Auction activity appears to be settling into its winter rhythm, with both the number of properties auctioned and the sales rate little changed over the last couple of weeks.

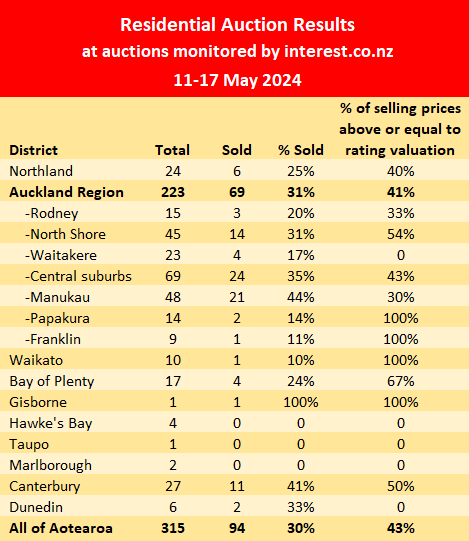

There were 315 residential properties around the country offered at the auctions monitored by interest.co.nz in the week of 11-17 May, compared to 296 the previous week.

That's well down from more than 500 a week over the peak summer selling season, with the decline suggesting auction activity is following the normal seasonal trend.

Of the 315 properties on offer at the latest auctions, 94 were sold under the hammer, giving an overall sales rate of 30%, down very slightly from 33% the previous week.

The overall sales rate has been between 29% and 33% for the last five weeks, suggesting activity settling into a new normal for the time of year.

Details of the individual properties offered at all of the auctions monitored by interest.co.nz, including the selling prices of those that sold, are available on our Residential Auction Results page.

The comment stream on this story is now closed.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

73 Comments

Into to the cave we go.

Going to be a long dark gold winter for the next 2 years.

It is the best thing that could happen for the property market and NZ.

Tradings house in a Ponzi scheme is not business we need to move onto more productive things and leave housings market to correct.

Spring will follow winter……

Just as the weather goes in cycles, so does the property market. 😇

Some, however, choose to ignore or forget the above. 🤥

TTP

You are right BUST is following BOOM

No one knows how big the bust will be, overhang means that its not over,

this is not a functional market yet, to many are hanging on to 2021 prices,

Capitulation will occur as more accept the market price and move on

Hint: its 10% lower then it currently is, lots of bids at these levels just ask REs

Spring will follow winter...

I will NOT follow IT GUY, Crazy Horse, NZ Gecko.....

Hehe

OK FHL Sun will follow Rain, Hog will follow Hedge, all the other useless wordisms be followed. Not.

Stay in your Echo, echo, ehco, echo chamber of "property being bid the moon" ....hahaha good luck with that group of REA nest egg eating ferrets.....

If people want to live in winter for 2 full years, it's their choice TTP. Meanwhile the more balanced people will enjoy each of the 4 beautiful seasons.

Well spoken, Yvil.

Much enjoy the enlightenment and inspiration that you bring! (There's precious little of it to be found here.)

TTP

Kum ba yah

Get the feeling that agents are getting a bit frustrated with vendors still being blinded by peak prices.. on the other hand it's their own undoing as they made vendors feel their houses were made of gold, in order to get the listing

Just a few months ago agents where pleading with vendors to have patience as after 3 months no offers they where moving agents..... another 3 month.... still no offers....

The results are better than I thought they would be.

Maybe 2024 house prices won't lift 5-10%. Maybe 0-5%? 2025? 5-10%?

Still sticking with my 4 to 5% prediction. Would like to add its going to be location specific so that's for Tauranga.

Well done, Harvey! That's the spirit. Chin up.

Nothing wrong with a level of optimism that many would consider is bordering on insanity.

The one thing I learned during Covid is there is no sanity in the housing market, its driven by emotional factors and if cheap credit suddenly becomes available.........Fact is the RBNZ could drop its pants at anytime if things get tight, its already been done and that was for no reason at all as it turned out.

Incoming DTI could easily be adjusted to save us from the greed of speculative stupidity witnessed over covid. See what happens....

I.agree. This week atleast is actually encouraging. I'm sticking to a flat 0% 2024. That could change with high winters stocks, and also dropping interest rates to counter.

And vastly reduced building of additional residences, that will show in the next year or three.

NZX had a strong rally in retirement villages this week, not enough to break the gloom but enough to signal there is still some interest in the residential market

Every dead cat bounces, when a spruiker kicks it.......

I watch the % equal to or above valuation which appears to be increasing?

40 out of 315

The percentage sold remains pretty static, percentage sold above valuation has increased slightly, I had thought that if prices were dropping substantially that this stat would move in the opposite direction.

Only the best selling, those that have had substantial work on them?

That's not always the case. increasingly I think the vendors listing by auction are those most motivated for a quick sale.

Have any stats experts here played with a distribution curve across the Auckland housing market and compared that with sales rates vs cv over time? Any interesting observations or too fuzzy?

If 31% are selling at auction and off that 41% are above cv, then only 12.7% of B&T auctions in Auckland are selling in-auction and above cv.

Of those that are passed in, what percentage also sell above vs below cv?

Difficult to get the real numbers these days. On all the homes websites they're all saying TBC for many months. Any suggestions for better information sources?

Yes, I find that frustrating that the homes site takes months to change TBC to a sold price. If you click on the property after it has been through their computer generated revalue, you get a pretty good idea of what it sold for as often the valuation becomes the sale price way before the sale price is added. (So that their valuation doesn't look so out of kilter I guess). The agent must have to supply a suggested sold price. Any agents out there that can verify this?

If it isn't updated straight away you can be pretty sure they didn't get a good price.

Tracking sale price against cv would only be worth tracking around the time of the value being struck or in a stable flat market. As soon as the market moves the cv is going to be too low or as now too high, then correct again in three years time. The shifts in market have been seismic in the last four years; shooting up, now retreating fast. Hard to decide prices currently. Just saw a registered valuation recently that used the previous 12 months local comparisons to set a price…. It was a rubbish document as sales were all old ( nothing in the high range selling currently) and set a price in the 21/22 range, no help to anyone.

Yep. Reference points should only be recent relevant market sales in the local. Reference again Council Valuation is a point for comparison after the fact.

I would also just like to add that viewing sales in my area, I note a couple of auctions were for houses that were basically land value as the houses were absolute dumps. (not livable) They would never attain CV in any state of the housing market.

Looking at %sold and % sold above or equal to rv is telling.Waikato is holding out and Manukau getting more realistic? Although with rating valuations being done at different times it is a bit hard to compare.For instance Whanganui was updated in 2022 and Coromandel is still on 2020 RVs

You can't draw conclusions for Waikato with 1 unique properly sold (over 10). Can only be 0 or 100%.

Better to focus on price paid IMHO as the sample size of houses selling at auction vs by negotiation is so small now.

April REINZ (ALL SALES DATA)

Auckland $1,050,000 (-1.9% on previous month)

Nationwide $790,000 (-1.2% on previous month)

Nationwide ex AKL $700,000 (-1.7% on previous month)

Data not opinion, shows the market is falling.

That is 1 month. Most of the country has risen in the three month range or one year range. Time will tell if the bad last month is a trajectory or just noise.

One could argue that 3-6 months ago bank economists were crowing about the end being in sight and how houses would rise 4-6% this year. Not so now, ay? Reality has set in. And even TA has realised he's been way too bullish.

BTW ... Where's that other perma-bull Ashley these days?

Yeah TA has tuned very "non bullish"...

Prices are still flat, next year we'll start see a major dacline in mortgage rates and guess what would happen?

Don't buy keep waiting, hahaha...

What have you bought recently? Be quick ...

Fingers crossed whenever the OCR goes down the RB introduce DTIs at a lower rate than currently proposed. Win win. Keep the shit fiesta that is our housing market on the same trajectory (aka down) and allow life back into our economy. If house prices are allowed to reignite again at some stage there will be a huge price to pay - how that reflectsi don’t think anyone knows.

But hey ho John, you keep doing God’s work mate spruiking the 💩 out of things.

He's right though. Prices are flat from a year ago, If not a tad higher.

Are you always this rude to people with differing opinions to you or is it just online?

I didn't find Amokk's comment rude. Direct? Yes. Rude? No.

Mr Mendel threw out a general comment directed at all people who believe the market will fall or flatline. Amokk responded to Mr Mendel directly - and with more substance than Mr Mendel's throwaway general comment that lacks substance and qualification. No foul. Carry on.

What would cause a major decline in mortgage rates....

Plunging confidence?

Collapsing demand?

Rising unemployment and job insecurity?

oh yeah all good reasons for housing to take off again...

a sudden drop in rates will slow the falls, it will take years for confidence to return as we will all be well aware of the global economic climate by then.

Well far out, a HUGE 87.3% in NZ NOT sold, at, or above the CV. What a booing market we have....NOT.

The Spruikers (TTP, TA, AC acolytes) are positively shisting bricks about now........ the only linchpin holding this market to a slow and steady decline is the seller still expecting to get near CV, then the colluding real estate agent drawing in the gullible, FHB suckers, getting lured in and completely stitched up by the silver tonged REA.....

Poor FHB connon fodder..... Their deposit becoming vapour and into the smelly four winds later over 2024/2025......

SOON however, the CVs are all about to officially plummet, pulling the loosened market linchpin, signaling to all, the next market shoe to drop and give the Ponzi pumpers yet another solid kick in their Gnuts:)

Capitulation stage to see some slalom style downslope, later 2024/2025.

Never seen a Council willingly drop Rating Valuations. Awk council is maxed out on debt. Any thoughts of them dropping their income should be in the very unexpected camp.

"Never seen a Council willingly drop Rating Valuations"

From memory council valuations declined during GFC in Queenstown.

Yes CV drops in the 1990s was common and in line with a general declining housing market prices, for a number of years.

I fully expect my Auck CV to drop -15 to -20% and my rates to rise in the range of 5 to 10%.

The Council is a hungry beast and with a good appetite for new cash.

Dropping or raising CV has no impact on rates overall.

Averageman

Stop showing your utter ignorance.

Councils have absolutely no influence in setting rateable values. These are set independently by QV who are an independent central government entity and rateable valuations are based on recorded sales by LINZ - “the land registry office” - another central government entity.

Auckland RVs are most likely to fall due to falls in recent house prices since rvs were last calculated.

You seem also under the impression that RVs determine total council rate take. Again an indication of your ignorance. Total rate take is determined by a budgeting process totally divorced from RVs. Once the total rate take is determined it is only then that RVs are used to apportion it amongst rate payers - whether RVs rise or fall is immaterial to council rate take.

Again, your ignorance; RVs can and have fallen as have been discussed on this site. Napier 2011 is one such example.

Average in AKL is 1,050,000. was it 1,295,000 at the top?

so its down 19%.... not impossible that the new AKL CVs are down about 15%

Plus a 20% loss in monetary value since 2020, due to inflation running rampant..... so a REAL 40%. This silent GFC is getting wild. Wait till it really gets-a-going.

Inflation doesn't factor in like that mate. Maybe you should look at new build prices.

REAL INFLATION ADJUSTED PRICES are the REAL price Zwiffy. Done.

However, if you must, free world and all that, grasp whatever soggy straws you may still have access to in, your underwater quiver bag....

"Maybe you should look at new build prices."

I am. They are falling to.

And some (perhaps many) are going for cost.

And build costs are going down too - albeit slowly (for much the same reasons that sellers aren't selling their houses for less even as stock levels mount. But eventually that stock must be turned into cash and it will be ... at lower margins ... and maybe even at, or below, cost).

Oh ... And I should point out that many builders are less than thrilled with government's policy to re-instate interest deductibility for existing houses as it ripped the floor out of the new build market.

Yes we knew that would happen.... been discussed on here a lot before the election, by HM and others...

Yup. It was. (My comment was just for those that pooh-poohed the idea.)

Had a good talk today to a senior architect at a big, prominent architecture practice. Residential work collapsed for them a few months ago, they effectively closed down their quite large residential team. Heard something similar last week from an architect at a mid-sized practice. This is leading intel.

"Inflation doesn't factor in like that mate"

Tell that to someone who is selling their residential property in Auckland or Wellington now and not buying.

Compared with the house valuation in Nov 2021, with the fall in house price and rise in the cost of living due to inflation, their net proceeds will pay for a reduced number of years of living costs. This is for a mortgage free seller.

It is worse for a highly leveraged seller as their equity has shrunk significantly more percentage wise. They may even be in negative equity, so they have lost all of their equity deposit and still owe money to their lender.

Here is one example:

Oct 2021: paid $1,760,000

April 2024: sold for $1,285,000 (before sale costs of say 3% - net proceeds of $1,246,000)

That is -29.2%.

Much less purchasing power for the October 2021 buyer due to fall in house price, even before the effects of inflation since 2021.

https://homes.co.nz/address/lower-hutt/eastbourne/23-marine-parade/0kYwN

Factor in inflation of 12.9% for living costs since 4Q2021, results in a decline in purchasing power of 37.2%.

https://www.rbnz.govt.nz/monetary-policy/about-monetary-policy/inflatio…

Note: the above is for an unleveraged buyer.

Yes the REAL loss is almost 40%. Glad to see some solid, free education being given to those, who still don't understand the killer of monetary value that high inflation brings.

Thanks for simplifying it down, for the youngins, CN:)

Still the current situation has me seeing the 2024 Wgtn buyer still overpaid by 400K, based on the current relevant factors at play and still to workout in this high persistent inflation and higher longer interest rate world.

Hi NZ Gecko! Remember, inflation also, in real terms reduces debt.

Are you and CN and ITguy the same person?

The salient question is........how does that big DEBT FEEL AT 7%???

All the while, the asset you endebted yourself big for, goes South, at a rate of knots.

"HOUSE IS BEST INFLATION HEDGE MOB" now back in their cave.

Use any straw you have left to clutch, along with your pearls, the world changed a 180Deg in 2021, the borrow big, buy any house, win, model snapped into small irreparable pieces.

See your a bag holder and missed the 2021 memo???. that some saw clearly.....

You still have time.....but still seem to live deeply invested n Ashley's Church??

“inflation reduces debt in real terms”

It can also reduce your ability to repay debt due to other living costs rising if your income doesn’t rise to match. Other factors like inflation pushing the costs of servicing debt higher (higher interest rates) can make that debt more expensive to “own”. And gearing works both ways too. I think your grasping at a perceived positive that’s not very positive at all, in order to shine a rather smelly turd.

Remember, inflation also, in real terms reduces debt.

That is a commonly frequently repeated phrase used by property promoters and frequently repeated by their students.

Have you ever done the calculations?

Just to highlight the impact if the buyer used an 80% LVR mortgage on an nominal and inflation adjusted basis for the example elsewhere in this thread

Nominal prices:

A) October 2021

Purchase price: $1,760,000

80% LVR mortgage: $1,408,000

Equity deposit: $352,000

B) April 2024

Sale price: $1,285,000

Sale costs (3% of sale price): $38,550

Net proceeds: $1,246,450

Less mortgage: $1,408,000 (assumed to be interest only for simplicity)

Equity: NEGATIVE $161,550 (they are in negative equity) - loss of 146% of original equity deposit)

They would still owe money to their lender after the sales proceeds are paid to their lender. And this is before the 12.9% rise in living costs due to inflation since 4Q 2021.

Inflation adjusted prices

B) April 2024

Inflation adjusted sale price: $1,138,175 ($1,285,000 adj for 12.9% inflation)

Net proceeds after 3% sales costs: $1,105,030

Less mortgage: $1,247,121 ($1,408,000 adj for 12.9% inflation)

Inflation adjusted equity: NEGATIVE $143,091 (negative equity, a loss of 140.7%)

So inflation has resulted in a loss of 140.7% of equity.

I think that the October 2021 buyers would have preferred to rent and a 0% nominal loss of their initial equity deposit.

Buying on the premise that inflation erodes debt has blindsided buyers to potential losses, and potential negative equity situations.

Spruikers do not like real examples of eye watering losses...... that one looks a classic divorce

That one is a doozey

That's like 15k a month for 30 odd months, that's 500k of dead money , would have been way better off to have gone renting.

Who would have thought owning was dead money

"Spruikers do not like real examples of eye watering losses"

Meanwhile who got paid on the initial October 2021 transaction?

1) real estate agent got their commission and moved onto the next transaction

2) if the buyer used a mortgage broker - mortgage broker got their commission paid by the lender and moved onto the next transaction

Owner occupier buyers, CAVEAT EMPTOR

Just to highlight the impact if the buyer used an 80% LVR mortgage

A) October 2021

Purchase price: $1,760,000

80% LVR mortgage: $1,408,000

Equity deposit: $352,000

B) April 2024

Sale price: $1,285,000

Sale costs (3% of sale price): $38,550

Net proceeds: $1,246,450

Less mortgage: $1,408,000 (assumed to be interest only for simplicity)

Equity: NEGATIVE $161,550 (they are in negative equity) - loss of 146% of original equity deposit)

They would still owe money to their lender after the sales proceeds are paid to their lender. And this is before the 12.9% rise in living costs due to inflation since 4Q 2021.

Reminder of what some commenters were saying on interest.co.nz.

Names omitted intentionally (but 2 of these commenters are active on this very article)

a) 9th Nov 21, 2:38pm

"I have always looked at this from the opposing direction - the risk in not owning a property? If you do not own a property you are short, not even square, but short"

b) 9th Nov 21, 5:52pm

"Or maybe right the opposite, don't hesitate, be brave and go for it, you'll be fine"

c) 23rd Nov 21, 8:52am

"It makes absolutely no sense for a couple like this to bank a capital gain now rather than wait two years and avoid 90k in taxes. The market is not going to crash 10% in the next two years."

d) 9th Nov 21, 2:38pm

"locally, I can not see anything in the near future that would decrease these current values."

e) 14th Oct 21, 11:25am

Shrewd investors will capitalise on perceived price weakness - cementing their position for the next market upswing.

Well located property remains a prime investment for the long term. (But you already know that.)

The financial impact and consequences of following the above advice:

1) for a cash / unleveraged buyer, lose 29% of their equity

2) for an 80% LVR mortgage buyer, lose 146% of their equity deposit, and be in a negative equity situation.

Their future financial trajectory is forever changed, their quality of life at retirement is now so different. What does having insufficient funds at retirement look like? - https://www.newshub.co.nz/home/money/2023/04/cost-of-living-pensioners-…

There will be potentially thousands of households in NZ who bought in the 2020 - 2022 period facing this situation. The highly leveraged owner occupier households will be facing cashflow stress and mental stress. Unfortunately some will resort to self harm.

Yep but, but, but new build prices!!.....smices. Yadayaya.....

They will drop like a rock, much further into liquidationesk value.....or just not sell and bankrupt the developer, his choice.

The volume mounted around me, like pile of smelly doggie dooo.....no interest at all and not selling. The financial pincers on the owners is withering.

People that mention "new build prices" as a reason, why currently, somewhat recently depressed prices, will hold the line.....are just gumby and have no knowledge on financial history, that continually repeats over decades and hundreds of years.

Often and in every market crash, as we have now in its infancy, the sale price can and does indeed go well below production costs. It will for housing to and for a protracted time, given the deglobalisation and ongoing wars.

I wonder what the build price would be if the OCR had remained at 8.25% from 2008 to 2024?

I’d expect it to trend down over the remainder of this year also. Without a source of fresh credit, the tide will continue to go out.

Tauranga definitely going backwards. 3 houses close to me for sale that were purchased during the covid period. All 3 houses valued over $1M. These 3 houses are now for sale for LESS than the purchase price. There's plenty of other examples of units and townhouses for sale, but interesting to see quality homes going backwards.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.