One of the hottest topics of conversation in the residential property market at the moment is second guessing when the Reserve Bank will start to cut interest rates and by how much.

Some have it that a cut to the Official Cash Rate (OCR), and a consequent cut in mortgage interest rates, will quickly turn the market around.

Buyers will return in force, prices will start rising, there will capital gains galore and all will be well.

Or so they hope.

Unfortunately things are not quite that simple.

The housing market is facing many more challenges than just high interest rates.

Probably the biggest is the current overhang of unsold properties.

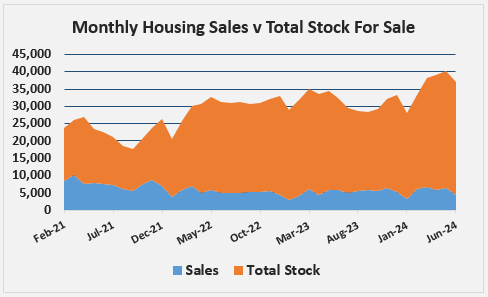

The overhang is the difference between the total number of properties on the market and the number that are sold each month.

And that has been growing hugely over the last three years.

The chart below illustrates the phenomenon.

The blue field at the bottom of the chart is the number of residential sales recorded by the Real Estate Institute of New Zealand each month. The orange field above it is the total number of residential properties available for sale on Realestate.co.nz at the end of the previous month (stock).

Three years ago, at the end of May 2021, there were 14,883 residential properties on the market. In June 2021 there were 7629 residential sales, leaving an overhang of 7254.

At the end of May this year the total stock on the market had increased by 119% to 32,598.

But sales have headed in the opposite direction to just 4356 in June this year, down 43% compared to three years ago.

Consequently the overhang of unsold properties has ballooned by 289% over the same period, to 28,242 in June this year.

This means the market will slog through winter and head into spring with a mountain of unsold properties weighing down on it.

Unfortunately the problem is even worse than the above figures suggest, because they are just the sellers we know about.

On top of that, there is also a potential tsunami of latent supply waiting to come onto the market.

These are people who may have already tried unsuccessfully to sell their property and then taken it off the market for the time being.

Then there are those who want to sell but are sitting on the sidelines for the time being, perhaps waiting for the market to pick up.

Those people will still be wanting to sell.

We don’t know how big this latent supply of properties for sale is, but anecdotal evidence suggests it could be very large indeed.

And if mortgage rate cuts, when they eventually arrive, are touted as a turning point in the market, it could well prompt latent supply to turn into actual supply.

And that could push the market even further into buyers’ favour.

All of that would be bad enough, but there are a couple of other factors also likely to weigh on the residential property market.

According to Statistics NZ, there was a net loss of population from migration in May, with around 2000 more people leaving the country long-term than arrived.

Those figures need to be treated with some caution because they can be subject to substantial revisions, especially following a sharp change in migration patterns.

However if they signify an ongoing turn in migration, and we have a net loss of population from migration for a significant period of time, then that could have serious implications for the housing market.

It would most likely affect demand for rental housing first, but that would eventually flow through to general demand for real estate as well, as investors reassessed their positions.

Finally of course there’s the general economy.

People often talk about the housing market as if it operates independently from the rest of the economy, but of course the two are intimately entwined.

And right now the economy has a bit of a cold.

It’s not at death’s door, but it’s hardly in rude good health either.

So all in all, the outlook for the housing market looks difficult, even with potential cuts to mortgage interest rates on the horizon.

- The comment stream on this story is now closed.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

69 Comments

Don’t think anyone smart is expecting a quick turnaround, these things take time, sentiment change takes time too. Nothing exciting until towards the end of the decade in picking and that’s OK.

There are plenty on here who think we are one OCR cut away from a return to the housing boom of old.

Cue “anyone smart”

I actually can't think of too many.

The general consensus is pretty grim.

Give me a list. Besides Zwifter.

You know, plenty.

Don't let's get bogged down in specifics.

Happy to make the short list. It all depends on the level of rate cuts, how long its going to take to come down and other smoke signals from the RBNZ. Just to clarify, all my money is in TD's so no vested interest in rates dropping but it sure will help existing mortgage holders.

"no vested interest" What about your partners fixed interest mortgage? It could be assumed you'd have a healthy vested interest in your partners financial wellbeing. That's a good thing - right?

Correct and she has taken my advice to fix for 6 months at 6.99% at the beginning of August. Fully expecting rates to drop by 1% between now and February 2025. The OCR is showing a disconnect, if the RBNZ doesn't officially reduce by 1%, the banks will do it for him. Rates are already down 0.25% so only 0.75% to go.

"the banks will do it for him" That's an interesting take/angle. It's people like you and me that are flooding the banks with deposits for which there is weak demand to on-lend. As the article above explains, cheaper money may not deliver what some are dreaming of. If enough people believe the asset which they're saving for is going to be even cheaper tomorrow - well....where's the hurry when they're gaining significant ground in the process?

Wingman just showed up

Let's look at the fundamentals, and not just at the current and short-term future OCR levels: the NZ housing markets is one of the most overpriced markets in the world, so there is only one way for the NZ housing market to go in the medium/long term: DOWN, at least in real terms if not in nominal terms.

There are many smart people ready to promote the quick turnaround theory, without caring whether they are right or not - they're well aware that the market runs on sentiment and fomo and how quickly they can get the pump going, at the very least in peoples' minds.

This is a very good article. likely to be AT LEAST 12 months before there’s any potential glimmer of life in the housing market. And even then it will be a very mild upturn

One thing to be conscious of is that it's not just whatever people's interest rates are today, it's about perception in the wider economy.

If we see continual rate hikes, and signalling of no relief in the short term, then people are going to behave more conservatively, in case rates resume climbing, or not lower anytime soon.

This isn't to say we'd be out of the woods, but sentiment would likely shift, and with it, behaviour.

Business turnover will not bounce back quick enough.

The interest rate cuts all already priced into the market for all but variable mortgages!

It will be a slow turnaround but the media needs to publish every day/week so expect a lot of "oh noes, the market isn't moving since last Tuesday, sucks to be an investor lol" type stories and comments for the rest of the year at least.

"We don’t know how big this latent supply of properties for sale is"

Maybe. But with a rapidly ageing demographic of property owners, it's probably bigger than we care to admit, and getting bigger as each day passes.

How many will want to go into older age with their lifetimes' savings/investments imprisoned in the residential property market? Because that's where they are, and it's what we've encouraged for the last 40 years. As owners age, price will not be the main driver to sell, liquidity; getting their hands on the cash to live out their lives to the expectations they had, will be.

Although we have people leaving, we still have a huge overhang of people that came after Covid in their droves! It takes around 2 years for those looking to live here long term to get residency. Once they have residency, they will be able to apply to purchase a home. That makes me think by next year a few will start to come on stream and that may contribute to demand. A slow and steady turnaround with rates coming back into 2025, but nothing major over the next 6 months that's for sure. The Reserve Bank I feel has overcooked a little and this will drag the economy through the mud a bit longer before it can stabilise.

"they will be able to apply to purchase a home."

No problems with that at all.

But what we have to do is get on top of those who want more than just their own home. And if we have any sense at all, that's where the target will be - secondary property holdings.

They're currently living somewhere though?

So we'll have increased demand for owner occupied properties, and reduced demand for rental properties (assuming people continue to leave). Unless you think the huge overhang of Covid arrivals are all living 10 deep to a 3 bedroom and their subsequent house purchases will only free up floor space?

Then we’ll see a corresponding dive in rentals, which will flow through to the housing market. And what’s going to be the bigger price driver? FHBs buying or squeezed landlords offloading?

Can we see the data 4 years before 2021?

Not to suggest there isn't increasing overhang, but it's always nice to see how NZ looked, before COVID. Because COVID era figures can be fairly extenuating.

I'll keep repeating it, house prices begin to rise at the END of an interest rate cut cycle, not the beginning.

Mortgage rates have dropped to about 6.8%, down by a full percentage point from October last year, and yet sales of existing homes have plunged, and vacant homes for sale are coming out of the woodwork... And supply in June spiked to the highest level in four years.

https://wolfstreet.com/2024/07/23/here-comes-the-inventory-of-vacant-ho…

To be fair, yes there's a lot more properties offered, but also a greater proportion of dreamers (>30%) that will end up in listings being withdrawn in 3 or 4 months.

Still the same number of "real" sellers to me.

What will any property sell for? What a buyer can pay for it. Not what they dream of, on either side of the equation; what the buyer CAN pay. Clamp down on that in one of many ways, and the asking prices keep falling.

Doesn't seem to work like that in the head of the agents I've spoken to. Called one last week to enquire about a property that, in the pictures, ticks a lot of boxes for me. $1.450.000 CV (Sep 2021, more or less peak) which is huge for Hamilton, could be interested for $1.300.000 (still too much I know) but the agent cut the conversation short "it's a luxury property, it will sell for $1.4M+". Arrogance? Anger?

His primary motive is to secure a sale.

His secondary motive is to try and make price expectations as high as possible.

Your view should incorporate how much it'd cost to replace said luxury home (is it an architecural luxury home, or just a slightly better spec'd new home), and whether you'd actually want to build that house yourself.

According to my standards it's just a "normal" newish house (better insulation than a 30 yo one, fresh-ish paint, etc.). Nothing special regarding its architecture, but in NZ having two heatpumps is a luxury...

I don't see him reaching his first goal with such attitude. I mean he can expect more of course, but what I'd do is walk any potential buyer in that house, praise all its great features and maybe manage to get them up their budget a bit.

It's a certainty it will not sell for $1.4M, not at the current rates. I've followed auctions of better houses (some truly luxurious), they didn't even reach $1.35M for the best ones.

Speaking to a friend/agent selling in central Auckland, it is beyond dead, lowball offers everywhere, but not much else. The fear of overpaying is big out there.

Yup, I've heard the same...

Inventory is still piling on. Indications are that more significant price falls lie ahead.

like -10% Dec 23 to Dec 24?

It is certainly looking like it! That was your prediction wasn't it?

Funny to think that Tony the Comb, and various other spruik-lords, were calling for a 10% INCREASE over same period.

The volume of appraisals being conducted right now, with a view to hitting the market in August/September, indicates that the real estate market will be swamped with stock in spring/summer.

An interest rate drop of 0.25 in November, already priced in by these banks recently cutting, so 0.25 in November and maybe 0.25 in February will make sod all difference to the housing market - it needs a drop of 2 percent to make any real difference and that’s unlikely given the OCR has seldom gone below 5% in the last 30 years.

Most people are happy if the price of there house remains pretty much the same, a drop in interest rates of 1% will see them not fall. Most people on here are screaming that houses need to come down further in price, not going to happen. If the RBNZ cuts rates in August and signals more cuts to come, then now is the time to buy and fix that mortgage for 6 months.

So how many contracts do you have your name on?

I received this from a RE agent today. It made me laugh how much smoke he was blowing

”This is just a quick market update as we look towards a recovery in spring. Right across the market we are seeing micro improvements, less homes for sale, more views across the websites, numbers of visitors at open homes improving, and there are more offers being made. We are also seeing rents still rising , construction still slowing down and interest rates coming down, slowly, but the trend is definitely down. These are all early indicators of a change in the market, there are genuinely more buyers than there are homes for sale and once those buyers realise that and interest rates come down a little more, we will see prices lift before the end of the year, now is a great time to buy! Please take a moment to look at the links to homes for sale below, there is some fantastic value available for you to buy now, “

And a convenient omission of any mention of sales.

Cherry picking and clinging to any positives they can. I don't see how they can say that prices will lift before the end of the year.

"I received this from a RE agent today. It made me laugh how much smoke he was blowing"

Vested financial self interest attempts at creating a fear of missing out and fake scarcity / buying competition to induce potential buyers to buy. The real estate agent needs to earn commissions to keep their job (or keep their business surviving) and at a personal level, be able to put food on their own table to feed their family.

CAVEAT EMPTOR. Remember that real estate agents do not owe buyers a fiduciary duty.

Note: the first example might be considered mortgage fraud.

Kudos to Opes Partners for exposing this behaviour.

https://youtu.be/O9hmVDTz9Yo?t=228

How the scheme works:

https://youtu.be/O9hmVDTz9Yo?t=105

When people are desperate, some will resort to desperate and illegal choices.

I am picking some suburbs are going to be hit harder then others in Auckland.

Many FHBers do so as a couple, one of the things they think about is school zoning. Places like Manurewa that where very popular with investors do not appeal to these FHBers. They are probably going to have to find another investor to buy the house. (The current tenant is not likely to have a deposit for the current valuation, or even 50%). That's enough said about how hard its going to be for them to sell....

There will be buyers because multi cycle investors can sense the fear and smell the blood.... Sharks are happy to munch on a weaker brother.

Just after the GFC we where buying these for around 275k-310k each, spending a quick $30k, and renting them about $5-525 per week. Most where flicked as investment properties. But then things turned against investors, LAQC, depreciation then interest rates and bright line

LAQCs were not able to attribute losses to shareholders for income years starting on or after 1 April 2011 and there are no new QC or LAQC elections. Existing LAQCs automatically became QCs (without the ability to attribute losses) at the start of the income year starting 1 April 2011.

Its just mind boggling how negative the cashflow has turned on the current so called investors (Bag Holders).

Its not just rates that have to come down, prices have to drop, there will be no more free capital gains with DTIs.

Most of these early post GFC investors got in around 3-400k , later investors are in a way way worse position.

"There will be buyers because multi cycle investors can sense the fear and smell the blood.... Sharks are happy to munch on a weaker brother"

Your metaphors make property investment/speculation seem dangerous. Oh, wait a minute.....

I think many FHBers are earning well, can control their costs reasonably easily because they haven't had kids - and so don't think about the school zone.

Then they have kids and have to bail into a better area.

Oh wait. That will be ugly looking forward.

Be careful out there...

The average age of a FHB is 36. I think most of them have had kids by then. That's probably why they are broke and taking so long to buy a house.

https://www.oneroof.co.nz/news/first-home-buyers-are-getting-older-desp…

And the median age of a first time mother was 30.5years in 2018, and no doubt has increased further since then.

Even more to my point then, that Manurewa is not that attractive to a couple able to buy there first home.

Its an investors paradise.

Been spendin' most their lives

Livin' in a gangsta's paradise

Been spendin' most their lives

Livin' in a gangsta's paradise

Keep spendin' most our lives

Livin' in a gangsta's paradise

Keep spendin' most our lives

Livin' in a gangsta's paradise

"Places like Manurewa that where very popular with investors do not appeal to these FHBers"

There will be lower income households where Manurewa is one of the few places that are affordable. Likely to be existing renters in the area or neigbouring suburbs.

Have relatives of friends who live in that neighborhood who bought decades ago and experienced the socio economic demographic change around them.

Not sure why anyone would be surprised house prices rise only towards the end of the rate cutting cycle , and it needs to be constantly reiterated… OCR cuts take time to filter through just like OCR rises take time to filter through , simple as that. 2 years from now we’ll probably see an upward trajectory in house prices.

I think the overhand is larger than the graph suggests:

- Developers tend to list one townhouse when they have ten to sell. There is about 3,500 new home listings in Auckland on Trademe, which probably equates with 10,000 homes

- Completions are continuing - even if building consents are falling - May was the highest level of code of compliance issues on record. That implies there is probably a further 10,000 new homes appearing on the market before Christmas. An new houses are additional supply - not a shuffling between houses.

- And, while building consents have fallen, they have dropped to the level in 2022, which was still a historically high level. Could be another 15,000 homes in the pipeline for the next year.

First two points spot on. Not the third. Current consenting levels will have a big divergence from build rates over the next 12-18 months.

I can't believe there isn't more discussion of the absolutely insane role of unrealised equity in driving the original boom. Allowing the leveraging of unrealised capital gains to invest further in the same asset is a recipe for an uncontrolled speculative bubble. It means next year's price growth can essentially be triggered by the reinvestment of last year's price growth, without needing to recruit any new equity from outside the market. That's how you end up with prices that are totally unmoored from the real economy.

It's also massively destabilising - just as one year of strong growth created the equity to drive the next year's growth, the reverse is now happening on the downswing. Every percent fall in prices pushes a few more speculators below the equity required to participate further, lowering demand for the next year and creating even more price falls. And so the whole bubble will eventually unwind and we'll be left with a market floor that's determined by real earnings, not speculation. I wouldn't be surprised if that floor turns out to be 30% below current prices, or even more.

That's why we should be taxing equity release for property investment. The $200k you've 'unlocked' from your home to buy an IP is effectively being used in lieu of cash, so should be taxed the same.

Obviously not the best revenue generator in a downwards market but I'd see this more as a tempering mechanism in a frothy market ... I wonder how much less insane the market would have become if people tapping their equity had to front to the IRD with real cash in order to do so.

"I can't believe there isn't more discussion of the absolutely insane role of unrealised equity in driving the original boom. Allowing the leveraging of unrealised capital gains to invest further in the same asset is a recipe for an uncontrolled speculative bubble. It means next year's price growth can essentially be triggered by the reinvestment of last year's price growth, without needing to recruit any new equity from outside the market. That's how you end up with prices that are totally unmoored from the real economy"

The extreme house price risks were preventable back in 2016 when the then Finance Minister did not give the RBNZ the tools they requested to address macroprudential risks. There was lobbying by those with their vested financial self interests to not implement the debt to income measures. It may also have become a political issue with the upcoming elections at the time and may have cost potential votes for the incumbent government at the time - this policy would have adversely impacted property investors, and most owner occupier buyers - a potentially large voting constituency.

The RBNZ can only operate with the tools available. If the necessary tools are unavailable, then there are consequences of having inadequate resources.

https://www.interest.co.nz/property/85201/reserve-bank-confirms-meeting…

The RBNZ governor stated in 2021, that the choice by the government to allow or not allow DTI's was a political one:

But he has suggested that the Government's decision around giving the central bank debt-to-income (DTI) restriction powers is a political one, as it might adversely impact first home buyers.

"It comes down to a political decision around whether they [the Government] are willing, or not, to provide those tools and accept some of the challenges that may bring," Orr told media this morning.

https://www.nzherald.co.nz/nz/reserve-bank-boss-adrian-orr-warns-mps-of…

If you assume it would have taken 30 months, then the DTI framework may have been ready to go sometime in in 2019. This would have been before interest rates reached their record low levels in mid 2021.

If a debt to income ratio of 5 was imposed back in 2019, then a significant amount of lending would not have been made (and house prices would have been less likely to have reached their record levels).

As a result of that single policy decision, this will result in potentially thousands of highly leveraged owner occupiers who purchased in 2020 - 2022 being collateral damage. This will cause cashflow stress, mental stress and unfortunately, some will resort to self harm.

This will likely also lead to an increase in demand for social housing.

Here is an example of owner occupier collateral damage from falling house prices elsewhere around the world:

1) https://www.investorschronicle.co.uk/2012/09/20/your-money/property/ove…

2) https://youtu.be/iKPG_l1P7lk

3) https://youtu.be/ugBKnP2FKDM

4) https://youtu.be/fiCXsu_4BoA

5) https://youtu.be/1hi7gV9uyK8?t=2297

The bigger the party, the bigger the hangover.

I heard the property "learned" high priest, Ashley Church, absolutely spit tacks on ZB, about the travesty of the GOVT/RBNZ imposing the DTI debt limits.

It was the most brazen selfish vested interest and was in effect, alĺ about his ongoing unearned wealth being crimped just a little and limited his future hoarding of still more homes. What an uncaring weasel

He showed his true colours in vivid and did not care one jot about the prices being bid to the moon and excluding average wage households from secure home ownership.

Go on RBNZ, once the market bottoms out in 2026-2028, cut the DTI back to 3.5 to 4xDTI, which was the reasonable norm 20+ years ago, before most of us lost our financial minds and become like the old time, stupid, Dutch Tulip traders

Booo!

"Make housing inflate again!"

The people who have withdrawn from the market because they are... sick of it, will come back at any hint of life... swamping it with silly asking prices. Big leg down, first chance of a turnaround is xmas 2025 or 2026

There is no way this mess can clear this summer, the gap between offer and ask is just to wide on the average house.

for years we've been praying for a lower house prices, now we are in a period of cooling housing market, and possibly staying there for quite few years.

not totally a bad thing.

lets check in another 10% down....

So a recovery means that all the money that could be used to invest in productive businesses will get hoovered up by selling houses to each other again.

Super.

People invest in what they think are 'productive businesses' all the time, only to lose their money.

Read about them in the news.

Property might take a while to turn around, but there's a good chance it'll be ticking over nicely just before the next election.

There's always areas that are going to do better than others, you just need to find them.

The thing is that when people make predictions, hardly anyone goes back to look what people previously predicted several years down the track. So many property experts in recent years have been wrong. It is just noise.

wingman is noise... yes

People don't get rich buying at the top, they get rich buying at the bottom.

Are we talking swamps here ?

We're talking places like Riverhead, up 12.8% in the last year.

It's a great feeling picking a winner.

https://www.realestate.co.nz/insights/auckland/rodney/riverhead

A guy came from out of the bushes again today to make financial recommendations in Granny Herald. The same guy late last year was picking boom times for Ryman shares in 2024 😂

That’s not even several years ago

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.