House prices declined for the second month in a row in May as vendors appear to be becoming more realistic in their price expectations.

According to the Real Estate Institute of NZ , the national median house price dropped to 770,000 in May, down from $790,000 in April and $800,000 in March.

The national median price was also down 1.3% compared to May last year.

However, the more important measure of price movements is the REINZ's House Price Index, which adjusts for differences in the mix of properties sold each month.

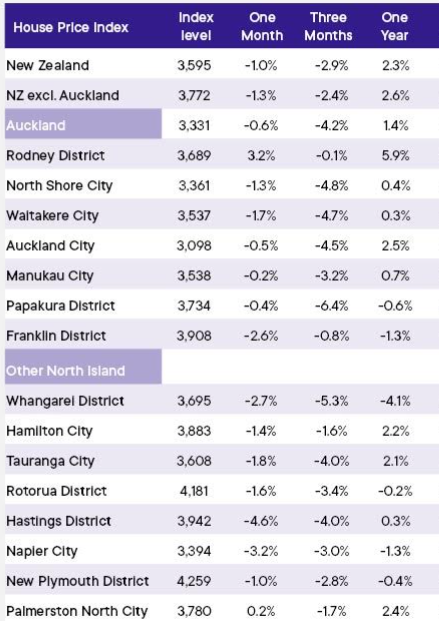

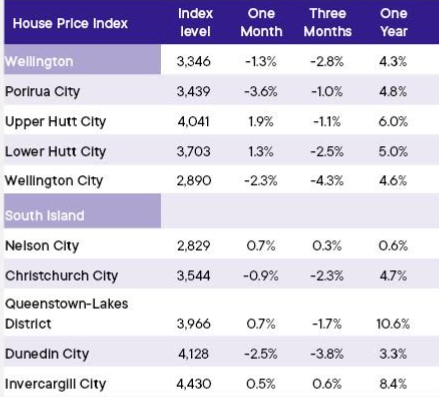

This shows that across the whole country, prices have declined by 2.9% over the three months to the end of May and in the Auckland Region prices are down by 4.2% over the same period.

Significantly, prices have declined in every region of the country except Nelson and Invercargill, which were up 0.3% and 0.6% respectively over the last three months.

The biggest declines were in Papakura in South Auckland -6.4% and Whangarei -5.3% (see the table below for the full regional figures).

But as the old saying goes, every cloud has a silver lining and the drop in prices appears to have stimulated sales, with the REINZ reporting 6303 residential sales in May, up 8.0% compared to April and up 6.8% compared to May last year.

Unfortunately on a seasonally adjusted basis, sales in May were down 4.9% compared to April and in Auckland they were down a whopping 11.9% compared to April, suggesting the lift in actual numbers in May may not be sustainable over winter.

"The seasonally adjusted figure is an important indicator of the underlying market trends," REINZ Chief Executive Jen Baird said.

"With a continued flow of new options coming to market adding to a large level of stock, this does provide a lot of choice for buyers and a sense they can take their time to make decisions," she said.

The comment stream on this story is now closed.

REINZ House Price Index - May 2024

Median price - REINZ

Select chart tabs

Volumes sold - REINZ

Select chart tabs

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

225 Comments

Oh I was close for NZ, 1.3% down versus my 1.2%. But Auckland not as weak as I expected.

Regional NZ very weak

Regions have to catch up with past AKL WGTN falls while the center is about to leg down again

Looks like Rodney the only thing holding Auckland back slightly..

Auckland excl Rodney down -1.33% month on month.

No interest rate relief in sight……

Chilly months ahead for some. 🥶

TTP

Has your account been hacked

I reckon it would be healthy to stop be-littling people for re-aligning their beliefs. I think for people reading comments TODAY, what TTP is saying is relevant. Why can’t we just agree to agree?

Owing to recent undeniable events, Tothepoint has been left with two choices. Either disappear altogether or to continue efforts to reinvent himself. If that fails, his plan "B" is his other username "Mypointis"

It's highly unlikely this Property Broker will ever accept any wrongdoing on here.

I would gladly appreciate his comments if they didn't flicker like a light bulb

At a general level, a sign of growth is to update one's opinions as we learn. To belittle change of opinion is to promote a culture of lethargic ignorance rather than being able to adapt to emergent insights.

I haven't tracked TTP, but I presume you have been holding yourself to account before passing comment across?

TTP has been Spruiking his guts out non stop since BEFFORE Nov 21....., and has only recently changed his tune.

Even The Comb has changed... only the Church of Ashley left to repent.

I am one of few on here who called -10% Dec 23 to Dec 24. At least I am consistent and if not correct will accept it.

The amusing thing is that the professional Spruikers have backed away from predicting price gains... while we have a raft of new clowns on here both calling the bottom here and saying prices will be up by xmas.

The irony is there are folks backing these clowns.. I guess it's clowns square

Many of the IDs may be the same clown.... I think its a one ring sized circus

Tothepoint, due to vested interests, and despite brokering FHB's absurd debt levels, never wanted the party to end. It wasn't a consideration until it actually did..

by tothepoint | 3rd Sep 21, 8:39pm - "NZ house prices are increasing - on a sustainable long-term trajectory"

As we all know prior to COVID, the housing market was already frothy, there were warnings being sounded from nearly every corner. Personally, I never saw COVID coming nor the rock bottom interest rates that set the housing market on fire yet again and therefore mine and other well meaning predictions were proven wrong and I openly admit that.

edit

Sure. I read those and laughed then whilst skipping past bull traps.

TTP then changed tune.... So what?

I'm genuinely curious...

Is it a frustration that spruikers have encouraged people to make decisions that have since lead to financially ruinous circumstances, and then don't say sorry or own the consequences of their self-serving use of their influence? Or something else?

Are there social contracts at play even on a relatively anonymous website like interest.co.nz? 🤔

Also they spent many years playing the man and not the ball.

Their inability to present a cogent counter argument based on facts to counter the perspectives of the house price bears. The only counter argument was extrapolation of historical house price growth. So they chose to repeatedly attempt to discredit the fact based perspectives of the house price bears through repeated negative labels.

And the potential huge vested financial self interest at work.

Their historical pattern of behaviour has caused many to question whether that person is trustworthy.

Fool me once, shame on you. Fool me twice, shame on me.

To belittle change of opinion is to promote a culture of lethargic ignorance rather than being able to adapt to emergent insights.

That's an exceptionally nice sentence. Isn't the English language great?

oh oh.. Someone forgot to take his daily medo..

Auckland's stronger data is down to a big bounce in the Rodney District (up 3.2%). I am not sure why that is bucking the trend. Any ideas?

Around Omaha/Matakana the more expensive homes are selling. Everything over $7m has sold. A lot of the other stuff is sitting on the market or been pulled.

So it might be a change in mix but unsure if this would be enough to come through.

-JH rates

-Job ads back to 2016 levels

-Job cuts just starting to come through

-Migration numbers starting to reverse

the housing market is in for a thrashing

We’ve come along way since Nov 2021….

Rational minds have de-leveraged and reconsidered the true value of NZ property over the last few years.

The rest? Well, buying the dip and HODLing (Hoarding) will teach many some valuable lessons about this Neanderthal approach pedalled by the greasy RE industry.

↘️

Wonder if Yvil will eventually understand that vendors are getting realistic..

I know he is a bit slow, but he seems to be struggling to think logically

Speaking of which, the YOY percentile might be along shortly to tell us all it's still up. This is nothing more than a Memorial Service for the dead cat that will no longer bounce.........

Play the ball, not the man....

Lol, now he has a bodyguard

Maybe some of us are tired of personal attacks on other commenters...

Hardly. I just get sick of trawling through the daily reams 'tit-for-tat' squabbling, when I'm hoping for contributions that will 'help me make financial decisons'.

Houses Overpriced is apparently not engaging with me anymore, as per his post of 2 days ago.

by Houses Overpriced | 15th Jun 24, 10:36am

Please reserve your insightful comments to those that deserve a response, Yvil is definitely not in that category

Just an observation, Yvil also often makes a specific reference to the Interest.co byline that is "Help you make financial decisions".

Digital fingerprint?

???

Nope, I'm me. Don't currently own a home, and effectively locked out of the market since a 2018 divorce. If I had to choose a camp, I would definately be pitched in the DGM side of the field.

Often riled by some of Yvil's comments, but more sick of the bickering amongst the usuals.

So stand down Dan, we still have a while before Interest comment section is just a handful of folk duking it out with their multiple accounts!

"Don't currently own a home, and effectively locked out of the market since a 2018 divorce"

Households on a median or even high single incomes are priced out of the house ownership market in many geographical locations in NZ.

Even more financially difficult to own if there are children involved.

by Houses Overpriced | 17th Jun 24, 9:34am

Wonder if Yvil will eventually understand that vendors are getting realistic..

I know he is a bit slow, but he seems to be struggling to think logically

Are you sure I'm slow HO? It looks to me that I was ahead of time and absolutely spot on!

by Yvil 7th Mar 24, 3:44pm

As I said at the beginning of the year, I'm still expecting house prices to start dropping in price, starting from April 24.

by Yvil | 31st Dec 23, 1:20pm - Housing is more difficult to predict, because huge immigration and more property friendly laws by the new government should normally provide a lift in sales and prices, but there are huge unaffordability issues because of the high interest rates, so I think prices will be mostly flat.

Some Spruikers find honesty to be quite a challenge. Sometimes they need a little help to get there....edit

.

Starting to resemble a Briscoes sale.

More like a closing down sale

Looks like those predictions of 10% down by Christmas for Auckland are looking increasingly likely..

More like 20%. Its accelerating.

+

You left the word Guaranteed out 😝

Look at this https://www.oneroof.co.nz/news/auckland-woman-emerges-triumphant-after-…

That headline is so misleading, so far from the reality of what happened, so patently biased that you can smell the desperation through your PC terminal.

Nest or Invest, Charming in Christchurch, meet the market

I have more respect for the local Indian vape dealer than One Roof journalists.

Its like an episode of The Block. Except mostly successful.

Oneroof.co.nz is a platform for listing properties for sale.

Since it is owned by the NZ Herald, many readers of Oneroof.co nz believe Oneroof.co.nz articles are independent and factual news.

Note the vested financial interests on Oneroof.co.nz. Remember the articles are all free. So what is their business model?

Oh dear.

Prices holding up suprisingly well in the face of the RBNZ crushing NZ. Rate cuts will send prices firmly upwards again from the end of the year.

It's always a positive HPI report in Spruiker-land

He has a point though - prices are still up 2.3% in the last year.

And prices probably will stabilise or even go up slightly if interest rates go up.

Of course in real value (after inflation) prices have dropped quite a lot.

Nah, he doesn't have a point. Prices are up 2.3% from the bottom of the trough 12 months ago. Since then, the housing market experienced a brief rebound, prior to the aggressive falls resuming - more commonly known as a bull trap. The comment is just an example of a spruikers' coping mechanism.

Property themed humour, love it.

"Rate cuts will send prices firmly upwards again from the end of the year."

Which year is that? 2025?

Amazing how many people are completely unaware that prices are dropping. Once it becomes the msm narrative the buyers will evaporate.

Long way down yet.

Wait until the new Auckland CVs come out and the general public loses their collective shit.

OneRoof estimate calculator has recently dropped on a lot of property I think around 12.9% down on average for AKL CVs

This will be a huge turning point. As there is still a significant contingent of the uneducated, spurred on by agents, who still think paying 2021 CV is a baseline, and an even larger chunk who think getting a couple of percent under CV is a great discount.

Pity the central interceptor isn't connected yet,that unprecedented volume of collective shitting might end up on the beaches. It's climate change( in the housing market) for sure!

The people buying now are those who need or want a home. Presumably the investor class is more than aware of how the larger market is doing.

The stupidity of covid is being unwound.

The stupidity of people thinking it's sustainable.

The stupidity of our response to covid is being unwound.

The stupidity of the RBNZ's response covid is being unwound ... Taking NZ Inc. with it.

(The Aussie banks have run rings around our RB. They must be laughing at us.)

Harder & Higher for Longer baby.👶

Stagflation next stop.✋

Stagflation is already underway

Lol. Hilarious.

Evidence please.

I think there was a whiff of it last year but not anymore. I think inflation is pretty much dead and buried.

Until the next offshore economic shock over which we'll have no control because we never plan for them and therefore have no systems in place to mitigate their effects. Rinse and repeat to ensure wealth gets accumulated at the top.

I also called it last year, but some said unemployment wasn’t rising much and that was a key aspect of stagflation.

Inflation is nearly dead and buried

Hope so. History shows that inflation is always difficult to put down. Lets see what happens.

"History shows that inflation is always difficult to put down."

History shows no such thing.

Since the formation of central banks, given the right to control the cost of money (interest rates), every bout of inflation in countries with central banks free from political interference has run to a standard pattern that can be defined as: raise interest rates, hold them too high for too long, create a Recession, inflation dies, rich get richer.

Averageman: "What more do you want...?"

Stagflation (with a capital 'S') isn't measured in quarters but in years.

I just re-read that BNZ nonsense ...

They open with ...

The New Zealand economy is currently in peak stagflation: two quarters of negative growth; a labour market that is unsustainably tight; and inflation miles above the Reserve Bank’s target.

Note that Stagflation is both negative or very low growth (in real terms) and high levels of un-changing unemployment and high levels of un-changing inflation. And yet they note that the labour market is 'tight'? That fails the basic Stagflation test. (I note this is the only time the word is even mentioned. And it's mentioned for a sensationary effect to capture the eyes of the gullible.

And as we know now - inflation has been falling while unemployment has been rising. That's recessionary and, yes, we're in a Recession. Stagflation it is NOT.

If you're gonna use a word, best know what it means, ay? But if you want to use it wrongly, you can. (We'll adjust our understanding of your intellects accordingly.)

What's the Luxy to do to help out the poor land lords..any ideas welcome.

The NACTF has already done enough so that those that want too can hang on.

The wiser will be selling up as they know changes to allow far greater densities have nailed down the tax-free capital gains coffin for 20-30 years (or more).

Also Water infrastructure bills are thashed out - example (Palmerston North $1,000 per year for the next 30 years mooted on top of standard rates).

Better than "Co Governance" I suppose.. lol

What are the changes that allow for greater densities? Seems that this issue is well under debate after National indicated withdrew from bipartisan density agreements. Just asking as I haven't seen much actual policy. Does Auckland go back to the Unitary plan or is there other plans in the wings?

"Does Auckland go back to the Unitary plan or is there other plans in the wings?"

Look up Plan Change 78. It is an update to the Unitary Plan for the NPS / UD. It is currently before the Independent Hearing commissioners who have been working away at it for months, if not more than a year. Expect at least another year(?) before it is 'defined' and becomes operative (most likely 'operative in part' as the finer details are sorted out). Many Councils, including Auckland, have asked for extensions.

Remember National and Labour got together and introduced the MDRS? Well, National reneged on that deal and has allowed Councils to opt out if they wish. This won't affect Auckland much as the Unitary Plan of 2016 had similar zoning rules already for much of Auckland.

Kate, are you over where things are? (It's as clear as mud to me at this time.)

Thanks for that. I agree things are as clear a mud a this stage.

Wellington also recently voted for massive upzoning so the MDRS repeal will not affect them much if at all, correct?

That's what a relative who lives down there told me. (They do some property dev on a small scale.) They didn't say 'massive' but it was welcome and very necessary.

Stuff covered it in an excellent 6 week series. It's worth reading the whole series to get a feel for how NIMBY''s hijack the process and how "independent expert" panels are neither independent nor expert. The council voted against most of their recommendations and Chris Bishop endorsed the Council's decision (something he deserves credit for).

https://thespinoff.co.nz/politics/14-03-2024/live-updates-wellington-ci…

From what i understood, Bishops plan is that councils can only opt out of MDRS if they come up with an alternative plan that re-zones 30 years worth of supply to be immediately available for housing.

That is my understanding too.

for people who wished house prices drops, here is your time to celebrate. enjoy!

This party is only getting started.

There is room for you too, we are inclusive

sure thing. I've got my popcorn.

"The seasonally adjusted figure is an important indicator of the underlying market trends," REINZ Chief Executive Jen Baird said.

"With a continued flow of new options coming to market adding to a large level of stock, this does provide a lot of choice for buyers and a sense they can take their time to make decisions," she said.

The fact that REINZ need buyers to make a rushed decision like they are buying a toaster as opposed to their largest asset says a lot.

The fact buyers have more time to make considered decisions at the moment should be the norm and celebrated. If it means buyers are making considered sensible decisions for themselves long term. That has ultimately got to be good for them and for the country.

Of course the vested interests will always be pushing to keep the market in a state of an artificial supply crunch.

So if my house was 800K, now it's 770K

Hahahaha...

Once the rate start going down, after the winter, I'll ask for 850K or even 870K and sell for 830K

I hear staging companies give massive discounts if you hire them out for 6 months or a year.

One of the funnier comebacks I have seen for a while

I've heard that staging companies are offering full fit out packages, so vendors can AirBnB the property while its on the market.

So yeah, losing 2.5K in value per week. Not exactly insignificant

Losing anything at all is significant !!!

Houses are a one way bet for financial riches in NZ, don't cha know?

"Houses double every 10 years."

"Safe as houses".

"You'll never lose money buying a house."

Must I go on?

Will be pretty happy to come back on here to talk about property prices in 10 years time. By then I will have saved a minimum of $400K in rent guaranteed and that's just for starters so yep, fully expecting my property to have effectively doubled in dollar terms in 10 years time.

My analysis confirms that very, very few houses double in value every 10 years. (And very, very few owners of rentals are making anything like as much as they say they are.)

Doubling in 10 years is 7% PA. It wouldn't be a particularly amazing return if it wasn't for the tax advantages.

Leveraging capability is the real advantage with houses.

It was a pretty bad "advantage" if you did it 3 years ago. Probably best case you lost all of your money, many will come out also owing a lot of money.

Kiwis are quite happy to borrow 70-80% of the price of an asset that has been highly volatile in the last few years, but will baulk at investing a few grand into a blue chip company. Shares are just too risky!

1987 share crash vs safe as houses. And all the Spruikers selling houses as a leveraged super plan .... looking at you Poopeller Property

I think you misunderstand me. I leverage against my property to invest in the productive sector, shares included.

I pay interest of 5-7% on a home loan. If I were to take out a business loan id be paying 12% plus.

...... looking up Spruiker manual for answer

Spruiker Manual Advice for Negative Equity .... - Tell them just to hold forever, inflation will fix all issues.

Except its 7% on a big chunk of money like $1 million and you get to live it it saving money on rent if you own it. The payback once you clear the mortgage is next level, I guess people need to experience it for themselves the difference it makes in your life. Probably not surprised that most people who come here cannot see the big picture.

You were claiming the rent saved as part of that 7%!

I am not surprised that property has been a good investment, I'm just saying it hasn't been that amazing compared to other options. And I doubt it will be anywhere near as good over the coming decade, especially if you bought 2 years ago.

There will be a lot of people who read and comment on this forum who are mortgage free or close to it, but they still get on with making a difference in their lives and those of others, they don't need to continuously talk themselves up on this forum like you do.

national median house price dropped to 770,000 in May, down from $790,000 in April and $800,000 in March.

The stand off looks to be unwinding and it was vendors that blinked first (no suprise there, but it is surprising how long vendors were able to hold onto their various forms of copium prior to capitulation and realisation of the new market ↘️↘️↘️↘️⬇️↘️↘️↘️⬇️

I've never seen someone physically type out their mental breakdown before.. quite bizarre!

When you wake up from your dream, you'll realize it's actually worth 600k

You'll like this one. We traded up in late 2021, paid around $900k. Just checked the ANZ app, it's now valued at $700k (about the same as homes.co). What's interesting is about 12 months ago homes.co had our place "valued" at over $1m, but it's now $700k.

Fortunately we had a 50% deposit, thanks to the generous FHB that bought our overpriced first home, which according to homes.co has also dropped by a very similar dollar amount.

Agre seems to be a consistent scenario across the Auckland area

"We traded up in late 2021, paid around $900k. Just checked the ANZ app, it's now valued at $700k (about the same as homes.co). What's interesting is about 12 months ago homes.co had our place "valued" at over $1m, but it's now $700k. "

Thank you for sharing.

I hope your household finances are still manageable with higher mortgage interest rates and you're not experiencing cashflow stress or mental stress.

Would be interested to know your perspective of the property promoters with their vested financial interests.

We're fortunate to both earn fairly healthy incomes so no financial stress here, a DTI of less than 3 and a 5 year fix runs out end of 2026.

Everybody has an opinion driven by either financial vested interests, or wishful thinking. That is spruikers or bears. While everybody is entitled to an opinion, people who are deemed "subject matter experts" in property should be held to higher account than Joe Bloggs and be censured when their prediction is wildly off. Just throwing "opinion" as a tagline shouldn't be a suitable caveat.

For example, Tony Alexander who boasts 25 years as a Chief Economist would be seen by many as a subject matter expert. If you told someone to "do their own research" before buying a property, Tony would be up there on their list of research material, it's even on his website. How much has he gotten wrong?

My aim: “To help Kiwis make better decisions for their businesses, investments, home purchases, and people by writing about the economy in an easy to understand manner.”

Interestingly I just checked my home sold end of March for well under CV. Funnily Homes.Co still has it as TBC.

It would certainly not be helpful for the other homes currently in the street/area if it was up and displayed.

The suppression of truth. Record sales are posted near instantly.

Reduced price transparency by those with their vested financial interests when prices are falling leading to lower house price expectations by potential buyers?

Yes i dont know how they get away with $TBC as the sale price for so long ,noticed it used when the sale price is lower than expected . clearly against the law https://www.oneroof.co.nz/news/ndas-legal-loopholes-and-paranoid-rich-l…

So much reporting on house prices, as if it's part of a thriving economy!

You non-starters are hilarious jizzing your panties over NZ HPI down 1% on the month.

I can't hear you over your bank smashing your door down.

How does a ridiculous comment like this get through moderation?

Well the racist ones do so lower your expectations abit..

Plus the constant repeat offending trolls

Don't be so hard on yourself.

You’re one of them - always coming to have a troll of me. 😂

At least pompous8 occasionally has something intelligent to say, when he leaves behind his vindictive and childish trolling and self-righteous pomposity 🥳

Might want to change your undies then champ as i think all your spruiking will give you some skiddies once acceptance finally hits....

https://en.wikipedia.org/wiki/Five_stages_of_grief

If u measure the drop price in USD (account for the NZD Exchange rate drop) and account for inflation.

Everyones losses are catastrophic.

My shares are performing very well mind you, business is booming. And house prices dropping is very good news for nz economy in the mid to long term

All is well people.

Auckland City median price up 18.5% year on year and 2.3% month on month!

You take that crumb of happiness and hold on tight!

As it stands, there appears to be a belief that falling interest rates will save the housing market (without exception) and that when this happens, prices will be on the rise. While I agree with this over the long term (ie over periods of decades) I don’t agree with it in the short term.

As I witnessed in the US during the GFC, falling rates were correlated with even faster price falls in housing. Once price falls become embedded in the psychology of society, it can take years to turn the sinking ship around. Falling rates are also linked to deflationary forces and rising unemployment - neither of which a positive contributors to asset price increases.

My guess (a guess like everyone else’s opinion) is that we are more likely to see further price falls as the OCR is dropped, as we are to see either flat or rising house prices. 2020 during covid was an exception given that the government kept everyone in employment/bailed everyone out - but that isn’t possible at every recession - if that is done, then we don’t live in a capitalist society/economy - we may as well live under communist rule where the government chooses who (what businesses) lives and who dies and not the free market. If this is true, the price of housing will be irrelevant as the state controls the prices and will dictate who lives where and what you own. This isn’t a future I would like to see.

Accurate. Spruikers don't understand that the worst unwinding may happen when rates start to turn as any positive feedback will take over 12 months to feed in.

Yes until yield curves normalise, which they haven’t yet, then I don’t think we can talk about a recovery or rising house prices. So I think we may see 12-24 months of falling prices are the yield curve normalised and recession really kicks in.

I’ll let everyone know when the yield curve normalised on here - but noting that it’s now been inverted the longest since just before the 1929 crash - hope no correlation between this and a subsequent depression - but given how extreme (reckless?) we’ve been with monetary and fiscal policy from GFC until now (and the euphoria involving asset prices such as housing, shit coins, tech stocks etc) who knows what might be ahead of us.

Another massive bailout would only further embed the issues we currently have (high inequality, problematic inflation, drop in living standards eg GDP per capita)

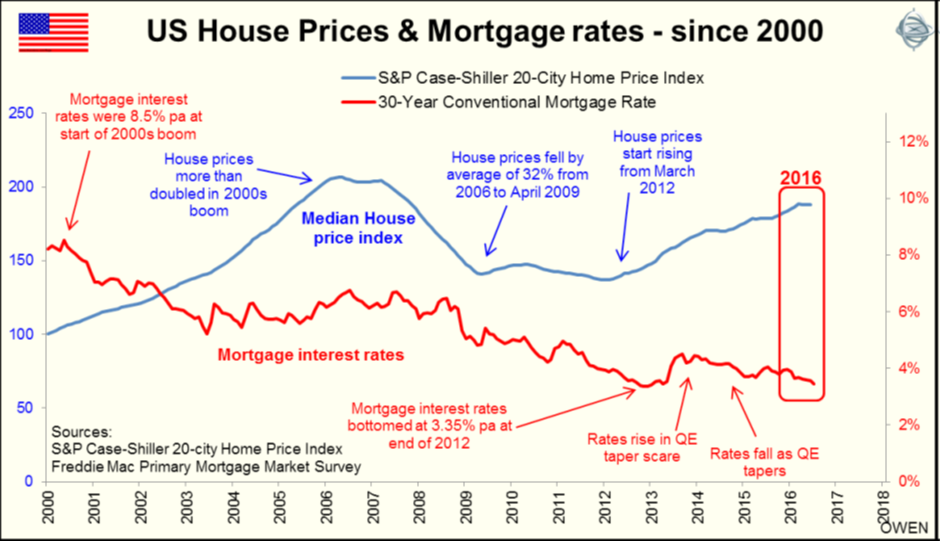

I think historic NZ data suggests that house prices are much more responsive to changes in mortgage rates than you might expect. This chart shows the dance quite nicely.

House prices are almost completely based on interest rates (in the scenario where supply is less than demand). The price is set by what people can afford to pay, and what people can afford to pay is set by interest rates.

This assumes that you or partner or 10% of the people on your street don’t lose their jobs/income. And that tenant in rentals don’t lose their jobs so as to afford to pay the landlords rent.

Otherwise I agree with your statement (in the long term - eg 5+ year) but not always true in the short term in rising unemployment and risk of deflation.

Yes good point. Although investors can flatten that out a bit, for example if interest rates dropped now to a point where yield made sense again I think investors would jump in as there is always people needing to rent regardless of the economy.

" if interest rates dropped now to a point where yield made sense again I think investors would jump in as there is always people needing to rent regardless of the economy. "

Only for cashed up investors or investors with lower LVR's of debt.

Many property investors took on the maximum levels of debt that were available at or near the peak.

With house price falls, the LVR's will have risen, meaning many will have insufficient borrowing capacity unless house prices rise. Without house price rises, many will be unable to use the widely used financing technique of equity release / deposit recycling. This how the higher house prices led to higher house prices without the debt servicing constraint - it was a positive price feedback loop.

For property investors with their portfolio in Auckand or Wellington, with allowed LVR's of 65% for investors, this would mean a property investor at the peak with an LVR of 24% or below would have the necessary available borrowring capacity to finance using equity realease.

That 24% LVR would now be 30% LVR due to a fall in price, leaving 35% to use as a deposit on another purchase in the same area.

With lower purchase prices in the regions, a property investor from Auckland or Wellington might look to those areas.

Maybe. I suggest many sensible investors saw the peak for what it was, unsustainable.

adds..... And how many investors are boomers who are more focused on cashing out than investing in?

Where will the new 'investors' come from?

They are gone, the age has passed, the notion that property is the game to be in is dead and buried. Folk are now just trying to survive, they do not have the capacity to gear up in the huge numbers needed to buy the 'investment' properties about to hit the market.

You over leveraged, high maintenance rot box is now a liability, not an asset. A consumer of cash as ownership costs spiral.

Wake up call time.

That only covers the exception that I mention above (covid in 2020) and a non-recessionary period prior.

How long post GFC did it take for house prices to rise after the massive drop in interest rates?

here you go - what do you think?

The index chart is a bit easier for most people to read

The NZ index has prices flat for around 4 years when interest rates were halved after GFC (end of 03-07 boom) - but most regional cities like Dunedin, Palmy etc were flat for closer to 10 years

https://www.opespartners.co.nz/house-prices/nz

Opes are NZ's biggest spruikers (self-styled property economists and all) but they do have some good data

Your chart starts at April 1992 with an average houser value of $110,000, 30 years later it shows an average house value of $875,000 almost an 8 fold increase in 30 years, or put in another way, a doubling every 10 years. Don't get upset, I'm just telling you what your chart states.

Here's a fun fact:

Did you know that house prices in Melbourne took 60 years to recover in real terms after the crash of 1892?

https://www.macrobusiness.com.au/2014/12/the-history-of-australian-prop…

My only comment would be that look at how far the OCR had to drop to prevent a deflationary depression and level out house price falls. Edit - immediately during the GFC time period.

Thus time house prices are already down 20% before the recession after having just stimulated the economy with war time like monetary and fiscal policy (during covid). Anything is in the cards from my perspective - including a falling OCR and simultaneously house prices for 12-24 months (see how the two lines were falling in parallel during the GFC?).

In my view the big spenders in the current environment are cashed up boomers living it larger with better returns in their TDs. If a contraction starts, and TD returns fall and their net worth falls on paper, they may well and truely close their wallets and we find ourselves in quite a few hole with big drops in spending - a deep recession would likely follow.

Or they re-discover the stock market and BBQs go back to total nonsense-fests.

"here you go - what do you think?"

[Warning black humor follows]

The RBNZ hasn't a clue what its doing? Too slow to raise. Too slow to drop. (As far as house prices are concerned, anyway. But that's the whole economy, right?)

Hey - Here's an idea ...

1. The RBNZ should just toss a coin each MP review and randomly raise or lower - and by random amounts - just to confuse the property market. I

2. Accompany each MPS with random phases about property copied from past MPSs.

(Note: I'd recommend monthly or fortnightly MPSs to heighten the entertainment value.)

Well - I suppose we're getting half of that idea now.

USA - mortgage interest rates started dropping in 2007, but house prices didnt bottom until 2009. Then they stagnated until 2012 when interest rates finally bottomed out. So its not the beginning of interest rate drops that stimulate the housing market, its the end.

https://www.firstlinks.com.au/uploads/wp/US-house-prices-mortgage-rates…

{kind=link}

"This chart shows the dance quite nicely."

It shows a conditioning phase between 2013 and 2017. Followed by absurd adjustments in the OCR with Pavlov's dog doing exactly what it had been conditioned to do. ;-)

Agreed.

I'd add that I expect quite a flatline in real terms as, once interest rates fall a tad, building will pick up again (assuming all the builders haven't left) and supply will increase again enough to meet demand (unless government opens the immigration flood gates again).

Interest rates will need to fall by more than a tad.

both sides of the funding equation (funding for developers to proceed, funding for buyers to buy) is reliant on interest rates falling by at least 1.5% minimum.

Until then it’s not going to make a meaningful difference

A 'tad' is enough for builders as they'll assume a full 1.5% (or more) by the time their build is finished.

That is correct. And its true in places like Ireland as well. Reason being is that interest rates were cut due to the economy falling into recession, and it was the recession that drove house prices down. So if the Reserve Bank decides that the NZ economy is so dire, that desperate measures like an interest rate cut is warranted, then dont expect house prices to boom in response. The economy will still be stuffed, people will still be unemployed, and businesses will still be going to the wall.

"So if the Reserve Bank decides that the NZ economy is so dire, that desperate measures like an interest rate cut is warranted, then dont expect house prices to boom in response. The economy will still be stuffed, people will still be unemployed, and businesses will still be going to the wall. "

The narrative that house prices will rise and bounce back as soon as interest rates start falling is being perptuated by those with vested financial self interests.

Owner occupier buyers: CAVEAT EMPTOR.

To be fair many on this thread wanted house prices to drop and to be more affordable to FHB so they did not need to be so chained to debt that could strangle them when unexpected life events happen.

A slow drop is preferable to a very sudden large one so articles showing small decreases of 1-5% (often considered the levels of sampling errors), are actually to be celebrated. As they are around the level of sampling errors we cannot be sure the moves are significant or for the suitable kinds of properties for FHB families (e.g. a bunch of 1 bedroom apartments in the city dropping like a stone or mansions having high variation in sales prices are not unheard of compared to affordable housing suitable for families).

Ideally the more stringent tests on DTI will help prevent some of the worst investments.

But more market drops please. The country as a whole needs it as even with 3 incomes NZ housing is unaffordable.

Well said Pacifica. I'd maybe go a step further and the ideal outcome for NZ as whole would be flat nominal prices with steady real falls.

.

I believe the worst is yet to come, we purchased a house in Hamilton in April 2022, and have recently listed it for sale as we are moving to another town for work, so far we have dropped the price roughly 10% from what we paid for it and there are only barely a few nibbles. Watch this space I reckon.

Unfortunately it doesnt even account for the fact that inflation has risen say 13% since you bought it and the NZD has dropped around 10%.

So in 'real terms' its worth maybe 25% less than you paid for it.

A big bounce in Rodney district this month against the flow (up 3.2%). Does any one have a hypothesis for why?

More affordable than other Auckland regions with nice beaches. The new motorway- Penlink being built which will make commute times into the city faster.

Yes must be the motorway. I considered buying there, probably would have if the market wasn't so bad.

More affordable😂 your checked out ara hills dev

House prices up 2.3% over 1 year... I'm confused why DGM are getting so excited?

The comments are identical to comments I read on Interest back in 2010 post GFC when property prices fell and then look what happened.

The property I purchased in 2010 for $500k when supposedly the market was in free fall is now worth $1.3M.

I bought my first home in 2010 for $195k. a three bedroom cross lease on hamilton lake. Many people on here said I was mad.

Is that really that great over 14 years? ~7% return P/A. I guess when you add the rent (after expenses) too its pretty good, but not particularly amazing.

With rent and capital gains I averaged 14% p.a. until I sold it in early 2023. So I was pretty happy with its performance.

Did you exclude costs - rates, insurance, maintenance, etc? And also did you exclude your time, any investment can make a good ROI if someone is working for free.

I guess the fact most of it is tax free really helps too. And the fact you can easily leverage it.

Yes. Yes. and Yes.

Disclaimer: my good news story in property should not be taken as a suggestion that all property decisions are wise. But generally, anyone who bought in 2010 when many on here were saying there would be further crashes, is happy they did.

I agree it was a good investment. You are probably the best case scenario in terms of buy and sell time so not exactly the typical return. If you looked at the best case scenario with shares or Bitcoin etc it would be many magnitudes higher!

For what was considered such an amazing period of house price increases, the actual returns weren't that amazing, especially after factoring in the declines of the last 2 years.

Apple shares were $11 in 2010, they're now worth $212.

Yet you cannot live in apple shares and cannot house a family in them. To have money for housing you would also need to sell the shares or have significant other amounts of capital. So any gains also would need to be offset with housing costs suitable for a family over the same period to be a better comparison.

"Is that really that great over 14 years? ~7% return P/A"

If he typically put a 20% deposit down, so used $100k of his own money, it's a return of 800%, rather good !

I wouldn't expect the same thing happening like after GFC.

there was a 10 year super lower interest environment, I don't see how we will have another super lower interest rates for the coming years at all.

Best case we have similar interest rates to the last decade. That won't increase prices, just keep them stagnant (maybe they match CPI).

Worst case interest rates stay higher than last decade, in that case house prices could actually decrease over 10 years.

Not until you sell it Dellboy

There does seem to have been a bit of a turn though don't you agree? 12 months ago media spruikers (e.g. TA and the banks) were talking about big house price increases this year (esp due to National), but now we have excessive stock, declining prices, and very quiet spruikers. I would say 2024 will be a negative year for housing.

I’m trying to better understand Rodney performance for the month and quarter and year. Why is sitting as an outlier from the crowd. Is it just as simple as people want to live in Rodney and will pay for the privilege, mix of sales probably screwed towards new houses or what. Any insight?

Im trying to figure this one out myself. I am not sure if REINZ include hibiscus coast in their data for Rodney. If so there will be a ripple effect from Northshore growing strongly in late 2023, high rent inflation, and the imminent opening of the Penlink that will bring many homes 20 mins closer to Auckland CBD.

Also, properties near the beaches have weathered the HPI storm really well, and just about every house on the hibiscus coast is near the beach.

Edit <Also the new mahurangi motorway to Warkworth>

properties near the beaches have weathered the HPI storm really well

Source?

Anecdotal.

Vendors with houses near the beach may be sadly disappointed when they realise their potential buyers can no longer get borrowing. Banks have been publicly announcing for some time that they are assessing their exposure to properties that could be impacted by coastal flooding.

Where I live beach front houses are not selling. In fact anything over $1.3m are not selling. Times have changed.

Move to the Gold Coast. Apparently its immune to climate change. Waterfront properties still selling for millions. Guess the only difference climate change makes to house prices is how media and insurance companies choose to exploit the narrative.

https://www.domain.com.au/news/a-big-milestone-gold-coasts-median-house…

i’ve been following Omaha market closely. data is from realestate.co.nz. some trophy houses on the beach sold for $8m+ vs $5m RV earlier on the year but now there are 20+ properties for sale vs none 2 years ago. They aren’t selling though. Failed auctions and eg only 1 offer post-auction which was 47% below independent Feb’24 valuation and 20% below RV. vendors expectations have not shifted and several preferred to take their properties off the market. it only takes one desperate seller to hit the panic button though and all the auto-valuations are re-written.. as they were on the way up, so they will be on the way down…

I live in Rodney, the only thing I can think of is perhaps we have less forced (motivated) sellers. I do see a lot of property for sale, lots not moving, expect a downturn towards end of 2024. We never saw the madness of Manurewa or Papakura rental suburbs...

This market is total nonsense for buyers, as I am.

Deadline sales actually linger several weeks past the due date, due to lack of offers, or single offers. Agents try to push me making offers only hours before the deadline, like you could make such a big decision in such short time... But I don't rush and magically the dealine doesn't matter at all anymore.

Negotiations? I threw a few offers I deemed realistic based on the REINZ figures, most often I'm the only potential buyer, still it's impossible to get anywhere with sellers, they want to meet 80% their way. Of all those properties over the last 3 months, only 1 sold (my back up offer was 30K more than what is actually sold for, but I was conditional of course), others have been either withdrawn or put for rent (at stratospheric prices, probably to fully cover the mortgage if sellers have bought an other property).

Advertised prices? Well, at or above end of 2021 CV...

"Agents try to push me making offers only hours before the deadline"

Many agents try to create pressure on buyers to transact. In many circumstances, the deadline may be an entirely false time constraint.

Caveat emptor to buyers, if a real estate agent is attempting to pressure any buyer to buy what is likely to be the largest purchase in their life respresenting 500 - 2000% of their entire net worth.

FYI - My watch list in Dunedin properties today has multiple asking price drops of 5-10% of current market value. This is a daily occurrence now. Houses on watch list is growing longer - not much selling. If these properties sell, at these reduce listed prices, then the next 3 months days of HPI could be more than the last 3 month 3.8% drop.

Tony will be reporting on FONGO soon

You reported this less than a week ago? But we are behind you hoping you can find the home of your dreams

"Recognizing downturns and being brave with purchasing is key to not buying in euphoria and having your financials stacked against you"

https://www.wwfp.net/resources/the-economic-comparison-of-owning-or-ren…

When in situations where owning is dearer than renting and house prices are steadily falling, for now, the sun is beginning to shine for euphoria averse saver. I think the above is excellent advice!

154 comments already. Some commentators joyful, some in denial as always. One thing is for sure. Prices are going to drop for some time yet. Too much weight from listings increasing. Gravity is hard to overcome. Buyers need to buy very very well as they are clutching a falling knife.

Yes if buying today only offer -30% lower than the asking price, or walk away.

Ten of thousands of cuts hands, cannot be wrong.

This worries me .Pressure is on to reverse the foreign buyer ban , i can see the govt caving

https://www.oneroof.co.nz/news/million-dollar-agents-urge-rethink-of-fo…

They are speaking their own vested financial self interests. There are very few local residents and other eligible buyers in their segment of the market - even fewer in a recession.

Here is the potential unintended consequences of that policy.

If foreign buyers are allowed even at the high priced segment, then the local sellers may be receive large amounts upon sale. Then they use these proceeds to buy up at lower price points (with leverage) & continue to outbid local resident owner occupier buyers and this trickles down to the first home buyer market.

If foreign buyers were allowed, then perhaps follow Singapore's stamp duty policy on foreign buyers with a stamp duty of 60%.

Singapore's tax policy is structured to give the highest priority to local citizens and resident owner occupier buyers.

Should NZ resident owner occupier buyers be given priority over foreign buyers?

Foreign buyers who are non residents should continue to be excluded. But currently the foreign buyer ban also includes non-New Zealanders who live here on non-resident work visas. How do we expect to attract highly skilled workers (like CEOs, Surgeons, Rocket Scientists) here if we block them from buying a home for their families to live in? And for international tax reasons, most of them don't want a permanent residence visa, they want a temporary work visa so they are not paying tax on worldwide income or assets.

Ditto for the international student market - wealthy students who actually want to come here for the education (not the visa rort) also cant buy a place to live in while here studying for 3-6 years. At an open home on the Gold Coast recently I encountered a young medical school student who was looking for an apartment to buy which her father will pay for. I thought to myself, well thats one highly educated and skilled University student that would never have considered studying in NZ, let alone staying permanently.

Can we all finally agree that the market is crashing?

Every time we refer to this as the market crashing we get a justification for why it isn't. Surely the excuses have run out ...

When the crash trajectory started a couple of years ago it wasn't crashing because the house prices hadn't dropped 20% in real terms, even though it was clear that was the trajectory

Then when they did actually drop 20% in real terms it wasn't a crash because they hadn't yet fallen 20% in nominal terms

Then when they had actually fallen 20% in nominal terms it wasn't crashing because we'd reached the bottom so couldn't be crashing

Now it's clear prices have fallen 20% in nominal terms (much more in real terms) and they are still heading down.

The market is crashing ... What's the next excuse?

If its crashed officially it must be a great time to buy?

Never throw a Spruiker an olive branch, this is not even 1/2 crashed...... no no crash at all, its merely a flesh wound.

Shock property tax rise hits landlords, holiday homes

John KehoeEconomics editor

Landlords, holiday homes and businesses in NSW will be hit by a $1.5 billion increase in land taxes, which the real estate industry warns could cost owners thousands of dollars a year and be passed on to renters.

NSW becomes the third state Labor government to target multiple property owners with higher taxes, following a bigger land tax increase in Victoria and a tax hike attempt in Queensland that was abandoned.

the things in Australia puzzles me. they had interest rate hike, and yet their house prices kept going up and up.

Some reasons come to mind:

1) There is still negative gearing on residential real estate. So residential estate is attractive for high income earners

2) expat Australians returning to Australia

3) bank of mum and dad continues to finance buying.

On housing affordability:

Lots of internationals buying in cash. Interest rates have little affect on them.

Negative gearing is still a thing here. So people throw their income into keeping the investment property a thing and incur less PAYE.

Plenty of “first home buyers” who buy a house only to rent it out as the tax benefit of doing so is more advantageous than living it it themselves.

tis why I think only owner occupiers should be allowed to claim back interest and maintenance deductions against their PAYE earnings.

in a logical world, it would result in an eventual mortgage free home. The equity is then used to leverage into an upsized/new home for the owner occupier with their old (and mortgage free) home being used for rental income.

either that, or sell off the old home for a lower mortgage on the upsized/new home.

If you know first home buyers who buy and rent the house out, then they are investors and nit first home buyers.

They still have the cost of their accommodation, in other words not financially beneficial at the moment.

I used the term generally to apply to people who are buying their first home.

negative gearing is more tax advantageous for them to do so as the cost of their own rental accommodation is effectively treated as an offset against their PAYE income so less tax to pay.

NZ got rid of negative gearing under Key iirc, yet Australia retains it.

New Zealand's problem is that buying a rental property is viewed as a typical kiwi's superannuation scheme. But, this can't work for everyone, it's unsustainable. My brother-in-law just permanently moved back to Christchurch so that his wife could be near her family when they have kids. He is 34 and withdrew $120,000 from his superannuation in Australia. That's not unusual. Typical balances are in the hundreds of thousands. Compare that to kiwisaver, in 2022 the average balance was $27k in New Zealand and $147k in Australia. For someone near retirement aged 60 to 65 - the average male balance is $400k AUD. Those figures are just jaw dropping. Add to that, the incredibly disadvantageous tax settings relative to Australia - where contributions are a compulsory 10%, you can choose to salary sacrifice some additional income which goes into your superannuation untaxed, and has an EET model - Exempt, exempt, taxed (which means over time you end up with a much bigger balance, as you get compounding interest over time). In NZ, we have a stupid TTE system - leading to overall smaller balances. Oh, and John Key made employer kiwisaver contributions taxable. He honestly was so against kiwisaver, or the idea that someone should save for retirement using a savings scheme other than property investment.

Christchurch property market is relatively quiet but prices have not dropped either.

Good investors are not buying to rent out which is not great for tenants and rents are certainly increasing significantly to try and recover the extra costs incurred by the previous bunch policies.

Opportunities are around to buy and improve and onsell so that is where the $ are currently being made in CHCh.

"Opportunities are around to buy and improve and onsell so that is where the $ are currently being made in CHCh."

Something for those who want to get into property trading business then.

I appreciate that there are issues with declining property prices in many parts of NZ!

Christchurch is not one of them, as it is a very stable market and has been for many years.

Far too many two storied townhouses have been built in recent years in wrong areas and that market is saturated but there are other markets where you can do very nicely and with next to no risk!

Yes it is a bit of a worry for many investors that are having to prop up their property holdings but just as much for the owner occupiers having to pay their mortgages.

Rents are increasing significantly so we are going to be seeing the OCR dropped before the years end as the tax take is significantly lower than the government requires.

The RBNZ have overcooked it and need to start dropping now, but ORR doesn't want to back down, but he will be forced to, watch this space.

Has the legendary, The Man, returned?

Resurrection Zac!

Thing is there needs to be a better balance to the site!

Far too many thinking they know it all, and in reality they do not!

The property market is just not Auckland as I have pointed out previously.

Welcome back, it's great to see you commenting again.

I read most of the housing postings and unfortunately it is pretty much the same tone all the time from the same posters!

Everyone is entitled to an opinion, but the site is meant to be here to assist people make decent financial decisions.

We all appreciate that times have become more difficult financially for every single citizen in NZ, but times will become better due to

changes that will be made.

Orr has overcooked the increase in interest rates and inflation etc. has been caused by the previous government without doubt.

At the end of the day if you arent happy with the way things are going for yourself, then get out and improve things.

Opportunities are out there for everyone I can assure you.

I appreciate that there are issues with declining property prices in many parts of NZ!

Christchurch is not one of them, as it is a very stable market and has been for many years.

Sorry but that simply isn't the case. CHC might be doing better than average, but it's following the same trends as everywhere else. Prices are down 2.3% in the last three months. Slightly better than the nz average -2.9%, but down nonetheless.

Not seeing prices down much at all.

Any drop in average in CHCh is due to more lower priced houses being sold rather than a drop in most property’s vslur.

Yes there are a lot of property not selling but that is showing that most are not squeezed as yet.

Reality is that even if prices have come down it is mainly due to the debt servicing rate being too high at about 9%.

If the buyers sitting on the sidelines think it is helping them, then it maybe it is in some localitie.

There is no doubt the tide will turn and prices will rise.

Australia cities are far more expensive to live than NZ.

House prices will collapse further - the first replacements for dairy products will hit the market next year and diary products are half NZs GDP, if you take Dairy products out of the export mix - NZ goes from 60% of Australia's GDP per capita to 30%. It leads to the situation of economic refugees from NZ pouring across the border into Australia which leads to the situation of Australia closing its borders. The impact on house prices - well salaries in NZ aren't going to fall but if GDP per capita drops this much relative to Australia then the dollar has to fall. This is all bad for inflation and the impact will be a high OCR for years to come.

Not when people find out the fat in fake dairy is industrial seed oil.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.