The housing market crashed to Global Financial Crisis (GFC) levels in June.

The Real Estate Institute of NZ reported just 4356 residential sales in June, which was down 25.6% compared to June last year, and exactly a third lower compared to May this year.

Apart from June 2020, when the market was still reeling from pandemic restrictions, the 4356 residential properties sold in June was the lowest for that month since June 2008, which was in the midst of the GFC.

The dramatic slump in sales appears to be almost nationwide, with June sales in Auckland down 35.1% compared to June last year, and sales in the rest of the country (excluding Auckland) down 20.7% compared to a year ago.

Northland was the only region to go against the trend with June sales up 11.9%.compared to June last year.

The biggest annual declines in sales were in West Coast -51.2%, Tasman -41.7%, Gisborne -39.4% and Auckland -35.1%.

All regions had fewer sales in June this year than they did in May (for the full regional sales volume trends, refer to the interactive graph beneath the HPI table at the bottom of this article).

But as bad as those figures are they may get worse, because while sales have declined dramatically compared to a year ago, new listings and the total amount of stock on the market are both up strongly.

According to the REINZ, 7805 residential properties across the country were newly listed for sale in June, up 25.5% compared to June last year.

That means the number of properties newly listed for sale in June was almost 80% higher than the number sold in the same month.

That is causing a huge overhang of unsold properties sitting on the market.

The total residential stock for sale at the end of June was 31,745 properties, up 28.6% compared to the end of June last year.

In a perverse way the price trends are the only bright spots in the latest figures, not because they are rising, they aren't, but because prices aren't falling as fast as sales.

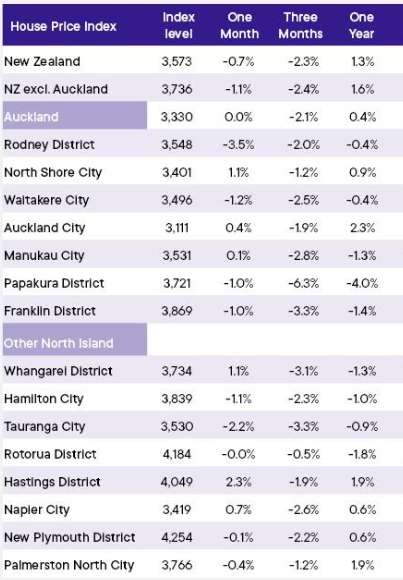

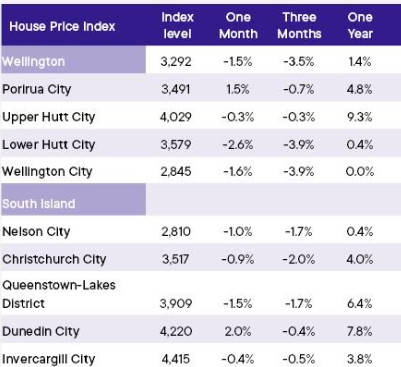

The REINZ House Price Index, which is probably the most up-to-date indicator of price movements each month, declined 0.7% nationally in June and has declined by -2.3% in the second quarter of this year.

The biggest decline in the month of June was -3.5% in Rodney District in northern Auckland, while the biggest declines in the June quarter were in Lower Hutt and Wellington City, both -3.9% (see the table below for the full regional HPI figures. For the regional median price trends, see the interactive graph at the bottom of this article).

The REINZ report on June's sales described the market as "a little chilly amid economic challenges."

"The property market in June is reflecting the wider economic climate in New Zealand," REINZ Chief Executive Jen Baird said.

"New listings have risen, continuing a trend seen in 2024, yet this increase contrasts with a noticeable decline in buyer activity, reflected in lower national sales figures.

"The typical winter lull, compounded by current economic conditions, has contributed to lower levels of activity in the market," she said.

The comment stream on this story is now closed.

REINZ House Price Index - June 2024

Volumes sold - REINZ

Select chart tabs

Median price - REINZ

Select chart tabs

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

207 Comments

There's some desperate hope out there, isn't there? False hope for those wanting for a return to The Good Ol' Days. If the RBNZ has any sense at all, it will take advantage of this to recalibrate the New Zealand economy. One no longer based on speculation but good old-fashioned real work.

"There are more houses for sale than there are buyers, but the outlook for the market once rates start to fall is more positive. A year and a half ago, we didn’t know when the Reserve Bank would call it quits on interest rate rises. Now, we know rates have hit a ceiling and at some point in the future they will come down."

What's the dollar likely to do from here, was up overnight against USD

Agree, keep rates as they are - our economy needs to recalibrate, painful as it maybe. We can’t have it both ways - high house prices and a strong economy. Much better to have lower, affordable house prices that will in turn, facilitate discretionary spent into the local domestic economy.

Labour said they would reset the economy and we believed them. By keeping the border shut and immigrants out wages and employment were going to increase to utopia. They pushed hard against the tide lying all the way, then gave in and JA waltzed into the beyond, ready for super stardom.

We are picking up the pieces...recalibration is a fantasy

If interest rates are high then there is no discretionary spending for most.

Aucklanders must be feeling the financial squeeze big time and if they dont drop them soon then businesses are going to collapse big time.

While rates are 7% and debt servicing at 9% then both home owners and tenants are going to feel it.

If you are waiting for prices to drop so that you can buy, then I would suggest you are going to be disappointed, as everyone will be into it and prices will increase once again.

Totally agree. The comments above about recalibrating the economy has nothing to do with the reserve bank and monetary policy.

Rates will be coming down soon.

If I had the money, I’d be out there looking to buy now. There’s plenty of room for negotiation with all the unsold properties out there. Not telling anyone else they should, but just what I’d do.

Monetary policy can’t recalibrate the economy. It merely corrects (or causes) short term fluctuations. Fiscal policies are needed to move the economy away from its dependence on housing and property investing

I love their optimism.. 'a bit chilly '.. be honest and confirm it's a couple of degrees short of being frozen

Yep. RE Agents fighting off buyers within minutes of listing, being dismissive as buyers offered ever higher record sight unseen offers sure was not work, it was an abuse of power. They were just the contracted face between the buyer and the seller, and boy did they ride all and sundry like a pony. Well things have changed, no pandemic panic, lower medium rates (not high), and job losses and construction activity in free fall everywhere.

Agents were implicit in basting buyers with greed based sauce as the desperate and greedy cooked everyone else's goose. They have to eat burnt goose along with everyone else now. I wish them well, there are plenty of other jobs out there....oh wait...

yes and as a cash buyer, i am noticing pathetic levels of followup and negotiating skills from the many agents who have my details. ie zero. they were glorified order-takers on the way up.. true colours now showing.

It's not really up to the reserve bank. They've got to keep the economy going... It's our tax system incentives. We got rid of land tax and loaded the burden on income tax and GST. In effect, disincentivising work and trade, and incentivising unproductive and inefficient landholdings.

Would the students of housing market history care to share their views on when we see some decent price adjustments.

A lot of what I am looking at has been sitting for months still wanting prices of old.

Which direction, though I guess you mean those smoking the green shoots

Would the students of housing market history care to share their views on when we see some decent price adjustments.

Hi Rastus,

Up or down?

TTP

That was also my question "which direction". Poor Rastus doesn't seem to know which way is up, forward or back

Markets very rarely bounce out of a bottom like they drop from the peaks, the chart looks more like a valley.

At the bottom more buyers and sellers will agree on value and sales numbers will rise, people would be comfortable about buying a new home before listing the old (not so much just here). There is no confidence that a stable bottom has been formed because it hasn't.

Most importantly the Fear of missing out has gone from the market, not one is being quick anymore.

The bad data is still coming out, peoples hours are reduced, overtime non existent, and bonuses not happening this year.

Winter is always slow for real estate in NZ, but the "busy" summer season this year is the time to judge the health of the market.

"There is no confidence that a stable bottom has been formed" A good pun from the horse trainer

"Winter is always slow for real estate" if you managed to 'close in' the new home yet before this winter blast you can keep working on it

Why do commentators always fall back on the GFC for comparison. That was nothing. I had a small business then and I was never aware there even was a recession. I think commentators should get a new set of rear-view mirrors and look back to the Oil Shock recession starting in the 1970s. I certainly felt that. Houses depreciated in the late 1970s by 40 % to 50%%. They took years to recover. My father and myself all but went bankrupt when we spec-built three home units. Eventually sold them for less than cost.

To call the tiny percentage declines that property indexes are showing in this article, 1% to 2%, are not worthy of even being quoted. I would call them minor natural fluctuations. But I suppose they make a good story for the hysterically inclined to take solace in.

And, if you want a wider perspective go back to the Great Depression of the 1929-1939 era. My late mother as a little eight-year-old remembered walking with her mother around the streets of Mt Eden asking "where have all the people gone" as every second house had been abandoned due to inability to service the mortgage.

Don't scoff...it could happen again. There's nothing to say that it won't.

Well said.

The current economic situation in NZ is much closer to the 70s than the GFC.

I'd also add that Councils around the country loosened zoning rules in the 70s too. The spec builders all thought they'd be able to sell at prices before the zoning rules were relaxed. The early builders did. The later ones finished as a supply glut was resulting in prices falling. Looks similar today, right? (Them's that don't study economic history are doomed to repeat it.)

That’s a great point about the loosening of zoning rules in the 70s. All those ‘sausage block’ flats flooding the market!

Yip I’ve done a reasonable amount of reading on history and financial markets, economic and demographics - one common theme is history repeats/rhymes every 80-100 years. So what we are living through right now is something similar to the 1920’s-1940’s. Think about what happened in those decades so you don’t get surprised about what could happen in the present/coming years.

It's going down, I know that.

My own observation is that a growing number are still holding out many months after listing. Some are cutting, many not.

I am interested in those who actually study the markets (without a conformation bias) on their views as to how long might we expect to see this 'stand-off' - as 'poor' rastus has cash from his freehold house sale to invest again shortly.

Not sure why you came out with such a childish comment? Rough weekend from the tenants perhaps?

Suggest looking at the rbnz OCR data and comparing with HPI data. Fairly good inverse correlation with a 12-18 month lag for prices to fully adjust upwards after interest rates dropped.

The market (vendors) have been more resilient than I had expected and HODL as the interest rates rose, so price drops from increased yield expectations haven't been fully priced into all vendors' bargaining yet even though it has been longer than 18 months.

If things pan out per RBNZ MPS, I'm picking a bottoming out between September and 6 months post first OCR cut... Say May 2025 latest, assuming a November cut.

In saying that, wholesale markets and banks have already started pricing in assumed drops to OCR

thanks for you comments. The lag is what seems important, not the 'now'.

Best comment today.

Any insight to add 1689Baptist regarding suspected lag duration or potential leading indicators to watch for a real turning point?

Noting that lagging indicators such as trends showing falling days to sell and taste inventory turnover rate, higher auction clearance rates help

As a student I'd say the current climate gives me 2009-2011 vibes more so than 2008 vibes. With solid assets (especially necessities) nominal prices will floor to a proportion of the building replacement cost and go no further.

There are some on here who believe prices will keep falling to 2015 prices (a 60% nominal drop). That simply wont happen when the cost of building sits around $4000/m2. You will either need a population decline or automated prefabrication of houses to make that happen.

Currently available stock vs demand is what influences sale prices in the short term. There's an over supply of listings and not enough demand at the current prices expected by sellers.

Future building costs don't overwrite these fundamentals.

There was a large volume of inventory in 2009/2010 as well. It took sometime to clear and the floor was elongated. But it did not lead to a deepening crash in nominal terms post 2008. Time will tell if i'm right or wrong Time Lord.

2009/2010 the OCR = 2.5%

Today the OCR = 5.5% (including the longest yield curve inversion in history)

Quite the difference impacting demand today than back in your cherry picked time period.

The average mortgage rates in 2009/2010 were about 6% so not too much difference on the coal face. Happy to disagree and move on on this one Time Lord.

But what matters for levels of house buying and the direction of property prices is not average mortgage rates on existing mortgages but current market interest rates. Massive difference there between 09 and now.

But prices were coming off a low base / rates coming down from a high base. July 2008 the OCR was 8.5% and mortgage rates around 9.5%. 6 months later the OCR was 3.5%.

6% mortgage rates after a 30 - 40% discount, vs 6% mortgage rates after a doubling/tripling and prices from a high base.

2009/2010

- GDP was rising

- Account balance was improving

- Government stimulus stable

- NZ House price to income multiple = 4.6

- 2-3 years after the yield curve became un-inverted

- OCR rate cut lag effect has finished

Today

- GDP is declining

- Account balance is declining

- Government stimulus is declining

- NZ House price to income multiple = 6.6

- Yield curve has been inverted for 836 days

- First OCR rate cut yet to arrive, lag effect yet to start

An important difference. We are about to find out what happens when the government is dumb enough to cut infrastructure spending going into a recession.

Apartment buyers part with 70k for a 15sqm carpark.. thats $4666 per sqm!!

was that here? Or Tokyo?

$288,000 for carpark in the Pacifica building, bidding commenced at $80. Orkland not tokyo

The stupidity of owners on Waiheke.

would make more sense to buy an 1 or 2br apartment with car park- rent out the apartment and keep the car park!

Sorry Baptist, the history of the various housing collapses I've studied indicates the cost of building new doesn't have much of a relationship with house prices. And I should note that building costs usually slump with house prices. And the size and type of new houses usually changes too, i.e. smaller and higher density. Check your logic very carefully. A floor will be found - but the reasons you give for the floor are tenuous.

Thanks for your feedback Chris. I am interested though in your research and why we have come to different conclusions. I think we can agree that there is little correlation on the house price cycle and the replacement cost. There are a multitude of factors that influence the former and not the latter. What I have concluded, however, is that the construction cost does becomes one of the two of three significant factors (Akaike's theorem) in determining floors. As far as I can tell, and granted I've only gone back to about the 70's, house floors do not drop below 75% of the replacement cost. We are at about that point now.

"house floors do not drop below 75% of the replacement cost"

Chicago, Illinois. There are other examples in a similar vane everywhere in the world. In essence, people just up sticks and leave, never to return.

Will it happen in NZ? Perhaps if the immigration tap is turned off as so many here want.

In any event, as NZ Inc is slowly gutted economically, we lose those with the most 'gumption', and economic activity is very slow to pick back up again.

right thanks. I have only been looking in NZ. We need to go to overseas for examples where there is a population crash. Completely agree the floor is near bottomless in this regard. I'd add Detroit, Michigan as an even more heinous example.

Detriot prices were down to less than 3x median multiple. This 3x seems to be an equilibrium point where if it is below this price, it is below its next best economic use point, and is certainly below the replacement value and there is no point building.

But at 3 to 4x then this is the range that true free market housing can happily be supplied for in stable thriving economies.

Above 4x suggests that restrictive housing policies are in place that allow speculative non-value-added capital gains to happen. The victims of which are homeowners paying way too much for a house with less amenity value than they would like, and developers whose margins are continuously getting squeezed, no matter what savings they try to find within their sphere of control.

We have a very large contingent of people in this country on temporary and permanent visas. If they lose their job, or their business goes under, and they cant pay for their house, and they cant sell their house - they can simply get on a plane and go back to their home countries, leaving all their debt behind. They always have the option to start over in another country on another visa. "History may not repeat, but it sure does rhyme"

I have said many times on this website that this is one of the very few upsides of high immigration over the past two years. It will buffer the employment impacts on kiwis

Does the pre-fab industry and smaller replacement houses factor? A family member talked about dropping insurance cover on the basis that if theirs burned down they'd buy a prefab package with smaller footprint over lime for lack replacement. A $400k replacement rather than a $500k? Could the new floor be lower spec/footprint replacement than the old spec/footprint?

Based on other property crashes: steady falls until 2027, flat for a couple of years then a slow pickup from there

I know it’s broken record but sorry you cannot properly compare 2008 sales to 2024 because housing stock has increased at last 15% since. Therefore sales per 100,000 of stock (or whatever gauge you want for a ratio) are much worse than it looks

Yes, they really like to selectively spin the stats.

It makes for more articles and click-baiting I suppose.

Indeed, that headline is deceptive. It can make many believe prices are back to 2008 levels, when in actual fact, they are almost double today.

much worse than it looks

That also goes for GDP figures

Guess house prices will be Lower Much Faster too.

is it me or does this winter feel a bit cold?

The latest modeling shows a cold economy is causing climate change.

Other than that, it's just you.

Apart from the wintry blast, the housing market is giving you the chills

And the chills, they're multiplying? If you're buying a house at the moment make sure it's the one that you want.

seller to buyer:

If you want my home

Forget my price

If you wanna get with me

Better make it fast

Now, don't go wasting

My precious time

Get your act together, we could have it now

I'll tell you what I want

What I really, really want

I wanna (Hey!), I wanna (Hey!)

I wanna (Hey!), I wanna (Hey!)

https://www.nzherald.co.nz/nz/weather-heavy-rain-warnings-for-northern-…

Polar vortex hits the NZ Property Market?

Auckland Median up 2.7%, HPI flat.

When the cuts come in a few months expect substantial price increases.

Pavlov's dogs you reckon?

Remember,

- Pavlov discovered that dogs can learn to associate a neutral stimulus (bell ringing) with an unconditioned stimulus (food) to elicit a conditioned response (salivation).

- The dogs’ salivation was not an automatic response to the bell, but rather a learned behavior.

- The conditioned response (salivation) was not permanent and could be extinguished if the bell was no longer paired with food.

Where's the money going to come from ? Interest rates aren't "automatically" going to go back to 3% . While if you lower rates in NZ, that will quickly reduce the NZD v USD and NZ will be paying way more for imports - while you will be the first one moaning that petrol has gone up 25%

You've had your fun .....the financial "gravy train" has finally derailed and "true" value of property is now falling, to come into line with NZ's "lacklustre" economy.

When the cuts come, expect the volumes to pick up slowly, and the prices to meander around at much the same level for another year post the first cut. That is unless the RBNZ massively overcook it on the cuts, in which case yeah, off to the races for another boom bust cycle we go, but with the DTI limits it wont be much of a boom.

Median house price creeping up in Auckland while HPI flat. Any theories as to why? A higher proportion of newer homes being cleared?

Remember that a median offers limited understanding without other measures of dispersion such as variance and mean.

Shortage of higher end homes available (as nobody is building them any more) so they sell for prices above CV, while lower end homes (particularly brand new 2 bedroom townhouses) sit on the market unsold while developers try to out discount each other. Thats what is happening in Christchurch at least.

Who said Stagflation?

Harder, Higher for Longer baby 👶

It would be nice if the comment's section was limited to people 18 yo +

It's a blue Monday, I am looking forward to some inspiration comments from TTP to perk up such a dull day.

It's a blue Monday, I am looking forward to some inspiration comments from TTP to perk up such a dull day

Hi Chairman Moa,

Agree with you...... Lately, we've been having a bad spell of wethir.

TTP

There's no such thing as bad weather, just poorly chosen clothing and shelter 😅

Sorry, "makechange", but you didn't get the joke (or maybe you just can't spell).

TTP

If you're going to make an spelling-based inside joke, at least spell your punchline correctly 🐏❌🥒

If one has to explain a joke or expect people to pick up on poorly communicated innuendo, it loses its element of surprise and is not funny anymore🤦

Yield curves yet to normalise - in my opinion, it is possible this recession is just getting started (ie we’ve witnessed the end of the opening act and the main event is the next 12-24 months)

Something which has been weighing on my mind is the possibility that when the curve does normalise, it may not do so only as the result of central banks dropping their policy rates. With all that is going on geopolitically, might we be entering into a 'new normal', in which longer term risk becomes even more elevated than it is currently, and the long end of the curve lifts another 50 bps?

If that were to occur at the same time that central banks made their initial cuts, might we see the long overdue normalisation, but without the short term relief that so many are praying for? Cast your mind ahead 6 months, and try to imagine a world in which the Republican Party steers American policy away from engagement with the world, and the ensuing turmoil that might cause.

If we see the OCR / Fed Funds Rate down to 4.50 - 4.75% in the New Year, with the longer end up of the curve lifting up near 5.00%, then we've reached the point at which things are said to be 'back to normal', but with little in the way of a break for the over-leveraged. There's a very real downside risk that you're right, and that 2025 turns out to be a right doozy.

US market starting to twig there is a serious refinancing issue in Commercial Real Estate, so many empty buildings coming up for refinance. I think we will see a rotation out of equities into bonds, could be very bad for tech stocks.

Concur.

Interesting to note too that this is longest period we've had with the OCR at peak rate. One has to ask the question why this bout of inflation control is different this time.

Longest yield curve inversion since 1920’s leading into Great Depression - does history repeat? (I don’t know but there are similarities in wealth inequality, booming share markets, excessively loose followed by tight monetary policy).

Because the central banks didnt put up rates fast enough, or high enough. So inflation became embedded and its dragging on.

Adjusted for population, worse than GFC.

And now try and reconcile the price levels we have today versus 2008.

No, it doesn't reconcile.

Down we go.

Bishop will be chewing on a cigar this morning...all part of the grand plan...right track

Bad news for buyers, it means that after winter the prices will start to increase again, mortgage rates around 5% by the end of 2025.

For those who think that they save money by paying rent and not buying a property, Rent is not going to be cheaper anytime soon, 3 bedrooms in North Shore, $900-1K per week

Google Endoparasites. Natures definition of blood from a stone.

Rents are actually starting to level off and without a sharp patch of immigration may start going down.

Prices on the other hand are just positioning themselves for a cliff jump.

Also say hello to your behind for me.

Rents are going to continue to go up.

Do you really believe that landlords are going to be wearing yields that are so much lower than the mortgage interest rates?

Reality is that they will only tolerate subsidising tenant accommodation for so long, so the rents get increased or they sell!

I would love to see more first home buyers as it is good for the economy and peoples wellbeing.

Truth of the matter is that it will not be happening in the overpriced locations in NZ.

Everyone knows that Auckland is far too expensive for first home buyers and the prices have been forced up by immigrants.

When interest rates go down, do landlords also drop rents?

If there is not the demand for the rental then landlords will meet the market and possibly lower the asking rent!

Personally never lowered rent on anything snd that is because we provide a quality product at a fair market value.

If we ever had a property that was not easy to rent to good tenants then it would be sold.

I can not talk about markets outside ChCh, but there is no doubt that rents are being increased significantly, to ensure that a reasonable yield on property value is achieved.

We are "accidental landlords" & we have just dropped $25.00 week of our tenants rent.

why did you drop the rent?

Lack of interest in your property?

what area?

Hey look a vulture

only tolerate subsidising tenant accommodation for so long

No, they’re only tolerating a bad investment for so long. Landlords do almost nothing productive, they do not build house (if they do I have no real problem with them). The price of houses could resolve negative yields by free falling after landlords figure out they can’t extract rents to cover their poor financial decisions and are forced to sell.

SKF

You are correct there are plenty of landlords that make terrible financial decisions and many that just should not be landlords.

There is plenty of skill required to be a successful landlord and make it profitable.

Part time landlords who pay property managers to manage their properties are relying on capital gain rather than cashflow.

Anyone can buy a property and rent it out and call themselves an investor / landlord, but running at a loss and propping up your investments is not really investing!

Anyone can be a landlord?

Go back forty years and the landlord visited the tenants on Thursday night to collect the rent…in cash! Fifty times a year. Can’t see many “investors” doing that today

got a block of twelve…drive home with a stack of cash and go to the bank in the morning

you needed a 10% yield to make a buck and pay the costs, same today

leverage? Oh yeah if you sold a large farm,business and knew a good solicitor

the whole thing has been turned into a lottery by the banks

I've said this a few times. The yield is so crap on rentals, only an idiot would invest. We appear to have a lot of idiots in this country.

Once again, thank you for your service to tenants. Heaven is a certainty

Look up 'carried over losses'. As the LL makes losses now, it offsets their tax bills in future years.

I understand that. But if you are pouring money in the front door on the monthly to cover the mortgage, tax losses carried forward are unlikely to cover this.

As a business, debt fueled landlording makes no sense, you are betting on the future earnings covering the current losses, - it's the definition of gambling.

The Man3: "Reality is that they will only tolerate subsidising tenant accommodation for so long..."

The reality is that LLs will do that for years.

Why? Unlike an owner occupier, LL's will simply assure themselves that it is fine to let the losses mount up as the carried-over losses can be used to offset their tax bills in future years. Who loses? The taxpayer! Who wins? The LL pocketing un-taxed capital gains.

And that sucks! Have I mentioned our tax system drastically needs an overhaul?

I can assure you that if there were any further taxes imposed on rental property owners, then property prices will increase more as well as rents.

Taxing anything never reduces prices, quite the opposite.

Yes with the mortgage rates at 7% puts our costs up from where they were but we are still positively geared overall, although we have not bought anything in the last few years for rental.

Prices have risen in ChCh to a point that it makes no sense to buy to rent out.

There are far better decisions to make money currently.

LOL prices wont go up until the stock overhang is cleared, the only thing that will clear it is dropping prices.

For those who think that they save money by paying rent and not buying a property, Rent is not going to be cheaper anytime soon, 3 bedrooms in North Shore, $900-1K per week

That is just patently false, even Takapuna has a median market rent lower than the bracket you've quoted..

It's almost crazy I'm paying over $20 an hour from my after tax pay in rent. Its a good place and cheap compared to what others are coughing up so I should be very grateful

If I dont get a place soon I'll get one of those mobile tourist homes and park it at the beach

168 hours in a week x $20/hr = 3360/week in rent?

I think they probably gets paid for near 40 hours a week not 168... So closer to $800/week is the answer you're looking for.

So a totally daft way of saying what they pay in rent. And an $800/week rental is either quite a nice place, or its a 3 bedroom+ place accommodating more than just the poster, ie probably their partner and offspring. Strangely enough, the more housing you require, the more you have to pay...

From one woof

Experienced buyers will use this opportunity to buy at the second “bottom of the market” and negotiate well. But, most will wait until they see more solid signs of recovery.

or the third or the fourth

I am waiting for solid signs. No point of timing the market really.

HPI for NZ: Jun 2024, 3573, down 2.0% for 2024 (HPI 3647 at Jan 2024), up 1.3% from 12 months ago (HPI 3528 at June 2023)

Number of Mortgagee sales in 9 months.

edit: Aww, you shouldn't edit your comments Yvil.

Did it ever occur to you that I had a problem on my phone while posting? My original comment only had the HPI number for June 2024, "3563" pretty obvious it was incomplete. So I completed it when I got connected again.

Don't worry, I forgive you.

Just out a few minutes ago....so much for the great kiwi property crash.

https://www.nzherald.co.nz/business/housing-prices-and-sales-drop-acros…

In Auckland, prices rose 2.4% from a month ago and were up nearly 5% from a year ago, to a median price of $1.05 million.

So Noel Leeming had a sale last year and they sold 1000 appliances for a median price of $2000

This year Noel Leeming had the same sale at the same point in the year and sold 600 appliances for a median price of $2100

"Great success" said the manager, our median price this year is $100 more than last year!

Next day he booked an appointment at WINZ.

And the 800 Warehouse Group Staff earning over 100k per year start a game of musical jobs.

It's time to create a clear separation between apartments/townhouses and stand-alone houses, townhouses are getting cheaper whereas house prices keep increasing.

That's why we need average price per dwelling, per sqm of land (Zoned Residential). The problem is there wont be historical data to properly compare it against.......but best time to plant a tree and all that.

Compared to when?

A house near us on a large flat section ideal for development sold a couple of months back for $1.4 mil, I reckon it would have got close to $2 mil 3 years ago. And even the standalone houses that are not good for development are selling for a lot less than 3 years ago.

This is the clear fundamental problem with all the "House" price figures coming out now, there is no distinction made on what is a "House". Now it needs categories because if over 60% of all new builds are townhouses then obviously house prices will be seen to be dropping when in fact they could be going up on your 3 or 4 bed house on that 500sqm section. My place is 175sqm two level so $4000 sqm that's $700K now just for the house, throw in the 550sqm land and all the other costs that's like $1.4m any day of the week replacement cost.

Thats definitely what is happening in Christchurch. In the streets around me, 4 bedroom family homes are selling for hundreds of thousands of dollars above 2022 CVs, while all the brand new 2 bed townhouses are sitting around for months still unsold, with developers forced to discount them (and more about to come on the market).

The first 12 paragraphs, more than half the article, are dedicated to the number of sales. Clearly, for RE agents who need sales for their income, that is important and it's very bad news. But for the vast majority of readers, price is much more important than the number of houses sold. Why not put a much greater emphasis on price, and ahead of the number of sales?

Because most of us are at a point where we understand that high inventory and low sales are a leading indicator to price, particularly when taking properties off the market is becoming an untenable solution for many.

See: 2022, but this time with less people employed.

Because that wouldn't fit with the photo selected...

IMHO I think what we are seeing now is a distortion due to wealth. Those at the upper end have money and are trading properties (albeit at a reduced value). And those at the lower end are not trading property.

This distortion is causing the market statistics to look better than they actually are.

Bingo!

Boys, the HPI is the value that adjusts these distortions… Educate yourself.

We are well aware but most of your spruiker comrades don't seem to be considering how often the median prices are coming up instead of the index figures.

It has been sometime since I did any serious studies in statistics, but I am doubtful that the median value can be that distorted with such a large sample size.

My only guess at the discrepancy between the median and HPI is the larger proportion of new houses being sold compared to the total stock. But even then that would tend to be a mean distortion rather than a median wouldn't it?

Median sales price is just that, the middle selling price. HPI is the indexed value for each type of property.

If the HPI falls 10% across the board, that doesn't change how much people have to spend on a house. They could instead be getting an extra bedroom for their money, or a slightly bigger section. You might also find the median is slightly higher because the marginal borrowers are not getting finance. But all just "reckons".

Within a defined area for the HPI there are still higher and lower valued properties so the distortion is still there, especially when the market is thin in terms of volume. So my comment still stands.

Barfoot's a week ago said their June 2024 average price was the highest since Dec 2021, lots of high end data is masking things by about 0.3% I think.

The fact that the Herald is asking how sick the property market is?, must be making the Spruikers feel sick.

What they actually state is that ASKING prices are higher than Wellington, which is a farce as it just means that there are more people in la la land in Nelson than in Wellington.

I follow the Nelson market as considering buying a place to retire to. Prices are not comparable to Wellington. My watchlist is a constant stream of price reductions. Looking like 2018 prices ...

The housing market crashed to Global Financial Crisis (GFC) levels in June.

Median house price in 2008 $395,552

Median house price in 2024 $770,000

(there was no HPI in 2008 to compare)

Well, when you lay it like that….

Looooong way down it will before any meaningful floor will be found.

Ouch.

Thanks for those figures. What they say is that over the past 16 years the price increases have averaged around 4% per annum - or probably less than the mortgage rate.

And of course history isn't an indicator of the future. Which is why the much proclaimed doubling of house prices every ten years over past decades isn't a projection for the future.

I have actually never heard the 'doubling every ten years' line from any optimist/spruiker on this site. It seems to just be a straw man fallacy from the pessimist/DGM side on this forum.

I have actually never heard the 'doubling every ten years' line from any optimist/spruiker on this site. It seems to just be a straw man fallacy from the pessimist/DGM side on this forum.

Run the data for yourself and confirm it against money supply growth and credit growth aggregates.

It's very real. Repeated a lot in MSM. And around BBQs. And by REAs. Most usually as the market is peaking to capture the 'greater fools'.

It's very real. Repeated a lot in MSM. And around BBQs. And by REAs. Most usually as the market is peaking to capture the 'greater fools'.

Chessboard and rice grains.

by Yvil | 25th Jun 24, 3:20pm

"Houses in NZ do not "double every 10 years"

Except that, looking at Interest's house price chart as far back as it goes, house values have gone up 7.92 times in 30 years. That's.... a doubling of house prices every 10 years, either you like it or not.

https://www.interest.co.nz/property/128405/prime-minister-christopher-l…

Thanks for finding that post NZD. It's quite amazing huh !

I put house prices double 10 years in the search box out of interest and came up with these:

An article about it: https://www.interest.co.nz/property/106963/house-prices-double-every-10-years-urban-myth-or-fact

by Zwifter | 17th Jun 24, 11:33am

Will be pretty happy to come back on here to talk about property prices in 10 years time. By then I will have saved a minimum of $400K in rent guaranteed and that's just for starters so yep, fully expecting my property to have effectively doubled in dollar terms in 10 years time.

by Zwifter | 19th Jun 23, 2:57pm

Not sure why people cannot get their heads around $2M house prices in 10 years time. The price of everything is going up, up, up so you just had better hope your wages have doubled in 10 years to match.

Did you know you can ask Chat GPT to search Interest.co for comments by certain commentators about certain topics?

No, I've never used it but I'm off work at the moment and looking for new things I can learn about so ChatGPT can be one of them, thanks.

Don't forget inflation - that $395552 in 2008 is $589372 today on general inflation (or $897903 based on housing inflation).

$400k equivalent to $590k mean it is not as dire as it appears at first sight, but still room to fall.

A key change is population - 4.26m in 2008 verses 5.27m today. That extra million people need somewhere to live and explains the demand for housing that provides a floor to prices - unoless they all go overseas.

Interesting - after 16 years with 4% annual inflation compounded annually, $395,552 would grow to approximately $835,105.78.

Chat GPT - If i've asked the right question;

To calculate the future value of $395,552 compounded annually at a rate of 4% over 16 years, we can use the formula for compound interest:

\[ A = P \times (1 + r)^n \]

Where:

- \( A \) is the future value of the investment/amount,

- \( P \) is the principal amount (initial investment),

- \( r \) is the annual interest rate (decimal),

- \( n \) is the number of years the interest is compounded for.

In this case:

- \( P = 395,552 \) (the initial amount),

- \( r = 0.04 \) (4% annual interest rate),

- \( n = 16 \) (16 years).

Let's calculate it step by step:

1. Convert the annual interest rate to a decimal: \( r = 0.04 \).

2. Apply the formula:

\[ A = 395,552 \times (1 + 0.04)^{16} \]

3. Calculate \( (1 + 0.04)^{16} \):

\[ (1 + 0.04)^{16} = (1.04)^{16} \]

4. Use a calculator to find \( (1.04)^{16} \):

\[ (1.04)^{16} \approx 2.1137 \]

5. Now multiply \( 395,552 \) by \( 2.1137 \):

\[ A \approx 395,552 \times 2.1137 \]

\[ A \approx 835,105.78 \]

Therefore, after 16 years with 4% annual inflation compounded annually, $395,552 would grow to approximately $835,105.78. This represents the future value of the initial amount accounting for inflation over the specified period.

Much of the worst damage is possibly done in Auckland, but there’s probably another few months of falls in many regions.

Hard to know isn't it. On the one hand we are probably at the top of the interest rate cycle, on the other we have loads of supply and very little demand.

Many regions are not being impacted, things changed post covid.

The data does not align with that opinion.

If the RBNZ adjusts both the LVR and DTI ratios to limit buyer's ability to borrow when the first cut in the OCR comes - as I expect they might (but they'll probably wait until it's closer to neutral, being 2.75%) - then they'll be little or no price response.

And yeah ... let's not forget the higher density zoning rules too which will mean more dwellings of much more variety being built once developers get going again due to lower working capital costs.

Flatlining for 20+ years looks like the most likely outcome ... Once we find a bottom.

Flatlining for 20+ years looks like the most likely outcome ... Once we find a bottom.

=======

What you're saying is ..."it's different this time"

It won't be any different. The market might flatline for a while, but will trend up, it always does.

Like it did in the 70s? Right?

No. Joking aside. I'm not saying it will be "different this time". I'm saying it will be much the same as in the 70s. And for mostly the same reasons.

No. Joking aside. I'm not saying it will be "different this time". I'm saying it will be much the same as in the 70s. And for mostly the same reasons.

From 1971 to 1979, the price of gold appreciated by around 2,300%, from USD35 per ounce to USD850 per ounce.

People need houses, they don't need gold bars......I've never figured out why anyone would buy a gold bar.

Pretty sure they listen to the spruikers like Peter Schiff about the great economic implosion that's always just around the corner.

You'd need to understand what a diversified investment portfolio is before you can understand gold.

I've listened to the gold spruikers for years - they might be rich, but none of their gullible clients are.

People need houses, they don't need gold bars......I've never figured out why anyone would buy a gold bar.

Agree. But I'm just pointing out what happened in the 1970s considering the person thinks that the near future will be similar. It's not a recommendation to buy gold. You buy the Ryman shares and others can buy gold if they wish.

Gold went vertical as dupes got sucked in by the "worthless USD", "running out of gold" and "gold is real money" BS.

There's a lot of suckers out there.

The biggest buyers of gold are central banks. The biggest private buyers of gold are Chinese citizens.

Central banks are civil servants with nothing to lose.

Most countries don't own any. It's an emotional trade, people get rapt up the BS posted by the likes of Peter Schiff and Jim Rickards.

Most countries don't own any. It's an emotional trade, people get rapt up the BS posted by the likes of Peter Schiff and Jim Rickards

I would suspect most Chinese don't know these two people.

You're probably right, for Chinese it's more than likely an emotional trade. It's nice to look at, therefore it must be good.

Your average chinese don't appear to be any richer than anyone else. China's chokka with poverty-stricken peasants.

Sounds a lot like Riverhead

I guess for aspiration they can drive across to Coatesville for a coffee.

Coatesville is NZ's most expensive suburb, and it's rubbing off to nearby properties.

Ditto for those in Wainui can hop over to Dairy Flat.Though Wainui is NZs next hot property market ... wait a minute

A sizeable chunk of Riverhead is owned by Fletchers, Matvin and Neil. And they're not in the habit of losing .

“Fletchers.” You are joking.

Not at all...Fletchers will not be going broke as you allege here. They've got assets of over $9 billion.

Conspiracy theorists thrive on the internet

That’s funny coming from you. I did not use the word broke. They make mistakes hence their share price. I have bought some recently hoping they make less mistakes. So far I am sitting on a good gain.

Surfs Up

I've been actively following (realestate.co.nz) a large number of properties in my area for about 2 years. All of these are standalone houses, similar in quality to my own, in central Auckland suburbs. A surprisingly (?unsurprisingly) large number were bought at some stage since 2020. I have never once seen one of these houses sell for more than what it was last bought for, and in many instances the discount is absolutely enormous, even where improvements have been made on the house. Nearly every single house I've followed has failed to sell at auction, and is then followed with a 'by negotiation', then a listed price (which often is revised down over time).

I can't speak for why there may be a small increase in median sale price, but I suspect it must have something to do with house selling at the top of the market. I have seen zero sign of a turning market. Just my two cents.

Yip I’ve been watching Dunedin the last 6-12 months as might need to move for family reasons. The reported data seems to show a flat market but very little is selling and everyday I get alerts for 5-10% drops on asking prices on houses on the watch list.

Yep. I suspect many new townhouses are struggling to sell, pushing the median up

From that article

There are more houses for sale than there are buyers, but the outlook for the market once rates start to fall is more positive. A year and a half ago we didn’t know when the Reserve Bank would call it quits on interest rate rises. Now, we know rates have hit a ceiling and at some point in the future they will come down.

Experienced buyers will use this opportunity to buy at the second “bottom of the market” and negotiate well. But, most will wait until they see more solid signs of recovery.

NZsheep, time to buy is now aye?

So how many are you buying, if not, why not...?

I've already bought. Outskirts of Auckland...can't miss. I've owned lots of properties, just gotta do the homework to identify your target.

I thought your wife does the homework?

Just goes to show how many of you guys hang on my every word.

You were providing investment advice to buy in Riverhead against all logical market signals and data. I tend to pay attention to that to see if there was anything to it as going against the norm is how you can make lots of money. Unfortunately it appears the Emperor was wearing no clothes.

I don't provide investment advice. Caveat Emptor.

Are wingman and rookie the same person?

My personal view (no evidence to back this up) is that Rookie is another 'persona' invented by the likes of TTP to try to spruik housing. He has a history of posting under different names and personas. It allows him to drop personas when they are proven to be wrong and also appear to represent a broader demographic.

No.

From that same article I don't understand how these two consecutive paragraphs below match up. Can anyone explain it to me?

"Property sales are up 13% year-on-year – a sign buyers have returned and that demand is picking up. However, there are some worrying numbers "under the hood". Annual sales are still below the long-term average of 81,100 per year, and the June sales figures from the Real Estate Institute of New Zealand suggest buyers are in retreat.

Nationwide sales were down 25.6% year-on-year and 32.6% month-on-month. The tally of 4356 was the worst for June since 2008. In Auckland, the situation was worse. Last month, sales dropped 35%year-on-year and 33.2% month-on-month to 1287 - Auckland's lowest tally for a June month since records began."

Spruiker's... if the mouth is mouthing, they are lying.

It's serious now!

Lots of keyboard warriors here without the courage of their convictions. If there's going to be a colossal housing crash like they're predicting, they should have sold up and gone renting.

You could always keep your last house and buy out of the money puts on Aussie bank shares....

up your game winger, no class at all

I've put my money where my mouth is, not many here have. I like housing, not gambling.

Shares are not gambling. Do your homework and watch them grow. Dividends are great when retired. It pays to be diversified. My broker has several clients who have equity portfolios in the $5-$10m range. People on average incomes who over a period of time created a diversified and variable portfolio. They never panicked. Bought more when markets had a dip. Now retired and have more income than they can spend. Every broker in NZ will have such clients. Humble astute clients on average incomes who had the courage and intelligence to buy good equities.

I've owned shares for decades, probably 50 years. I've seen all the manias and the crashes. I sold up after visiting the Auckland stock exchange early '87 and observing the mania in progress. The 87 crash wiped out a generation of 'investors', or should I say gamblers. A lawyer at a firm I was using shot himself....dead.

I still own a few. There's a lot of skulduggery goes on, shifty directors, pumping and empty holes in the ground. I'm not a fan of other people in charge of my money.

Tell that to the multi millionaires who just bought more after the 87 crash and GFC. They are very happy campers who only have one problem. How do I spend it before I die.

I've got a similar problem. I sold my last house for $2m (less agent's fees) more than I paid for it. And I've owned 14 others.

A tad better than that 1c a share divvy.

20 Hadlow Terrace, Grey Lynn, Auckland City, Auckland (trademe.co.nz)

A classic example of the disaster that has befallen anyone who purchased an off plan terrace house in 2020 or 2021. This example paid $1,160,000 in Feb 2020 as you can see on the trademe listing. It is now asking $959,000 and has been for sale since Oct 2023. A loss of $201,000 at asking price - there are about 80 similar units in the complex so owners currently sitting on a combined loss of equity of approximately $16m in that one complex in Grey Lynn.

Amongst all the doom and gloom, finally some good news verifying that the thinkers, philosophers and common sense practitioners are more perspicacious than the ponzi spruikers that infested society

Thinkers, philosophers and common sense practitioners are generally poor.

Many real estate investors are rich. I know what I'd sooner be.

River-Head or River-Dropping-Like-A-Stone

No one ever got rich being a keyboard warrior. People get rich taking risks and making good decisions, but I realise that's just not for you.

The builder I use has just hired 2 more tradesmen, he builds quality houses that sell. Not the kind of crap that I see being hammered up every day by cheap imported labour.

The builder I use has just hired 2 more tradesmen, he builds quality houses that sell.

Maybe he hired 2 more tradesmen because 2 left? I know, I know, you're trying to imply that despite the market tanking everywhere else, you have the nous to build in the right place, using the best builder who has a chocker book of work, you'll only use the best materials and in the process you'll make millions building on a flood plain next to a mothballed retirement village.

Pretty much. No, 2 builders didn't leave, they've got a ton of work. Flat out, while the keyboard warriors and eternal pessimists like you waffle on.

You obviously haven't done your homework, which is why I'm successful and you're not. You're suffering from the kiwi disease, you despise winners.

Armchair critics...hahaha

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.