Residential property values are "teetering on the brink" as the market heads into winter, according to Quotable Value (QV).

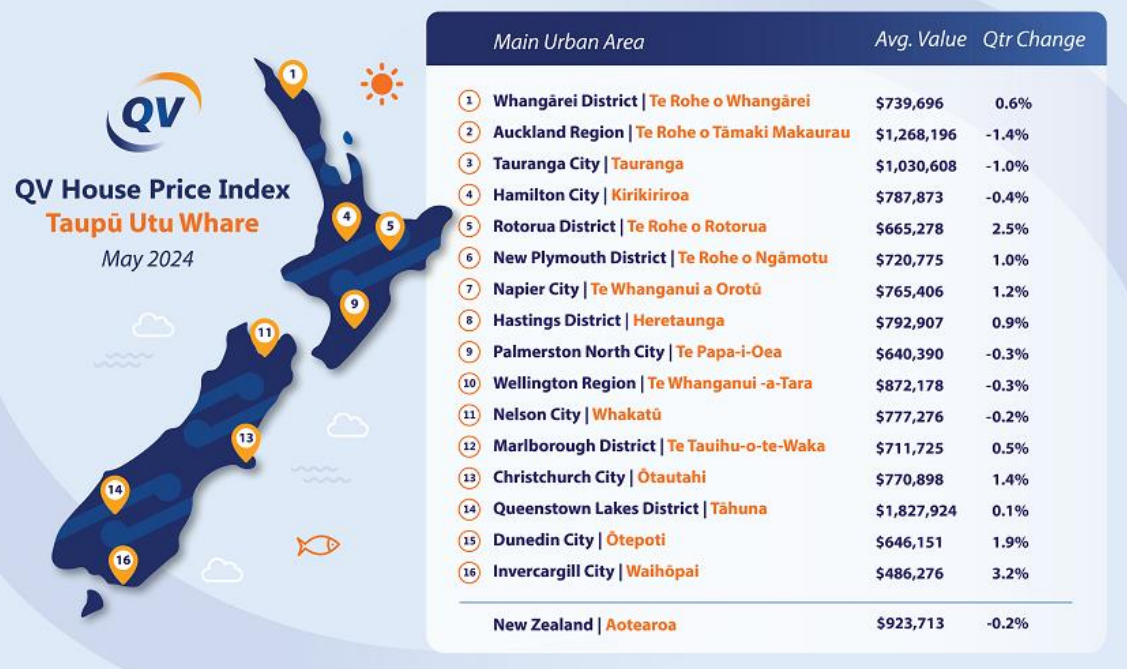

According to the QV House Price Index, New Zealand's average dwelling value fell 0.2% over the three months to May this year. That's the first quarterly decline since July last year, and followed a 0.1% increase in the three months to April this year, suggesting values could be at a turning point.

"The average rate of home value growth either decreased, or the rate of decline increased, in nearly all of the main urban areas we monitor," QV said in its June Report.

The biggest declines were in Auckland, where the average dwelling value dropped 1.4%, followed by Tauranga which slipped 1.0%.

Going against the trend, Invercargill had the biggest gain in average value at 3.2%, followed by a 2.5% gain in Rotorua. (See the table below for the full district values).

'Home values continue to bobble up and down from month to month and quarter to quarter, but they aren't moving one way or the other with any real conviction," QV Operations Manager James Wilson said.

"The housing market has largely stalled, and now the seasonal slowdown is well and truly upon us, with both buyers and sellers continuing to grapple with difficult economic conditions. Against this backdrop, an excess of housing stock on the market is maintaining downward pressure on prices."

"So those who are in a position to buy right now, have the upper hand," said Wilson.

"Purchasers are spoilt for choice and appear to have time on their side, with nothing to suggest that house prices are going to take off again soon," Wilson said.

The comment stream on this story is now closed.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

187 Comments

Wile E. Coyote

Beep beep

Given how delayed this series is, the REINZ numbers are going to be a lot worse.

Agreed. Bubble curve has us at the start of the capitulation phase.

https://www.classicbuilders.co.nz/house-and-land/waikato/hapori-park/lo…

Close to Mormon Temple and under 1m

A house built on a postage stamp surrounded by concrete.......for a million bucks....tell them they are dreaming.

But IT GUY can graze horsies in the parkland owned by the LDS and have spare millions $. Deal

What does LDS mean?

I am grazing horsies

Latter Day Saints

Don't the Mormon's collect a tithe and also provide loans to their sheeple?

Auckland leads on the way up. Auckland in free fall as is Wellington = regional speculators get ready for reality, or try to bail out now...

Actual sales are as rare as hens teeth. Buyers and banks hold the trump cards

Who on earth would buy a house now... when it is likely to fall a lot further in value in the near to mid term.

Now is about bottom, great time to buy!

Love the jokes!

We are only halfway down this epic slope, at best.

The New Zealand housing market is currently in a state of transition, presenting both opportunities and challenges for potential buyers.

1. **Market Recovery**: Property sales have started to recover from a significant downturn, with a notable increase in the number of properties sold compared to last year. This indicates a possible bottoming out of the market, suggesting that prices may start to stabilize or increase soon [[❞]](https://www.opespartners.co.nz/property-markets) [[❞]](https://www.kiwibank.co.nz/personal-banking/home-loans/guides/housing-m…).

2. **Interest Rates and Inflation**: High interest rates are a significant factor, leading to higher mortgage costs. However, some banks have started to reduce their home loan rates, which could stimulate demand and provide some relief for buyers [[❞]](https://www.nzsothebysrealty.com/insights/news/nz-housing-market-predic…) [[❞]](https://www.kiwibank.co.nz/personal-banking/home-loans/guides/housing-m…).

3. **Supply and Demand**: The number of new homes being consented has decreased, which might tighten supply in the near future. This could put upward pressure on prices if demand increases [[❞]](https://www.interest.co.nz/property).

4. **Regional Variations**: Some regions, like Wellington, Auckland, and Christchurch, are considered undervalued and may offer good investment opportunities. Conversely, areas like Queenstown-Lakes are seen as overvalued [[❞]](https://www.opespartners.co.nz/property-markets) [[❞]](https://www.nzsothebysrealty.com/insights/news/nz-housing-market-predic…).

5. **Long-term Trends**: Historically, New Zealand house prices have risen by about 7% per annum. Although the future growth rate is expected to be around 5%, the long-term trend remains upward [[❞]](https://www.opespartners.co.nz/property-markets) [[❞]](https://www.nzsothebysrealty.com/insights/news/nz-housing-market-predic…).

Given these factors, it might be a good time to buy a house in New Zealand, particularly if you can secure a property at a favorable price and manage the higher interest rates. However, market conditions can vary significantly by region, so it’s important to consider local factors and trends. Consulting with a financial adviser or real estate expert can provide more tailored guidance.

Good post. Some points I agree with, some less so. But you are looking at long term trends which is of more consequence than short-term factors such as interest rates and DTI ratios.

There are a lot on here who think the current downturn is going to rumble on for years Japan style. While I respect everyone's opinion, to get to that conclusion they are ignoring or underestimating these the long term trends.

I used Chat GPT. Strangely the "overvalued" area of Queenstown is about the only area being chased

Looks like you included 'max delusion' to your ChatGPT prompt

More seriously, that ChatGPT output clearly reflects the overwhelming spruiker generated online content about the housing market.

It's just regurgitating the dominate narrative. No actual insight of course.

But interest rates and DTI's are what's driven our long term trends of house price growth, so these are long term factors.

- Interest rates dropping from the 20%+ we keep hearing about in the 70's to 2.5% in 2021.

- DTI ratios increasing due to

- a) lower interest rates allowing for bigger loans

- b) shift from single to dual income households.

The only way for house prices to continue to grow exponentially is either wage inflation, or some other form of wizardry (negative interest rates, triple income households).

These are the long term trends I pay more attention to vs the trend of rising house prices. It is about the 'why' behind said price changes.

I'd say demographic changes drove it - when women entered the workforce household incomes doubled. Secondly, the big Boomer bubble entered their prime earning years and had money to burn on bigger houses, holiday homes, and investment properties. Expecting the effects from a period of massive socio-demographic changes to continue indefinitely is foolish. Household incomes are not going to double again, and that big Boomer bubble is now in the process of selling up and downsizing.

Some boomers are indeed selling up and many are moving out of Auckland.

And other boomers are transferring their wealth to their GenX and GenY children either through inheritance or trusts.

I see a huge generational transfer of wealth occurring over the next 20 years with GenX and GenY retiring in their 50’s or reinvesting that inheritance into investments.

Perhaps Interest should write a piece on this generational wealth transfer and what it means.

Look to the Netherlands, however at least they found ways to harness this to have a great health system.

Great idea but unfortunately politicians in NZ would squander a death duty on pet projects instead of building a great health system.

Interesting isn't it, as we can't ever double our workforce again, we should never expect to see the growth and development or price increases as across this period when work opportunities for women opened up. Now how does that sit with historical long term trends and current predictions?

Add in the decline in cheap energy (fossil fuels were a once in history jackpot) and the depletion of core materials (rare minerals, construction sand, topsoil, etc...) and the biodiversity collapse of our natural systems.

Growth in it's commonly used definition is dead. That doesn't mean however that humans can't flourish and thrive, we just need to focus on things that actually make humans happy and get the profit seeking at all costs rentiers out of the picture.

Completely agree. And I suspect the decline will be felt more keenly in the cities - as people drift from large urban centres back to smaller communities. Back to the future.

"... as people drift from large urban centres back to smaller communities. "

The 'people' are getting older. They'll drift to where older people get the best services. So no.

I would say you are on target K. W. But there is an extra wrinkle, in that the international boomers flood of capital build up over the last 20+ years, probably lowered interest rates more than people realise. Leading to the Property Ponzi that NZ is well known for, the unwinding of that capital accumulation will mean some interesting years for interest rates in my opinion of course

Which to be fair, is how it should've been all along

If you look at how long house prices took to recover in the US after the GFC it was about 6 years. We are in Year 3 so another 3 years of falling prices is not a far fetched idea. The question is what happens to people in negative equity during the next three years?

The distinction though is we remain in an inflationary environment, whereas the GFC brought about a deflationary environment. House prices can fall in real terms while nominal prices remain the same.

That would be the ideal outcome, provided the wage inflation is keeping up.

If you look at how long house prices took to recover in the US after the GFC it was about 6 years. We are in Year 3 so another 3 years of falling prices is not a far fetched idea.

FYI, for those who don't know.

Time periods for real estate market prices (nominal) that are yet to recover to peak price levels in some residential real estate markets:

1) Japan: 33 years and still counting (peaked in 1991)

2) Russia: 18 years and still counting (peaked in 2006)

3) Kazakhstan: 17 years and still counting (peaked in 2007)

4) Cyprus: 16 years and still counting (peaked in 2008)

5) Spain: 16 years and still counting (peaked in 2008)

6) Italy: 13 years and still counting (peaked in 2011)

7) Saudi Arabia: 10 years and still counting (peaked in 2014)

8) Qatar: 9 years and still counting (peaked in 2015)

9) Macau: 6 years and still counting (peaked in 2018)

10) Hong Kong: 5 years and still counting (peaked in 2019)

Ireland finally recovered in 2022.

By 2012, the index had fallen by just over 50 per cent to 76, a post-crash low. By 2022, prices had recovered to 2007 levels. By the end of last year, they were 4 per cent above the 2007 pea

https://www.thetimes.com/world/ireland-world/article/recession-or-crash….

Yes. That is a recovery time of 15 years.

@flying high

😂😂

Refering to the "reeferendum" at 2020 election

You missed one

6.** Reality Finally Applies**. Debt remains at historicall normal levels. Decades of ever lower cost of debt fueled price unwinds. Normal debt, no income tax rinsing, ever higher rates, and no further capital gains makes roi an increasingly greater loss making exercise. Spec crowd starts exiting for any capital gain possible. Boomers retiring see this trend and accelerate the trend by starting to exit in mass.

Ponzi unwinds as maket learns importance of yield again.

" **Long-term Trends**: Historically, New Zealand house prices have risen by about 7% per annum. Although the future growth rate is expected to be around 5%, the long-term trend remains upward"

This belief heavily influenced the future house price growth expectations of many buyers and was used in many property investment calculations.

Weinstein ?

I would buy... am not looking for the cheapest deal, just a good fit

Good Answer. My Mum just went unconditional on a house yesterday. She's moving to be closer to her grandkids. She is confident she will be better off in the ten year period than renting at crazy auckland rent prices, and she doesn't want the hassle of moving twice to 'time the bottom'. Nonetheless, she says she is going to avoid looking at online valuations of her property for the next couple of years!

My mother bought during the market peak, the money becomes irrelevant, you don't have time to wait as you hit 80. Money just becomes digits in your bank account that you just do what you want with. Its all just about enjoying the time you have left.

Exactly. These are the people buying now. Those that either have so much money they don't really care about price or those who soon will no longer be with us and don't give a shit. If you're financially prudent why would you buy now?

Riddle me this?

How can Homes have this property valued at $2M when it sold in October for under a million? Answer: all the residents on this street asked a real estate agent to up their Homes values because they didn't want the real value to appear in the algorithm

https://homes.co.nz/address/auckland/devonport/4-garden-terrace/norYM

https://homes.co.nz/address/auckland/devonport/4-garden-terrace/norYM

On the Oct 2023 reported price of 956,000, what does ASR mean? Doesn’t seem like a regular code used.

ASR = Agent Sales Record so seems legitimate. Sometimes it will be a sale between an owner and his own company (no agent involved) which will be recorded differently and to be wary of as likely not market price.

Zachary,

Thank you for your clarification.

When does it change to one of other codes that begins with "S"? Upon settlement & title transfer?

"Sometimes it will be a sale between an owner and his own company (no agent involved) which will be recorded differently and to be wary of as likely not market price."

Given the low price, relative to market valuations, this is exactly the situation that I wondered if this may have occurred.

Interesting how the homes.co.nz link above no longer works?

Someone has restricted access to that information now. The removal of price transparency.

How strange! I had it open just a few minutes ago.

So strange. I had it open. Then tried it again and it didn't work. And now it's suddenly working again. 🤷♀️

I saw the issue too, CN. The link was broken for a few minutes, but is now up again.

I live near there when in Auckland. It's plainly not a real price, just a transfer for compony, trust, or personal purposes. The idea that the elderly residents of that street are getting together to game the homes.co.nz algorithm is "interesting"!

Say it all really. Vested interests gaming the system while claiming independence.

#liesofthevested

Great for your mum, some people don’t have time so the market is irrelevant . If it was your daughter/son in the scenario what would you tell them?

I think its a good time to Buy, opportunity for people to get in with less competition and lower prices.

As long as you can with stand some pain, for who knows how long.

Necessity?

Who on earth would buy a house now... when it is likely to fall a lot further in value in the near to mid term.

While I completely agree with the sentiment, we found the right house at a price we could afford - and bought.

Thing is, it's so hard to find a good house for sale in Auckland (finding a place that's not completely crap is already a challenge).

We didn't want to buy:

- adjacent to or in the middle of a floodplain

- a leaker or plaster disaster

- a new build (as in a cramped doll's house on a tiny section)

- next to a Kainga Ora housing complex or near a park that might catch Kainga Ora's interest in future

- on a big, noisy road

- a house on a steep slope or next to a massive retaining wall.

- a house with untreated frames (circa 1992 to 2004, I think), especially in combination with absent eaves

We also hoped to find a house:

- near the kids' schools

- beautiful leafy, suburb

- sunny and north-facing

- open plan kitchen and friendly, cosy shared living spaces

- a room that can work as a home office

- enough place for a trampoline outside

- a low-maintenance garden (big enough for pets, but not requiring you to spend every free, waking moment working in the garden)

Lastly, our kids are already teenagers. If we waited another few years it would be too late to buy a family home and they'd have spent their childhoods in crappy rentals.

Sure, it would be best for us not to look at house valuations in the next few years, but I'm very happy and grateful to have finally bought a place that ticked our boxes. In boom times or even in a normal market, we'd probably have faced lots of competition for the house we bought and paid much, much, much more - or wouldn't have been able to afford the house at all.

Anyway, may prices continue to fall, making it possible for more families to raise their kids in a secure, happy home.

Actually the ones in charge in due course will those with CASH and plenty of it.

That 6.1% Kiwibank 1yr TD rate certainly paints a better picture.... FHB's need to be wary I see some locales that have plenty of scope to decline much further.

New Zealand won’t automatically turn into some quarter acre pavlova paradise should property prices correct. Here’s what concerns me should prices continue to drop:

- Rich people (whose wealth has been growing much more than ordinary people’s) will swoop in and buy up assets, including ordinary people’s houses as they continue to feel the recessionary pressures and are forced to sell.

- Idiotic government policy in future, such as fully allowing foreign investors to purchase NZ property.

Good governance is rare in human history and one can never underestimate human stupidity; Both measures would re-inflate the ponzi and temporarily kick start that rock star economy feeling. But longer term, we’d be selling off opportunities from under our children’s feet.

Unsure. Firstly, although building consents are falling (but still above historical levels) housing construction is still relatively robust. Construction activity in Q1 2024 appears to be about 10% below Q1 2023. Lots of building consents being completed still. So supply is going to keep ahead of demand.

We also may be finally getting rid of the concept that house prices will keep going up forever. The result may be less speculation for capital gains.

Auckland prices still haven't fallen to the point where rental return is a viable investment. Auckland is therefore still a little overpriced, which provincial New Zealand is still good

We also may be finally getting rid of the concept that house prices will keep going up forever. The result may be less speculation for capital gains.

It will take a lot more than a few bad years, and the little speed bump we’re currently negotiating to remove that belief from the New Zealand psyche.

If prices continue to decline, there's no way any astute foreign investors are swooping in to save an overpriced and declining market. They were piling into a bubble before and just timing their exit.

Auckland isn't London and has nowhere near the same appeal as a place to store wealth than other major international cities.

That being said there is still the element of this being a haven for people to get their money out if China I suppose.. but from what I understand, current rules aren't having much of an effect on that anyway..

Try no capital gains tax and no stamp duty for a start. We are a solid location to park some cash.

Maybe, but that still relies on solid capital gains prospects in the first instance. I think the pendulum has swung on that one, as the underlying value isn't there.

Not necessarily. They may just want to park the money without it being in a bank account. And (in Auckland) an income of $800 pw, so they don't care much about capital gains.

That goes back to my first point though of their being much more stable markets supported by much better fundamentals. NZ and particularly Auckland resi housing just looks incredibly precarious for anyone with cash to invest.

Only rich people that prepared for this. Aka cleared debt and built a cash bazooka. Many just kept buying interest only but they are vapor rich only with a huge risk angle.

NZ needs this. We need to value production and not exploitive speculation.

I think a slow retreat from housing as a first choice investment is in motion as other (better) options get mainstream and the older crowd wisen up . Policy will adjust to suit the (now) younger voters as the landlord generation expire, and we'll move onto the next problem of passive investment artificially inflating the top end of index funds.

You don’t get rich by doing dumb stuff like that

I look at auction data for Auckland region on here every day and I am surprised the fall is not more than 1.4%. The number of sales for 10, 20, 30 and now 40% below RV have been increasing each month all year and there are fewer that are at or over RV. there must be an awful lot of non-auction sales going though at higher levels to balance it out and get to -1.4%. So far, June auctions are definitely looking worse than May.

its the way they calc the series , QV include too much aged data hence my comment on the REINZ release will be dire

When does REINZ HPI come out, must be about this time of month?

Also today.

Do you know when?

Unfortunately not, just going by previous issues.

Not today - likely to media Monday public next Tuesday.

Constantly getting a string of notifications from trademe on the properties I am watching: Auction > deadline sale > price by negotiation > asking price > asking price reduced.

Although I will say there are a few numptys out there still paying 2021 CV or above for some of the better properties..

The Mr and Mrs Numpy, need to take -40 to -60% off the 2021/2022 CVs. Thats where this market is headed by 2026/2028.

Yes I’ve been considering a relocation to Dunedin for family reasons so have had a watch list for that market the last few months. Very little appears to be selling and getting notifications on a daily basis with asking prices reduced 5-10% - yet the data in the article shows that prices are up in the quarter which does not align with what I’m seeing.

And more stock coming to market every day so choice increasing while asking prices are on the slide.

Any suburbs in particular that take your fancy? I always loved living in Dunedin when I was at Uni, as I had friends from there living all over so we would frequent all parts of the city vs the usual studentville.

You of all people are mixing up asking prices with selling prices

A vendor asks $200 for something thats worth $100, he reduces the price by 5-10 percent every week but eventually sells for $110. Presto, a ten percent lift in market value

I am surprised at the regional patchiness. Only Auckland and Tauranga have had significant drops this quarter. Everywhere else is stable or even seen good gains (Dunedin/Invergargill).

It will be interesting to see in the coming months if Auckland is leading the provincial market as it has done traditionally, or if we are witnessing the decoupling of two distinct markets.

Unemployment has dropped in the regions since the start of the year, its only going up in the main centres (and Nelson). Tauranga is being sold off as cash strapped owners sell holiday houses, because the GST on AirBnB has killed the AirBnB market.

I think the issue with Auckland is the volume of supply and the declining population. Migration has off-set recent declines, but generally industry moving from Auckland. Trademe has around 15,000 homes listed for Auckland region, of which 3,500 are new builds. The new builds won't list all the stock - a developer won't list all homes on trademe - so they is likely to be at least twice the number of new builds. It looks to me like around 3% of all houses in the Auckland region are currently listed on trademe.

Aucklands population did decrease by about 15000 during the pandemic but has grown by 2-3% in the last two years. The most conservative estimates project Aucklands population to be over 2m by 2030.

"Against this backdrop, an excess of housing stock on the market is maintaining downward pressure on prices"

So we apparently have a housing shortage.....but an excess of stock for sale?

There is no shortage, but repeat something enough and it becomes accepted as fact.

I’m not certain we had a housing shortage - but instead not enough houses for sale for cheap post GFC credit/debt to purchase.

ie the supply demand imbalance was between availability of serviceable cheap debt to houses and not people/family to houses.

The opposite may now be true and was always the risk of pumping markets with cheap debt.

A simple analysis of the number of houses compared to the population increased suggested there was around 45,000 fewer homes compared to population in 2018 compared to 2006. Around half that shortage has been met

From my vantage point, I can see a definite shortage in rental stock. Houses for sale, not so much.

I think when people are speaking of a housing shortage they mean it in the long term trajectory. building consents are dropping while the population keeps rising.

Hallelujah

Deluded

Where are you looking???

11,500 available for rent on TM, many more unlisted townhouses. There seems to be an abundance of rental stock. Here in Wellington city there are 25% more available for rent than to buy.

It's winter.

And house price falls reported arent the 'real falls

- We have a >10% decline in the value of NZD AND a 13% inflation since the prices started tumbling.

Also is key to remember that we have a net outward migration of people - and if we were to target the net migration of skilled younger professionals it would be a frightening number as we have so many skilled kiwis leaving and unskilled people coming.

Combine this will a likely HFL OCR and glut of rentals and houses for sale... and 100% probability of some of the probable serious issues overseas coming true (expanded or additional wars, trump wins election, climate issues, china expands on trade wars...)

anyone thinking this will all improve in less than 2 years is dreaming. by then enemployment will be up and the emigration of young skilled more pronounced.... house prices will fall further

Where do you live?

Rental stock is soaring in Auckland at least. Lots of townhouses still being completed. Many not selling so being rented out.

Fair enough House mouse/ Malamah. I may have my local goggles on. I live on the northshore where rents are going up due to limited stock. That might not be the same everywhere including other parts of Auckland. I believe Malamah is in Wellington and things do look different there.

In Wellington renters are struggling to get new flatmates after someone loses their job or moves overseas. Sign of difficult times for some.

Ex agent, did you give up your REA job because you didn't get enough sales anymore ?

I have never been an RE agent. I went to university and got a degree, worked hard at my profession and retired relatively young.

Good to know the local markets people are viewing from. Sometimes I think your views are a bit wild, but I think that’s more to do with the local markets we all monitor being slightly different. I look mostly at Wellington region due to work. Malmah is on the money about the rentals. The Hutt had a wave of infill townhouse construction that’s increased supply. Insurers have figured out almost all of their pricing for Wellington is wrong (too cheap) and are trying to price the Flood/EQ/Landslip etc on new models so insurance premiums will only increase. Set this against the backdrop of crumbling water infrastructure that can only lead to higher rates. The employment situation still has to play out and most people aren’t looking at a major purchase with such uncertainty. I just don’t see how there is any wind in the sails for price growth. On the ground and at the water cooler then general feeling is the economic tide is going out.

Some fairly reasonable accidental rentals coming to market in Wellington. A lot of family homes. Undercutting typical rentals by $100-200 per week is what I’m seeing.

The for sale listings are full of ex-rentals.

A story of two stories.

"Undercutting typical rentals by $100-200 per week is what I’m seeing."

So this is how rents fall. Price competition by non owner occupier owners for potentially fewer renters / tenants.

Lower rents mean potentially more cashflow stress by highly leveraged non owner occupier owners.

This is us. Formerly owner occupied home. Spent money over the 15 years of ownership upgrading the ex state house with wood burner, double glazing and insulating every exterior facing wall. Escaped to Australia as no desire to live under a 3rd go around of an economically inept National government.

100 days on market. Dropped price by $125k. Last price was 35% below 2023 CV. No buyers.

As we only have a small mortgage, and including rates/insurance we were able to rent out for $150/wk less than other specuvestor properties. Prop mgr encouraged us to rent for more but we declined as we aren’t in the business of bankrupting tenants and well aware that National’s exorbitant additions to living costs for many which a derisory $2/wk tax cut will not change, means that renting for more = more tenants.

prop mgr found us a very nice couple, moving from their existing rental of 5 years due to that house being sold. By a specuvestor, ironically.

so yes, owner occupier “accidental landlords” who have relatively manageable mortgages are unlikely to be renting out at the maximum.

we also do have another rental property, and that was a near rebuild last year, so warm and dry, and being rented for less than market value as the outgoings aren’t ridiculous.

I think you might be an exception to the rule and the majority will seek the maximum no matter what.

Kudos to you for having a more balanced approach and consideration towards your tenants position.

The problem with specuvestors is their greed. When I worked in banking, it was common for specuvestors to load up the mortgage against rental properties for their own personal use. As negative gearing was still a thing back then, it meant that tenants were paying for the landlords lifestyle. It’s morally repugnant.

if genuine landlords really only wanted an investment property to help them in their dotage, then keep the rent tied to the actual outgoings and don’t expect tenants to pay for your lifestyle.

those landlords are entirely the reason why there is so much backlash against them.

we refuse to be one of them and would prefer a stable long term tenant that can cover the outgoings. Not fussed about tenants covering the interest costs as they are deductible, along with rates and insurance. Might even drop the rent next year too once the 2025 tax year draws to a close and tax receipts are done.

"Not fussed about tenants covering the interest costs as they are deductible, along with rates and insurance."

Being deductible doesn't make them go away, just means whatever dollar amount they represent in your rent received is not subject to income tax. Unless you're paying for them out of your own pocket?

Can you afford $850pw for a basic 3 bdrm w single garage, may have to pay 900 or 950pw

Incorrect.

Try and provide specific insight

Yes - you should try and provide truthful and specific insights on a public forum. Instead you made a blanket statement exaggerating the numbers to help your spruiker narrative.

So go ahead and justify your numbers for the reader.

I'm currently renting a 3 bedroom house in Auckland with a DOUBLE garage for less than the lowest number you provided.

Yes your one rental property example represents the market of course

The statement was regarding new 3brm townhouse stock, do a search online of whats available like I did

Haha, you said basic not new

I suggest you follow the thread right through then. "Basic new" not basic old. Of course you could rent an up market new home ie not basic and pay more

It was a blanket statement regarding basic 3 bdrm w single garage

Now you're trying to add variables to suit your narrative.

My example was one more example than you have provided. And I can see plenty of brand new 3 bedroom houses in Auckland for less than $850p/w.

Do you want to add another variable to your statement we weren't aware of?

Ok, so you're clear now that housemouse talked about homes being completed then rented out not sold. Goodness

Incorrect again.

Let’s review the facts:

- Baptist claimed there was a shortage of rentals

- HM said rental stock was soaring in Auckland due to new builds failing to sell, and consequently joining the rental stock.

- You added a blanket statement exaggerating the price of renting a basic 3brm townhouse with a single garage

- I questioned your narrative and provided an example.

- You now claim we’re only talking about the price of new build rentals in Auckland.

- Your price indications still don’t represent basic 3brm new build townhouses available to rent in Auckland.

And why would a renter ever need to choose a new build to rent anyway?

New builds represent a proportion of the market, so without them there are LESS rentals 😉

Have a good night, dont take your frustrations out on your partner or phone though

Stepping on rakes again FH?

Relax it’s Friday, have a beer :)

Fewer* rentals

"So we apparently have a housing shortage.....but an excess of stock for sale?"

Most people misunderstand the difference between

1) underlying supply vs underlying demand

2) effective supply vs effective demand

There can be a shortage of underlying supply vs underlying demand and at the same time, an excess of effective supply vs effective demand.

Only one of the above impacts house prices.

The key issue is that there is a shortage of affordable housing in both the house ownership market and the rental market.

In terms of the shortage of affordability in the rental market, look at accommodation supplements paid by the government in the private rental market. There was also a graphic in the Economist - 25% of renters were paying more than 40% of disposable income on rent - it was the highest of the 9 countries shown.

As a result, there is also a shortage of social housing - look at the waiting lists for social housing and the numbers in emergency housing.

This doesn’t seem affordable if owner occupier buyers need to rent out rooms on Airbnb to make mortgage payments.

If these are purchased by non owner occupiers for use in the short term rental market, how does this result in increased number of dwellings for those local residents in the long term rental market?

https://www.stuff.co.nz/business/350305789/queenstown-affordable-homes-…

There is no housing shortage- rather an inability to pay. So we keep building more and more houses at the same price and wonder why we still have a ‘shortage’.

Yes, I dont understand why all those renters havent just gone out and bought a place. Wasnt that the whole point of the War On Landlords - so every renter could become a First Home Buyer? Gee, anyone would think those policy wonks in Wellington got it wrong ....

The ratio of first home buyers to investors significantly increased in favour of FHBs following Labour's excellent housing policies.

They didn't get it wrong at all, repealing the changes was the wrong move.

Ratios mean nothing when its caused by the decrease in landlords buying, not the increase in first home buyers. If I sell 100 houses, and normally 30 investors and 30 first home buyers (and 40 other owner occupiers) buy them its 1:1 ratio. Now if I have 100 houses and only 20 first home buyers and 10 investors buy them, the ratio is now 2:1. But there are still less First Home Buyers than before.

So the changes did nothing unless they increased the absolute number of First Home Buyers. Which they didnt. The number of FHB was 28,719 in 2019 and 26,390 in 2023. The number of Investors in 2019 was 36,371 and 21,403 in 2023. So why didnt the FHB buy the excess 14,968 houses that investors didnt buy in 2023?

And now we scratch our heads and wonder why there are so many listings for sale and unsold houses, a rental shortage and escalating rents. Duh.

https://www.rbnz.govt.nz/statistics/series/lending-and-monetary/new-res…

So why didnt the FHB buy the excess 14,968 houses that investors didnt buy in 2023?

1) Lack of affordability perhaps?

2) Inability to borrow a sufficient amount to finance their purchase at last year's prices? Especially in Auckland for those without the bank of mum and dad, or willing to co-own with people outside the nuclear family.

3) Cheaper to rent than buy?

Nope. The ratio doesn't matter for a lot of things but in terms of effectiveness of the Labour housing policies the number of landlords vs FHBs it is a key factor. Remember, Labour didn't say they were going to crash the market, they just said they would balance the scales to landlords wouldn't have an unfair advantage and be able to easily outbid FHBs as much as they had been doing. It worked, hence the ratio changing.

Good point. While K.W. is correct, there isn't an uptick in FHB, what FHB do have is less competition with their landlords seeking to grow their portfolio.

No it didnt work, Labour did absolutely nothing to enable more FHB to buy a house, all they did was destroy the rental market making life far more difficult for those tenants who cannot afford to "just go out and buy a home". Personally, I dont call that "winning" even if the mathematical ratios of the housing market changes. Nobody cares about ratios. People care about how much rent they have to pay each week, and how long it takes to save a deposit when your rent is going up 10% a year, and how hard it is to find a rental property when your landlord sells up and not end up on the social housing waitlist. I'm 100% sure knowing the "ratio changed" doesnt help them sleep better at night, especially the ones sleeping in their cars.

There’s no such thing as an excess of housing stock.

really? What happened in Ireland after the GFC?

.

The vast majority of the properties for sale in North Shore are townhouses and apartments, stand-alone houses are still around 2021 RV, so don't get to excited.

That’s why the REINZ’s HPI is the best measure, it controls for those things.

"stand-alone houses are still around 2021 RV, so don't get to excited"

Hmmmm, closer to 2017 CV

https://www.trademe.co.nz/a/property/residential/sale/auckland/north-sh…

Wealthy people will continue to buy, good deals everywhere til market turns again. Rinse and repeat.

What’s a good deal now as values continue to drop. Is it not better to wait till the market stops dropping and you buy slightly above the bottom

You never know the bottom, top, or whatever. Adopting your approach a buyer might have bought last September / October when the "green shoots" (subsequently found to be weeds) popped up.

A good deal represents different things to different individuals, yes it is often about the price.

Like fuel discount day if I know the fuel price is going to drop further I would fill up only half a tank. If I think the house price might drop further I might buy one or two only in good locations, good deals for me if I get an immediate return and I’m not worried about price dropping another 50k in the short term.

Going against the trend ...a 2.5% gain in Rotorua.

That will be Kainga Ora buying up houses as they move people out of motels.

Maybe Tauranga buyers widening their search for value

It's a good thing right? Lower House prices.

'Higher for Longer baby!'👶

"Purchasers are spoilt for choice"

This seems to be the new euphemism / phrase being used for "buyers market"

Gotta love the (misleading) headline on this bit of spruiking.

Bungalow smashes past the reserve, delivers vendors $1m profit

Is the return really that spectacular?

Actually - it isn't.

Remember the old nonsense that "house prices double every 10 years? Using the Rule of 72 that means you need to get about 7.2% p.a. So what did they get?

Homes.co.nz says it was bought for $338k in 2005. Sold for $1.321 million.

https://homes.co.nz/address/auckland/avondale/20-wingate-street/Dr0E2

That's a per annum gross nominal rate of return of about $7.4% Very, very few sales get anywhere near that so it is 'spectacular' in that regard.

The 'gross nominate rate of return' does not include carrying costs like maintenance, rates, insurance, etc. Nor is it adjusted for inflation. But the rental income could be huge? Nope. Pretty ordinary.

So, yeah. Not that spectacular. But better than most sales at this time that are between 2% and 4% with a few getting 5% or a bit more.

So where is the value?

Auckland Council created it! The land has been rezoned into the THAB (Terraced Houses and Apartment Building) zone which allows six to eight stories.

And who bought it? F##king land bwankers !!!!

These people will hold for years and years hoping to see further land appreciation that'll be un-taxed while denying the land's development and contributing to shortages of land.

(I think I've mentioned our tax system seriously needs an overhaul if NZ is going to raise it productivity? This is just one example of why our tax system is failing us.)

Its a corner site as well, so very attractive to developers. But all profits on any eventual sale will be taxable regardless of how long they hold it as (a) it was bought with the intention of development and sale, and (b) the owner is in the business of development and sale.

Hilarious!

No land bwanker will ever admit to IRD that that is what they are doing. They're there just for the rental income in their retirement - don't cha' know.

K.W. you're not an accountant, right?

What impact will another million people have on our house prices?

People might laugh, but if you conducted a survey in India (population of 1.4 billion), asking who would be willing to immigrate for a ‘better lifestyle,’ my guess is at least 500,000 might be interested. And there are other countries you can run the same survey on.

The number of people leaving NZ will be easily replaced and that is the future.

[DC, why isn't ctrl-c / ctrl- v working anymore on Chrome? (edit: intermittently working.) Seems to work in Edge.]

"What impact will another million people have on our house prices?"

All depends on whether NZ can build enough to meet demand. Over 10 years that's - depending on household size - less than 50,000 more per year. A challenge - but not insumoutable.

Just an aside:- some years ago I was reading an analysis of human displacement due to global climate change. i.e. when people move from what were arable lands which have become too dry to farm. They presented 3 potential scenarios. Even the most mild is truly scary for NZ. Or put another way ... A million will be just the beginning. And yes - our central and local governments know this but many don't want to talk about it..

Sad thing is these sorts migrants aren't moving to New Zealand because we're attracting them here with how spectacular and dynamic our economy is. Rather it's a case of push factors, many would do anything to escape their very limited life opportunities in their home countries. It's a pretty dire world out there for the vast majority of people.

"House prices on the brink"

Very apt title and picture. Who on here said the market had found a floor again?

Me. Values are still up 1% from a year ago so you're ejaculating a tad prematurely.

The article also says "Home values continue to bobble up and down from month to month and quarter to quarter but they aren't moving one way or the other with any real conviction."

Baptist, with for sale inventory piling on, asking prices decreasing, July 01 Brightline changes approaching, increasing unemployment causing FHB's to pull back, you've got to spin it to win it - right.

Keep up the great work. You're an energetic and resilient ambassador for the highly embarrassed Spruiker community.

Now, read the title again - over and over. At least try and be honest with yourself :) edit

RP, I agree with you on all the factors you have just listed. But I also believe in the following factors that counter them: rising population, falling building consents, imminent OCR drop, wage inflation, and the fact that a 25% real drop has already occurred.

I have been fairly consistent since Christmas that I expected flat prices through 2024 (when many on here and other economists were expecting the rises in the second half of 2023 to continue). How that makes me a spruiker I am not sure. Frankly, it is an ad hominem attack.

Gee, calm down. You only call it ad-hominem attack when you don't like the headline of the day. Please feel free to use similar sideshows on other days to. It's typical Spruiker denial type tactics and sideshows.

Again, keep it real and be honest with yourself. Call it a form of financial "spatial awareness" if you like....

To be fair though from the comments I've read, 1689Baptist provides reasons for his views, it doesn't mean anyone needs to agree with them, but he does provide them unlike others that don't back up what they say with reasons and often disappear when challenged.

Unlike rents, a rising population has not led to an increase in house prices due to the limited wealth of immigrants. Lets not conveniently forget the well documented analysis that on a rental yield basis the figures still don't stack, especially after rates and insurance are covered - so no support there. There is a clear glut of overpriced homes that are still out of reach hence the weakening outlook. With increased unemployment, wage inflation will begin to top out then many are still left with a cost of living crisis to grapple with. Increased wages have been soaked up by high borrowing rates, food, electricity and rent so that is not a credible support for todays asking prices.

I agree. Those who offer sources for their opinions should get a level of respect even if you disagree with it.

You forgot to mention the proposed ability to build 60sq metre dwelling in any back yard in NZ no consent required and the potential to drag down demand.

How that makes me a spruiker I am not sure.

Why would you bother spending so much time & energy here everyday spruiking and defending your narrative? We're sure.

You only have too look at the slumping Ryman Healthcare shares to get a look at what happens when, through denial, you fail spectacularly in your efforts to dictate the direction of the market. Many economists are revisiting previous bullish forecasts and revising them down with little disclaimers like "risk to downside"

https://www.nzherald.co.nz/business/rescuing-ryman-chairman-reveals-his…

Ryman's thought there was an endless supply of their much favored cashed up demographic. This same asset/equity rich demographic want to sell houses in this weakening market too!

Rymans are a property coy. I bailed out a long time ago for that reason

"Values are still up 1% from a year ago"

Looking solely at 1 year price changes runs the risk of missing the big picture. I think you live on the North Shore in Auckland.

In Northcote on the North Shore of Auckland. From realestate.co.nz:

1) Median house price April 2024: $1,085,525

2) Median house price at peak (the high water mark is used in assessing house price bubbles): $1,442,158

From the peak, that is a price fall of 24.7%.

You may have bought when house prices were 10-15% below the peak and got a bargain at that time (i.e a discount), so you may be referring to your own personal situation and lived experience of a minor price fall from your bargain purchase price.

Many commenters however are referring to general owner occupier buyers who bought at market prices using high amounts of leverage. Like this owner occupier buyer in Wellington who has seen their equity & potentially lifetime savings evaporate in under 3 years.

https://www.newshub.co.nz/home/money/2024/06/housing-market-drop-wipes-…

Or these owner occupier buyers

https://www.newshub.co.nz/home/money/2024/06/thousands-of-first-home-bu…

You could "jac" up the floor. Not a good reference from baptist mind you

Meanwhile in Australia, rich people get cheap mortgages and only need a 5% deposit. Povvo's need not apply.

ANZ is shrugging off fears of rising mortgage stress to implement a controversial policy that allows wealthy customers, based in 145 postcodes including Point Piper and Toorak, to borrow up to 95 per cent of a property’s value without mortgage insurance.

The new policy, being rolled out this month, creates three distinct categories for wealthy borrowers in higher socio-economic suburbs, but excludes any postcodes in South Australia, Tasmania, Australian Capital Territory and Northern Territory.

All part of the wealth transfer.

The question still remains...if house inflation is no longer to underwrite our ongoing credit expansion what then is?

Volume fueled by (inward) migration?

The fact there is no answer is indicative....fiat will fall over

I noticed a house listed near our old home in Wellington, 280sqm, 4br,2br and 2 cars garage, etc.... Listed over 1.2m in Jan, now asking 995K.. That's a big ouch!

Ouchy ouch will be the sale price

Meaningless without quality adjustment (?) Lot of new builds for sale in AKL are townhouses with little land.

I'm stunned that prices have held up so well given interest rates. I think it's very much a case of people holding on, and hoping rates come down by the beginning of next year. NACT's restoration of interest deductibility has been a boon to this group, but that alone is not enough. I wonder if Labour would even bother doing away with it if they got in last time, cos 100% NACT will just get back in and reverse it once they're elected next. It feels like this country is unable to make any sort of meaningful progress on anything because we just have these massive see saws backwards and forwards on various policy issues.

"I'm stunned that prices have held up so well given interest rates."

It's too early to be stunned. Be patient. It's far from over ...

Labour's removal of tax deductibility didnt have much of an effect, because rising interest costs offset the decline in deductions. It would only have been from March 2024 that the new rules would have made a difference. Example. 100% deductibility in 2021 of a 3% mortgage is exactly the same as 50% deductibility of a 6% mortgage. So the same amount of income tax would have been payable in 2021 as in 2023.

However, the National changes have headed off the looming fiscal cliff of landlords having to pay income tax on rents while only being able to deduct 25% of 7% interest costs in 2024.

"Labour's removal of tax deductibility didnt have much of an effect ..."

You sure about that?

It did send the message that government could change the tax rules that made residential property "investment" so 'wonderful'.

And they could do this at any time.

"Labour's removal of tax deductibility didnt have much of an effect, because rising interest costs offset the decline in deductions"

Policies need time to work. If the policy had remained and interest deductibility had been fully phased in to zero deductibility, many highly leveraged non owner occupier buyers in the existing house market may not have chosen to buy in the existing house market. The tax incentives in the new build market was attracting non owner occupier buyers in the long term rental market thereby creating demand for new supply to meet underlying demand.

Maybe, but there would also have been severe "unintended" consequences. Like crashing the prices of existing housing (and increasing the yields) as leveraged landlords were forced to sell up, making new builds less attractive as they become economically unviable to buy and rent out due to the high cost of building and low rental yields. And like forcing up the average cost of rent as new builds are more expensive to rent than older housing, which penalises those low income renters who can only afford to rent cheaper older housing and not brand new builds.

And were the tax incentives really attracting investors? Or was it the lure of buying off the plan in the middle of a massive housing boom and selling for a profit a few years later?

Why couldnt FHB be pushed into the new build market instead of investors? That would make more sense (and in the past was how it used to work). They get a brand new house which they will live in for a long time, while renters get to temporarily rent the cheaper older housing while they save up their house deposit.

Where is that post by NZ Gecko telling us in CAPITALS, in bold and in itallic, that following this 0.1% drop, the sky is about to fall, house prices will drop by 489% and that we're all doomed?

Geese, don't know how I feel about living rent-free in Yvers head......

Anyway the continued drip, drop, drip of the housing markets continual decline, has many dancing in the streets with joy.

All apart from the land bewankers and home hoarders.......

Meanwhile, drip drop downwards we go....

If prices drop 0.1 percent every month for 83 years the property will be worth 37 percent of todays prices

So gecko doesnt have long to wait to reach his goals

So strange, no REINZ data today.

it must be very ugly or scary?

stuck in legal

Is it against the law for them to disclose the truth?

They getting the A-team onto this damning Housing market report pronto....

Tony and Ashley huddled into a room, beads of sweat pouring from their furrowed heads, "how the fux can we spin this clusterfux report" "our careers as superspruikers is over"..... how has god damned us so ??

The wailing goes on without reprieve. How can we wrap this utter turd of a report, in candy floss? they ponder on.....

Lightbulb moment: "I know says the devout Superspruiker Ash": "Property Seventh Heaven Returns in 27". Lets run with it, "winner" - shouts old furly locks Tony!

"Thats it! we are saved!"

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.