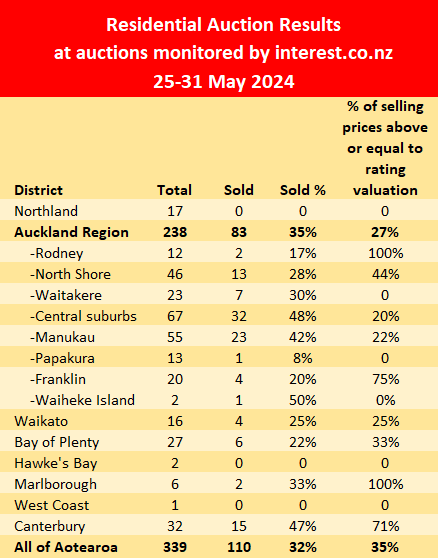

It was groundhog day at most of the latest auctions monitored by interest.co.nz, with the overall sales rate remaining stuck just below a third for the fifth week in a row.

A total of 339 residential properties were offered at the auctions we monitored over the week of 25-31 May, down from 375 the previous week, but up from 315 the week before that.

Of the 339 on offer, 110 sold under the hammer giving an overall sales rate of 32%.

The overall sales rate has hovered between 30% and 33% for the last five weeks, suggesting the market is settling in at that level for winter.

The table below shows the regional results from the auctions we monitor around the country, and details of the individual properties offered, including the selling prices of those that sold, are available on our Residential Auction Results page.

- The comment steam on this story is now closed.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

171 Comments

The only smart buying, is those paying a few hundred grand, WELL BELOW, THE ABSOLUTE STERIOD INFLATED current RVs.

The areas where the no one (0%) pays above RV, maybe getting reasonable deals, time will tell in 2 or 3 years time, as the bottom of this once in a lifetime, NZ housing market bust, finds 7 to 10% Yield support.

Currently, this buyers market has ZERO confidence, of prices holding the current value. Falling knives cut deep.

EARNINGS ARE IMPORTANT! A lesson many have plainly forgotten, in the blindness of greed.

When the new, official RVs are reset much lower in the comming months, based upon much lower average sales prices, reality will sink in for vendors expecting moonbeams for their shacks on 600 to 800 squares.

Those stupidly paying near or above RVs, will see the still outgoing tide undermine their tenuious foothold!

2015 prices, here we come......

Shoppers, it's time to play lowball. The well informed Vendor will have their eye on the ball.

Have their eye ON the ball, BUT what will they DO... put simply a lowball is easy to kick not catch

Today your post reads like you're a Vendor. Yesterday you were a shopper.....

Tomorrow?

Hey I resent that. A minute ago you had this to say

by Retired-Poppy | 1st Jun 24, 8:03am

You're incredibly smart

Stop monkeying and modifying posts to suit

Fair enough, I thought you might take it as a compliment so I removed it 😆🤣

Are you trying to reinvent yourself?

I think what you're referring to is where I said "their eye".. No am not a vendor, save your labels

You are going to have to be prepared to waste no end of time and money to be successful low balling sellers. Its not a car you are buying its a house. Most sellers are in no hurry to sell and they will just kick you into touch.

Zwifter, with such a negative response such as yours, it's no wonder some people miss out on precious money saving opportunities. Stands to reason when It was you that posted August to October was the last opportunity to buy.

Timing IS everything. 2020/21 buyers thought they timed it perfect, now its the FHB's turn at giving it a better informed shot.

Timing definitely isn't everything. Even your own promoted system relies on someone being disciplined over a long period of time and then striking. Hell, when you bought, it was right in the middle of an upward cycle, you aren't even a benefactor of your own advice of capitalising in a distressed market.

You have a significant say over your own approach, methods and goals. You have almost no say about what a market is doing at any given point in time.

.

Based on the comments here today, there’s still abundant enthusiasm for the housing market……

Forever the flavour of the month. 😋

TTP

If housing is by far and away the most popular topic on interest, that should give you some indication of it's importance to the wider public.

Agree: housing is up there with sport, celebrities and crime. 🥷🏻

TTP

...speaking of crime.

Such a dumb line of reasoning. Homicide gets a lot of attention too. Doesn’t mean (most) people value it. Likewise, the housing market is a crimescene.

August to October was the best time to buy, how long are you going to wait now for prices to drop ? Sure prices could drop from tomorrow but what if they don't ? how long are you going to wait ? 6 months ? a year ? 5 years ? its pretty simple, the longer you wait the more likely that prices will have increased.

“its pretty simple, the longer you wait the more likely that prices will have increased.”

So you wouldn’t mind explaining how house prices are going to increase while rates are held HFL, listings continue to pile up and the global economy deteriorates?

Sure but you first answer the very simple question, how long do you wait to buy from today ? Feel free to come back anytime in the future and tell us that NOW is the right time to buy, we are all just sitting here waiting.

Zwifter you’re the one trying to give people advice to buy - you should provide some information to back up your claim. Or maybe you can’t?

The time to buy wasn’t last year, it isn’t now. It will be in the future when prices have corrected further.

Zwifter, my partner used to flick 30 houses a year in Manurewa back in the day.... ITS ALL IN THE BUYING mate....

Funny now you can hardly sell them

You might not have to sell buddy, but buyers aren’t the ones holding the debt grenades.

Which side of the fence has more time on their side…

Thought so.

Surely that depends on the area? There are plenty of suburbs around where RV would be a good deal comparatively.

Can anyone please give some plausible reasons why property prices will shoot up significantly again over the next couple of years?

Personally, I think they’ll drop. Fear and à deepening recession is in the air.

We all survived mortgage rates of 20%, 50 year ago, didn't we? Yes, because here we are, again. That's the way the Central Banks are going to look at the current situation and DROP their guidance rates (OCR etc) even into the face of current stubborn inflationary headwinds. That will allow those who have to, to refinance for as along as they can. Then, voilà, back to ramping the official rates up to control the 'unexpected' runaway prices of everything.

And just as we did in 70s, there will be that brief window to get as much debt coverage as possible before rates skyrocket. It won't matter to lenders, as their collateral (property prices) will have enhanced price levels to back the lending that will be done in the future. There is no other option left now.

Good to see you're back 🎉

Lenders have given wrong misleading advice on interest rates over the last 3-4 years, either wilfully or ignorantly. First to say that rates would go even lower, then recently to say rates would go even higher. This works in the banks' favour both times

Central Banks are going to look at the current situation and DROP their guidance rates (OCR etc)

Of course they are but the important question you aren’t addressing is - how much are they going to drop the OCR this time?

ZIRP is long gone and we’re now paying the price for it. 1-2% cut to the OCR won’t be enough to save house prices from dropping further.

I think this is very true. Surveys are revealing that while people believe interest rates will drop going forward, house price expectations are still weakening. Fewer people at open homes.

https://www.interest.co.nz/property/127981/asb-survey-shows-more-people…

Mortgage sales are almost zero despite the relatively higher costs. A 1-2% drop will help some

Banks are allowing default thus suppressing reality.

You’re correct FH. A 1-2% drop will certainly help some PEOPLE

But we’re talking about the house PRICES. Will it be enough to turn falling house prices around?

Mortgagee sales aren’t required for house prices to drop.

Yes "Not Required" however m'gee sales do prise out some properties, regardless of price. Those lowballers get satisfied.

Flying High, the bigger picture suggests we are not even near the worst of the downturn yet and you could ask what will it will be like in six months? It could be argued this cost of living crisis is a slow moving train wreck. This aside, risks of all sorts are building overseas that are beyond our control. It would not surprise me if we get a Global shock and subsequent crash. Buying opportunities galore beyond the clouds. I've seen and lived it all before.

Mortgage pressure / cost of living pressure in general will no doubt be motivating many to exit. Mortgagee sales are easily manipulated by Landlord banks and are a last resort. It's not a good space to be in.

TTP will argue NO recent buyers regret purchasing much aligned to the ignorant belief "there is no emotional depression and poverty in NZ"

Late last year you predicted that March/April 2024 was the precipice.. that was also 6 months into the future

As said before "you're all over the place like a rash"

Precipice? What a convenient word. I would use something more positive like "opportunity"

by Retired-Poppy | 31st Dec 23, 11:48am "House price falls by way of (HPI) measure will once again resume during April and be reported in early May. Aided by the restoration of Brightline to two years (01-July), rising unemployment, the continued intensification of financial stress and more financial nightmares reported in the media, sellers will feel more motivated and therefore realistic in their expectations and buyers ever more cautious. Selling pressure will be somewhat more intense and endure well into the following Summer.

I have on several occasions suggested that saving FHB's prepare to make lowball offers from about now.

Much to your frustration, I've been clear and CONSISTENT.

by Retired-Poppy | 3rd Oct 23, 11:55am

"Evidence suggests this dead cat bounce will soon be in the rear vision mirror......"

....and your priceless response was;

by Flying high | 3rd Oct 23, 12:55pm

"Is that humour from you"

Wow a double reply, how often does that happen.

Whose the good boy then... you are.

Ooof, RP has the receipts…. That’s embarrassing FH…

No there is nothing embarrassing for me. My recent hunch about the exchange rate popping up to over 60usd was right on the money. I was the only one here who had that opinion. I can name others who were predicting carnage but I'll leave it for them to fess up

Good luck there.

"Distressed prices in 3-6 months!"

Then

"No, actually maybe in another 3 months"

Then

"This time it's for real, couple months away, honest. Bobs your uncle"

Then

Look, just save up enough to buy most of it outright.

Or just cast shade on some imaginary predictions counter to your own that haven't come to pass, that'll put people off the scent.

Nobody likes to relinquish home ownership. 🏚

Once gone it's hard to get back.....

For many people, there's only one bite at the cherry. 🍒

TTP

I don't think they'll shoot up. But neither drop significantly. I think we are now at a stalemate that'll last a year or two. So I'll try to answer your question without full personal conviction. Why will prices go up?

1. The OCR has peaked and will soon be tracking down. CPI Inflation is inside the target range for the last quarter.

2. Retail rates are already dropping.

3. Rents are inflating by 12% in Auckland.

4. Repatriation funds from Australia

5. High immigration.

6. Low consents.

7. The rising unemployment rate for the most part won't effect those who are on the cusp of entering the market.

8. Building costs are very high. As existing houses are a supplementary good. They will go up too in time.

9. Interest deductibility is back.

10. Even in this tight market, prices are already tracking up. HPI up 0.6% from start of the year.

1. If rates have peaked, they’re sitting on a plateau, not a pointy mountain top.

2. it’s a trap.

3. Rents are set by renter incomes only

4. lol like a developing country?

5. We have high immigration now, and it isn’t making a dent

6. there was a glut of consents, building is catching up, they’ll tick up again

7. lol what?

8. Short term issue being addressed by Nact policy

9. so is dti

10. inflation is running way above that and volume is basically zero. We’re in a unrealised crash.

ZIRP is over. Housing minister is a YIMBY. You can’t outrun incomes forever. Time for the regression to the mean. It’s over.

You can’t outrun incomes forever. Time for the regression to the mean

Nothing is forever, but if you think what we have now is peak housing values outstripping incomes, you could be in for a surprise.

There's a lot I could reply to but let's stick with point 3. How can renters income be the only factor in determining rent? If that were the case, why have rents in Auckland gone up 12% in the last year while wages have gone up 3-4%?

This is the situation where supply is constrained.

Rents in the Auckland CBD declined several years ago because of the closed border and the lockdown, so there was slack, and competition in that rental market. Rents shot back up again as soon as it hit the (constrained) capacity again.

Overall, supply is severely constrained in NZ, so no other factors matter. Landlords won’t pass on interest deductibility, nor will they pass on increased rates. They’ll probably take the renters’ tax cut too.

Hi 1689 Baptist,

Much of what you say above resonates with me.

Nonetheless, I do hope that the OCR will not "soon be tracking down". The OCR is our best hope of keeping the lid on inflation - a phenomenon which is caustic to both individuals/firms and the macroeconomy. It includes spiralling house prices and rents.

Also, "higher for longer" interest rates will provide a degree of market discipline - cautioning those who, imprudently, have become over-indebted through there own imprudence. It seems every generation needs to learn about the perils of over-borrowing. It's a scourge with far-reaching ripple impacts.

TTP

Can anyone please give some plausible reasons why property prices will shoot up significantly again over the next couple of years?

If a "couple" is literally two years, there's probably not too many reasons, given the economic malaise or decline we're going through.

If you're talking about 10 years, there's a range of factors which could make prices continue to rise.

And then there is this little issue called Demographics....

Zeihan has some great data on China, probably shouldn’t have messed with reproductive rights, but then again when does the CCP get anything right…

They were always up against it by having the largest, fastest instance of urbanization in human history. The one child policy was just kerosine.

They are so screwed by the old one child policy and now too many men not enough women...

Too expensive to raise a child and buy your way into education... Total mess.

Cities everywhere make children a liability.

Although Chinas super high youth unemployment indicates maybe manpower isn't their biggest problem.

Likely to play a significant part of the story of the 21st century.

Within that though, is an increasing amount of migration, and a supply of hundreds of millions, if not billions of people motivated to be somewhere they're not. And more likely, relatively stable democracies not near hostile zones will retain appeal.

Auckland sales rates seem much higher for the areas closer to the city. Although a small data set.

If you have ever driven in from the outer burbs in Awkland during peak, you will clearly understand why the stuff in the middle is priced the way it is. Stories of 3-4 hours travel every day, 5 days a week, how many years of that can people put up with that, then there is the fuel cost.

Remarkably stable

Yes stable today, at much lower prices .....then the other 3x shoes to drop in July and then later in 2024, will test any thoughts on NZs General Financial Control or stability.

ANY support will quickly evaporate, like a fart in the wind.

Hot tip: Can’t drop if you never sell.

Hot tip: Sticking with an 'investment' that makes 1-3% per annum is just stupid.

"Hot tip: Can’t drop if you never sell."

But the costs of holding can send you into bankruptcy.

If someone stands on the train tracks long enough, sure. When most people are faced with added costs, they usually modify behaviour somehow in response.

- increase your income

- decrease other expenses

- finance the shortfall

Selling is usually the last option.

Selling fast is often the BEST OPTION.

Sell now and only lose 20%? or sell last and lose everything!

Selling for some people could be their best option, but like many obvious life decisions, many people will wish their unlikely desired outcome to be the inevitable one. Especially if there's a supposed relief somewhere in the near future.

Then again some people will panic and bail on something at the first sign of discomfort.

The consensus on this site seems to assume the latter is more common than the former.

The key factor is how much leverage, as it bidirectional. Plenty of seminar believers all hocked up on interest only which is being exposed as to much leverage. As prices drop and algorithms spiral downwards, equity thresholds at banks are triggered. The proverbial "show me the money" moment. A show stopper for those that don't have any.

🍿 fried in 🌶 sauce

Haven't ever been to a seminar - you have significant experience here?. Do we know the amount of low equity, interest only investor loans have been written in the last 5 years?

My understanding is that banks had been curtailing interest only mortgages even before COVID, but some data would be interesting.

Hi Pa1nter. I can't give you national data, but I can tell you that I have 3 interest only loans.

It’s going to be interesting when the new RVs are out. It’s going to cause some issues for those selling to go to retirement villages when they have been using figures from their home sale that will no longer materialise. It’s not like these people can wait 5 years for a recovery in prices.

Fantastic let the correction begin.

Anonymous member's Post

Property Investors Chat Group NZ

Anonymous member

Cashflow problems

I have 2 investment properties in Auckland which were neutral cashflow few years back but after doing cashflow analysis for this financial year they will cost me $28k a year ($550 per week) to top up.

Realistically i could probably hold on for another year (maybe two) at these interest rates but wanted to see if others are in a similar situation and what their thoughts are?

Are you just praying interest rates will come down?

Are you going to increase your rental prices up dramatically? (I have done mine recently to market value)

Cashflow is really tight atm so i wouldn't be able to refinance to another bank to get Interest only, extend the term.

This, X 100,000 Plus.

Its why if the market moves up there is a wall of overhang prepared to "Get out flat", some will chase it down, not looking at wasting everyone's time level offers....

Some will flip flop Nothing is truer then the fact that

Fear turns into Greed at Breakeven!

A response on the same thread.

"We are in the same boat with ours, it’s costing up to top up the mortgage and the property needs work, which we just can’t afford…

Can’t wait to sell it!"

IT Guy - another this morning:

‘I have two units which I bought in 2021 which then were putting money in my pockets. However, I’m having to top up $30,000 yearly($2500 monthly) after rent and it’s getting a bit hard to pay it. I’ve had it listed with 2 agents last year but it didn’t sell. Can anyone suggest what is a good solution at this point of time?’

Something will need to give soon - either interest rates or sales volumes (Ie with falling prices).

Not every investment is an asset if the cash flows don’t justify the purchase price - which was always going to be extremely risky if buying when the discount rate applied to future cash flows of the asset were incorrectly determined as being near 0 (ie the assumption interest rates would never rise like they have).

It is then possible to realise you have invested in a liability and not an asset. Ie it costs you more than it returns. This appears to be what those holding negative cash flow investmen property are waking up to - you don’t always win with property - most of the time you don’t but when you don’t it can badly wrong (ie it was a leveraged bet buying during covid that didn’t allow for rising rates).

This is not an investment, its a boat anchor.

Options sell at a loss...oh no. Or wait for the Bank to do so when interest only finishes. A poster child for the last sucker.

I see in the Herald today that property prices are up. Since the trough, 2.9% in Auckland and 3.33% across NZ.

So much for the great kiwi property crash.

Every dead cat bounces, when a fully laden DDDEBT truck, hits it square on.......

Dude...if you believe what the Herald publishes as a front for the RE lobby, your not as smart as you make out. It's only use is helping light the fire.

"I see in the Herald today that property prices are up. Since the trough, 2.9% in Auckland and 3.33% across NZ."

Link please. I can't find that article.

This mornings Herald....I bought it. Page A11.

Headline? Author?

"I see in the Herald today that property prices are up. Since the trough, 2.9% in Auckland and 3.33% across NZ.

The property promoters don't want those that are uninformed to know the full picture. Hence the juxtaposition and marketing spin of positive price momentum to try and convince the uninformed.

"So much for the great kiwi property crash."

That is what the property promoters want the uninformed to think. People are free to choose what they believe, however people are not free to choose the consequences of their choice.

Something for people to think about. When was the last time house prices

1) in NZ, fell 15% from their peak in nominal price terms?

2) in Wellington, fell over 20% from their peak in nominal price terms?

3) in Auckland, fell over 20% from their peak in nominal price terms?

The highly leveraged buyers of the 2020 - 2022 period are going to be under cashflow stress and mental stress. Unfortunately some will resort to self harm.

Residential real estate is the largest asset class in NZ, that was valued at $1.76 TRILLION - a 15% fall means a fall in value of $264 billion (this is more than the entire market capitalisation of all the companies listed on the Stock Exchange of New Zealand). Can anyone think of any other larger fall in wealth in NZ history? (either in absolute nominal dollar terms, inflation adjusted terms or relative to GDP)

What are the consequences of such a fall in wealth?

How did house price risks get so elevated?

Reminder of the narrative of the property promoters at or near the peak

1) Tony Alexander - 19 reasons why there's no crash - December 2021

https://ndhadeliver.natlib.govt.nz/delivery/DeliveryManagerServlet?dps_…

2) Catherine Masters - July 2022

Why the New Zealand housing market is nowhere near crash point

https://www.oneroof.co.nz/news/why-the-new-zealand-housing-market-is-no…

3) Ashley Church - April 2022

Four reasons the housing market won't crash

https://www.oneroof.co.nz/news/ashley-church-four-reasons-the-housing-m…

4) Kelvin Davidson - Dec 2021

“But will prices actually fall? I’m not convinced because in the past a serious housing downturn has come with a recession, but no one is suggesting that and unemployment is low at 3.4 per cent.”

https://www.stuff.co.nz/life-style/homed/real-estate/127305870/what-lie…

5) Nov 2021 - Here's why it might be fruitless to pin your hopes on a house price crash

https://www.stuff.co.nz/business/300449314/heres-why-it-might-be-fruitl…

Man alive ... This really was a budget for Landlords !!!

1. LLs got interest deductibility re-instated (essentially a tax cut) ... But wait, there's more ...

2. LLs also got the PAYE tax cuts ... But wait, there's more ...

3. LLs' tenants - yes, their tenants - got PAYE and various other tax cuts so their disposable incomes increased ... so LLs will be able to push through even more rent increases !!!

Man alive our tax system is going to ruin NZ.

Does NZ have so many LLs that they can dictate government policy when they vote? Or are Kiwis so dim they can't see what's going on and vote to be screwed?

Awesome budget for you then.

Our movement away from production towards consumption and luxuries is what'll "ruin" NZ (potentially already ruined, it's a bit of a one way street).

Tax policy around landlording is trying to find somewhere to put a burden that realistically can't be afforded under the current housing configuration. The government can't afford to be the landlord it supposedly needs to be, and private landlords need enough incentive to undertake it themselves.

Or they could sell and have an OO buy the property for their family. Rent is not the be all and end all and we used to be a country with pretty stable housing & house ownership (which was primarily used to support children with a stable upbringing & retirement housing for the owners). Losing significant house ownership in NZ has done a huge amount of destabilisation in the fabric of society (from unstable childhoods to more high social cost & unstable retirement). There are actually very few itinerant workers incomparison to people who want and need stable housing to live in an area long term (1yr+).

OO also used to rent to working singles who were more itinerant to supplement income and for the boarder to have a lower cost then renting a whole place or pay by room rentals.

"Awesome budget for you then."

Not really (1). I haven't increased rents since covid and have no intention of raising them until the RBNZ takes its foot of NZ Inc's throat. All of my rentals are dwellings I have built. (I do have 3 three beneficially owned that I didn't build but these are 'trading stock', pending development.) That makes me pretty unique among NZ's "property investors", i.e. I really do invest, I create new stuff, some gets sold but some I keep.

Not really (2). By my calculations, the RBNZ is likely to see the tax cuts as being potentially inflationary. This means they'll (wrongly) hold rates higher for (as I've already said) way, way longer than they should. Now that really pisses me off. Why? Because I won't be building anything new until i-rates come down and I'm not lining the pockets of bwankers. Further, while the RBNZ persists with this foolishness, NZ Inc will continue to go nowhere - or further backwards. Or put another way, the potential purchasers of stuff I produce are getting poorer, or fewer, so my potential market is shrinking.

So absolutely NOT an awesome budget for me. ... Unless you consider the nickels and dimes handed down as tax cuts 'awesome'.

So much of your business is dependent on discretionary spending requiring cheap access to credit?

Most governments' activity end up being inflationary at some sense. You either give tax cuts or financial relief, or you're spending money on projects.

Oh well at least you're going to benefit more than most from your IP tax advantages. A consolation prize perhaps.

"So much of your business is dependent on discretionary spending requiring cheap access to credit?"

No.

What a wanky / dorky / ignorant thing to conclude.

"Most governments' activity end up being inflationary at some sense."

Total bulls1t !! Prove it.

Not engaging further.

This is much of our economy, and your own post sights higher interest rates (for longer) worsening the liquidity of your clients. So a fairly reasonable assumption, but clearly touching some sort of nerve. Try not to assume what I'm saying to you is in the form of some sort of personal slight, even though that's how you want to roll. I'm super not interested in what you think of me, and I don't really have any interest in engaging in some sort of teenage internet shitfest with you.

Business trading environment is definitely much better when you have a populace flush with cash. Not only do they actually have the money, but with it the confidence to consume and invest.

You are highlighting the fact much of this is now dependent on low interest rates. Is that a potential problem? We are currently finding out.

Lol, so you're not engaging further, and then a few minutes later, engaging further by

a) editing your post

And

b) including a question for me to answer in your post

How are government decisions not inflationary, if they result in spending money (either they spend it directly, or they give/refund/rebate it to someone to spend)?

Chris are your IP mortgages paid off now, you dont qualify for deduction

Like I've said, there are good financial reasons for having a mortgage even if you don't need one. (And all have significant, unused revolving credit facilities attached.)

Well, that and even if you have money, debt allows you to retain some of it for other things.

Wonder how many small business owners also have investment property debt.

Wealthy people buy when everyone says sell. The Rothschilds were experts at it.

They could afford to make some mistakes. Joe Average does not have that luxury.

If they're as aware as the likes of the Rothschild's as to how the system works, then it's probably their best opportunity for advancement.

Taking risks is how people get rich in the first place. Not pumping out kids, buying homewares or cars on tick, or being big spenders.

You seem so fixated on being rich. Some people just want to be happy and therefore have kids and buy things. Horses for courses. I am probably rich but I can guarantee there are people out there happier than me and they are far from rich. They probably have richer lives than you or me.

Getting wealthy is a psychological aspiration many don't have.

It's worked for me and it works for others who are prepared to give it a go and make the sacrifices.....and then there's the Marxists who say it's all unfair and such affluence needs to be taxed until the offenders are the same as everyone else.

I disagree. Many want to have enough or be comfortable. They know being wealthy does not make you happy. People make you happy.

In this day and age, having enough to be comfortable is being wealthy.

I agree. I have done enough travel and probably have had the best of it. My wife and I love spending time with our children and grandchildren. And we are shovelling our children capital as what we give them now we don’t need. We only need a car each, a warm home and good food and coffee.

Yeah but probably, you're capable of accomplishing this because at some point you had to make wealth creation/retention a larger priority in your life.

Presumably you've also been at a point where it was hard paying all the bills. For most people, harder to really be at ease and happy in those circumstances.

I too can see that hedonic treadmill, many of my contemporaries are well sucked into it. Relentlessly pursuing either more money, or material attainments. Which I spose is fine, if that's what you find value in. But life is fairly short, and a meal is as good as a feast.

"We only need a car each, a warm home and good food and coffee."

A reminder of things taken for granted that we all need:

1) personal physical safety

2) physical safety of loved ones

3) personal good health - physical and mental

4) good health of loved ones - physical and mental

For perspective, a wealthy relative has recently discovered that they have late stage cancer, whilst another relative who had cancer very recently passed away.

Other friends have dementia.

Another family friend recently lost their child aged in their early 20's due to self harm.

Most of those scenarios are easier if you've got decent funds.

Wealth has made me extremely happy...happier than you can possibly imagine...don't believe that BS that money doesn't make you happy...it's crap.

You're correct, at 19 I was poverty-stricken after paying to learn my trade, and my father gave me $50 as I got on the aircraft to head overseas.

You keep believing that. There are a lot of people who are not wealthy who will be happier than you. An old friend said to me once, “life is about people not things.” He was right. Wealth is a thing. You might be happy but you would be happier if you made people your driver not wealth.

Probably, the "happiest" people I've encountered have bugger all.

But they're also unlikely to lament not catching enough crumbs.

Living in countries where everyone is in similar circumstances.

Mmmm, mostly, although not exclusively.

I doubt anyone could be happier than me.

I do what I want, when I want, how I want. I wake up in the mornings and think "what'll I do today". Both my kids are in Aussie, with my blessing, so I'll be decamping shortly to spend a few weeks there.

The money has bought you independence and full control over your life, its not the things you buy that make you happy but that said it really comes down to your personality, for some people enough is never enough when it comes to money so they are destined to be miserable for life.

If someone can live a life where money doesn't factor in so much to their day to day existence, that's often a beautiful thing.

For everyone else though, unfortunately they have to have a more financially orientated outlook to help ensure their existence. If you're relegated to working for 50+ years just to survive, you're better served making the most of the time you're spending having to work.

Like living off the land. Maybe you can get by on berries and foliage, but it's a lot easier if you learn to hunt/fish.

Well said ex agent.

I'd also point out that they chose their parents well. And were educated to a good / high level. Very few - in fact extremely few - have those advantages. (All facts that providers of folksy wisdom often seem completely ignorant of.)

Yep, it's very, very hard out there, with little margin for error. And getting harder.

So you're better to learn the averages, and play to them (via folksy wisdom). Highlighting ad nauseum how tough the world is, doesn't put any more food on your plate. It's more often an added impediment.

Or maybe a source of appreciation, or reciprocated gratitude, depending on your bent.

Cringeworthy.

Well, at no point have I ever said it was easy, nor heavily biased towards ones' parentage.

Being financially educated and disciplined is even more critical for those worse off. And it's possible, albeit increasingly harder for someone to elevate themselves financially.

Yeah, I've seen all those poor "happy" people in the news, whining and grizzling that they didn't get enough in the budget. And telling us all how tough life is with 4 kids. No one forced them to have 4 kids.

You certainly have a mean steak in you. You do not sound very happy to me. If you were truly happy you would have some compassion and empathy for those less fortunate than you. You certainly show us your age.

I'm happy, see my post above. Only morons denigrate others because of their age....and that's you buddy.

You use the word moron. Pot calling the kettle black. Nearly every one of your posts show us you are unhappy. A happy person would not post the nasty comments you constantly make about those younger and less fortunate than you. If we are to believe your story you strike me as a measured and driven person who has had very little spontaneity in life.

You're the socialist wanting to strip the money from those that make something of themselves. I'm happy alright, more than you can possibly imagine, not a worry in the world.

I am not a socialist. I just have some empathy and compassion for those less fortunate than me. That includes donations and gifts and helping charities with governance. Do you do anything for anyone other your family? I suspect you would find that hard to do as they would be lazy bludgers or failures in your mind. Your posts constantly attack working class people with large families.

There's a lot of common sense involved in life, and there's a shtload of people who don't apply it. The jails are full of them.

I had great parents who encouraged us to go to Uni. Not everyone has such good parents, has the same amount of grey matter or even the same level of physical or mental health. As a society we need to help them. You would have less wealth if everyone was as shit hot as you say you are.

I never went to university, but I acquired a skill that was very handy and paid pretty well.

I've paid millions in taxes, so get off the guilt trip because it isn't working.

I understand that as narcissists do not understand guilt. Having lots of money(or so you say) makes you happy. You cannot get shallower than that.

Waffling on, promulgating glib, pathetic, socialist views on a daily basis makes you happy. How people like me should be paying more taxes and being a better citizen. What a load of BS.

I have never said you should pay more tax. I am just saying that there will be lots of people who are not wealthy who will be happier than you as you are obsessed with wealth. They are being good citizens and that makes them very happy.

Older Indian ladies go to cafes with their Indian woman friends and have a ball. They are affluent and rich from years of hard graft and very happy to be in NZ not the homeland. No uni degree between them just proud doing basic jobs well

Yeah you're right agent, wingman just comes across as a bitter narcissist. Sounds like he's desperate to convince himself of his own happiness.

The line about his children being in aus with 'his blessing' is very telling..

I'm happy alright - no boss, no job, heaps in the bank, no debt and a new house under construction in Auckland. I travel and do whatever I want. Life's sweet as.

Yep, my kids are in Aussie and I've suggested they stay there.

Don't believe all that BS that money doesn't make you happy, and if you want proof go onto FB and look at the posts that the budget didn't give them enough.

I come across different from you guys because I'm a contrarian, I bet against the herd.

At your ripe old age you should not be working. If you have the money you say you have why don’t you help your kids so they can stay in NZ. Then you could see your grandchildren more often as people are more important than money and things. Why have your kids gone to Aussie. We have a great life here.

I'm fit as, I walk miles several times a week, I'm not some decrepit codger in a wheelchair. My kids went to Aussie because there's more opportunity there. I see them often.

I have helped my kids, and they're making something of themselves, they like it there. I'm proud of them. Why do you think so many kiwis are abandoning the NZ handout ship?

To get away from their parents who are often so ignorant and out of touch.

A double up sorry

What do you do in your retirement? Play cards, trainspotting or go to painting workshops? Maybe for you, not for me, I like too build houses and do something I find stimulating and useful.

And if leftists like Comrade Ardern ever get in again, I will certainly pull the plug and move to Aussie.

Something you do to make money which you absolutely love. Have you not got enough? What’s wrong with playing cards? I don’t but if I did it would mean I am more zing with people which is good for us as we age. You should try socialising with people. It might make you less grumpy and more tolerant of people who live differently from you. My children would be horrified if I spoke about Jacinda the way you did above. Misogyny and narcissism comes to mind.

Arden is the most vile PM that's ever inhabited Premier House. She almost destroyed the NZ economy, wrecked the airline and tourist industry, and locked NZ citizens out of their own country.

She should be prosecuted. "Be kind." What a load of BS. The biggest favour she ever did NZ was to quit.

Wow I thought you were of that ilk but you have really revealed yourself now. You have absolutely no empathy or compassion for anyone. What about the frail old people and the very sick. Those with cancer including children who had very little immunity. Sorry in order to protect my wealth we will leave you to die. My first granddaughter was born in January 21. Did she not deserve our protection from something that killed millions including doctors and nurses in hospitals.

You're getting a bit carried away there old chap....might be time to retire from the debate gracefully.

People’s lives come before money. But as you obviously love money and live down a rabbit hole you would not agree with that.

I'm guessing wingman grew up when lead was present in paint and children's toys, with his exposure levels significantly higher than the average person. Maybe he had a penchant for tasting the paint straight from the tin when he was a child and nobody was looking?

Even low level exposure has a huge impact on intelligence and makes people less agreeable/lack empathy.

Everything's tickety-boo in my life, esp. my bank account.

Jacindas big monument the Christchurch Call is crumbling. That was happening naturally and National tried not to cast too much shade on her as people like yourself would feign anger

Lets see if she can keep it alive and the donations rolling in

The National Party received record donations in 2023, and now that failed PM Hipkins has been reduced to begging his flock for alms.

We are a mid 30’s couple. Had owned a 1 bedroom unit, central Auckland for about 10 years, sold it about a year ago, now watching the market and waiting to ‘upgrade’ when the right house at the right price comes up. So far we have put offers on 3 houses and been outdone by 100k more each time. No regrets though as we feel our offer was reflective of where we believe the market to be / heading. We cannot understand how so many people believe in the current value of homes in Auckland. Time will tell if our wait to re-enter the market is fruitful.

We cannot understand how so many people believe in the current value of homes in Auckland.

This is a phenom of most growing cities. Very often they have significant demand and supply side pressures. The perception of which further drives values and urgency.

I understand that for the past 5-10 years. But now we have a LOT of new builds and more people choosing to move away, than to Auckland, at the same time as a cost of living crisis.

I’m obviously biased, hoping for a small reduction in housing prices to help us get in (along with the belief that this will be great for others in our position and younger generations that currently have no hope of home ownership). The reality is, if this doesn’t happen, we will look to move out of Auckland. Maybe that’s what the people helping prop prices up actually want?

As an ex Aucklander I can't really endorse staying there, but it seems to be the countries largest draw of new bodies so presumably it's desirable to most.

Does Disneyland drop their prices in a sluggish market?

No but they offer bigger discounts

.....queue side eyed Chloe meme

Auckland is where the action is, where the jobs are and it's the place many would prefer to live rather than join the commute queue each morning from Warkworth or Hamilton.

In the long term prices in Auckland will outstrip surrounding areas.

looking at the numbers Rodney has the lowest clearance rate next to papakura .Have noticed the Millwater ,Milldale vendors have a high expectation of prices compared to their CVs . They could be in for a big shock when it comes to meet the market time.

The Millwater houses are not selling well, perhaps it is their price point in the market, they are generally OK well built.

Lots are in the $1.5-1.7 mil range. Tough place as this is 2nd home range but many FHBers from 5 years ago do not have enough equity to step up and why mortgage yourself for 800k here?

Dick Mammoth, Hugh Jorgan. What next... I hate to think

Auctions are so stupid

They're not real auctions, duh

so many listings, so little interest. but vendors seem to be refusing to panic. despite being told by multiple agents that their vendor is desperate to sell, when they see my lowball offer (c. 20% below CV), they say they will take the property off the market. I’ve put 3 offers in during May. never got closer than 20% between my price and vendor’s price. so hard to be patient…

did the property sell to a higher offering person? No... not hard to wait then

FOOP

My wife and I once watched a programme about these old ladies who lived in a Japanese town. Every day they put on wet suits and went diving for sea food. Some were in their 80s and 90s. They were not rich. They had each other and all they did was laugh and smile. They had a rich life. And a very healthy one.

Okinawa maybe?

The common elements for a long and healthy life are

- fresh fruit and veges (which you farm yourself)

- not sweating the small stuff

- active social life

- getting up a lot (many Japanese live on the floor, and people in other long lived areas have to contend with stairs or hills).

I recommend watching Blue Zones on Netflix.

Yes I've seen that too. The ladies spend their time when they are not free-diving doing what you do, only watching docos about rich kiwis like yourselves.. its real TV. They see you laughing and smiling but dont realise its because you got a pension from age 60 or ride around in a tesla paid for by the younger gens who are paying off student loans

An example of many many (this is worst case) exploits, these are not house buyers, not even renter

https://www.stuff.co.nz/nz-news/350293195/misery-vines-tale-exploitation

https://www.oneroof.co.nz/news/buyer-pays-711-000-for-south-auckland-ho…

So desperate buyer paid $711,000. After 5 years the owner loses 25K, nominal not real terms, plus selling fees, plus rates/maintenance, etc. But you can't lose with houses, and property doubles every 10 years right?

Auckland still crashing.

The buyer was one of two bidders competing for the home, which had last changed hands in October 2020 for $736,000.

Depends on where you buy...South Auck? Good luck there.

I've bought some dirt in West Auckland, and the area I've bought into is selling out. The work going on there's huge. Do ya homework and buy when the herd say sell.

Here's a couple of examples.....Westgate's massive.

https://www.nzta.govt.nz/projects/sh16-brigham-creek-and-waimauku/

Interesting that Auckland is very similar to where Brisbane was in 2011-2015.

I bought my inner-city home in 2013, I made an offer two weeks after it was passed in at auction. The seller told me that he won't play in my "low balling game". Two months later, he accepted my offer and I could've low balling him again but I didn't.

Roll on 2024, Brisbane is now second most expensive city in Australia, by passing Melbourne. My house value is now more than twice what I paid for it!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.