Asking prices for residential properties are sinking like stones, as vendors bite the bullet and become more realistic in their price expectations.

The average asking price on property website Realestate.co.nz has fallen for five consecutive months, to $816,797 in July from $927,312 in February .

That's a decline of $110,515, or 11.9%, over the last five months.

In the Auckland region, which is by far the largest real estate market in the country, the average asking price has dropped $142,857, or 12.8%, over the same period, falling to $976,928 in July from $1,119,785 in February.

July marked the first time since August 2020 the average asking price in Auckland has been below $1 million.

This suggests vendors are finally starting to realise the inflated valuations prevalent during the last brief boom in 2021/22 are no longer relevant, and they need to adjust their price expectations significantly downwards if they are to make a sale in the current subdued market.

However falling asking prices aren't the only thing in buyers' favour at the moment.

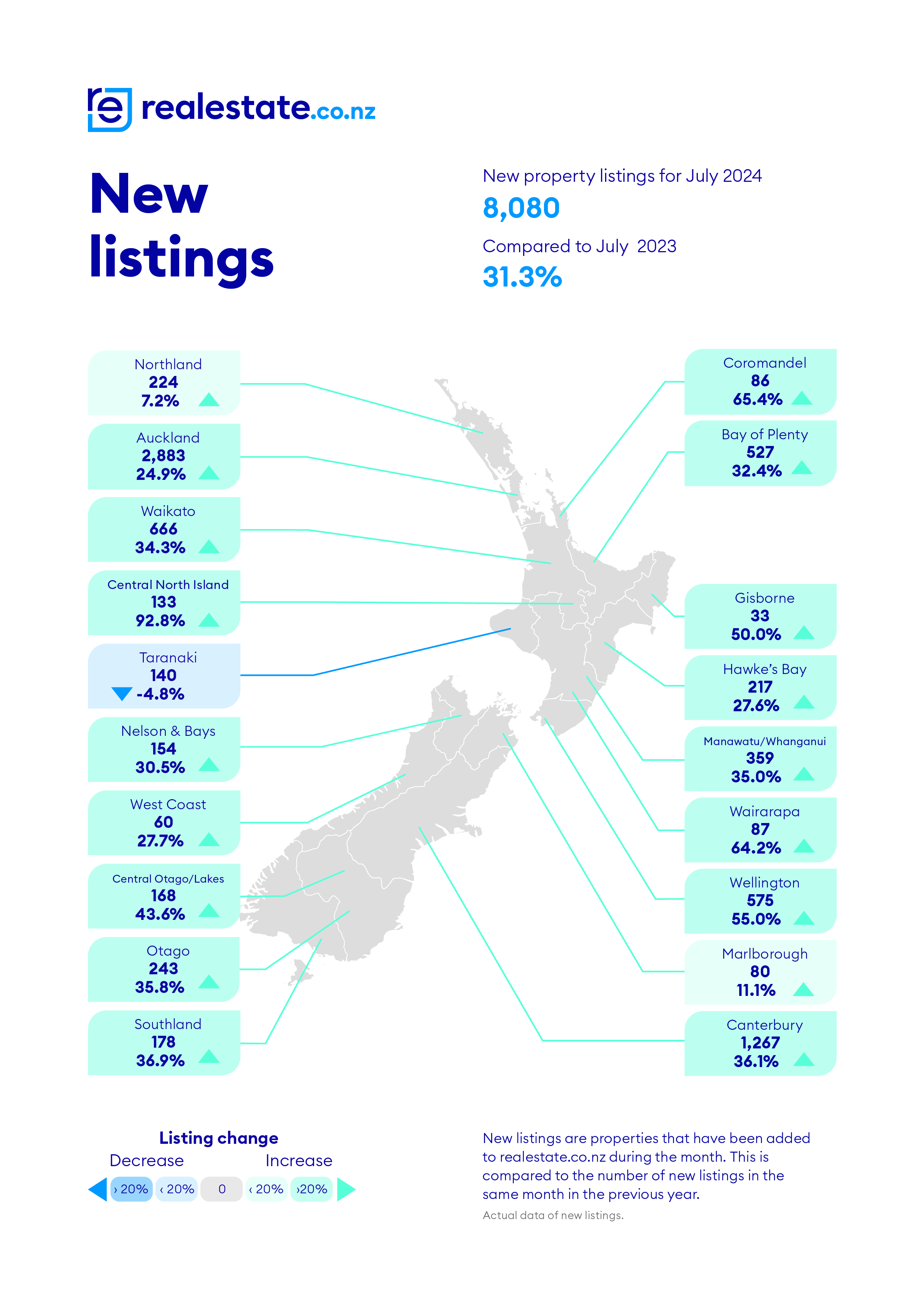

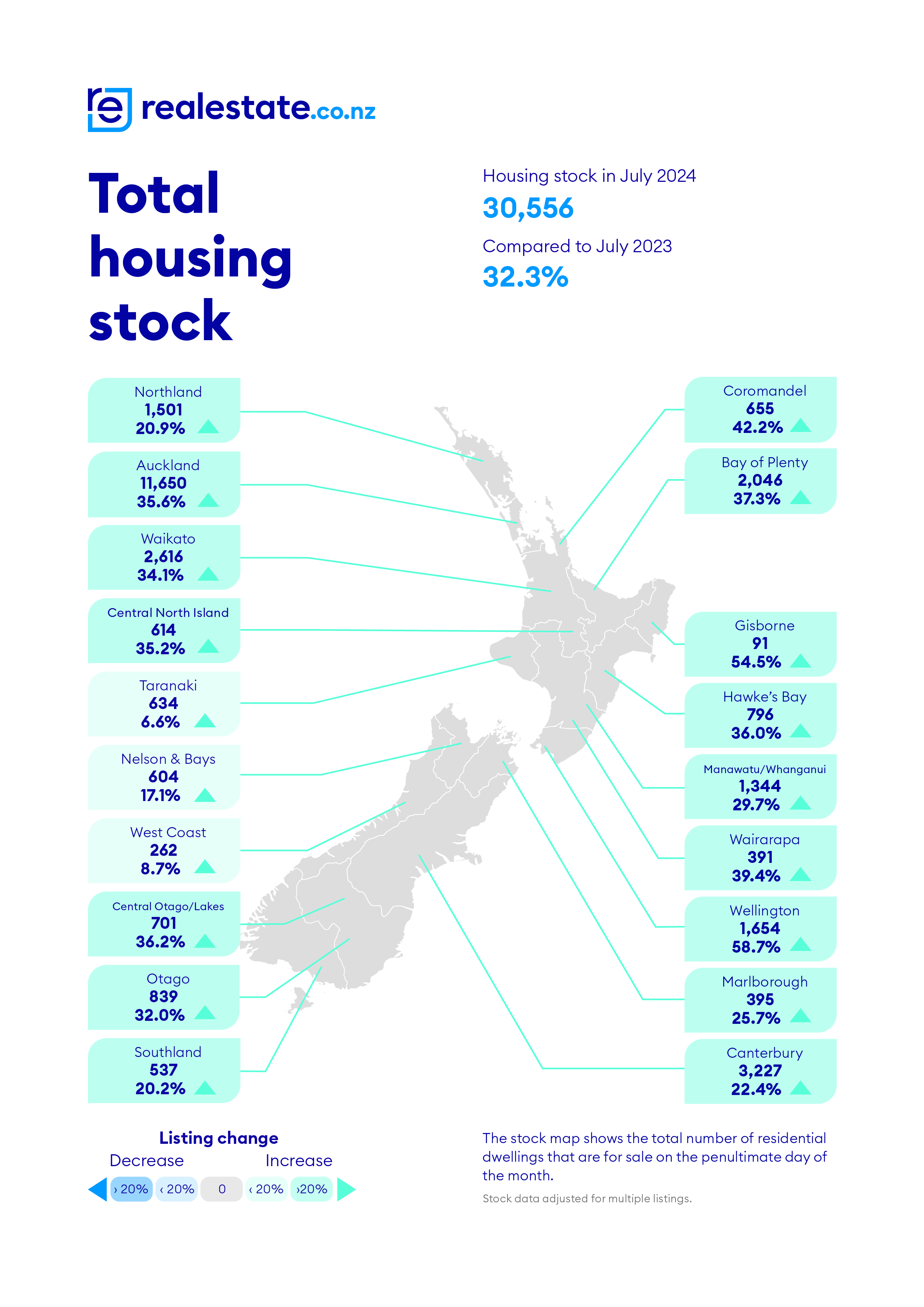

New listings and the total stock available for sale on Realestate.co.nz are both running at unusually high levels at what should be the quietest time of the year for the real estate market outside of the Christmas/New Year break.

The total number of homes for sale on the website in July was up 32.3% compared to July last year, while new listings received in July rose 31.3% for the same period.

So there is still a flood of properties coming onto the market.

"Buyers have ample choice and time to decide," Realestate.co.nz CEO Sarah Wood said.

"But this will be a competitive market for many sellers - they should research local market trends and be prepared to negotiate to meet the market," she said.

- The comment stream on this story is now closed.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

169 Comments

The worst is yet to come.

The snowball grows....

At current prices, the exit door is still very small.

Dragging the Evil with them..

Just as well there are tax cuts....

Funny, one Spruiker recently implied latest changes to CCCFA would be a game changer unleashing a tide of cheap money to all and sundry. In anticipation of this epic event, why are vendors drastically reducing their asking prices?

What spruiker said that Poopy? Please add their full quote...it'd be interesting to see if you're interpreting things right as a DGM...

by Nifty1 | 25th Jul 24, 12:01pm

Don't worry, the Government are making changes to save the day... including CCCFA adjustments to make it alot easier for banks to approve loans...watch this space.

by Nifty1 | 25th Jul 24, 5:49pm

I think you'll find what I've said is facts on what's happening - due to role out 31/07/24 that will impact bank lending. I've mentioned previously the other changes the Govt and RBNZ are implementing this month which will have an impact in the coming months.

Why do you keep editing your original comment? Next you'll be accusing others of misinterpreting?

Some might call it back-peddling.

Nice can you find my quote of the other changes that took place in July...

I still can't see a reference to banks 'unleashing a tide of cheap money to all and sundry' nor that it would immediately impact asking prices...

It was an observation that Government & RBNZ are once again doing what they can to support the property market when it is down and it will have an impact going forward... a hard concept for some to understand or simply DGM wanting to dismiss it.

It looks like it is you who is Pee-fty in the end.

Haha Poppy came with the receipts, you really walked into that one…..

Ouch.

Just like many spruikers seem to believe atmsopheric pressure and moon phases can be positive signs for the Real Estate industry! Modern day snake oil salesmen.

😂😂😂😂😂

I'm still trying to decide what I'll do with the extra 0.5%, maybe put it on my 21.8% council rates increase.

I admire the change in your thinking over the past 2-3 years on the housing market, Yvil. From a real spruiker- you can never lose with property! - to someone who is much more objective and balanced on this issue

Agreed.

Almost none of the (very few) property investors on here are spuikers, that's just an intellectually lazy slur and I really don't care what you or others do with your money, it's none of my business. Most detractors come from a moral point of view rather than performance. There are spivs in the property industry no different to stock market, crypto etc etc. Property goes in cycles like every asset class amd will be back. I still prefer it over all other asset classes through the cycle due to the leverage and tax benefits.

Disagree, there’s several that are very much spruikers

Reckon there's many DGMs here HM?

Yep

and just like the spruikers there’s a spectrum of views, from end of the world nonsense (10% interest rates by Xmas) to more moderate and well reasoned doom and gloom

Just depends for how long it lasts

Thanks HM.

Property remains a top longer-term investment, as I’ve mentioned here many times.

The name of the game now is “pick the trough”. Those who adopt a countercyclical approach stand to do well from the current market conditions - reaping gains from rental yield as well as capital appreciation.

Nice for some - and even nicer for them in the future……

TTP

Timing the market is a fool’s game. Follow the fundamentals. (The fundamentals don’t look good.)

Should I sit back and wait, even if the right property comes along. Then compete harder with more bidders later??

It's pooperty according to IT GUY who is sitting on a 16hec $3m place he is hoping to convert to residential oneday, buying and selling horses in the meantime.

It will never be residential, just a couple of LSBs.

Property as a good investment is largely a thing of the past.

That's big call HM. I'm in my 50's, so I have seen a few cycles in the past. It's surprising how many people are short sighted. When there's a bull run, many people think it will never end, now that we're in a bear market, also many people think it will never end. IMO, both are foolish expectations.

No real change in the number for sale in the BOP. I have been monitoring Trade Me for 5 years now, total listings only fractionally higher than I have seen it in the past.

Ah yes nothing could happen to your precious TGA!!!

Developer puts up all 5 properties for sale at the same time in this development.

https://www.oneroof.co.nz/news/latest-news/south-auckland-developer-put…

Are they under time pressure from their lender?

I've seen many of these.

The trickle of new builds being listed for sale in Jack Point is turning into a grade 2 rapid. $2.8m asking for a $500k build, there is going to be some hefty discounts I'd imagine.

Yeah Qtwn will be interesting to watch. The last few years the market has seemed to defy gravity largely due to aussies and jaffas pouring in.

I've heard the AirBnB market in Qtown is dead. Which is surprising, as while its well known the AirBnB market is gone dead NZ wide, I would have thought Qtown would be more resilient. Especially since its ski season. But I guess even the top end of town is feeling the pinch. The problem though is that a lot of places down there were built as Home & Incomes, especially in places like Jacks Point, with a wee 1-2 bedroom attached flat that the owners depended on being able to rent out in order to pay their million dollar mortgages. No AirBnB = forced sale.

Those flats cant be rented out to long term tenants either, as Labour banned the renting of granny flats unless they were legally seperate dwellings, and most of them are not. If National wanted to fix the rental market overnight, simply undoing that ban would be extremely helpful. That would release a flood of small flats on to the market overnight.

Interesting, thanks. Jacks Point is like Wanaka, rapid growth of cookie cutter new builds and there seems to be a lot hitting the market. If the rental market isn't healthy then a 1% cut in the OCR isn't helping anybody and buyers will need to be found.

Haha of course the obligatory Ford Ranger out in the garage !

Two million to live in a dormitory suburb. You might as well be in Lower Hutt.

I feel sorry for anyone hitching their fortunes to that dumpster fire of a platform. They have a quality control issue with miserable hosts. I’m not doing your list of chores and paying a cleaning fee. I’m just stay in a hotel thanks.

Yes exactly this! Hosts who don't realise they are in the service industry. Think they can make the same daily rate as a hotel and expect there to be absolutely no trace that their batch has ever been used.

They can still be rented out. Just call your tenant a boarder.

Just wait until Auckland people receive their new CVs while paying more for rates.

And elsewhere....

RV's in our area down 12.9%; rates courtesy of this morning's Inbox, up a nominal 7%.

what area are you in, please bw?

Would be a magical moment.. suckers for punishment

Toye .....had a conversation with someone yesterday about that ...they were pissed !!!

I can see a movement brewing where the Auckland Mayor is going to be absolutely inundated with howls and screams of disgusted ratepayers ...and it's going to be way too much for him and the Council to handle .....wonder what he will say to all this, when he has been banging on about Council and all and sundry cutting back on costs !

I have always said this country lives way beyond its means ....

Wellington valuations due next month, I'm expecting a chunky 25% drop. No biggie, it was never worth the 2021 RV.

I just got my Christchurch rates assessment. $9,280. That amount would get me 5* resort facilities in a luxury apartment building on the Gold Coast.

(For those that think I must live in some Fendalton mansion, I don't. This gets you a 2016 built 4 bedroom home on a 500 sqm section in a decent suburb with a median sale price of $725,000).

What? That's simply outrageous. So what would the rates be on a $5m property in Fendalton?

Having said that, rates and insurance on a property just let are $200 p/w combines so you must be up around $250 p/w for that.

Well, a $1.9m place in Fendalton is just over $10k in combined rates, so $5m would be about 2.5x that. Call it $500/week in rates.

Would I be right in guessing that'd be another $100/ week in insurance in the shaky city?

Just to make myself feel better, I checked what the rates are on a mansion in Fendalton lol. $43,022.

That makes AKL rates look cheap, I pay about 5.4k on a just under 3mil rv, commercial ACC rates are a rort.... much much much higher

Keep in mind Christchurch rates include rubbish collection and water, where-as Auckland doesn't, as far as I am aware?

Auckland City includes rubbish. North shore doesn't. None include water.

Pretty much an identical house here in Tauranga but worth more like $1M, the rates are $3300

Weird how you mentioned everything except the ratable value of your place.

I just looked up a random property in CHCH and it was $3.5k rates for a $600k place. Seems about right?

Mine is about $4k for a CV of $750k. As mentioned elsewhere, this is all-in, no additional water or other fees except for very heavy water users.

Yes, how dare I live in a good school zone. I should immediately sell up and move to Aranui and learn to shoplift.

No need to get defensive, but obviously the value of your home plays into any discussion of rates.

Not sure where your numbers are coming from...my parents 700k home was only rated at $3800 per annum...bad enough but a long way from your claim

Correction..have just checked latest info...CV of $770k and annual rates 2024 of $4550pa

I would take what K.W. says with a grain of salt, based on past comments.

That seems steep. What area? We're in Halswell. RV 1.2m and rates 6.8k

Think you are having us on a bit KW.

You do not pay anything like $9k rates on a 750k property in Chch.

Our RV is over $1m and we are paying over $5k per annum

The housing market is now starting to buckle under it's own weight.. tighter the noose gets by the day

Spec leverage looking like it turning into phosphorus exposed to atmosphere. Burn, white hot baby.

My -10% Dec 23 to Dec 24 is starting to look like a TAB Unders / Overs bet, there could be some really big price movements as this overhanging stock clears in summer. If the clearance rate does not lift the market is in very serious trouble.

I thought it was way overpriced before Covid came along

The market's been overpriced since the early 2010's.

Happy to confess I was wrong on the robustness of the Auckland market. If the average asking price is 950k and the current median is 1m, we can expect at least a 100k drop between now and Christmas.

Agree, asking prices are a leading indicator to the coming larger drops.

Welcome to the team.

The current prices paid are a reflection of vendors not dropping price, hence so little is actually selling. There will be a step down to the current offer level over summer. We could easily see a -3% or -4% month soon. Nothing will have changed except the vendors finally taking current offers. Buyers are tryers and will lower offers as well, like all markets at each level the weak hands have to be shaken out. Its only once weak hands , retiring ,downsizing vendors are meet in equal number by new buyers will we see the final valley shaped bottom, it will feel dead for ages.

Yep

There’s a decent chance that TA’s +10% 2024 prediction will be 15-20% out. Ouch!!!

Yeah but TA is a laughing stock. His reputation is in the toilet.

OneWoof still publishes article from him

’nuff said…

Act now, the market is about to start rising! All go in 2025!

AI Chatbot?

No AI is smarter then that, its a real person

When's that RookieInvestor chap going to say something similar? Eerily quiet now

Well, he’s a ‘rookie’ after all

making rookie errors

He made the right call and left the chat. I think he got sick of banging his head against the wall and just moved on. Cannot blame him really, there are literally thousands of FHB every month and they don't need to waste their time on here.

FHB with plenty of time to waste on here right now, buying power for us is rapidly increasing. So I'll keep an eye on things, and see when the drops taper off, all the while saving a larger deposit.

Thanks to intrest.co.nz for a place where I can get clear, factual, figures backed information without the spin.

Also 1st home buyer, sat on a 300k deposit, growing every month while prices decline. Definitely in no hurry to buy, and the platitudes of yesteryear still being spewed out by unscrupulous spruikers are laughable!

FHB here also.

No debt….large deposit…ample time.

With falling prices, increased supply and market adjustments there’s no rush.

I recommend to many fhb’s that they follow int.co. Foolish to follow msm.

See it in my area of Auckland!!

Property down the street sold late 2023........now they are 150K down the Karzi, if they resold it today.

These current and future losses will, will without doubt be financial WMDs for the NZ economy. Banks stable???

We are amidst massive losses being racked up currently and this will continue downwards for at least another 2+years as the economy deteriorates further.......forced liquidations will see eyewatering pain.

Bag holders will not just burn their hands, we are talking hands being blown to pieces and a financial abomination!

These current and future losses will, will without doubt be financial WMDs for the NZ economy. Banks stable??

According to the central bank, the commercial banks are stable as. But that doesn't really matter anyway. Taxpayer is backstopping them.

Remember that the Funding for Lending program was there supposedly as an "investment in NZ", not for the banks to issue debt on existing housing stock as if no price is too high.

Nobody holds the ruling elite to account. The sheeple are left to their own devices during these periods of extreme exuberance.

All banks will always be stable, until they're not.

It the aussie owners have a way to ask for a bail out from Nz givt rather than take losses. They will.

No way in hell should the NZ govt bailout the Aussie-owned banks unless it comes alongside significant nationalisation. Australia got to take money out of NZ in the good times, now they get to deal with the shit in the bad.

Agree. Interesting thing will be that our economy would be beholden to them.

by Averageman | 2nd Aug 24, 10:07am

Spec leverage looking like it turning into phosphorus exposed to atmosphere. Burn baby burn, white hot.

Must admit I am feeling the heat cashflow is a real problem - anyway lets see. This message is keeping me motivated - if interest rates come back to 5.5 by March i will survive if not there goes the family house. I feel by DGM standards here I am a specuvester - I will comment in MARCH again - for the moment I am working to keep head above water

There are thousands in your position, good luck to you, I think you will be able to to get close to 5.5% by March or just after.

Incredibly an advert appeared on my social media last night from what appears to be a reasonably popular female REA on the Northshore. She was telling her followers that her and her husband had just purchased yet another rental and that because rates are dropping that she was certain now is a good time to buy.

The apprehension on her face is real (even if she isn’t aware of it). She might be right (and I could be wrong) but it is also possible that now is a terrible time to buy and that waiting 6-12 months could reward you by 10’s or 100’s of $000 - just by being patient.

Periods of rising unemployment while yield curves are inverted or normalising from an inversion are almost always a terrible time to buy assets (other than gold etc) - but I imagine this isn’t a point of discussion at the RE agency.

You would be literally insane to buy now.

A glut of houses for sale, unemployment still rising, skilled youngsters leaving the country and not many arriving... the retirees getting caught with investment properties they can't sell and a ton more new properties coming in the market.

Interest rates can't drop too far too soon.. our exchange rate scenario is precarious already... when they do drop it will be in small increments. Trying to kick start our economy by trying to reignite the housing ponzi won't work while it's still in free fall. Wages are low as is job security . Smart young kids are leaving for better work and more affordable houses and lifestyles...... pushing house prices up will take a big change in the ocr and simply make matters worse.

If you spend the whole night binge drinking (gorging on nearly free credit) you can't avoid the hangover.

Those you refer to as DGMs are mostly sitting pretty now with useful skills, we are cashed up and ready for what always was the inevitable downturn... ready to make some money (what I call smart investors... who bet carefully and for the long term and account for economic cycles... ). Now the real economy is back I have more work than I can actually deliver . At great margins.

Are you a liquidator? Keen to know what industry as apart from that has “more work than I can deliver” especially “at great margins”…seriously keen to know?

Over leveraged speculation is akin to gambling. It is quite different to true investment with a risk balanced return/yield. Banks lending practice and central bank actions have rewarded the gambling option for so long people thinks it normal. It is not. In the US you can send the keys back to the bank via no recourse lending. The opposite applies in NZ. We are more aligned with its original definition under French Law used during in the Middle Ages meaning "death pledge". A rate change of 5.5% would be a big drop from today's 6 month rates of more or less 7%.

Do you mind discussing your thinking here, eg carefully weighed analysis or other etc...?

If you possess a second passport, you are always free to hand the keys to the bank, and dump your leased car in the airport long term parking lot.

Everyone is always free to break the law and skip the country, so long as the crime is white collar?

One of my friends came here as a backpacker just after graduating. He didn't pay his speeding fines. They passed on the fines to a debt collection agency who tracked him to Scotland 2 years later and made him pay plus interest.

Leaving the country is not a guarantee you get to leave your debts (a lot will depend on which country you're going back to)

I had an Australian friend who also racked up thousands in speeding fines. She also had a NZ passport. She flew to NZ, changed her name by deed poll, got a new passport, and re-entered Australia as a different person.

I'd also suggest that its much easier to track someone down in Scotland than it is in India or China. Especially if they didnt immediately just apply for another visa to a different country, and headed off again to Australia or Canada to start over.

Facial rec in all airports. Unless you have James Bond movie like surgery they can track you it they really want to.

Hang in there!

Sadly, there'll be a few lurkers here that wish you nothing but ill will, but remember, it always rains after a drought.

No point of the rain if your brains are fried with the heat..

One of my North Shore neighbours just sold his stand-alone house 10% above 2021 RV

STAY AWAY FROM TOWNHOUSE/APARTMENT

Hahaha...

I've seen sales for less than half of CV as well, it doesn't mean its the norm.

Another neighbour sold his house 8% above RV six months ago

And the 3rd neighbor sold theirs for 20%above?

And I've seen more than one house sell for less than half its CV...

Is this a comforting mechanism for you or something?

Would have to be a leaker, you are lucky to get land value plus 10%, they are a wrecking ball job and its costs like $30K just to demo it. Plenty of them on the North Shore, I should know I owned one.

But why did they sell it at all?

"Because they think prices are going higher from here!" isn't one answer.

And in all likelihood; as our esteemed Prime Minister is doing now, selling investment property off before prices recalibrate looks like a mighty fine idea; as long as you can find someone who CAN pay an asking price. I wonder if the IRD will ask him some pertinent questions - and they can, regardless of how long the property has been held.

https://www.thepress.co.nz/politics/350362509/christopher-luxon-puts-in…

FYI, the net PBT yield is estimated at about 2.69% on this property. Compare that with:

1) 1 year time deposit of 5.6% p.a at ASB

2) 5 year time deposit of 4.3% p.a at ASB

3) 10 year NZ government bond yield of 4.25% p.a (the risk free rate")

JM.....the North Shore property levitation Agent. Leveraged bigly, by the looks?

Must be tough work in a crashing market, such as the facts obviously show.

But your anecdotes are carefully portrayed, to defy the facts in the above researched article.

Did they offer a gold bar with it?

Thank god, we were all worried for a moment. Nothing to see here folks, Realestate.co.nz are just being doom and gloom goblins.

Du Val into receivership

The first one

Won't be the last one. I admit I am surprised by how long this has taken though. Investors should have acted months ago, if for no other reason than to not give the Clarke's time to siphon funds out of the company and in to personal offshore bank accounts. Currently owners of certain other development companies are busy selling assets too, there is going to be nothing left for their investors either.

Saw them swanning around in a high end place just a few weeks ago drinking champagne

Ha, I thought they were already gone.

Wellington will continue to see huge increases to the housing stock.

The Public Sector job loses aren't one clean cut, they're a constant monthly stream that looks to continue over the next year (and their could be further cuts in outyears).

The short/medium term contractor market has also dried up. This this is reducing market short to medium rentals so their is also a glut of rental properties on the market (particularly central city apartments).

This is also impacting retail and hospitality significantly, driving more people form the city.

Yep. Those job losses are being felt in probably every industry right across the lower North island. My cousin is a builder there and he said work has dried up pretty much. A lot of people have jobs because of the public sector, and contracts are getting cancelled left right and centre. It's a dark day for this country. I don't think I've ever seen it in such a dire state.

Wellington is right f%%#ed

Don’t forget their 19% rate increase with the water infrastructure still decaying and insurers catastrophe models getting more sophisticated which means further insurance premium hikes in future.

Would never have happened under a Labour government.

It did happen under a Labour Govt.

While the NZ housing bubble's initial trigger was the opening up of lending and snowballing equity in the 2000s, Labour's money printing policy and encouragement of artificially low rates and and LVRs definitely supercharged the bubble. It didn't matter who was in power, this bubble was going to bust. The only options to keep that from happening are exceedingly reckless...and I worry the current coalition will implement them instead of letting the market take a natural correction.

Time to buy, next year we might see 5-10% jump in house prices

Could be.

But if they fall 30%, a lot of owners of 'investment' property are going to the wall. And as we all know about DEBT - it's nominal, and not only can it take all your current assets, but those that you are yet to earn.

That's the wonderful thing about speculation - it goes both ways. And often against the holder of assets at the most inconvenient, unexpected of times.

(That's why Crashes happen. Black Swans and all of that.)

10% up in 2025, guaranteed!

100% this is a TTP sock puppet account

Walk the Talk

"Time to buy, next year we might see 5-10% jump in house prices "

Here is one for you to buy:

https://www.oneroof.co.nz/news/latest-news/pm-selling-1m-investment-pro…

Yes, somehow in the middle of the growing recession and widespread job loss, housing will surely make a recovery.

Townhouses have recently accounted for around 45% of all new dwelling consents across the country, compared to just 6% back in 2012. Pretty hard to now do do any form of price comparison, the average will obviously be falling.

Which indicates that the developers are building to meet future demand - town houses. So those caught with other product, e.g.: the old 4/5 bedroom stand-alone, are in for a challenging time. Even worse. Those caught on a 10 acre life-sentence block away from Countdown; the doctors and the public transport (the older we all get, the less chance that we keep our driving license etc)

You mean those people wanting to buy a decent 3 bedroom house on a stand alone section will find it challenging to be able to afford it ? Kind of my point, the price of these could be going up while all the rest of the market is being dragged down due to cheaper townhouses.

Do you know why jewellers are selling so many lab grown diamonds these days? Because the natural stones are so much more expensive (say, your 3 bedroom stand alone). And as more lab growns are bought, the price of the natural stones FALLS to try to attract buyers back to their product.

The same will happen to stand-alone properties. The alternative product will force them to fall if they want to be competitive.

Probably not a good comparison. So you think something on your finger you don't even need is a good comparison to a house that pretty much everyone needs in one form or another ?

Terrible comparison, you should be comparing carat size. Not lab grown vs blood diamond.

Those townhouses are only fit for housing people who just got off a plane with a suitcase. They are not suitable for families (too small, no storage, pathetic kitchens), people over 50 (who don't want multi-level), people with pets (no backyard), or anyone with a car (they'll soon get sick of getting their car windows smashed in).

If I were an investor right now, I'd be looking at those standalone houses, as those are the things you can add value to by renovating, subdividing, or adding a second dwelling to. Now that interest deductibility is restored, investors are back buying existing dwellings which have much higher yields, than those crappy townhouses that are hugely cashflow negative. (As a comparison, the yield on a new build townhouse in my area is 3.8% compared to 5.7% on an existing 2 bedroom unit. Which would you pick?)

It all comes down to the specific house, you cannot generalise. A decent quality build house on a large elevated section with views is only going to go up in value, its that simple. A townhouse over time will simply not keep pace and it will at some point take a massive dive in value. Those Townhouses suck, the whole place can hear a single domestic, parking is shit, too many are rented with shitty tenants, the list goes on.

Those townhouses are only fit for housing people who just got off a plane with a suitcase. They are not suitable for families (too small, no storage, pathetic kitchens), people over 50 (who don't want multi-level), people with pets (no backyard), or anyone with a car (they'll soon get sick of getting their car windows smashed in).

While not preferable, there are plenty of tenement apartments and flats in many cities of the world where families grow up. I have friends in the UK who are included in this.

Drove past a Duval development in Mangere today. Looks close to completion. A standing army of trades working on site. 180 units next to the motorway. Starting price from 800k. Even if you could pay all cash. Why would you? Lucky to get to 4% yield and within a few months the development having the "lived in" look they will depreciate faster than a European car.

800K is still well short of the average Auckland "House" price, hence the market is being dragged down by places that are in no way comparable to a decent 3 bedroom on a stand alone section. Anyone who has lived in a variety of places knows full well the difference between the two.

Yeah many have noted that AKL averages before Covid was reasonably flat due to this effect, even though large 800 sq m sites where going nuts. You have to understand the market suburbs and potential buyer of a site, developers pushed prices up 20-30% now they are gone.

wonder if they will get finished.

Not likely based on todays developments. No idea when I posted. Just and observation. Poor tradies will be screwed over as usual. Hopefully they are in there taking everything out they can before the security arrives.

Tale of two property markets. I've maintained two Christchurch TradeMe searches for years now. The first is for properties at the higher end of the market, and listings for those are pretty light at present. About what you would expect for this time of year. The other is for <$700k properties, and those are running high, and I expect the arrival of spring stock will push it to the highest level in years. Its the tidal wave of new build townhouses that are piling up.

Which brings me to the other article on shoebox apartments. The problem is that, like with townhouses, developers will start building them en masse, only to find out that there arent enough buyers in that niche market, and then none of them can sell, even with massive discounting. Then they go broke. So perhaps the Council should put a limit on the number of shoeboxes that can be built, so we don't end up like the townhouse situation where half of all builds are properties that only temporary residents want to live in.

B&T auction today had 10 properties and all passed in with just one attracting bids that got no higher than the 2016 price. Earlier in the week a property sold for almost 450k less than what it sold for in 2021. Owners had bought so hopefully they got a good price on the new property.

I know someone who bought the site next to them for $2.38 mil a few years back, where going to bowl both and put units in.... not so much now, was passing in at auction last month now asking $2.45 mil

Its going to really sting, to move that on. Bedrooms too small, not a problem if you going to bowl it, big problem come sale time, maybe $1.85...

"Buy and Hold maaaaate, not making any more maaaaaate, you cant loose maaaaaate".....until you do. Big time.

Wonder when the online value estimation sites will catch up with market changes. That will start to hammer it home to many people.

You mean the online estimator operated by vested interests. Not holding my breath on that.

Owner going to need to take a downward revaluation on the property now?

Yep 40% to 60% off future deals. It will eventually mirror the USA commercial crash.

FHBs, Take at least -45% off all 2021/2022 CVs, or face bad negative equity depression in the NZ Housing market bottoms of 2026/2027.

This timeframe bottom is so predictable, even Tony Alexander will get with the program.....

DGMs don't forget though that FHBs are often looking to trade up.

Waiting now to secure a nicer place than you could afford at the moment is obviously a great financial strategy.

However the doom and gloom of being in a place for 5-10yrs and then trading up is actually not so negative during a downturn.

Let's say I buy a million dollar home today (20% deposit) and I'd love to retire/raise my kids in something worth 1.5mill currently. During a 'boom' growth period of 5% per year for 5 years I will gain $276k in appreciation on top of the $200k I put in as well as paying off $72k of mortgage. A lovely chunky $548k, but the place i want is now $1.914mill. Leaving me with needing a $1.366mill mortgage.

Conversely during a depressive period (5% loss per year for 5 years) my million dollar home will be $774k. The only equity I will have left is $46k. The house I want is now $1.160m.

So... The question is in which situation or in-between is the better? Can me and my wife in 5 years handle trying to find an extra $186k to stump up what will be needed and end up with a total mortgage of $928k?

That means for each of us we need to save an extra $18.6k per year over those five years. But we will end up in our dream home which will only cost in mortgage payments 16.5% higher than for our first home.

Conversely in the boom situation despite the huge equity, to end up in our dream home we will have mortgage payments increase 70% to currently a big ask.

Saving an extra $18.6k per year each for 5 years is conversely similar to for 5 years having a mortgage increase (for that period) of 71.5%.

Two very different scenarios, and both with benefits and detriments to lifestyle, career goals etc. $18.6k each for 5 years is a hell of an ask, but in the end much better off for the remaining mortgage than the 71.5% increase from the boom scenario.

Unfortunately most people are financially illiterate and do not understand this. This applies to all the vendors who have pulled their houses off the market in order "to wait until prices recover". They fail to understand, that even if prices do recover, that means the house they want to upgrade to has also gone up in price, and they will have to borrow more to cover the gap. Whereas even if they sold now "at a discount" they can then go buy something "at a discount" and save themselves some money. Even better, if they wanted to rent for 6-12 months in between selling and buying, they could buy something at "an even greater discount". But no, they sit there in their old house waiting for the house they want to buy to become extremely unaffordable, only to find out later that the bank won't lend the money to buy their dream home due to servicing limits and DTIs

LOL

Surprised there's no mention of "bubble" anywhere in the article or the comments, so I'll do my bit.

Yep BUBBLE.

We are still very near PEAK BUBBLE. Warning, warning!

It is not DGM to state that bubbles are very dangerious and the FACT is that ALL BUBBLES BURST COMPLETELY.

There is no alternative.

Those that ponder taking anything near 1 million in debt as a FHBer, are a problem to themselves, and taking monumental financial risks.

They should be in a straight jacket and padded cell, just to stop stupid, self financial harm. But no, we won't do such sensible things and let people pick up heavy, debt grenades and put said "pin pulled" explosives, in their pockets.

They are much safer buying within their means, that allows comfortable repayments ar 9.5% interest rates.

This is obvious right?

So some free and usefull advice for FBHs:

Don't be the landed gentry Boomers, bag holders, high priced liquidation IDIOT and don't take Debt of anything more than 400k.

HINT: Don't be buying off or near Wingers swamp, in the Riverswamphead.

Live humbly at the start FHBers.

Hold off the champers lifestyle untill it matches your diversified, much later wealth. Live humbly.

Article in ODT today (03.08.2024) "Incentivised to buy new Home" ... if the article is correct some developers are offering cash back upon purchase and the idea is that rather than discounting and "devaluing' the sale price, the 'cash back' will maintain the properties purchase value. Couple of things I think about here ... Is it misleading the market ? Is it reflective of how dire things are for developers? Should such a practice be regulated so as to avert distorting market values (should the practice become normalised). Are lenders factoring such moves into their assessments?. I can only surmise that the rise of such activity red flags where some developers are presently. https://www.odt.co.nz/news/national/incentivised-buy-new-home

A return of the 2008/2009 "free car" with every new Horncastle Homes build type of model.

I wouldn't necessarily call it a market distortion, while one developer may offer a $10k cash back another might price an "identical" property $12k less. The lenders might want to be aware of it. While they're happily writing up the loan, they are in a roundabout way "overlending" by $10k and in hindsight may have preferred to loan $10k less to limit exposure.

Would you call it a market distortion if someone slapped 200k on top of the price and said to buyers if you buy at this price I will throw you 150k back ? Where does it stop? 10k today...100k tommorow....250k next week... Why not just take the lender for all you can get... and keep the market guessing... Im thinking this type of activity needs to be regulated before it gets out into space with what can be cashed back.... lol

I'm sure everybody's a grown up and is capable of making a rational call on the merit of these cash back schemes and doesn't need the Government to step in.

No different than the "market distortion" that is our subject matter experts (banks) dropping their test rates to 5 - 6%, before ratcheting them up to 9% within 12 months. How many FHB got burnt, but are told they should've done their homework? Do we regulate the test rates?

"Do we regulate the test rates?"

Some people should be prevented from borrowing too much to protect themselves from getting into potential financial difficulties and financial stress - especially those that are financially illiterate.

Bank stress test rates restrict the amount of credit to borrowers including first home buyers. This is now done via the RBNZ's debt to income restrictions.

Remember, the extreme debt risks were preventable back in 2016 when the then Finance Minister did not give the RBNZ the tools they requested to address macroprudential risks. Remember that there was lobbying by those with their vested financial self interests to not implement the debt to income measures. It may also have become a political issue with the upcoming elections at the time and may have cost potential votes for the incumbent government at the time - this policy would have adversely impacted property investors, and most owner occupier buyers (including first home buyers) - a potentially large voting constituency. At the time many with their vested financial interests were arguing that the debt to income restrictions would restrict first home buyers from buying (what they didn't say was that it would also protect first home buyers from taking on too much debt because that would not support their case and vested financial interests)

The RBNZ can only operate with the tools available. If the necessary tools are unavailable, then there are consequences of having inadequate resources.

https://www.interest.co.nz/property/85201/reserve-bank-confirms-meeting…

The RBNZ governor stated in 2021, that the choice by the government to allow or not allow DTI's was a political one:

But he has suggested that the Government's decision around giving the central bank debt-to-income (DTI) restriction powers is a political one, as it might adversely impact first home buyers.

"It comes down to a political decision around whether they [the Government] are willing, or not, to provide those tools and accept some of the challenges that may bring," Orr told media this morning.

https://www.nzherald.co.nz/nz/reserve-bank-boss-adrian-orr-warns-mps-of…

If you assume it would have taken 30 months, then the DTI framework may have been ready to go sometime in in 2019. This would have been before interest rates reached their record low levels in mid 2021.

If a debt to income ratio of 5 was imposed back in 2019, then a significant amount of lending would not have been made (and debt to income levels would have been less likely to have reached their record levels). Many first home buyers would have been rejected for large unaffordable mortgages like this guy (https://www.newshub.co.nz/home/money/2021/11/first-home-buyer-not-very-….) He was disappointed at the time of his loan rejection, but in hindsight he is likely to be thankful that the bank refused to give him a large mortgage that he applied for and hence avoided cashflow stress and a large loss in his equity (and potentially negative equity).

As a result of that single policy decision back in 2016, this will result in potentially thousands of highly leveraged owner occupiers who purchased in 2020 - 2022 being collateral damage, including those first home buyers that you refer to. This will cause cashflow stress, mental stress and unfortunately, some will resort to self harm.

This will likely also lead to an increase in demand for social housing.

Cash backs are great for the developer but not for the buyer. The buyer is effectively overpaying for the property by $10k, borrowing an extra $10k from the bank and paying interest on it for 30 years, just to get $10k cash to go spend on something like a couch. They would be far better off getting $10k off the price.

Also keeps the recorded sale price up for developer borrowing metrics, and valuation modeling. So not true market and a means of last resort, probably before liquidation discussions with funders.

Fraud in all but name.

Here is the dinkum oil...must be true!!!!

https://www.oneroof.co.nz/news/im-calling-it-agent-says-aucklands-lates…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.