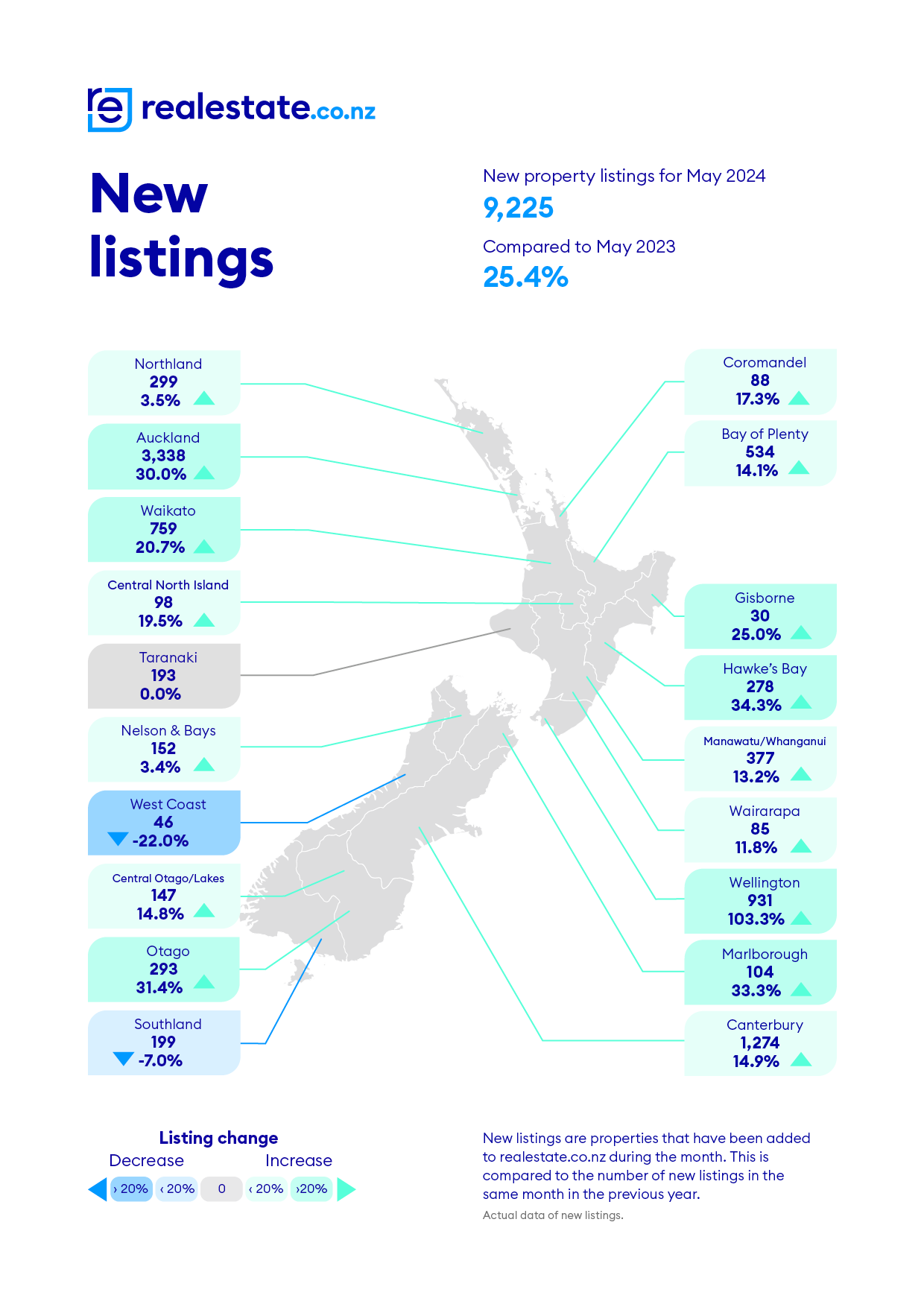

The number of new property listings, the total amount of stock available for sale and average asking prices are all declining, according to the latest data from property website Realestate.co.nz.

The website received 9225 new listings in May, the third consecutive month the number of new listings has declined since the summer peak of 11,788 in February.

However, May's new listings were still up 25% compared to May last year.

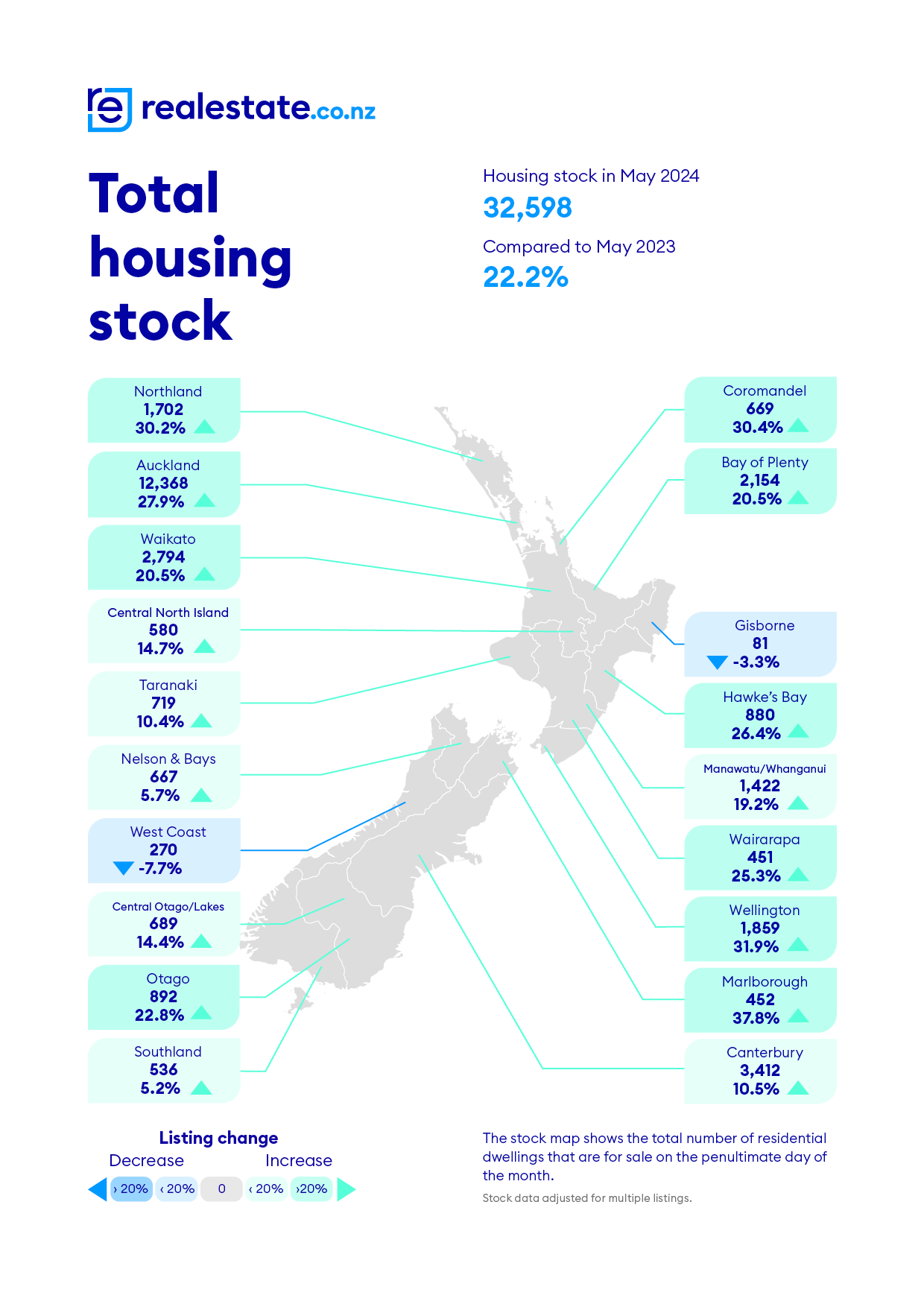

The total stock of properties also appears to have started to decline, with 32,598 residential properties available for sale on Realestate.co.nz at the end of May, down from 33,815 at at the end of April.

That means stock levels at the end of May were up 22% compared to the a year earlier.

A decline in both listings and stock levels is normal for this time of year as the market settles in for the quieter winter trading months.

Asking prices are following a similar trend, with the national average asking price on the website dropping to $845,454 after declining for three consecutive months from $927,312 achieved in February.

May's average asking price was down $14,185 compared to May last year, and down $149,431 (-15%) compared to the record high of $994,885 in January 2022.

May's figures suggest the market is following its usual seasonal trends, however the total amount of stock available for sale remains high.

The decline in asking prices suggests vendors may be accepting they are selling into a buyer's market and are starting to become more realistic in their price expectations.

- The comment steam on this story is now closed.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

87 Comments

Stock levels falling at this time of the year is often because the agents have advised the sellers to relaunch in the spring as if it's a fresh listing and not continue with a stale listing over winter.

Ummm . . . no. A pretty naive comment.

An agent would not advise to take a house off the market. While its sitting there, no matter how unlikely, there is at least some possibility it could sell. Also the agent would not advise that it be taken off the market as there is the risk that the vendor may sign up with another agency. Listings are keenly sought by agents - even for the potential listing fee even if they personally don't sell and get the sales commission - and once they have a listing there is no reason or cost to the agent for the listing to simply remain sitting there. And why would an agent not want to keep it on the market and continue to market it for their commission from advertising revenue at a cost to the vendor?

Yes, a vendor may on their own accord decide to take the property off the market as there is considerable stress while a house is on the market.

Well I'm aware of agents advising this in recent years - so not naive at all because it's based on facts.

They don't need to waste their time running empty open homes and dealing with low ball offers when in the spring you have the perception of a new listing and more active buyers for a quicker sale. There maybe other reasons too - it happens.

Yip was reading about multiple examples of this over the weekend (on the PI FB page comments) - it appears to be a real thing. Listings removed at the agents advice.

If they are not being removed they are dropping their prices.

At the start of 2022 very few believed there would be decent house price falls - as the economy felt solid despite interest rates rising with projections they could double.

Whether prices would fall was a healthy debate for many.

The only real economist that could see what's coming was Bagrie, who said 'it's not looking flash'

The rest of the paid clowns predicted a soft landing for the economy and housing market.

Right now I can't see any reason to believe we're not at the start of the next big leg down in values. On most metrics we still have the highest prices in the world. The numbers simply don't work.

I have about 200 random houses on my Trademe watch list - and every day I get price decrease alerts - some properties are having two in a week.

It's even happening in Queenstown now.

I think the only real debate left now is how much are prices going to fall.

The prediction before every economic/market crash is for a soft landing..why? Because it is human nature to not want to be ostracised by the crowd e.g. the fear of being ostracised as being a negative person or a doom gloom merchant by your friends or work colleagues - even if the economic data clearly shows that trouble is ahead. It is a weakness in human nature - the need to be liked. Is it better to explore what could be true or to be liked?

Yes likewise - I’ve been considering a relocation for family reasons to Dunedin so have a watch list of properties there. They aren’t selling and each day there an alerts for price reductions of $10-50k on these properties.

"They don't need to waste their time running empty open homes and dealing with unrealistic greedy vendors who refuse to meet the market..."

Fixed that for you

Possibly a little unfair toward the vendors. Plenty of real estate "professionals" will set high expectations in their effort to secure the listing. I can imagine it's pretty hard to adjust when the market expert that you engaged for advice and sales prowess is back-tracking hundreds of thousands on their "estimate".

They only have to find one sucker.... but suckers are thinner on the ground right now...

The neighbours are selling. Their agent recommended a really unreasonable sale price. So much so that it even 'outbid' the homes.co.nz estimate by over $100k, and we know what a spruiker that site is. On the market for 5 months now...

That price was fine in early 2023, not 2024.

Correct. It is the response you got that is naive.

https://www.rnz.co.nz/news/business/518569/house-prices-consistent-but-…

However, the biggest price fall was in Wellington with the average price plunging 13.4 percent on April to $739,497, the lowest since November 2020, and 14 percent lower than a year ago.

13.4 percent in a month seems like a decent drop for such a short period.

Prices in Wellington peaked ~$1m. In nominal terms, this would indicate 26% down. In real terms probably closer to 35%.

It's not over yet. What crash?

if you have a closer look at the wellington market, there isn't many decent properties listing at the moment. almost all of them are old, ill-repaired or ex-rentals.

I won't find anything if I am buying to live in at the moment.

Lets be honest here, Wellington is not nice. The terrain is hopeless, its an earthquake risk just waiting to happen and the weather is pretty bad as its always blowing a gale through the Cook straight. Its quite possibly one of the the last places in NZ I would like to live. I really hate old villas unless you built a brand new one to the modern building code.

Nonsense. a lovely city to live in. Beautiful coastline, great food, interesting jobs and great trails and parks.

it might or be for everyone but it is clearly one of the best places to live in NZ. Otherwise people wouldn’t live there!

I mean look at the choices. 90 percent of Nz towns are a dairy, a bakery selling crap, shit schools and a rough pub. No thanks.

And while I won’t claim it is Nelson like, Wellington weather has actually been great for a good spell now. Better than getting battered by a cyclone in Akl or east coast.

You could not pay me to live in Auckland. Christchurch I’m not sure about.

begs the impossible question - where is the best place in Nz to live?

Wellington has the most accessible & cleanest harbour in NZ (with more reliable wind for sailing LOL). Fishing is excellent both South & West coasts.

I was born in ChCh & lived there a couple of times however have now been in Wgtn over 40 years. While the CBD is now a nogo zone thanks to over a decade of useless left governance, I live in the Eastern suburbs & have no regular reason to enter the CBD.

I've considered moving back to ChCh in recent years & may when I'm too old for the hills - it's coming up well with the rebuild & still much better value for housing $ - or I will seriously consider moving to join family in Oz if there's ever another Labour led Govt.

Edit: clean air, no pollution

Can't say the cleanest harbour with sewerage spilling in there on a semi regular basis, but it is a nice harbour. Wind is rotten more often than not but the good days are good there and it doesn't get frosty often due to air movement. You just don't realise how much the wind effects your life until you leave Wellington for a while and look back.

Why is there so much fog at Wellington airport often no flights in/out for days or a week on end.

They get the predominant NW and then Southerly winds every time a cyclonic system rolls over the country, but in the centre it gets very still and often causes this. Can't win with the wind, can't win without!

don't judge Labour. they are not the bad apple that give the left a bad name.

Labour are the enabler.

Wgtn is ok if you're under 30-35. The climate ruins quality of life.

No cyclones in Auckland in winter. You can often wear t-shirt and shorts.

As I am today in Auckland

S u r e ... As I sit WFH in very thick socks, trackies and a warm hoodie...

Still in holiday mode going commando?

Maybe I am weird but I liked Wellington's climate a lot better than Auckland's when I lived there. Humidity sucks.

Frame the question correctly. You have $1m to spend on a house, where do you live - Akl or Wgn?

Yes, Auckland beats Wellington - but if it means you have to work until 65 instead of 45, is it worth it? No.

I honestly like the weather better in Wellington. Everyone always moans about the weather but I never really minded it. Plus heaps of amazing MTB tracks and walks right next to the CBD. To do anything in Auckland ends up being a shitfight against traffic. Main issue with Wellington is a lack of decent jobs outside of the public sector. At least for my industry.

I've made this argument a few times. You can buy a second house in Coro if you choose Welly so it's not as if your stuck there. Just use it as a base for schooling/medical care and have a holiday home by the beach/alps. Prefer that over a $2m average house with traffic nightmare in Akl.

Every time someone comes up to Auckland from Wellington they remark about how warm it is. They do find it too hot in summer (as not used to it) but in spring and especially autumn Auckland is a lot nicer.

Wellington is the nicer city (they haven't quite ruined it with a ring of motorways yet), although Auckland is getting better and Wellington seems to be going backwards.

I find all other NZ cities too small (incl ChCh which feels more like a big sprawl), but obviously some people like that.

Even when I'm used to it I hate the heat. Think it's mostly a personal preference people since I know heaps who like the heat and climate better in Auckland.

Queenstown has them both beat in Summer, nice dry heat no humidity.

I can count on one hand the times I have found Auckland hot - and one of those was roofing.

"Auckland ends up being a shitfight against traffic" - it depends where you live. We live and work reasonably central and hardly ever get caught in traffic.

I'm originally from out west if that gives some context. I think living in central would be a very different experience.

In my opinion the best place to live in NZ is the Queenstown Lakes district. Lived here for a few years now and love the place.

Where I am as well, it's nice having proper seasons. Plus 2 minute bike ride into work can't complain.

I also don't really like living in flat places, having some mountains around is always nice.

@Zwifter

Honest..? 😂

No idea

I think Wellington is a great place if you want to commit suicide but lack the courage.

That's old John Cleese's line for Palmerston North!

Zwifter, Baptist, I don't think it would matter whereabouts in the country you both lived as you'd still suffer from foot in mouth. The convenient gripes you mention didn't stop others buying homes there and pushing the income multiples. As unemployment spreads, other cities will surely follow Wellington house prices down in similar fashion. To explain away falling house prices, will you conjure up gripes about them too? - probably.

Zwifter, I guess this must mean that Wellington house prices are WAY cheaper than they were from August to October last year!

Sigh. Tis a joke Poppy. lighten up.

All good here Baptist. Some of your post's are indeed jokes :) I mean they have to be - surely. Like the one when you said Landlords raise rents to compensate for falling house prices. You were alluding to depreciation along the lines of rental car companies - LOL!

Keep up the great work. You obviously feel there's a need to spin it to win it.

Grown up in Wellington, 12 years in Auckland, 2 years in Palmerston North, few months in Hawkes Bay. I'd pick Wellington anyday, my ideal suburb would be north facing Kelburn or Seatoun!

I don't follow Wellington's housing market but friends who live there say there's long been a shortage of good family homes close to the city/CBD.

TTP

The building code has barely improved since 1992.

Old villas a far better buy than any modern builds. Proper hardwoods. Good drying and drainage. Easy to maintain.

Only upgrades you need is new joinery, ducted heating and ventilation.

Can also look at installation of internal air/vapour barriers and improving waterproofing to kitchen and bathrooms when/if doing a general refurb, but you'd be wanting to go well beyond the 'modern building code'..

Here we go….

We sold an 8yo 4brm home in Miramar in Q1/2020 (early Covid scare, few buyers). QV currently has it valued at our then sold price.

Houses are a bit like a new car, they depreciate a lot when new. At 8yo it was probably still reasonably modern, at 12yo you get to the point where almost everything is looking dated. It probably doesn't depreciate too much after that (except if it has issues).

Link to to QV ?

'13.4 percent in a month seems like a decent drop for such a short period."

Might be due to sales mix, and the impact on "average" price. The REINZ house price index will give us a more accurate picture.

Northland and Coro stock both up. Aucklander's selling up holiday homes?

...and Waikato Farmers. Plenty own holiday homes in the Coro area.

The decline in asking prices suggests vendors may be accepting they are selling into a buyer's market and are starting to become more realistic in their price expectations.

Or may not. They're not ready yet in my experience, on the other hand if they hold long enough (possibly years) the market will catch up with their expectations just for inflation.

Listing's rising, more listings coming when flipper tax window is reduced, debt remaining normal levels (HFL), debt to income limits arriving shortly, and the economy on the skids big time. All drivers for a pricing hit, and further hits.

Return to mean is underway.

.

3 Years 2020-2022. There were 735,656 new mortgages created. First home buyers, investors, business lending, upgraders and refinancing. 244 billion of debt that was taken on at interest rates probably averaging half where the market sits now.

When your economy is a housing market with other bits tacked on. What do you think happens next?

And we can't control the direction.

Was reading today that most Americans would prefer a recession to persistently high inflation. So hfl there and potential for a rise.

I think we will also have HFL and given most people are banking on early 2025 drop... if we have a scenarion where there is no light at the end of the tunnel by Q1 next year... we may see a much bigger longer downturn and correction when people sick of the struggle start to sell up.

65% of American homes are owner occupied. If they have a mortgage it is more than likely fixed for 30 years at a 3 - 4% interest rate. In that situation inflation is your friend.

Just like it was for those New Zealanders who were lucky enough to have State Advanced fixed rate loans in the 70's and 80's.

If US interest mortgage rates had doubled for existing debt within 2 years they would have had an outright depression. The MBS holders on the other side of the trade are getting laid to waste. But as long as they don't have to sell they can pretend they are not losing.

25-Year-Fixed Mortgage Rates

Loan OptionRateAPR

25-Year Fixed *7.375%7.728%

VA 25-Year Fixed *6.49%7.001%

FHA 25-Year Fixed *6.625%7.63%

"we may see a much bigger longer downturn and correction when people sick of the struggle start to sell up."

The current interest rate levels are hurting the highly leveraged. Many are using their funds and they may run out of funds before interest rates fall to managable / sustainable levels (i.e. without requiring any use of savings) . As the highly leveraged run out of savings / funds, they are more likely to default on their debt service payments. Look at the hardship withdrawals from Kiwisaver.

From looking at financial hardship withdrawals over the last 12 months, Hartmann said there had been a 90% increase in KiwiSaver withdrawals compared to the same period a year earlier.

Between March 2023 and March 2024, $262.5 million was withdrawn from KiwiSaver because of financial hardship.

In the previous year, between March 2022 and March 2023, financial hardship withdrawals came to $136.9 million.

“If you look at the number of withdrawals over that time, there has been a 68% increase in the number of people withdrawing,” Hartmann said.

In the year to March 2024, 33,130 people withdrew KiwiSaver money because of financial hardship, up from 19,760 in the 12 months to March 2023

https://www.interest.co.nz/personal-finance/127511/kiwisaver-financial-…

Interesting to see how realestate.co.nz has presented their data linking total stock and active users to the average asking price (all on the same chart without any units). And they conclude that prices have stabilized because, as they put it, 'Both stock levels (supply) and the number of property seekers visiting realestate.co.nz (demand) has increased year-on-year. This confirms the laws of economics, where price stability is achieved when supply and demand are matched.'

https://news.realestate.co.nz/blog/new-zealand-property-market-2024-may

" [nonsensical fantasyland b.s. omitted].... This confirms the laws of economics, where price stability is achieved when supply and demand are matched."

And that !!! Right there !!! ... is the sort of b.s. that gives economics a bad name. How dare they.

Were their methodology in anyway realistic (it's not!) - the makers of top end sport cars would be rolling in the green stuff!

could not agree more.

Starting with a conclusion and then inventing a methodology to fit it

"Starting with a conclusion and then inventing a methodology to fit it"

That's what the property promoters with their vested financial self interests do.

Agreed. #compromised

"#compromised"

Conflict of interest with buyers. Real estate agents do not owe any fiduciary duty to buyers.

Owner occupier buyers: CAVEAT EMPTOR.

Yep, and a failure of integrity.

" is the sort of b.s. that gives economics a bad name. How dare they."

The real estate agents will find any justification that is believable to buyers to complete a transaction.

The motivation to make a sale over rides any factual accuracy.

Mortgagee sales still around the 60-70 mark. Listings with the word 'urgent' up above 550 tho ...

One of the few mortgagee sales with pictures ... primo location.

https://www.realestate.co.nz/42575379/residential/sale/72-compass-point…

WTF was the bank doing here? Risky Bankers at the wheel again?

- So they have lent around 3 mill and then just 1 year later, the owners finances are on the rocks?

This will sell at around a 1 million loss, maybe more, under the price paid just earlier last year.

The current mortgagee iceberg is likely on showing the actual worst 1% or less, of the stressed and in-breach borrowers.

- Bankers are giving out rope, in all directions now!

We should be marking the banks books to market. They all prefer opaqueness.

It would not look pretty in a true Asset to Debt marking

This will only get much worse into 2025/26.

Monoclad, no eves. What could go wrong?

Yup. Definitely want a thorough builders report. Got to factor into the price the higher maintenance costs too. The Council file could have stories to tell too.

Primo location if you love sitting in traffic for most of your life

Hop, skip and a jump to the Ferry. Supermarket 100m away + other services. (Us 'WFH'er couldn't care less.)

Most who live thee get the ferry into the City. So one of the best traffic trips in Auckland.

You can't beat Wellington on a good day! On a really bad day the alpine fault goes off.....

The gravy train really left Wellington with the previous government didn't it?

By bus, trains were cancelled for track maintenance ......

And in true NZ style, the next train isn't due for a very long time.

It certainly is quiet where I live. Even coastal properties in great locations are not selling. Anything above $1.3/1.4m is dead. Who would want to borrow big dollars even if the Bank is willing to lend them to you. Where all this is going to end up at I just do not know. What is certain. There will not be a quick large bounce. Those pesky interest rates are not going to move for some time and the moves from the RB will be measured to make sure inflation keeps going down.

so be slow?

I think when we see lots of mortgagee sales the horse will have well and truly bolted. I believe the banks are all holding hands at the moment and extending and pretending knowing full well that if they start tipping to many people out on the street the general public will catch wind of what’s really going on and will lose any confidence in the housing market and stop buying. Once blood is evident recovering costs will just get that much harder. Correct me if I’m wrong.

Lots of developers are about to drop... that will set things off.

Over 100 comments on all on housing - yet we moan that housing takes too much focus away from alternative investments.

yet no one comments on

With the fall in the New Zealand dollar against several major foreign currencies in the tax year to 31 March 2024, the paper gain for many may be more pronounced this year. Under New Zealand's tax settings for FIFs, owning such shares can result in an annual tax bill based on 5% of the valuation of that investment.

I don't think FIF is going away. It probably brings in a lot of tax that they now rely on and not many are complaining about it. The 50,000 threshold means many aren't affected by it. To even the playing field as you suggest - a land tax could be the answer.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.