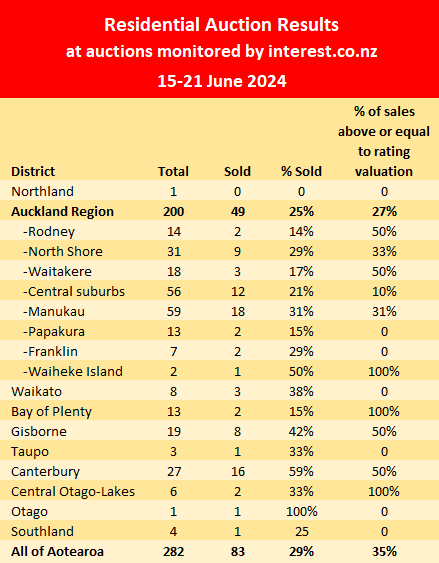

There was a winter nip in the air at the latest residential properties auctions, with fewer properties on offer and fewer being sold under the hammer.

Interest.co.nz monitored 282 residential property auctions over the week of 15-21 June, down from 301 the previous week.

Of those, 83 sold under the hammer, giving an overall sales rate of 29%, down from 33% the previous week.

That was the lowest sales rate in two months and the percentage of auctioned properties selling under the hammer has slipped from over 40% at the start of the year.

The sales rate was even lower at just 25% overall in the Auckland Region and 15% in the Bay of Plenty.

The table below shows the regional results from the auctions that were monitored last week while the details of the individual properties that were auctioned, including the selling prices of those that sold, are available on our Residential Auction Results page.

The comment stream on this story is now closed.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

126 Comments

Auction results similar to Cook straight Ferry's ..on the rocks.

Dont forget the pylon. Its been a big week for infrastructure and housing

And the RNZAF Boeing 757. Is it just me or are we on the march to becoming a third world country?

I don't think we ever became first world...defiantly C List only

You need to have substantial levels of human and financial capital to be considered first world.

We are pumping out high school grads who can't read or do basic maths and our "skilled" migration policies are a complete mess.

Household saving rates never meaningfully recovered after its GFC drop.

NZ businesses haven't built up much savings either since 2018 outside of their real estate assets. [Link] All those easy pickings from cheap money slushing around vanished into thin air and soon entire sectors will be screaming for bailouts.

You guys crack me up. I asked Copliot:

Yes, New Zealand is considered a first world country. The term “first world” originally referred to countries aligned with NATO and capitalism during the Cold War, and it has since evolved to describe developed, capitalist, industrial countries with relatively high standards of living, advanced economies, and well-established infrastructures.

New Zealand fits this description with its:

- High-income economy: It has a modern, prosperous, and developed market economy.

- Quality of life: New Zealand consistently ranks high in various global quality of life indices.

- Stable political system: It has a stable democratic government.

- Advanced infrastructure: The country has well-developed transportation, healthcare, and education systems.

So, in the context of economic development and global classifications, New Zealand is indeed categorized as a first world country.

Advanced infrastructure - I wonder what far north residents feel about this morning on that topic?

The pylon collapse was caused by human error not a lack of investment. As for the Brynderwyns and the state of roads in general. That’s a different story

And those humans undoing the hold down bolts at only one side of the pylon is not a product of our famous first world education?

Would this be a summary sackable offence or do the workers responsible have to have extra training and a warning given

The mayor of Auckland has weighed in with his assessment of the bolts

Well said Zachary but we must not forget that NZ was also the last discovered country in the world wether Maori or European. We have only been a western country for 200 years. Compared to say Britain wereby the Roman's were building roads, bath houses, sewage systems thousands of yrs ago. Also England had a train system going when NZ was literary just getting settled. So for such a young country we have coma along way. Yet we love to whip ourselves at hoe bad we are

Yes, and our population is tiny compared to our land area. We do amazingly well.

Yes. We are a first world country. But we have a segment of society that just bleats and moans about everything and blames everyone else for their hopelessness whilst asking everyone for a handout. They should really be shipped of to some third world shit hole for a field trip and they will that to realise that NZ they actually have it pretty good, and maybe also stop moaning.

The usual "Tuggers" will be along soon to put it back on course....

How long before the 65M 'band aid' package runs dry....and what of the hidden costs that users/consumers must wear for the disruption ? Wonder how much those replacements will cost now that the initial contract was ditched? I see debt accumulating here and the long term outlook is poor....some futurist should have gone to spexsavers....lol

Well worded double entendre. Though its the auction results we should be discussing, I cant help noticing that Gisborne is "banging" out higher numbers

I thought you are already here.

At least there is hope for the ferry..

I suppose the cheapo cost cutting current govt will just dedicate tugs to tow it back and forth for the entire term of their governance that is if they can refloat it and the hull /structure isnt damaged......... glad nobody was seriously hurt and that it didnt sink...

its a bad piece of water to be running old passenger boats, its not silly to say there is some serious tail risks.

International tourists spend a considerable amount of their travel money driving down to Wellington, crossing the strait and resuming their journey downwards to central Otago from Picton.

The current lot running this country can't understand the clear opportunity cost of not future-proofing the ferry fleet.

Dodged a bullet me thinks - 26 year old ferry beached as

Watching the housing market at the moment is like watching a speeding, out of control car crash.. in slow mo.

At some point it will have to stop whereupon it will need to be fixed up, restarted and driven somewhat more slowly and sensibly.

Friends of the family in their 80’s used their TDs to buy and move into a two bedroom ownership flat thingy and rented out their 4 bedroom family home of some 35 years. They had never previously owned more than their own home. They took this action due to the bottomed out interest rates imposed during the pandemic/lockdown etc making the TD income worthless. They had very good tenants right from the start but one lost work and the other had a bad covid experience. The old couple lowered the rent, right down. They reasoned as their old house was rocketing up in value they could afford to and in need go to a reverse mortgage. The tenants are still there, both working and well and the three children a bedroom each and going well and the rent is back to the market. A good story but the old couple still somewhat wonder why it became necessary in the first place. On reflection it’s rather difficult to decide what was worse, covid itself or the draconian government enforcements that impacted so deeply negatively on the nation and society at large.

Im no genius but it seems to me that pinning it all on Covid is a very long stretch of the imagination. Put the blame where it lays...GREED.

100%! Greed and FOMO.........

Oh greed is not novel. It’s one of the seven deadly sins afterall. So it hardly needs a kick start, does it.

Well back in the late 1990s property was an investment class, then due to serious tax advantage of LAQC it became fashionable and gains where tax free, by 2005 it was speculation driven, but still cheaper then offshore RE. it was peaky before the GFC but we only dropped 10% vs way way way more offshore, so we started from a higher base in the run to Covid, and perhaps only China, Canada had more stupid price to income averages at the Covid peak.

These auction results and recent trends just show that current bag holders cannot find a greater fool at these price levels, in fact many are selling below last sale so actually a slightly lesser fool is being found.

Due to its woeful super system, NZers will always be looking for a get rich quick scheme, if we fix super (compulsary from 18, paid for by employer - no TEC, and modelled on Aussie) we will both have funds for PPP infrastructure and a better future.... and be less vulnerable to asset bubbles.

Though the best protection is to just sit and watch, just like 1987 share crash put people off shares, this crash will put people off investment properties.

Good comment. As this downturn drags on, misfortune will gather apace and peoples regret by word of mouth will surely spread. Property was once aggressively promoted as a get rich quick scheme with the use of others money. Now, in particular for the heavily leveraged, it is a complete dog and an expanding number of regretful bag holders are losing sleep strategizing how to exit this mess financially intact. Houses should be for living in, not the speculation of assured and easily bankable riches.

It's looking increasingly likely, all COVID gains could be wiped out and possibly more. Like you say IT GUY, it was frothy even before COVID, warnings were being sounded. Post COVID gains in wages have been soaked up by the rising cost of living. Could we see prices revert back to where they were at the end of 2015? I wouldn't rule it out.

Edit

Some, but not many, are selling for less than they paid. My guess is 5%. Is that many?

Edit: I just went through the first 20 successful sales at B&T auctions last week and all except two sold for considerably more than vendors paid. One loss was -23K and they purchased in June 2022 - a pretty good result imho. The other a loss of 145k and had bought in 2021, a bit painful. If they are moving somewhere else then their new house will be cheaper too, so possibly no great loss. In the good old days it was expected you would lose if selling only a couple of years after purchasing. It's only been in recent years that people expect to make a fortune after only a short time.

Guessing now? It was 5% around this time last year. It's now obvious more bag holders are being forced to sell into a declining market as this unwinding grinds on.

"Corelogic data showed that 7.1 percent of homes that changed hands in the first quarter of this year sold for less than they had been bought for"

https://www.rnz.co.nz/news/business/517441/vendors-selling-before-bank-…

Well, that's not far off 5%.

Thats just the first quarter.

We're in June. Guess what direction this stat is trending in...

A reasonable wind vane I would think. Of course for the individual it’s not just the loss on the marker. On top of that all the RE charges, conveyancing costs etc and what about Brightline, possibly.

Yet even in boom times people were still selling at a loss. Some may not be affected much at all if they are moving house in the same market. Of course those who bought in 2021-2022 are likely to sell for less.

aaah - Zachary, if only such a dirty statistic could be so easily trivialized, if only :)

Let's not talk about the gamblers...i mean investors, who subscribe to the keep debt stacking to buy more rentals crowd. Many of them are in for a grand old time. You only need to look at any Facebook Investor group you like to see the pain that is coming.

From RNZ this morning: https://www.rnz.co.nz/news/business/520264/rents-dropping-housing-stock…

Rents dropping

It has been harder to rent out homes after a significant increase in rental stock in the past quarter.

Data from realestate.co.nz showed that while rentals had increased by 40 percent nationally over the last quarter, the number of rental seekers had increased by just 2.5 percent.

The website's data shows the stock for the same period is up by 40 percent for Auckland, 56 percent for Wellington, and 35 percent for Canterbury.

To all those people who said that restoring interest deductibility wouldnt increase rental supply and lower rents, don't you look stupid now?

"To all those people who said that restoring interest deductibility wouldnt increase rental supply and lower rents"

It would be interesting to know how many additional rentals are being added which are primarily motivated by the reintroduction of interest deductibility. Many recent buyers will still be cashflow negative.

1) How many properties are being added to rental stock due to lower house prices? Seeing reports of owners who wanted to sell but due to lower than expected prices, they have chosen to rent out the property in the rental market. The owners may have chosen to move into an apartment, move in with family, move into the granny flat, move into a retirement village, move cities (e.g move to Australia for better employment opportunities)

https://johnbutt.substack.com/p/50-growth-in-rental-inventory

2) How many properties are being added to rental stock due to owners moving abroad?

There are reports of those moving overseas for work renting out their home in NZ for a period of time to better assess whether their move abroad is permanent (& keep the home in NZ so they have the option of returning). Some friends who have found jobs overseas have chosen this option.

"Stats NZ figures show 81,200 New Zealand citizens left our shores in the past year, a 41 percent increase on April 2023"

https://www.newshub.co.nz/home/money/2024/06/migration-new-record-set-f…

3) How many properties are being added to rental stock for other reasons?

E.g

i) Airbnb is no longer profitable due to higher costs, higher vacancy rates?

https://www.oneroof.co.nz/news/rotoruas-airbnb-landlords-under-pressure…

ii) Holiday homes / baches / previously vacant homes being rented out due to higher ownership costs - rates, insurance, etc, or change in income situation of the owner?

Comments made in another article.

by

malamah

|

14th Jun 24, 12:01pm

Some fairly reasonable accidental rentals coming to market in Wellington. A lot of family homes. Undercutting typical rentals by $100-200 per week is what I’m seeing.

by

James Thrace

|

14th Jun 24, 3:57pm

This is us. Formerly owner occupied home. Spent money over the 15 years of ownership upgrading the ex state house with wood burner, double glazing and insulating every exterior facing wall. Escaped to Australia as no desire to live under a 3rd go around of an economically inept National government.

100 days on market. Dropped price by $125k. Last price was 35% below 2023 CV. No buyers.

As we only have a small mortgage, and including rates/insurance we were able to rent out for $150/wk less than other specuvestor properties. Prop mgr encouraged us to rent for more but we declined as we aren’t in the business of bankrupting tenants and well aware that National’s exorbitant additions to living costs for many which a derisory $2/wk tax cut will not change, means that renting for more = more tenants.

prop mgr found us a very nice couple, moving from their existing rental of 5 years due to that house being sold. By a specuvestor, ironically.

so yes, owner occupier “accidental landlords” who have relatively manageable mortgages are unlikely to be renting out at the maximum.

we also do have another rental property, and that was a near rebuild last year, so warm and dry, and being rented for less than market value as the outgoings aren’t ridiculous.

All good arguments, but all those things happened over the last year as well. ie. none of them have suddenly happened such as to make a dramatic difference in rental supply and asking rents in such a short time.

https://johnbutt.substack.com/p/inventory-charts

As you can see, there was no change to rental supply over the 12 months to March - yet people were still leaving, house prices were falling, people still tried to sell houses, interest rates were still high ....

The only "sudden thing" that happened in March 2024 that looks to have driven the significant and obvious surge in rental listings was the tax change. As I predicted, this would have (a) stopped investors from selling up to avoid financial armaggeddon this tax year, and (b) investors would have re-entered the much cheaper existing housing market where even First Home Buyers dont want to buy (eg. old 1-2 bedroom units) where rental yields are much higher than that on brand new yields.

You can pay $750k for a brand new 2 bedroom townhouse that rents for $550 a week (a 3.81% yield) or you can pay $385k for an older 2 bedroom unit that rents for $425 a week (a 5.74% yield). You do the maths.

https://www.trademe.co.nz/a/property/residential/sale/canterbury/christ…

"The only "sudden thing" that happened in March 2024 that looks to have driven the significant and obvious surge in rental listings was the tax change"

Also the ending of the summer selling season as autmn starts? Those who were unable to achieve desired prices may have chosen to take their properties off the sale market and rent out in the rental market until next spring when there are more active buyers.

Many who were leaving after March / April 2023 may have chosen to wait until the Nov 2023 - Feb 2024 spring / summer season where there are more active buyers. Especially given the price weakness in winter of 2023, many who were not time constrained, could wait to list to sell in the Nov 2023 spring season. Then when they were unable to sell during that period at an acceptable price, they chose to rent out to cover the cost of ownership - rates, insurance, etc)

Also interesting that 60% of the increase in rentals were in Auckland (over 2,000) in 2024 where yields are lower (with the exception of leasehold apartments in inner city).

Property managers who rent out properties on behalf of landlords will be best to see the types of landlords that they seeing who are listing their properties in the rental market. Would be interesting to know what they're seeing.

What do vendors choose to do when they don't get acceptable price offers? or offers below their expectations?

Anecdotal evidence of non time constrained vendor behaviour when they are getting unacceptable price offers from buyers. Seen similar behaviour multiple times by vendors in similar situations.

He and wife Sarah had dropped the price to as low as they were prepared to go and had a huge amount of publicity. “We weren’t prepared to drop it any further. We had done open homes most Sundays for about five months,” he said.

Unfortunately, the Nashs were unable to sell their home before settling on the courthouse so are now planning to rent the house out.

He told OneRoof that they might reconsider relisting it closer to summer when the weather was more conducive for a big house with a big pool and a big section.

FYI, from John Butt

"The change appears to be driven by sellers pulling homes for sale and putting them up for rent. This has happened before, they are called accidental landlords. "

50% Growth in Rental Inventory - by John Butt (substack.com)

"To all those people who said that restoring interest deductibility wouldnt increase rental supply"

K.W

Just out of interest, due to reintroduction of interest deductibility, are you buying in the existing house market to supply in the rental market (without any changes to the property such as add room, add minor dwelling, convert to boarding house, etc)?

If not, then why not? Perhaps the numbers still don't work at current price levels? In many locations, the numbers still don't work for income oriented investors.

For capital gain oriented investors, they may choose to buy.

I've seen reports of property traders who have bought last year and now having a tough time selling. Seen one listed for sale for over 9 months and still unsold.

You can buy older properties in the Chch market now that return 5.7% yields without doing any work whatsoever (and thats an example from a premium suburb, you can probably do even better in the crappier suburbs). These are properties that First Home Buyers dont want either, so investors should find it easy pickings now. The problem is going to be offloading those brand new townhouses that have yields half that of existing properties.

"You can buy older properties in the Chch market now that return 5.7% yields without doing any work whatsoever (and thats an example from a premium suburb, you can probably do even better in the crappier suburbs"

If you were an income oriented investor, would that be attractive for you with an LVR of 70% at current interest rates? It might be interesting if an investor is expecting interest rates to fall quickly. It might not be attractive for an investor expecting interest rates to stay higher for longer.

Might be attractive for a capital gain oriented investor.

And yet in my area the quantity for rent jumped a couple of months back on TM and has now dropped dramatically again

The -$23k loss tells you nothing of what was spent on the house. We would likely lose ~$100k or so on the house we purchased a few years ago, but we've also easily spent over $100k on it.

"Friends of the family in their 80’s used their TDs to buy and move into a two bedroom ownership flat thingy and rented out their 4 bedroom family home of some 35 years. They had never previously owned more than their own home. They took this action due to the bottomed out interest rates imposed during the pandemic/lockdown etc making the TD income worthless"

This is an interesting case study of zero interest rates on those who are in of need investment income.

Retirees who

1) are mortgage free

2) need investment income to meet living costs beyond those met by government superannuation.

Since bank deposit interest rates fell to zero, there was no investment income from their time deposits. Real estate offered gross yields above zero so the retirees rented out their prior home (likely to be worth more than their time deposit) to earn investment income for retirement.

They used their time deposit to purchase a new place to live which would be easier for 80 year olds to clean, and maintain with lower rates, insurance compared to the large house.

The purpose of renting out the prior residence was motivated by search for investment income, not capital gain. With interest rates at zero, there was no investment income, yet rates, insurance, maintenance costs were rising. There would have been many more retirees in that same situation.

"Friends of the family in their 80’s used their TDs to buy and move into a two bedroom ownership flat thingy and rented out their 4 bedroom family home of some 35 years. "

Does anyone else find it odd that not a single person has commented about the poor utilization (a measure of productivity) of two retired people living in a four bedroom home?

Just me?

My current street approx a dozen houses. Mostly 3 bedrooms on 500sqm sections.

Approx 8 single females (in 70’s - 80’s), 1 single male (90+) 1 with a couple in 80’s. Only a couple of families using all bedrooms.

Id say 80% of occupants will be selling their homes and downsizing in next 5-10 years as properties are too big/beyond their ability to maintain.

Entire suburb is similar - feels like a retirement village. 80% over 65-70.

I think there’s going to be a big transition coming soon. In 20 years most of these people will be dead or in care.

One key variable of the downsizing decision is the health of the occupant.

If health deteriorates and independent living is no longer possible, then downsizing is quite common.

Elderly occupants are comfortable with the community and lifestyle, & may find change associated with downsizing uncomfortable with an entirely new living environment.

Another key variable of the downsizing decision is proximity to children & grandchildren.

Studies have shown that elderly people benefit from remaining in their existing homes and continuing their normal routines, as change is disruptive and has cognitive and other health impacts that can lead to an earlier death. If they are going to move, they should move while they are still able to cope with the changes such as getting rid of their possessions, navigating the financial and legal house sale process, and re-establishing community networks. Leave it too late and it can be traumatic and result in isolation, loneliness and advance ailments like dementia.

An alternative is a live-in carer.

I know of a few retired people that have rented their own homes out and live rent free (and usually with no other costs) looking after people 20+ years older than them. One even does this while spending 6 months in Europe and 6 months in NZ with their travel costs paid for as well. (An ex-nurse.) Very cheap way to live in a well to do area.

what's the average price on your street

Likewise, our street is old 1920's properties on 1/4 acre +. Many old retirees/empty nesters that will eventually find it too difficult or costly to maintain the properties (gardening etc).

It might happen earlier. Rates alone might force them out. If I were on the pension with rates around $9,500 next year, while the pension pays $27,000, then 33% of my income would be going on rates.

I'm careful to differentiate between "covid" and "the covid response". I believe that the response with its associated economic impacts will ultimately lead to more loss of life than had we had we stuck to the official pre-prepared pandemic response. Yes, said in hindsight but if we don't critically analyse what we did we will make the same mistakes next time.

What use is this data other than noting 1/3 sell at auction in a falling market and 2/3 sell at auction in a booming market?

Did anyone force you to look at it? It's definitely a leading indicator prior to other lagged monthly data

Exactly, Greeneggsandham.

Very active today aren’t we…. Feeling the heat?

I think it was my early morning workout and breakfast of beef liver and eggs.

I've actually found myself in a rather strange position of having a foot in both camps due to losing my nerve back in 2018. Back then I suggested that property investors should reduce debt. When COVID came I was feeling a little smug and then horrified when, bizarrely, house prices shot up. Now I'm kind of neutral. However, I like to call people out when they are being overdramatic.

Facts are "overdramatic"? Interesting take.

Both of the following pairs of statements are factually correct.

A)

1) The glass is 50% full

2) The glass is 50% empty

B)

1) The glass is 93% full

2) The glass is 7% empty

C)

1) 93% of property sellers in the last quarter have sold above their purchase price

2) 7% of property sellers in the last quarter have sold below their purchase price

No, people are overdramatic.

Area dependent results, Canterbury and Gisborne are holding up the "tail", Auckland has the "hump"

Still amazed people are pushing auctions. Auction fail. Price by Speculation fail. List a 2021 price fail. Finally banks come knocking and it's bring me an offer.

All the while in a declining market 3-4 months have passed by making it worth less. Greed and stupidity.

Does this article show how many properties sold shortly after auction?

no but the REINZ data includes all and is most recent

The great majority sell after the auction. Some are withdrawn from the market. Auction is often just the first stage of the marketing process and costs the vendor about a grand.

To be fair, a 29% chance of an unconditional sale, in less than a month, looks pretty good in this market!

Yes but IMHO the prices achieved are pretty average... so it indicates people who really want/need a sale are using auction with a realistic reserve... the rest not so much

"Still amazed people are pushing auctions"

Is that due to real estate agents recommending that method of sale to vendors so that vendors pay for marketing costs? I think that real estate agents have a profit element in that payment by vendors.

Don't vendors pay for marketing costs regardless of sale method? I get the impression Averageman thinks the whole marketing process starts again when a house is passed in at auction. What happens is the agent goes and puts some sticky tape over the auction date on the for sale sign.

Averageman: "Still amazed people are pushing auctions."

Why are you amazed?

Perhaps you've not noticed, that even in this less than positive climate, some sales show two, or more, bidders (for whom emotion got the better of them) paying considerably more than other sales methods would have achieved?

The best City in NZ Christchurch, continues to outperform others with a 59% success rate under the hammer.

Steady as she goes with people opting to move to ChCh for liveability!

Until the next earth quake...

Do they have a super rugby team?

Have not seen them on TV lately

Think Crusaders felt it was time for someone else to win it!

59% success rate is very impressive for winter.

Perhaps its telling you that AKL is still too expensive rrealitive to incomes vs CHCH, lots of AKLers moving out, offshore and south.

AKL is a very expensive city to live in. Hours in traffic, Big city violence

Christchurch ain't all that flash either... remember the shootings? Cheaper ain't always better.

As long as you went to the "right" school CHCH is a friendly place.

I went to Cant Uni, yeah the right school helps. Plenty of white trash suburbs in Chch to avoid....

$1.7 million people vote that Auckland is right for them. Better weather, lovely harbour, and job and business opportunities. As people leave people arrive in Auckland and for good reason.

Mostly immigrants, not many head to Auckland nowadays, as too many issues.

Of course they go to Auckland , this needs to stop!

Chch has had the most stable property market for a long time.

It has been voted the most happy city in NZ but most intellects already appreciate that!

The shootings were done by an Ozzie.

And as a result it should have been immigrants who had been resident in NZ fewer than ten years that were banned from having a firearms licence. Instead they used the opportunity to target ordinary kiwis instead.

IT GUY: "AKL is a very expensive city to live in. Hours in traffic, Big city violence"

Thought I'd check your "Big city violence" assertion.

Using:

1. https://www.police.govt.nz/crime-snapshot

2. https://en.wikipedia.org/wiki/List_of_cities_in_New_Zealand

CHCH has more violent crime per capita than AKL. And more per capita crime overall.

Be the Aucklanders coming down for a better lifestyle.

Nar maaate. Just the endemic, white trash Chch suburbs, doing the crimes they always do.

Aucklanders say no to crime.

To be fair, per capita statistics for Christchurch doesnt really reflect the actual city population these days since so many people live in Selwyn and Waimak Districts. They still come into Christchurch though to buy their drugs and beat up people at the bus station.

Has it become less racist, small-minded and bigoted in recent years?

Still full of bogans...

Probably not, that is why it was voted the happiest city in Nz!

Depends. It's still pretty bad but improving. Go to any kind of city council community type meeting you'll find plenty of racist selfish homophobic retirees who want nothing to change (housing zoning changes, road changes, any cycle ways of any kind, anything that might bring on the future). You know, it might cost them an extra few bucks or force them to open their minds! We don't want that now do we.

Auction clearance rates have been mostly 25-39% in the past 12 months, so 29% in mid winter is hardly surprising. It's a "nothing to see here" headline, but already around 50 comments.

We treat the Saturday auction report like a weekend footy match.

One month is a long wait for the regularly scheduled REINZ HPI food fight….

It came out. Short food fight. MSM did not report it (which is odd).

https://www.interest.co.nz/property/128281/house-prices-falling-vendors…

When the headline is downbeat, some will even resort to complaining about grammar, spelling, editing or even the number of comments made.

Go figure 😆🤣

Grammar and spelling are important under any circumstances.

"Lets eat people"

"Lets eat, people"

Yes, I see where you're coming from. Grammar saves lives. I wonder how many people have died because of me?

Any other thoughts on your mind today retired poppy as well as eating people and tugging.. maybe people are dying to be you, and reincarnate as Retired-Poppy

Here's a couple that might be more relevant:

1) House prices are crashing.

House prices are crashing!

"House prices are crashing"

House prices are crashing?

2) House prices have bottomed.

House prices have bottomed!

"House prices have bottomed"

House prices have bottomed?

Also, when using (appropriate) words like "Eejit", it doesn't necessarily mean the commenter can't spell.

"Nek minnit" is also acceptable.

The funny thing is Waitākere area sold 3, but 50% over the CV, that is mean 1.5 over the CV, how that accounted? Actually truth is only one over the CV🤣=33%

Yes, glad i'm not the only one to notice it. The table data is nonsense (for the % sold over CV at least). Manukau, 31% of 18 sold over CV.. hmm, 6 would be 33%, 5 would be 27%, so 5.5 sold at above CV?

One common way of judging whether housing's price is in line with its fundamental value is to consider the ratio of housing prices to rents. This is analogous to the ratio of prices to dividends for stocks.

~ Janet Yellen

Blues and chiefs are both boldly sponsored by NZs dominant industry, Barfoots, platinum homes on their shirts

I was expecting RP to troll you on your comment, but he must be in bed already. Never mind.

Guaranteed that he will be back tomorrow.

Yes I want to see egg on his face again, seems to be avoiding me now haha

There can be no doubt that our house prices are under some pressure. Recent data from VNZ and the REINZ put that fact beyond doubt. The number of listings coming onto the market daily puts more pressure on existing listings that are sitting around. When a blast from the past comes back to comment incessantly about how wonderful their patch is you know it’s actually the opposite and it’s currently tough. If you are comfortable with where you are at you say nothing. If you are in fact feeling insecure you brag about how great things are. When in fact they are not.

That's not true.

Yeah. Def not true. Maybe it’s the case for some, but that does not make it a rule.

170K loss, or much more on this new build beauty, just purchased 2 years ago, by a silly and hapless Kiwi:

2/472 West Coast Road | Glen Eden | Waitakere City | Houses for Sale - One Roof

Sadly, buyers today, could be in for another 100 to 200K loss, as all this sucker is worth, is at best under 400k in 2026/2027.

These losses and destruction of wealth in NZ Property is life changing and just eyewatering!

Will NZ inc, make it through this once in a lifetime, major property crash? Not so sure.

Not for a long time. This is going to change people’s attitudes like the 1987 share market crash did. People are finding out in a real hurry that holding an asset that is rapidly falling in value, encumbered by a lot of debt and that you cannot quickly sell is really really painful.

IRISH Bubble facts - House prices in Dublin, the largest city, were briefly down 56% from their peak and apartment prices down over 62%.[3]

Impacts

- Approximately 31% of mortgaged properties, or 47% of the value of outstanding loans, were found to be in negative equity at the end of 2010.[76]

- As of September 2011, Central Bank figures show that 8.1% of private residential mortgage accounts are in arrears for more than 90 days – up from 7.2% at the end of June 2011.[77]

- As of August 2012, more than 22% of Irish mortgages are in arrears or have been restructured.[78]

- In the first 10 months of 2011, 8,692 houses were completed. This compares to 76,954 in 2004, 80,957 in 2005, 93,419 in 2006, 78,027 in 2007, 51,724 in 2008, 26,420 in 2009 and 14,602 in 2010.[79]

- The Irish National Debt has significantly increased: Ireland's ratio of General Government Debt to GDP at the end of 2009 is estimated to have been 65.2%. The revised estimate for General Government Debt to GDP ratio at the end of 2010 is estimated to have been 92.5%. The forecast for General Government Debt to GDP ratio at the end of 2011 is estimated to be 105.5%.[79]

Facts and figures

- Up to 12.6% of the Irish workforce was employed by the construction industry.[80]

- Up to 9.4% of Irish GNP was dependent on construction. Of this new residential housing construction made up nearly 7% of GNP.[81]

- The P/E ratio (Total Price divided by annual earnings) for private housing reached an all-time high when, in March 2006, a Davy Stockbrokers report suggested that for prosperous Dublin suburbs the ratio could be approaching 100 times. Davy stated that these ratios can only be justified if investors were extremely bullish about rental growth. Given the plentiful supply of rental properties in these areas however, Davy suggested that it would be an adjustment in property prices, rather than rents, that would eventually bring valuations down to more realistic levels.[82]

- Although housing indicators like price to income ratio and rental yields were worse in many other countries, high price per square meter and unsustainable Irish economy indicated a bubble.[83]

Agreed. Leverage in reverse as greed fades to panic is indeed a tough place. Self inflicted though.

By any international measure, this NZ property bubble is at best mid-pop.

I myself, looking at buying another owner-occupied property and fully expect any new purchase to drop at least another 50 to 100K over the next 12 months......unless a low ball gets accepted. Buyers market 100% for the next 2 to 3 years.

Sellers currently have ZERO power. Bottom is years off.

Policy settings created the boom 2020/2021. Policy settings created the bust 2022/2024. Policy settings could easily recreate a boom 2025/2026.

Do you think the RBNZ wants core inflation to hit 7% again?

I think that the RBNZ is more likely to want unemployment to hit 7%. However I suggest that neither outcome is going to be acceptable to the country as a whole.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.