised my two kids , great schools and made me about 2.4 mil. SOLD TO THE HIGHEST BIDDER.

Rank group where the under bidder, it was a fair price at the time. They saw value building an exec house there just down the road from the homestead.

Changing the story? Pretty sure you bought in 2019, maybe you also sold then but sounds better to say "sold October 2021"

Your insecurities, envy and bs stories are particularly strong today ITG.

I thought you were the resident hall monitor to shun this kind of behavior. Did you give yourself a hall pass to type this out?

Well, it looks like you thought wrong.

The country is nice IT Guy, done it twice in my lifetime its great when you are young, did acres of pine plantations twice but finally moved on to the ultimate place in the burbs with all the land to just view without having to look after it and cows in the paddock next door and can watch the sunset over the Kaimai. There is a time and a place for everything and I no longer care if the market goes up or down.

Surely you would have commented about this twice in your lifetime country living before now, it's not like you not to blow your own trumpet.

So you're into comedy now J.C. that's a good one

Nothing funny about it Dr Y. Dispassionate might be a more apt adjective than 'emotion free', but it's definitely not amusing. I don't think anyone should underestimate the destructive effects that emotion and psychological impacts can have on our economy. The problem is that I think we have been to led to believe our own BS, so when things don't work like we've been told by the ruling elite, media, influencers, and our peers at the water cooler, people start to get nervous.

Or not funny if you're Yvil's neighbour in St Mary's Bay and you have an empty home you can't sell

https://www.trademe.co.nz/a/property/residential/sale/auckland/auckland…

Paid $2.35m in 2015

CV. $4.05m

Asking $2.85m

Bet's on what it will sell for?

"Bet's on what it will sell for?"

Depends on whether the vendor is willing to meet the market. The property has been listed since April 2024.

There is a property of a property trader who has listed their owner occupied property for sale in Jan 2023 - 20 months ago. They have dropped their price to a fixed price and still unwilling to meet the market, so it continues to remain unsold.

My thinking is around 2.4m

Imagine the noise let alone the carbon monoxide streaming in the windows from the motorway.

yeah massive downside of that location.

It looks like it's on the cliff, so possibly some existing geotechnical issues or risks exposed by the rains of 2023

What storm?

What happened to your green tick you had for about a month HM?

He's ticked off

LOL

Really Yvil? Really?

They have had a tough H1 2024 and the rest is going to be shit for Spruikers as well.

Their true nature is on display tonight via their comments. Cannot accept they are wrong and market is heading lower.

Breath in that pure motorway air! Enjoy the quiet surrounds! Put your mind at ease with its clifftop setting!

"I don't think anyone should underestimate the destructive effects that emotion and psychological impacts can have on our economy"

The bigger the party, the bigger the hangover.

Remember, the extreme debt risks were preventable back in 2016 when the then Finance Minister did not give the RBNZ the tools they requested to address macroprudential risks. Remember that there was lobbying by those with their vested financial self interests to not implement the debt to income measures. It may also have become a political issue with the upcoming elections at the time and may have cost potential votes for the incumbent government at the time - this policy would have adversely impacted property investors, and most owner occupier buyers (including first home buyers) - a potentially large voting constituency. At the time many with their vested financial interests were arguing that the debt to income restrictions would restrict first home buyers from buying (what they didn't say was that it would also protect first home buyers from taking on too much debt because that would not support their case and vested financial interests)

The RBNZ can only operate with the tools available. If the necessary tools are unavailable, then there are consequences of having inadequate resources.

https://www.interest.co.nz/property/85201/reserve-bank-confirms-meeting…

The RBNZ governor stated in 2021, that the choice by the government to allow or not allow DTI's was a political one:

But he has suggested that the Government's decision around giving the central bank debt-to-income (DTI) restriction powers is a political one, as it might adversely impact first home buyers.

"It comes down to a political decision around whether they [the Government] are willing, or not, to provide those tools and accept some of the challenges that may bring," Orr told media this morning.

https://www.nzherald.co.nz/nz/reserve-bank-boss-adrian-orr-warns-mps-of…

If you assume it would have taken 30 months, then the DTI framework may have been ready to go sometime in in 2019. This would have been before interest rates reached their record low levels in mid 2021.

If a debt to income ratio of 5 was imposed back in 2019, then a significant amount of lending would not have been made (and debt to income levels would have been less likely to have reached their record levels). Many first home buyers would have been rejected for large unaffordable mortgages like this guy (https://www.newshub.co.nz/home/money/2021/11/first-home-buyer-not-very-….) He was disappointed at the time of his loan rejection, but in hindsight he is likely to be thankful that the bank refused to give him a large mortgage that he applied for and hence avoided cashflow stress and a large loss in his equity (and potentially negative equity).

As a result of that single policy decision back in 2016, this will result in potentially thousands of highly leveraged owner occupiers who purchased in 2020 - 2022 being collateral damage, including those first home buyers that you refer to. This will cause cashflow stress, mental stress and unfortunately, some will resort to self harm.

This will likely also lead to an increase in demand for social housing.

There has been a lot of speculation in residential dwellings in many other countries also - look at Japan in 1990's, Ireland in 2007, USA in 2006-2007. There were many owner occupiers that became collateral damage.

Here is an example of owner occupier collateral damage from falling house prices elsewhere around the world:

1) https://www.investorschronicle.co.uk/2012/09/20/your-money/property/ove…

2) https://youtu.be/iKPG_l1P7lk

3) https://youtu.be/ugBKnP2FKDM

4) https://youtu.be/fiCXsu_4BoA

5) https://youtu.be/1hi7gV9uyK8?t=2297

it's not good psychologically for consumption. And we need those wallets to be open.

True, but to what end JC?

Maybe we have to face the reality that most of the recent decades have been debt fueled consumption 'growth' and that if opening the wallets is just more of the same it's only ever going to end one way (an almighty crash when the can finally disintegrates from being kicked too many times).

While I very much want lower housing costs (rent and purchase prices), I take no joy from these reported decreases because they aren't from deliberate corrective measures to fix the cost of shelter. Another spin of the wheel so to speak and nothing that more population growth and lower interest rates couldn't reverse.

Bang on Murray, unfortunately it’s not a sustainable change in long term housing affordability bringing down prices…its all on the back of higher rates from an intentionally engineered recession…what happens soon when RBNZ’s narrative changes 😟

I can attest to this. I just gnawed off my own arm.

perhaps the bottom is 1% lower?

The DGM talk about "Ponzi" with no understanding of what the word means.

TTP

And you do, I am very certain!

TTP's certified qualifications are more along the lines of price fixing.

"TTP's certified qualifications are more along the lines of price fixing."

Does that merit questioning that individual's trustworthiness, integrity and quality of character?

"Problem is that if people start believing their net worth is falling $17K per month, it's not good psychologically for consumption. And we need those wallets to be open."

From the peak, the collective fall in wealth in housing is NZ$295bn in nominal terms. This is approximately 72% of GDP.

In inflation adjusted terms, from the peak, it has been a 26.5% fall in purchasing power.

According to a number of regular spruikers, this still isn't a crash....

The objective observers have recognized the housing crash since 2022.

"According to a number of regular spruikers, this still isn't a crash.... "

Property promoters are motivated by their own financial self interests and this can result in misinformation, and disinformation. That can cause conflict of interest from those seeking facts.

Jimbo was on here the other day saying NZ was great because we are the 6th wealthiest nation in the world and he and all his mates have made a killing through property. We might start slipping down that rich list quite rapidly if the current trend continues - you’ve highlighted that a significant amount of that wealth that Jimbo was referring to has just vaporised..gone..may not be seen again unless we can restore the aggressive house price rises once more. In y view that wealth is an illusion (the real wealth is production which raises the prosperity of everyone and not just asset holders of benefitted from falling interest rates.)

a significant amount of that wealth that Jimbo was referring to has just vaporised

That's the main issue, it isn't wealth until realised by selling to a greater fool, it is simply an imaginary concept. At some point people wise up and realise that they don't need to be a fool.

In my view property is done for years to come. The reality of betting on an illiquid asset, loaded up with debt where the rates change and you are unable to leave the sinking ship is now becoming clear to everyone. For those who have purchased to live in (such as me - but I purchased years ago), there is no issue, the mortgage is easily manageable, and the house is sound (assuming you have not purchased a leaky home of course).

Those in the market purely for capital gains and there are many, are done. Many facing bankruptcy either now, or in the next 12-24 months as the prices relentlessly job, as more desperate gamblers put their properties up for sale to save their family homes or stave off bankruptcy and total ruin.

I think for many years, once a bottom is reached, prices will remain stable for a protracted period, and people will begin to invest in other vehicles, such as shares, which have remained quiet in NZ really since the last market crash as a result of speculation. We may see the rise of finance companies again and an eventual meltdown like we have in the past, but I think we can be pretty sure that the next speculative investment vehicle will not be property in this country.

yes the market is out of fools.... buyers are in control

-5.8k a day!!!!

1.6% for Auckland ☺️

Tauranga pretty much stable. Expecting a rise from here. Probably a bit late now to see my predicted 3 to 4% gains this year but a few more OCR drops will see that happen next year.

a few more OCR drops will see that happen next year

Wouldn't get your hopes up. For that to happen we'd need major Govt intervention in the market, again. Job losses, business closures. OCR cuts got us looking like we're slipping down a muddy bank grasping at green shoots to try and stop us sliding.

That was almost poetic

Tauranga pretty much stable. Expecting a rise from here. Probably a bit late now to see my predicted 3 to 4% gains this year but a few more OCR drops will see that happen next year.

Chin up Z.

A fish rots from the head, the regions will follow Auckland down.

I don't believe so, things changed post Covid and the regions are now more desirable than ever. Auckland is now pretty much buggered with traffic congestion and its never going to improve. The market will turn pretty fast, lets come back here are Christmas, only a few months to wait.

Tauranga is the poster child for free flowing traffic..... wrong straw to clutch at.

Traffic is bad in TGA for all of a few kms at peak hours. Nothing compared to Auckland.

Tell us you've never driven around Queenstown, without telling us...

As an Aucklander who recently had to work in Queenstown for a week I was horrified at the traffic. Far worse than my daily commute in Jaffaville. The views from the car were lovely though.

Yep, that 14km Lakes Hayes to Queenstown Central gridlock sure is pretty.

Same feeling in Christchurch.

Auckland also helps fuel other regions as people leave, however that is dependant on them selling their AKL place 1st....

Have to wonder how Tauranga will survive with TD's heading down.

Will not be a problem down here with so many cashed up retired people. Went to Mitre 10 in the middle of the day on a Tuesday down here, was lucky to get a seat it was like lunch at a rest home, place was packed with oldies tucking into way to much food. Also I see a record number of new jobs in the BOP, its leading the way in terms of recovery.

The CBD is thrieving

When the Aucklanders cant sell then Tauranga sales are also hit especially at the top end and lifestyle market - supply of Aucklanders buying in Bay of Plenty has dried up

Record number of Boomers moving here, its a growth city. Got in just in time, better even than Riverhead.

Boomers are dying - just read the obituary section of the newspaper.

My street (10-12 hoses) has about 70% widowed women living in them all 70+. At some point in the next 5-10 years they are al going to need to downsize from the current 3-4 bedroom homes they are living in on 500-800sqm sections (I spend a decent amount of time doing jobs to help them at present after their husbands have passed). One house is now sitting empty as the 90 year old man living in it just moved into a rest home the last month or so. Only two or so families living on the street utilising all the bedrooms.

This. We rent in a central leafy street. 3 bed bungalow on a street with a mix of similar bungalows, villas, some in-fill townhouses, and state housing down the lower end. With the exception of one house, we are surrounded by the elderly (mid 70s and up), mainly widows and widowers.

In one case, they have family coming to visit. In all other cases, there is no one coming or going, and the houses are in poor condition and deteriorating rapidly. It's very sad

where are you guys located?

One wonders if banks risk management teams have employed actuaries like insurance company's have, I doubt it.

They do.

Clotshot?

According to REINZ this is green shoots. Uhhh....

They needed an extra weekend to find a way to spruik this one

The positive spin they've put on this release is comical

Its called capitulation

I think we are still in denial stage. Capitulation looks worse than this but might happen the next 6-12 months if prices keep dropping.

In 3 months time if the market has gapped lower and even last months prices are not achievable, then yeah summer could be real ugly and 2017 prices may not hold, 2015 support?

I look at the price chart and if prices keep dropping the next few months with downward trend I have no idea where the bottom is.

As I’ve mentioned numerous times here I believe it is entirely possible that rates get cut but house price falls accelerate simultaneously (ie cuts are only happening in parallel with just how bad the economy and debt servicing has become).

To me, a sensible national average house price (relative to incomes) should be around $550k. And that is a long way below where we are right now. We can mask that by dropping rates to zero but we only find ourselves back where we currently are with a kaput economy. Until we can reduce private debt vs gdp we are fkd in my opinion. But that will require even more government spending which could be highly inflationary meaning rates could be on the rise once more down track which will limit any house price appreciation as we’ve witnessed the last few years with above 3% inflation.

Could be wrong but I think we’ve left the goldilocks era of the past 20 years where inflation was contained and falling interest rates with modest income growth (coupled with high immigrantion) gave tremendous tail winds for house prices here.

I agree

Indeed, there is still hope in the form of lower interest rates and population growth. We haven't reformed taxation so that owning more property than you need to live in is a poor long investment. Only when the masses believe there is no chance of owing multiple houses being a road to riches, will we see capitulation. As such, there is a chance we never will with current settings (tax, immigration, interest rates via inflation midpoint target of 2%).

We can still reach capitulation in the short term (6-12 months). Interest rates will remain restrictive and aren’t dropping fast enough to stop the price corrections in Auckland & Wellington. There’s simply more sellers than buyers at currently expected prices. 25bp cuts can't slow down the momentum.

The HPI for September will be interesting - positive months will be dropping off the 1 year. Probabilities are increasing for the 1 month / 3 month / 1 year numbers turning red for Auckland. Not a good sign for the denial phase.

Patient FHB's who ignored the call to buy in August 2023 will have done well adding interest to their deposits as opposed to paying it! Look at what's happening now. The flawed August 2023 bottom call is hanging on by a wafer 0.2% margin. If adjusted for inflation, that's equating to quite some fall on a pa basis - Nice!

Retired Poppy

"Patient FHB's who ignored the call to buy in August 2023 will have done well"

Yeah, and those FHB who listened to your call throughout 2017, 2018 and 2019 are now finding properties 30 to 35% more expensive.

And don't blame Covid; your advice was poor throughout 2017-19 as house prices continued to rise. The only Covid effect for them was that they missed out on the opportunity to pay their mortgage down at 2.5% as your favoured advice of term deposits got next to nothing.

While I reluctantly agree with you (with hindsight) on the 2017, 2018 and 2019 statement. It is hardly something to crow about as a known fact in the same way I wouldn't claim someone was alive and well until the life support machine was removed.

It was a gamble on whether or not Orr would cut at the start of 2019. After the first cut in 2019 though, I would say the chances that they would continue to prop up property to save the economy became more likely as we weren't even in recession. While I wasn't commenting back then, I don't think anyone was predicting interest rates going as low as they did nor as fast as they did. Personally, I wouldn't have taken long term pain for short term gain, but I guess I'm a contrarian for a reason.

Exactly and that the government would intervene and employ the entire country and prevent any business failure while simultaneously creating a ‘cost of living crisis’ by flooding the country with cheap money and massive deficient spending while doing nothing to increase the quantity of goods/services produced (ie creating massive aggregate demand to keep asset , goods and service prices high to avoid deflation at all costs).

We can’t do that every time a recession rocks up on our door - at some point real productivity is the only thing that counts - not printed money.

Pretty sad, RP cannot seem to let my correct August prediction go, still like I said yesterday now is the second best time to look at buying, you have until Christmas.

poor Zwifter.... your predictions in tatters.

I also called August 2023 as the bottom, albeit a fair bit after you Zwifter. I think we may prove to be off by 0.5% by the HPI standard. Im sure RP will be leaping around on the various threads with his usual passive aggressive lol's if that happens. In the meantime he will keep quiet about himself predicting house price crashes on this site since 2015. Or hinting that he wouldn't be surprised if we bottom out at 2012 prices.

I'm looking at the HPI report, the 0.2% gain in the year, the upward trend through August 2023, the downward trend through August 2024.

Mate. Come on, now... the HPI "first bottom", remember last year, March, when all the banks were bleating on about how the bottom is in, buy now! Then the election sugar rush. Where is all that sentiment now? There are a save few who are promoting property across everything investment related I see. FB IP page is a great place to start for sentiment, and it ain't nice.

Printer8, now that you're once again triggered (as are others here), let it be known that I've already owned my wrong call so there's little point in you prattling on. I think it's time we celebrate as a collective that house prices are falling - that's all. It's a given there will always be the selfish holdouts wanting to pull the rungs on the next generation for their own ends. These folk lead really sad lives unable to show empathy for others.

This is a time for celebration!

I think it's time we celebrate as a collective that house prices are falling

On this I would disagree - there is no reason to celebrate because all the same awful settings and policies that enabled the covid blow out (and the blow out of the previous 20+ years) are still sitting there, biding their time, ready to inflate house prices again...3,2,1, ...

Had these falls come from non-accidental lower immigration, an LVT and PAYE tax cuts, then I would indeed be in celebration mode.

Murray Falconer, I see and respect your point. I'm just seeing the positive side of this much needed correction to counter-act the many sad sacks that want to preserve their own nests. If you're like me and bought your house to live in, it's value is very much secondary to the precious family memories created. I see houses are for living in and not speculating on.

Absolutely RP - a decrease is better than an increase. There is still work to be done for our shared goal of houses being thought of as homes rather than investment vehicles to come into fruition.

So RP you agree that this is the time to buy then ? If not when do you predict it will be the best time ? Basically you have to preempt it, you cannot sit back on your high horse looking at past data saying the best time was three months ago. Finding and buying a house takes months, if you started looking tomorrow you may not actually move in until just before Christmas.

We're looking to upgrade from around second quarter of next year to take advantage of the manifesting upper end weakness. We will still have no debt. TD's have served us well and as each day passes there is more house being offered for the same money. Sure we will have to meet the market with our existing dwelling but on a dollar basis, it doesn't appear to be dropping as much as the upper we're now seeking. Just think Zwifter, we may well help someone out of a tight spot!

Posted this yesterday night but thought it was worth reposting

Neighbour selling up. Deceased estate.

Premium suburb. Solid listing. Way lower than 2017 prices.

Looks like it's listed for double the 2005 price. What was the spruiker catch-phrase again? Houses double every 7 or 10 years. How about every 20 years? Doesn't sound quite as good does it?

Changed to asking price of $1.3M, at the peak Homes had it at $2.6M.

2021 CV is $2.1M

50% fall from peak. Woowza.

Also not a leaker. Similar property, similar condition sold in March for $1.95.

It's crashing all right.

And your comparison with the peak ‘value’ on Homes is a nonsense. That platform has no credibility

I know it has no credibility. That's why I'm posting it. People are still referring to Homes and Oneroof values.

Yet you still base your 50% off claim on it. Hmmm.

Correct, people were buying house based on the Homes upper estimate at the peak.

Some people are just stupid, no point in fighting it.

Comparing to peak homes.co.nz price, lol. And almost every deceased estate I've viewed is a run down mess, if you're lucky they just need everything inside refreshed, but quite often they are in need of structural remediation. People in their twilight years don't tend to be on top of maintenance, nor redecorating.

Here we go, the excuses for why it is priced so low start coming. It is so hard to believe that the market is crashing so hard that people cannot even imagine it to be true when they are presented with hard data/facts. Mass delusion.

Have you been thru? Is it tidy inside, not still running a 1970s decor? and structurally sound?

Or is it you who is cherry picking a dunger and trying to pass it as typical.

Its possible that the 7.8% Auckland drop was influenced by "dungers" but statistically unlikely, and REINZ where crowing about a 20% increase in actual sales.

Maybe every "dunger" in Central Auckland sold hence the 14% fall in median price, alternately and worthy of scientific consideration, is that this is the capitulation many saw coming.

No green shoots in the July HPI, feels like the most scorhced earth report I HAVE EVER SEEN, we never had Auckland rise 7.8% in boom times. IMHO its no wonder it was delayed, they would have wanted to make 100% sure this data was correct. I don't see a conspiracy there, its peoples biggest asset and they had a duty to report the truth.

People will make decisions on this data and set reserves etc, it has to be right.

Sigh, this is why the HPI is the gold standard, it adjusts for the type of properties, so a full lot of apartments settling in a month don't skew the figures. But the crash spruikers on here are every bit the cherry pickers they claim the spruikers are.

its this one

https://www.trademe.co.nz/a/property/residential/sale/auckland/north-sh…

the flow smells bad and narrow house good location location location

That does seem a sharp price for the suburb.

Sharp price so far, Bart

Land is 293 sqm. ... [does maths] ... $4,437 per sqm. Developable? Nope. Great house? Nope. Capital gain will be minimal. Location is the only thing going for it.

Devonport ain't going anywhere as the road in and out is a friggin' nightmare that the locals have been arguing about for so long that AT and AC have just about given up.

Oh, and last sale was 2005 for $600k. So according to the "houses double every ten years" nonsense it should be selling for near $2.4 million.

But it will appeal - a lot! - to someone. (Two someone's and who knows.)

Here's another one close by that sold for under a million. CV $2.2M

Not everything is selling 50% below RV. But there are enough now that it seems like a trend. Those paying more are still in the mas delusion phase.

https://homes.co.nz/address/auckland/devonport/4-garden-terrace/norYM

WOW. 2012 Prices are commmmmmming back into fashion!

The biggest property PONZI bust in the world, is right here in little ole NZ.

NZ LEADS THE WORLD AGAIN!

Looks like a good buy to me! Honestly that looks insanely cheap compared to similar cities, not many better locations around than Devonport.

I suspect its the mid - higher end of the market that is struggling the most. Who has a spare $2 mil these days for a fairly average house.

Is it attached or detached? A potential leaker? (Edit - I see you say it isn’t. What’s the era of the house build?)

without knowing these sorts of details the headline figures - which admittedly look bad - don’t mean much

It's a detached villa on a 293m2 site in a premium suburb on the Shore. You can probably easily find it with the info I've posted.

It is not disimilar to half the villas in the suburb. If this one is an outlier then so are the other 50 odd percent of villas.

"on a 293m2 site" - might be related.

The whole suburb is on 293m2 sites. They were selling at over $2M a while ago.

Nothing has changed except that now there are increasingly lots selling at 2017 CV and below. Not all. Some are still paying silly money but it's a prestige suburb that attracts Uber wealthy from NZ and abroad. Money is not really a barrier to many and they will happily pay just to get settled quickly.

Ignore it if you want but from what a I'm seeing there is an increasing number selling well below CV. The property algorithms don't pick them up because the agents hold off posting prices for as long as possible. I believe (and it is a belief) that the only thing still holding up prices in the suburb is a concerted effort by the real estate agents to hide low price sales supported by people in the suburb that don't want their properties to decrease in value. Unfortunately for them more lower priced houses are becoming known and people are getting nervous.

A few years ago, all the conversation revolved around was how much houses were going up. Now the conversation is only with trusted friends and there is quite a bit of concern about both the economy and people's ability to pay for the mortgage following the big reno's.

It feels the same as Ireland and Spain when the bubble deflated.

Yes now I know location that seems like a real bargain. "Sell the car, you can ferry to the city and beyond" - might have to, no off street parking, that is probably part of the reason.

Surely this has to be the bottom!

They are bringing in residents parking scheme, villa's with no off-street parking are top of the list for eligibility. Less than $200 to guarantee you an on-street spot to garage your car, all at the ratepayer's expense.

Parking is not a factor.

3 bed houses in our street have sold recently for $200k less. And we are certainly no Devonport by any means. Even townhouses are selling here for $800k. I wonder if the contagion will spread; if you can buy in Devonport for $1.2 mil, what does that make a house in a bad area of Manurewa worth, $400k? Or is it all about rental yield these days?

I must admit I am a bit gobsmacked by that!

Not for a villa, many in Ponsonby etc on this size. this would suit an elderly parent of someone in devo before going into a home etc

Found it.

Yes that is a sharp price / discount, for sure. Even accounting for the lack of development potential with the small site area and zoning

Jimbo can buy it.

I'm bloody tempted!

The family need the money to pay off their own debt, if any paper loss is taken it will be shared across family members and will still pay off the 6.85% debt the family members have, enabling a better quality of life.

Out she goes, on the market and NOW SELLING screams the auctioneer

They tried auction and negotiation. Now has an asking price. I posted 2 others in close proximity to this one a few months ago and there were all sorts of excuses for why they were selling so low (one sold for $1M under $2.1M CV) e.g. must have been selling to a family member, it was tax dodge, it must have been renoed, etc... They are selling so low because there are no buyers.

If it wasn't for Riverhead, those falls in Rodney district would be much larger.

Thank God for the Bog

In Bog we Trog 🙏

I know right. Someone out that way is going to make a killing...

I wonder if Chris Bishop will front the cameras today? "Look. It's a good start we've made, but it's only a start. As I said recently, we need lower house prices to benefit the wider New Zealand"

Perfect time to do so. Mortgage rates look set to fall, so those imprisoned with their holdings can hang on a bit longer. But I suspect he'll be 'busy' on other things - for some time to come.

Prices need to fall 16% he said - another month of this and we'll be there for Auckland

He is onto something. When they fall 30% he can claim to have smashed his target. Good man

Just my two cents:

One thing to note about the median price chart in the article is that in the late 2010’s before prices shot up dramatically, housing was already overpriced.

Historians have argued that every financial bubble eventually pops.

If our housing bubble continues to deflate and correct according to historical measures, then there’s a long, long way down to go yet.

Spot on!

John Key told us the same in 2007. But after getting elected, that thought seems to have been put to one side. Besides, Max, is a Property Speculator (sorry, Developer) now.

We often forget because it's no longer in living memory, that it was called a housing affordability crisis in 2007 when National were seeking to be elected. When the Auckland average house price was $493k.

https://www.rnz.co.nz/news/political/308084/housing-'challenge'-still-n…'

Politicians mudslinging here

"The answer to that question is yes, because the complete mismanagement of the previous Labour government saw interest rates go to 11 percent so of course it was having a huge impact on affordability," he told the house."

Yip it isn’t being mentioned by anyone here or in the media, but there is the possibility that prices drop another 25% in nominal terms from here.

Not a prediction just a possibility that people should consider if buying/selling. Speculative markets have the tendency to over extend in both directions and as it stands a lot of people are simply expecting a return to normal still everyday now, but not realising the normal we’ve been accustomed to in recent decades is highly unusual in terms of upside price growth in housing above the general rate of inflation.

"...the normal we’ve been accustomed to in recent decades is highly unusual in terms of upside price growth..."

Quite right.

But arguably the thing that been unusual is the sheer amount of Debt the World has created in that timeframe. And as we all know, money has to find a home somewhere. And Assets of all kind have been it. Once it becomes embedded, it's nigh on impossible to remove. And that's what those who create it know and rely on. At the first sign of trouble, what do they do? (1) Lower the Price of Debt (%), then (2) Create even more of it, so the new Debt pays off the Old Debt, leaving asset prices (the collateral) intact - or so they hope.

I have said several times that investors will return as property become cashflow neutral, at about 4.5% and another 20-25% down they will return

Does this take into account new DTIs or just positive cash flow?

true DTIs limit gains which will be taxed... shit its worth just buying BTC here....

Ireland housing collapse 2007-2021 has entered the chat.

People don't perceive that far back. NZ's property bubble has existed since, gulp, 2010!

IMO we should be concerned with the 'everything bubble', a product of economic policy designed to mandate debasing currency and our response to it. Unless we can find a new way of keeping people addicted to debt in a stable manner, I don't see how growth in the manner we have become accustomed to, can continue.

Like every bubble it seems it's either growth or bust. Things either accelerate up, or they crash down. If we need low interest rates to continue our way of life, have things continue to accelerate up... that's a bad sign to me.

That's a $5,870 drop PER DAY.... be a great NZ Herald headline that you will never see.

The biggest monthly drop in Auckland was in its central suburbs, which includes suburbs such as Herne Bay, Ponsonby, Grey Lynn, the CBD, Parnell, St Heliers, Epsom and Remuera, where the median price declined by $182,000 between June and July, dropping from $1,250,000 in June to $1,068,000 in July (-14.6%).

I thought the median price in those areas was much higher. If we consider them 'blue chip' suburbs, those median prices are quite reasonable compared to other major cities in the Anglosphere. Even the lower socio-economic districts of Sydney seem to have median prices around AUD1-1.2 million.

Mind you, in many ways, Aussie is a economic basket case run by a never-ending revolving door of incompetents.

I think you'd be struggling to find a detached house in those suburbs anywhere near those medians. The average may be pulled down by new terraced houses and apartments.

Yes but the suburb has not changed since 2021... but agree there are a lot of grammer zone apartments etc.

Maybe its all dungers.. all the way down

This is a pretty misleading article. The central suburbs are up 13.4% year on year, while Auckland as a whole is down 4%. So the central suburbs are outperforming by a long way.

Just as well Riverhead and Christchurch prices are still rising. I would not be able to sleep otherwise.

Hahah. Gotta say Queenstown lakes continues to defy gravity. Foreign cash and cashed up boomers keeping it pumping. Talked to some people down there last week. Town and vibe dead as a donut though.

When I stepped off the plane and straight into the path of the Real Estate agent, (I reckon they must have spotters at the arrivals gate! ) I asked him "How long will it take me to find a suitable place?" His reply, " I reckon we'll get you something you like at your price by 2:00pm today!". Cool! My next question, "And if I want to sell it, how long might that take?" Reply? "Oh, probably about 18 months".

Queenstown. A viper nest of vested interests today, and worse tomorrow.

You meant flood water?

Will take at least another 1% in mortgage rate reductions before we see this market start to turn around. Foreign offshore buyers banned, First Home Buyer Grant cancelled, DTI commencing etc. Council rates and house insurance have seen huge increases and the recessionary environment with job losses, hours cut back etc resulting in very stretched household budgets. Auckland house market being hit hard and usually it’s a ripple effect - when Auckland tanks its spreads to the smaller cities and provincial areas so expect it to be no different this time. No wonder REINZ delayed this release by 5 days later than usual eh!

Too many bright young people are leaving, they can get better value for their hard earned money elsewhere.

For the kids Oz is heaven. More money, better lifestyle, more interesting careers and cheaper stuff.

Nz has some serious work to do.

For those who don't know, haven't been told, or unable to see it, new lows from their peak REINZ House Price Index:

1) Auckland region: -23.4% nominal; -32.5% inflation adjusted

2) Waitakere: -25.7% nominal; -36.0% inflation adjusted

3) Napier: -21.6% nominal; -31.1% inflation adjusted

4) Carterton: -20.9% nominal; -29.7% inflation adjusted

5) Horowhenua: -22.2% nominal; -31.9% inflation adjusted

6) Kaipara; -17.5% nominal; -26.6% inflation adjusted

7) South Wairarapa; -23.4% nominal; -31.8% inflation adjusted

Remember this is before the impact of leverage. For a 80% LVR buyer at the peak in the above areas, the owner would be in NEGATIVE EQUITY (except for Kaipara) - assuming that the owner has been able to maintain ownership and not under cashflow stress. Would an owner in that situation likely be happy that their equity (and likely lifetime savings) has evaporated in under 3 years?

Also something to note - remember the common, widely held conventional belief that house prices rise in line with inflation?

We traded up at peak 2021 in Masterton. Have lost 20% equity in our current place (according to ANZ/Valocity) and for once homes.co valuation is in line with this valuation (after they dropped it by 35%).

Same with our previous home, an overnight homes.co revaluation downwards of 35% in May this year. Which suggests homes.co (as we all probably know) have been applying at least a 10 - 15% adder to property values.

Hi CN, love your great stats! You should give the Herald a ring and advises them on creating some good, informed media.

What past date did you account for the inflation losses?

I see that from late 2020/early 2021, it is listed as around 19% accumulated inflation loss, to now.

1) You should give the Herald a ring and advises them on creating some good, informed media

They have their own agenda, and vested financial self interests.

2) What past date did you account for the inflation losses?

Each region had different months for their peak REINZ HPI value. Used the peak value and the number of months since the peak.

Inflation adjustment here.

https://www.rbnz.govt.nz/monetary-policy/about-monetary-policy/inflatio…

Used a monthly rate for above calculations.

Love your work, CN. Keep it up.

(I feel the need to re-post about why zoning changes are going to keep the fall going for some time ... But I won't bore people with it this time.)

Not much on The Herald or Stuff, maybe they report on it in 5 days time, so funny why so many do not trust the media any more.

Meanwhile headlines around pretend banking competition changes.

Delay, delay, delay.

Creative speculation needs time to marinate.

Something looks very 'massaged' about this month's HPI values. Auckland City HPI in June (last months release) was 3111, this month it is 3006: a -3.38% monthly decrease, not a -2.7% decrease as shown in this months summary table in this article.

Looks like they've noticed your comment, and changed it to 3.38%.

This is a disastrous result for the property development sector. It will make developers even more nervous about developing. And it will make lenders more nervous about lending.

I keep banging on about this as many people don’t get how the two are tied together. The Development sector, both land and building is dead. And absolutely f**ked.

Until development feasibilities start to work there will be very limited construction activity. Declining house values are going to make any form of recovery so much harder.

it’s a downward spiral and as more have no work, they get forever to sell… and round and round we go.

Exactly. Developers tend to go gangbusters when prices are booming ie. 2021-2022 (and refer back to 2002-2006). The reason is simple - there’s every chance they will make more profit.

The opposite forces are in play when prices are falling -ie. if I start building now, prices might be even lower, or….. they might eventually rise a little by the time the development is complete but does that give enough risk contingency given everything is so tight?

My prediction of a 40% fall in consents, and more importantly dwelling completions, might he too low. Might be more like 50-60%. Keeping in mind that Kainga Ora is pulling back massively as are retirement villages

Now would be the time for Kainga Ora to pick up the private sector slack after spending a few years building up their capability and resourcing. Unfortunately coalition of chaos just revoked their mandate to build state housing and sacked the people who know how to do it. Clowns.

Well said.

This exactly the right time for Kainga Ora to get stuck in. (And for Kiwibuild to have started.)

The govt has an incredible knack of buying or building at the peak and selling when the market has crashed.

The next 12 to 24 months will be the best time for KO to buy up teardowns and land from belly up developers and then start pumping out state houses (fully insulated, 50+ yr cladding, double glazing) all over the country.

They won't. In much the same way as the Nats cut contributions to Super, at the time markets were at an ebb and missed the opportunity to ride the rise, they will do nothing wise this opportunity either.

"Developers tend to go gangbusters when prices are booming ie. 2021-2022 (and refer back to 2002-2006). The reason is simple - there’s every chance they will make more profit. "

Do many developers recycle all their profits and equity from previously completed projects into larger and larger projects due to the attraction & pursuit of larger profits (in absolute dollar terms)?

Usually, it's an addiction for them. Most eventually go bust.

And you know this, how?

.

I can't speak for 'many', but no, most established players don't.

They have a target size, and market, and generally stick to it. That minimizes risk, while leveraging their core competences.

(Just quietly, many established builders & developers have kept their powder dry since the RBNZ started the 'crazy'. A few too many Johnny Come Lately were throwing money around to be sustainable. The RBNZ has much to answer for.)

edit: Sorry CN. Because you asked, I feel obliged to give a better answer. A buyer may look at a dwelling and say it's 100 sqm. We look at the cost. Cheap land = cheap build. A cheap build requires a different skill set. Expensive land = expensive build. And a different skill set. A stand alone house on its own section is the easiest. But - and this is a big but - only if the service connections (water, sewage, electricity, etc) are in place - and sufficient capacity is available. (And not so aged that it becomes a problem on its own.) If the connections aren't great, risks go up - a lot! In fill housing - also not too bad, risk wise, but unless you own, and will keep the dwelling, not a huge amount but good for keeping people busy. Terraced houses. Again, connections - they need to be good. But they cost a lot more to build. Tons more things like sound, fire, strength to consider and price in. They cost more. Apartments are a big step up. If they're built from sticks (US for standard timber), the cost is less but still more expensive due to fire, sound, engineering, etc. Sticks - with engineering - gets to 3-4 floors in NZ. Using concrete or steel for the base stories can get you higher but again, but the cost goes up due to multiple materials, trades, engineering, etc. Mass timber (glulam technologies are in their infancy in NZ) cost a bit more but you get speed and therefore less bank profits. NZ should be doing more mass timber - in fact we should be world leading - but, as always, risk stops many. Once you get bigger than 3 or 4 stories, its a whole new game again. You have to build completely differently. Planning and project management are crucial. As is site investigation - i.e. extremely thorough geotech work that costs heaps - think machine bore holes to 20m, 40m depending on the ground - a stand alone house seldom needs more than a 3m hand bore. And selling apartments? Yeah, well, Kiwi parochialism makes this hard (but this will change as more kiwis actually live in apartments - rather than spout off in ignorance - and find they're fine, if not better.) Hope this helps. The key concept I'm trying to convey is that they're very different. Staying within one's lane is safe. And that's what most real developers & builders want - to be around for the next cycle.

"A few too many Johnny Come Lately were throwing money around to be sustainable."

This is the second time around for Kenyon Clarke of DuVal?

Is this the rise and fall and rise and fall ( .. and rise?)

We all know who is living on the edge.

ChrisOfNoFame,

Thank you very much for your comprehensive response.

Yes 100% and they carry massive amounts of debt chasing those oversized profits.

They think that because they made 30% profit on a 3 townhouse development, that they will make 30% on a 30 townhouse development, if successful they will up the ante again and do 3 X 30 townhouse developments. This cycle continues until a recession happens and all their companies go bankrupt.

"I keep banging on about this as many people don’t get how the two are tied together. "

Far less tied together than you seem to think.

Thanks to the RBNZ's 'free money' program, many new entrants with dollar signs in their eyes, will exit, licking their wounds.

But for others, the game never stops.

Yip and each time prices fall the equity of investors (with debt) falls. When prices were rising investors continued to increase equity allowing more investment - the feedback loop is now reversed but was always a significant risk given how overinflated everything got.

"This is a disastrous result for the property development sector."

For the less well capitalized, sure.

But for many who have been at it for a while, nothing new, and we plough on (squeezing the gouging suppliers as we go).

So as a developer, how do you view things and how do you play things from here?

At this point I try to make sure I've finished property to sell when things turn around for buyers.

And hold off on commencement of new? Or plow on with another project, assuming price declines will cease, interest rates will fall significantly, and hence demand returns?

That's why you are shit at predicting HM, you see the problem but predict Oct is bottom with slight up from there... FFS

I like your views as a here and now call but you are shit at understanding wider impacts delayed impacts etc etc.

re developers, they are f ed, they will not raise the funds, the holding costs will kill them and asset prices will plummet, they will be forced out at the bottom as always, failing developers produce some of the BEST BUYS , stay close and be ruthless. Don't care if it has foundations on it, if you get at good land cost.

Pardon me? Where did that come from…

I was putting that to Chris as something he might be thinking of (I know some developers are looking at doing this), it’s not what I think at all…

You might see that at the top of the thread I effectively called the development sector as totally screwed

I have made a note of your comment rubbishing my October call. You might be right. You may not be. Let’s see

I've been 100% idle for quite a while, thanks to RBNZ foolishness, but got going again recently. 18 months from now I'll have finished some. Mix of major reno and new. I'm not "assuming price declines will cease, interest rates will fall significantly, and hence demand returns". They're just inevitable facts. Part of the economic cycle. The only question is whether I'll meet my target ROI. 99% sure of breaking even. Anything more is a bonus. I've created something that doesn't currently exist. And that makes me feel good. Building (creating new stuff), as you know, gives a nice warm glow for quite a time. Loved (and still do) designing systems & writing code for much the same reason. Still learning. And getting better? Yes. I think I am. At least I hope so.

"This is a disastrous result for the property development sector."

There will be projects that were started several years ago where developers were working on 2020 - 2021 sales prices. Had costs remain unchanged, the projects would be profitable.

Many of those long term development projects (e.g apartments, land development) may now be unprofitable at current lower price levels and furthermore costs have increased due to supply chain disruptions, inflation and interest rates. For those apartments that presold, developers may be selling at a significantly reduced margin (or even at a loss). Some of the off the plan buyers may now have insufficient financing due to lower market valuations and lower lending amounts by lenders. Have already seen some off the plan buyers try to sell before settlement date.

Property developers are unwilling to cut their prices, meaning that prices in the existing house market may be more appealing to buyers now.

What other key challenges are developers facing in different residential related property products?

E.g townhouse, apartment, land / sections

Issues concerning cost of land, timeliness of approvals, council development charges, availability of financing, difficulty in achieving pre-sales, raw material shortages, labour shortages, reintroduction of interest deductibility has made existing dwelling purchases by non owner occupiers more compelling than new builds, other?

So after all the hikes to absolute peak OCR, economy in recession and all the talk of people leaving the country my area North Shore is only down - 1.5% for the year? Can’t be right.

North Shore is only down - 1.5% for the year?

What REINZ isn't telling you (and likely don't want you to know as they aren't publishing the statistics publicly and keeping the public in the dark / uninformed as it doesn't suit their vested financial self interest);

North Shore REINZ House Price Index from peak: -20.0% nominal; -29.5% inflation adjusted

What are you talking about “aren’t publishing” “in the dark” they are publishing an annual rate which is -1.5%. Even after all those factors I mentioned. I, like most people didn’t buy at peak so why is that relevant.

They aren't publishing the house price fall from the peak.

The fall from the peak is relevant for those determining the magnitude of the asset price bubble. The high water mark is used. It also impacts buyer expectations of house prices.

How would it affect a potential buyer's confidence of an average buyer, if they knew that house prices had

1) fallen 20.0% from the peak,

2) fallen 29.5% in inflation terms from the peak

3) And that house price momentum is continuing to trend downwards?

That is likely to result in fewer potential buyers who are active in the market. Those numbers are likely to influence the house price expectations of potential buyers and their offers (increased likelihood of low ball offers).

Compare the impact on a potential buyers confidence and house price expectations if they did not know the above data and only knew the following data. House prices

1) have fallen 1.5% from last year

2) have fallen 1.7% from 3 months ago

3) have fallen 1.6% from last month

These are the numbers provided by REINZ in the above table. Potential buyers might conclude that prices have stabilised and have increased confidence to buy at the vendor's asking price (which suits the vested financial interests of the members of REINZ as there is a transaction).

Price trends matter and are extremely influential to the confidence and house price expectations of most potential buyers.

If potential buyers expect house prices to fall, many will either wait or make low ball offers.

What if these were the most recently reported numbers for the North Shore:

1) REINZ house price index: +1.2% vs last month

2) REINZ house price index: +7.6% in last 3 months

3) REINZ house price index: +23.8% vs last year

How would that influence the house price expectations of potential buyers under those conditions?

This caused a massive fear of missing out (aka FOMO) by potential owner occupier buyers, property traders, and raised selling price expectations by property developers.

https://www.interest.co.nz/property/113767/apart-few-soft-spots-housing…

I'm sad but delighted. I sold and bought in March. Im sad because 1.9m house I bought is likely worth 1.75 based on the homes selling my road. My paper wealth feels less :-(

But I'm happy because my 23 year old work colleague is now starting to feel hopeful that she might be able to get a home in the future. She's re-thinking moving to Australia. This correction needed to happen. Its been hamstring everything. Too much interest paid to the banks, Too much rent being paid to landlords, all sucking the life out of our economy and making us more and more dependent on credit.

Wages in NZ have gone up a lot for some industries, to a situation where many are comparable to Australia. We were able to increase my colleagues wages from 75 to 85k + 10k Bonus over the last year which puts her at a similar level to Marketing Exec (think marketing assistant) and prices in auckland are starting to approach some normalcy. Need that Median price to get down below 850k.

Coatesville up 40.7% and Riverhead up 3% in the last 12 months.

It's not all gloom and despondency.

Riverhead is also down 21% since January. Refer yellow line in the suburb trend graph.

https://www.realestate.co.nz/insights/auckland/rodney/riverhead

If you expand that same graph out to 3 years median had dropped from $1.7M to $1.2M!

If it's down 21%, then it must have been up 24% before January...right? It's still up, while everyone here is predicting real estate hell.

https://www.realestate.co.nz/insights/auckland/rodney/riverhead

its merely a flesh wound

I mean, the latest average sell price is the lowest in the last 3 years ($60k lower than July 2021).

But if you want to celebrate the gains of the last 10 years you can switch the graph to 10 year and enjoy the "moving average smoothing" of the chart. They're not your gains though, because you claim to have bought in 2022 or 2023 which was effectively Riverhead peak and the values clearly have declined since then.

some good discounted prices to be found.

Let us know the details when you buy one.

All Rookie no Investor .....

If you put a ruler on the graph it looks like house prices are now where we would be if there had been no COVID madness. We could have reached the bottom.

It was a bubble before COVID.

LOL. We weren't in a recession pre-covid while trade with our major trading partners was humming along.