Fewer residential properties were sent to auction last week and prices remained weak but the sales rate picked up a bit.

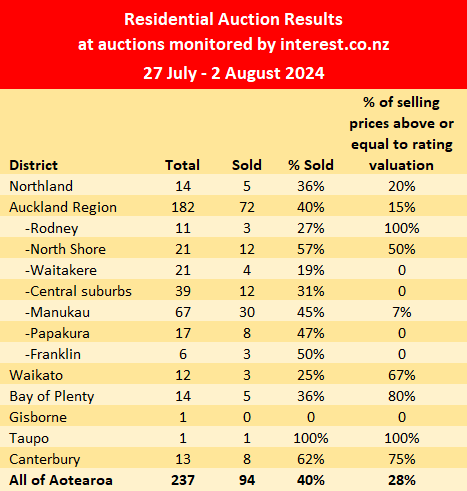

Interest.co.nz monitored the auctions of 237 properties around the country last week (27 July - 2 August), down from 265 the previous week, but up from 212 the week before that.

Auction numbers have been under 300 a week for most of winter and have been bouncing along the bottom in the low to mid-200s for the last few weeks.

However the sales rate showed a slight improvement last week, with 94 properties selling under the hammer, giving an overall sales rate of 40%, up from 34% the previous week and 31% the week before that.

That was the first time the sales rate has hit 40% or more since the beginning of February.

However prices appeared soft, with just 28% of the properties that sold fetching prices equal to or above their corresponding rating valuations, which was a five month low.

The latest figures are broadly in line with other data such as Realestate.co.nz's monthly data for July and Barfoot & Thompson's July sales figures, which suggest asking prices are declining as vendors become more realistic in their price expectations, which is prompting a lift in sales.

The chart below shows the sales results by district around the country, and details of the individual properties offered at all of the auctions monitored by interest.co.nz, including the selling prices of those that sold, are available on our Residential Auction Results page.

- The comment stream on this story is now closed.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

30 Comments

More time constrained vendors meeting buyer's offers?

FONGO will define the rest of the year..

Debt is going to seem like devil's paradise.. with only a few daring to enter..

Fear Of Not Getting Out [of property]?

Underlying demand for property is strong.

Assuming interest rates continue to fall, let's watch their impact on the market.......

TTP

"Underlying demand for property is strong."

What do you base that on? Seems to be a lot more supply of houses for sale these days than demand

What do you base that on?

You'll soon find out as interest rates fall.

TTP

You'll soon find out as interest rates fall.

Is this another one of those "watch this space" Spruiker posts? We've hashed that one out on here already (chuckle)

Eventually house prices will rise - sure. As we already know Spruikers are a truly impatient bunch. The recovery won't happen soon or in such a way as they wish. It's almost as if the vested are so focused on themselves they unwittingly trivialize the financial and emotional suffering of others out there....

Pull the other leg, Poppy.

You know very well that I don’t support interest rate drops at this point - after the multitude of my posts here on the topic.

I’m very much in the “higher for longer” camp, as I believe that those who have got themselves over-indebted need to learn a hard lesson. But RBNZ makes the interest rate decisions - not me.

You ought to be brave and honest - instead of misrepresenting the truth all the time.

TTP

You ought to be brave and honest

The irony in you of all people posting that. Bloody hilarious! Back in the day, you would have been exported to a colony on the Australian mainland.

His bad language and shouting shows that Poppy is as guilty as sin - and arrogant with it.

TTP

Why is it that every time you question the integrity and honesty of others, I burst into uncontrollable fits of laughter. Can you help answer that? It only seems to happen with you.....

Also upvoting oneself speaks volumes.

🤡

huge demand 20% below current asking prices.

Ill raise you another 10

underlying demand for methods of tax free capital gains is strong. whether property still meets this description is the key

The last 5 years have been an interesting rollercoaster ride however, I think we have nearly completed the ride and the slow rise back up for the next ride is upon us.

Mypointis | 6th Aug 24, 10:46am - The last 5 years have been an interesting rollercoaster ride

Are you feeling a little giddy?

Way too optimistic.

I'd be surprised if we see a bottom before 12 months.

(But if the RBNZ is forced to drop the OCR below the neutral rate - about 2.5% - then all bets are off.)

I think it's brave to assume the success rate will still be 40% or more post the usual spring listing surge. There's a lot of flood waters yet to pass under the bridge before a sustainable bottom can be called.

Note 28% at or above RV. Not sure that helps determine true value of any sort given it’s a number places across the housing market that was greatly overvalued and inflated around September 2021. Just thinking about FHB and how best they can navigate the next year or 2. If we relate any value towards the RV what the likely impact when the new updated RV are issued in Auckland, I believe towards the end of this year. I’m just thinking aloud, FHB buys something 50k below current RV thinking they have secured a level of fair value and 3 to 6 months later is removed with a new updated RV. thoughts on any impact?

Not sure if this answers your question: In leafy central auckland suburbs, for 3+ bed fully detached houses, sales prices are rapidly approaching 2017 CV. Currently the median is around 105% of 2017CV (excludes new builds and houses with significant renovations or improvements such as a pool)

The way I think about it is, 2021 CVs were massively inflated by the explosion in value of land as a potential development site. Now that demand has evaporated.

I think it's brave to assume......

Poppy talking about bravery...... Whatever next⁉️

The property market is not set to take off with those rate cuts. Seems like the lag effects, rising unemployment, and an increase in bankruptcies from a deep recession are being discounted. Over the next one to two years, if not more, we might just see this play out. Plenty of businesses and households will probably be more focused on sorting out their finances than jumping into buying properties (balance sheet recession).

This is going to hit different folks in different ways. Those with dry powder will find plenty of assets up for grabs on sale. People loaded up with debt will be busy trying to get their finances in order. For those with heaps of debt and no job, they will find themselves forced to sell to the first group.

How refreshing to read a good, well-balanced post! Well done EL.

Could the increase in the number of sales be due to the reduction of the Brightline test, to two years from the 1st of July ? It's hard to tell, I think if the higher numbers of sales and clearance around 40% hold up in August, it could be a sign that it is so.

Been alot of changes taking place in July - tax rules relaxed (interest deductability, 2 year brightline), LVR rules relaxed (investment properties + low deposit lending), CCCFA relaxed (less checks required to be made by banks), Interest rates down and further falling... as I've been saying, it will be interesting to see what impact this has on the market.

Depends where ya live or have an investment.

https://www.realestate.co.nz/insights/auckland/rodney/coatesville

Buy in Coatesville, or nearby. It's up 40.7% in the last year.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.