House prices appear to be on a serious slide as we head into winter, according to the latest figures from the Real Estate Institute of New Zealand (REINZ).

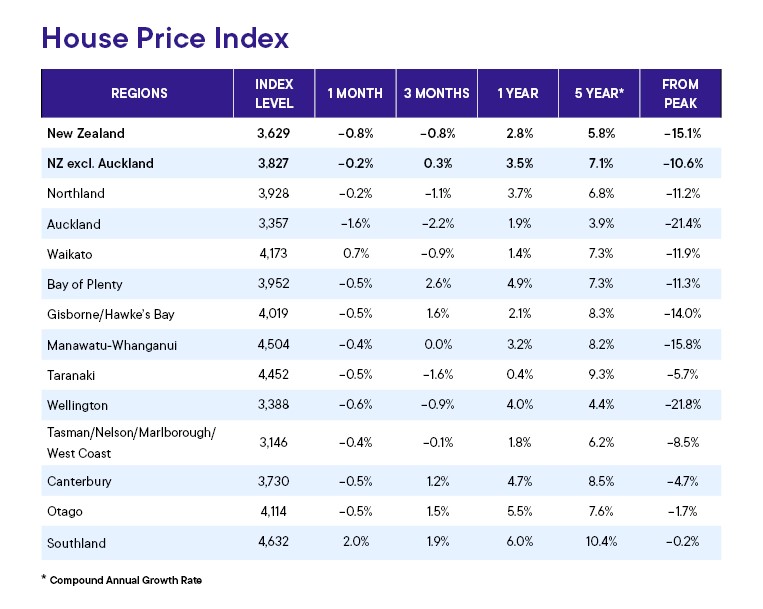

The REINZ House Price Index (HPI), probably the most reliable indicator of housing price movements because it accounts for changes in the mix of properties sold each month, declined by 0.8% in April compared to March.

The Index declined in 10 of the of the country's 12 regions last month, with the monthly declines ranging from -0.2% in Northland to -1.6% in the Auckland Region.

Only two regions posted increases in the HPI last month, - Waikato +0.7% and Southland +2.0%.

However the decline in prices may be more serious than those figures suggest, because a slight majority of regions have also posted drops in their HPI over the three months to April.

Six regions - Northland, Auckland, Waikato, Taranaki, Wellington and West Coast/Tasman/Nelson/Marlborough - posted declines in their HPI over the three months to April. Five others - Bay of Plenty, Gisborne/Hawke's Bay, Canterbury, Otago and Southland - posted increases, while the HPI was unchanged in Manawatu/Whanganui. See the table below for the full figures.

That suggests the decline in prices is picking up pace heading into winter.

The REINZ's national median selling price was $790,000 in April, down 1.2% compared to March.

Auckland's median price was $1,050,000 in April, down 1.9% compared to March.

The comment stream on this story is now closed.

Median price - REINZ

Select chart tabs

Volumes sold - REINZ

Select chart tabs

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

144 Comments

Auckland down 21.4% from peak (1.9% this month) and price declines gaining momentum

Those QV figures are so distorted by old data, I am not sure why they bother.

Being down 21% before the job cuts and redundancies bodes real bad.

Adjusted for inflation?

I wonder if the media will finally say the market is crashing?

re: HPI being inflation adjusted, we had some discussion about this years ago. I think we eventually settled on "no".

The market is crashing? No

The national median price will most likely remain in the region of $750-800,000. Median price in Auckland will probably drop because they are overpriced.

Look at the graph, and you will see that the "crash", if you want to call it that, ended many months ago.

That's just the end of the beginning. I'm still picking a market bottom in 2027.

Given the very large increase in house prices in the decade ended November 2021, the housing market is doing okay. (There are plenty of examples of properties that tripled in value through this period.)

Once rental return is factored in (as it needs to be in any credible financial analysis) housing has been a high-performing investment for the vast majority of house owners.

And, of course, there are the non-financial benefits of house ownership, including security, avoiding landlords and being able to do as you wish with the property. For some people, social status is also significant.

That we don’t have people coming to this blog cursing about their house purchases is convincing enough. (Most of the despair here comes from people who don’t own a house - and/or have inherently negative/ pessimistic mindsets.)

Cyclical peaks and troughs go with the territory but, in the longer term, property remains a pretty safe, hard-to-beat investment for many New Zealanders.

TTP

"but, in the longer term, property remains a pretty safe, hard-to-beat investment for many New Zealanders."

Past performance is no guarantee of future performance.

And local governments, supported (driven?) by central government, are loosening the planning shackles that have been in place since the 80s.

Sorry, TTP. I'm going to call b.s. on that advice until 30 years hence!

Also, councils really need to start charging more appropriate rates to actually pay for the infrastructure and utilities that the landholders benefit handsomely from. This government has put the burden of the water infrastructure back onto the councils, I personally think it's the best thing they've done. Time to pay the piper.

It's already happening, in Hamilton they are proposing +19.5% in 2024 then 15.5% the four following years. Compounded that's more than a 100% increase in 5 years.

No guesses as to what is going to happen with rents...

Tha'ts the spirit. Drive more young working renters overseas.

Renters are already fully squeezed. The adjustment needs to be in the price of housing. The rental yields can get much more attractive at lower price levels.

it can move in both directions to find equilibrium. House prices come down AND rents go up. I am predicting more of the latter in the next four years. Rents in NZ are actually pretty low compared with.most countries we tend to compare ourselves to.

I believe you are correct on this one!

"rents go up"

Potential unintended consequences if rents rise faster than household incomes:

1) more households requiring accommodation supplements,

2) potentially higher accommodation supplements per household

3) more households on social housing waitlists

4) more social housing required by Kainga Ora.

5) due to increased government spending on the above, there will be less money to be spent on other government spending (infrastructure, health services, education, police services, etc)

These are some of the consequences of unaffordable housing.

Or renters say no to proposed increases en masse

Landlords meeting the market are as likely as vendors meeting the market currently. The level of reluctance and delusion is unreal. We'd see many overcrowded houses form mass evictions and many empty houses for a reasonable period before there would be any change en masse sadly.

Nothing. The market sets the rents. This will come out of yields, pushing house prices down as it'll be less worthwhile borrowing the money for buying rentals.

As a landlord I put my rents up higher than I normally do at the last review. Solely because of the rising costs and rates. The tenant didn't batter an eyelid.

With immigration soaring, we would be foolish to think rents are currently at a ceiling

Baptist, you're free to think, say and claim all sorts of things on here however, try to caution yourself over the "immigration is soaring" bit, when in actual fact, whether it be by Government intervention or word of mouth regards growing scarcity of jobs, latest figures re-confirm net migration has begun tracking down.

To some, much like the (much trusted) latest HPI release, it's just merely more bubble deflation stuff that needs to happen.

Do you really believe those new types of immigrants have the earning capacity to pay the average rent in New Zealand? You need at least 3 of them in the same rental before it will work.

Currently the average rent in nz is about 39% the average wage. In India and China, where the bulk of our immigrants are coming from, the ratio is 50 -70%. Of course there is regional variation. As a landlord for 15 years it has never been easier for me to increase my rent without fear of losing a good tenant or finding a good replacement.

For now…

Time to pay the piper

Just wait for the many retirees who can't afford the rate hikes due to no longer working, but demanding low rate hikes for the majority of their working lives. Govt benefits will increase in this space if not kept a close eye on via MSD, and pensions are already our largest benefit payout.

TTP suffers from hindsight bias so completely he is prone to living in a fantasy world.

Those with an ounce of social conscience might well say "Given the unsustainable increases in house prices over the decade to Nov-21 and despite falls to date, the market remains considerably overvalued and prices will continue falling until more sustainable fundamentals are reached"

Anyway, if you cannot reconcile with what's happening right now why not reminisce - eh Tothepoint?

"For some people, social status is also significant." This is something that only/mostly exist only in the Anglosphere. Like renters are a second class people...

Agree, SND.

I’m referring, of course, to the blue-rinse set in Remuera - and all the people who are into “conspicuous consumption” in suburbs like Parnell, Omaha, Mission Bay, Ponsonby etc etc, including some well-healed real estate agents.

Like it or not, there are plenty of people obsessed with social status - and I count myself fortunate to have avoided swelling their ranks. 🍀

TTP

Not sure I agree with you there Tron. The graph shows that prices have fallen back to 2021 levels. If you cast you mind back to 2021 interest rates were 3-3.5% they now sit at 6-6.5%. Given that it costs 2 x as much to service any debt I can only see prices continuing to fall.

Wages are higher than they were in 2021. As are rents.

How fitting, peoples wages increase so rents to as well, thus deleting the increase in wages for many and passing this to the landlord. What motivation there must be to work hard and achieve. Gives more of an impression of milking as much from renters as possible. While I appreciate there are yeilds to consider and increases in rates and insurance, but why then for landlords who have no mortgage on their IP's are they hiking rents when they are already creaming it. Answer: because they have the power to do so.

As a landlord with no mortgage, I can say I have not increased the rent in at least 7 years, while expenses such as rates and insurance have gone up.

While my example is not proof that landlords in general are thinking of there tenants, neither is selecting examples of the opposite proof that landlords are inherently creaming it either.

Unfortunately we are given very little information about the costs of the person has, whether it be fruit and vegetables or rent. So we see it from our perspective which is clearly biased towards us.

"The market is crashing? No"

I thought the consensus on what constituted a crash was a 20% or more decline from peak. I don't recall of this was fall in real terms or nominal prices but it's irrelevant as the fall has been in nominal prices.

Auckland prices are still falling so it is still in the process of crashing. Noting that where Auckland goes the rest follow.

So why do you say the Auckland market is not crashing?

"I thought the consensus on what constituted a crash was a 20% or more decline from peak. I don't recall of this was fall in real terms or nominal prices but it's irrelevant as the fall has been in nominal prices. "

FYI,

1) the REINZ house price index for Auckland and Wellington have met that quantitative criteria.

2) the REINZ house price index for other geographical areas have not met that quantitative criteria

Different people may be referring to different geographical markets which is causing misunderstanding.

It only takes a 21.4% price drop to wipe out 27.24% of the previous price gains.

It also means anyone who bought with a 20% deposit near the peak is now in negative equity. Their gamble now is get out while the debt can still be repaid or hold on possibly for many years for a recovery.

And don't forget the 5% loss on selling due to RE marketing and commissions, Lawyers, and moving costs.

Don't think it matters too much... a number of people were saying they don't mind seeing their own property prices crash 50% so still ways to go for a good opportunity to pay cents on the dollar for the properties bought by the millenials/Zers.. lol the future gens are so fked in this country... they should leave NZ as soon as they are able as the name of the game here seems to be to become the biggest vulture sucking on the government's teat and screw the future generation :P

Minor correction. Auckland is down 1.6% this month but up 1.9% for the last 12 months.

Reposted

I prefer it described as "..a great winter for the housing market.."

Prices falling is not a bad thing.

The house price explosion of recent years has been New Zealand's greatest social disaster.

Recent years?

Yeah, was thinking the same thing, more like "recent decades, tfify"

Nobody talking now about the loss of capital gains in retirement villages.

But people bought Ryman shares to participate in the gains …. Wait a minute

Dead cat bounce well and truly over.....

There's now significantly more stock on the market (Akl at least) than at any point in the last seven years. (~15,300 now vs ~14,300 in March 2019). This time in 2021, just before things went stupid, there were only ~8700 and fell to ~6800 at peak stupid (Sept '21). Usually the stock level starts to fall quite quickly in April post-peak, but seems like it's holding flat this year.

There is a lot sitting on the sidelines too.

Enter July.

Yep. The tsunami of latent tax avoider's to hit in July. No OCR change coming up, prices dropping causing banks to drop valuations and leverage math. What is going to get better....?

If one has already lost money, meaning no CGT applies, then why wait until July?

5 properties being listed for sale by a time constrained property investor.

https://www.oneroof.co.nz/news/landlord-calls-it-quits-900-000-onehunga…

Great marketing from him, Its a plaster home so no surprises there, medium term its potentially only land value. Probably still will get in the $800's so he will not care.

I hate OneWoof.

I have to re-search with the address to find the listing on another site because I can't see enough detail in their damn images! Especially floorplans.

I.e. right click on the image, open in another tab, and zoom to my hearts content. (Using Chrome.)

And yes, I have told them about this massive fail multiple times over the last few years.

2 issues (possibly more)

Firstly, it's on a cross lease, and, secondly, it's plaster. The agent says that it has eaves and therefore "it's not leaky". However, the issue with leaky homes is the absence of a cavity and not the presence/absence of eaves.

Yup. Paying Council to get the property file can be the best insurance ever!

For those that don't know, Council's property files have copies of the building consented plans (and reports, e.g. geotechnical) and any amendments made up to the issue of the CCC. If you don't understand what you're looking at, take them to someone who does.

Someone used to post the link to a chart showing how nz property was tracking vs Ireland crash etc indexed etc ?

They all went quiet after prices went up 6% instead of down another 15% as was predicted.

Watch as banks trim margins and the v recent mortgage rate cuts accelerate to support valuations esp when 5% deposit mortgages have been out and about from a few banks lately.

OCR to plummet again once stats NZ days catches up with reality

You are clearly on another planet.

Watch the calamity once people start getting mailed their new CVs in Auckland.

I do not envy the council call centre staff on that day

What sort of a calamity are you expecting when the Auckland CVs are mailed out? CVS will be about the same as June 2021, or maybe down by about 5%. What sort of change in behavior is that going to induce?

Simon is right that the OCR will soon begin dropping, followed by retail rates. 2022-23 were the bad years. 2024 will be flat. 2026 we will begin seeing steady climbs again.

Bit of a yawn isn't it ? Just watch the OCR take a dive at the first sign of real trouble.

You don't understand how inflation works.

There's a number of things Zwifter doesn't understand. As this downturn evolves that list only grows with each comment made.

August to October WAS NOT the last opportunity to buy. Denial of what's happening today is weighted with as much foolishness as Nov-21 being the right time to buy! The vested have such limited understanding of what's really happening out there.

Do you understand how LVRs and DTIs work? Do you know what up-zoning is?

One of the biggest drivers of non-oil shock 'inflation' is the cost of housing which drives wage increase pressure. (Housing costs accounts for between 40% and 60% of take home pay! By far the biggest cost for working people and young families in NZ.)

Control the cost of housing and inflation is much easier to contain. (Hello? RBNZ? Central & local government? You listening?)

What inflation? We are now at 2% annualized

Baptist, measure for measure that must mean house prices are falling at a rate of 10-15% annualized and TD's at 6.3% before tax exceed the prevailing inflation rate?

Better than a rental by a city mile you reckon?

The last time that happened was 2008 in GFC

The RBNZ slashed the OCR from 8.25 in July 2008 to 2.5 in June 2009

https://tradingeconomics.com/new-zealand/interest-rate

House prices didn't bounce - they remained stagnant for almost 5 years as an NZ index, and in most regions, there was a decade of no house price growth

I suggest it was the global banking failures at that time that triggered the stupid drops in debt.

I’d like to think we learnt something over the last 20 years that suggests slashing interests rates is not the best outcome. Source, lower them a little, but slash?

Slow and steady wins the race

Correct. Same thing happened in the US - the US housing market took a nosedive in 2006 after several months of the Fed's hiking cycle. By Sep 2007, the Fed began reversing its position and slashing rates, effectively bringing it to 0% by the end of 2008 and kept it there for a very long time.

Yet the median house price in the US only returned to its 2006-high exactly 14 years later when the Fed and Biden injected trillions into the economy during the pandemic.

I am sorry but the most of those trillions were injected by Trump and the Fed. May I also point out that Biden was installed in 2021.

You clearly don't understand that this housing 'correction' is going to take 5 - 10 years to sort itself out.

His username was Miguel-something, appreciate his effort

He did stop posting those when the "green shoots" were "sprouting" before the election

It'd be cool to see that revived, including the plateau of the past year or so

Many DGMs have stopped posting, but at least a dozen still remain.

"Double grammar munters"?

Here you go https://i.imgur.com/RPlCniI.png

{kind=link}

Hard to make predictions, but this Winter looks like it could touch the trough from last Winter. A USA style decline with seasonal ups and downs over a few years is a possibility. It's not looking like an Ireland style crash now.

Thanks. Useful and sobering.

But I'd argue this cycle is quite different to the GFC inspired cycle, i.e. this fall will be shorter lived.

History will decide whether I'm right - or wrong. (I expect the morons at the RBNZ will come to their senses earlier than the bank economists are telling us.)

HAHA 😄 classic.

Thanks for that.

18 months of nz prices flat and edging up 6% or so compared with ireland continued constant fall.

We aren't day traders trading shares no dead cat bounce just a solid bottom formed where FHBs can with inflated salaries and kiwisaver buy and it make a lot of sense.

I bought my first 5 earning a little over current min wage - that was less than 6-10 years ago with minor rent roll helping but mainly job salaries 57k ish. Anyone with a real job not just min wage will be 120k plus in late 20s with fat kiwisaver.

The bottom has been formed. Investors back at first sniff of rate cuts where yields can be created (not bought as is) of net 7% plus for an easy set and forget free house

That’s how I see it too.

Love the graph.

Onwards and upwards NZ housing. No crash to be seen. The worst is in fact over.

Good for you mate, at least you’re smiling as we resume the downtrend and near the cliff….

Thats the fighting spirit!

I always find this is helpful when I'm becoming bewildered by some of our MSM articles:

5 Years of The Irish Times Headlines Related to House Prices

Given the lagging effect of HFL, it was an obvious conclusion we hadn't even had the worst of the current downturn. A resumption of a declining HPI from April 2024 seemed done and dusted to me.

Dead Cat Bounce is well and truly history.

Damn it's cold today.

But not as cold as the property market.

This is all before the job calamity train which is steaming full speed ahead at the car (property market) stuck on the tracks.

Where I live only the entry level houses are selling. The sea front properties and the odd exceptional home always sell. People are still holding out for 2021 prices. It’s amazing how stupid, or greedy or just uninformed some people are. Some have been on the market for over two years. I would not encourage anyone to buy now. The next six months of the year are going to be tough for vendors and fantastic for buyers.

"I would not encourage anyone to buy now", "The next 6 months are going to be fantastic for buyers". You're not making much sense there.

Over the next six months prices will continue to drop as more houses come on the market. Some vendors will have to drop their pants to sell and that will hit values of similar houses in their locality. When spring arrives this year and the usual large number of new and old listings hit the market it will be particularly tough for vendors.

Indeed. All they will have managed is avoiding paying tax on their spec gain. Why are young trained doctors fleeing to Aussie again...oh yeah the tax collected there pays much better wages.

Save the housing market, bring back Labour!

It's turning out to be a bad morning for the Jaffa's

https://newsroom.co.nz/2024/05/13/aucklands-gravity-defying-debt-swallo…

NZ Stats are a mess, only showing general trends, but not any even moderate analysis to give any real insight.

How much of that median fall is due to a greater share of the market in the cities being smaller apartments?

Can we not split out the housing type to see the difference?

That's what the HPI is for.

Winter is coming and the certainty of housing marking will be the same as snow, falling from sky high!

All of the international crashes took 6x years to bottom (except Japan which, was 20x years to bottom)

So this rapidly the failing knife in NZ, will hit the floorboards or the Spruikers feet in 2027/28. Maybe later....

This epic crash in NZ is now at REAL terms off -40 to -50% values and still to be seen plumbing downwards and may see support at maybe another -20 to -30% down, in 4 years.

The biggest crash in NZ history is before our eyes.......and the great story of Tulips being repeated.

We have learned nothing from history.

So with houses now 40% + cheaper, are they affordable?

What crash, NZ house prices are up 2.8% year on year??

I mean, I know it feels weak but you really are talking nonsense.

Yeah, the bigger picture is not as bad as people make it out to be:

National $790,000 up 1.3% (where did you get +2.8% from ?)

NZ excl Akl $700,000 0.0%

Auckland $1,050,000 up 6.1%

But the latest trend is down and most likely will keep going down.

THe HPI grid, NZ 1 year is +2.8%. What am I missing?

You're not missing anything, I was talking about prices, you quoted the HPI, which, for the year are:

NZ + 2.8%

NZ excl Auckland +3.5%

Auckland +1.9%

So, yes the bigger picture doesn't look as terrible as the article claims.

That's because you're not looking at the bigger picture (as you claim). You're ignoring:

1. Inflation rate during that period

2. Mortgage rates during that period

3. Homeownership costs during that period

4. Latest house price trend (down)

Actually you even mentioned where the prices are trending:

by Yvil | 14th May 24, 11:28am

But the latest trend is down and most likely will keep going down.

Obviously it's helpful to define what we mean by 'crash'. For me, it's simple. A greater than 20% decline from peak in real terms. For the market I am most familiar with (Wellington), there has been a crash. Whether or not it is continuing is up for debate. Personally, I see many more reasons to think it will rather than won't continue. I would say the same for prices nationally. For me to conclude that the crash is over will take more than a single YOY increase in nominal prices. Zoom in too far and you miss the forest for the trees.

Sale prices finally dropping was to be expected:

National $790,000 -1.2%

NZ excl Akl $700,000 -1.7%

Auckland $1,050,000 -1.9%

It's the result of some vendors not selling at the asking price in the busiest month of the year being March, and having to drop their prices. With stock rising and unemployment business failures about to get worse, I expect prices to keep falling for the rest of the year. A lowering of the OCR in August won't save the RE market.

I think we have a better chance of seeing a pig fly than the OCR falling in August.

Banks will continue to trim their rates and the numbers for FHBs (v renting) and investors will start to stack up again and activity will lift. Plenty of people in good positions sat on the sidelines waiting.. collateral damage on the fringes was always going to happen given the fuel on the fire of Covid policies. Nice to see a more normal market where purchasers have choice and there isn’t such crazy fomo b’sh!t

I absolutely agree. I can’t understand why some people are hanging onto the belief that reserve bank can drop the official cash rate. We are tied inexplicably to the federal reserve. If we drop rates too soon or too low capital will leave our economy fast, push down the $NZ and drive inflation back up. The opposite of what they are trying to do. Short term thinking

If one looks at Auckland's 'flatline' between 2016 and RBNZ inspired covid-madness, the flatline price was about $850k.

So using the RBNZ's inflation calculator (here), the inflation adjusted 'flatline' price today would be $1.036m. I.e. $850k in Q3 2019 is worth $1.036m now.

So ... One could argue that Auckland is back to 'normal' values? Perhaps a bit above.

But maybe not ...

When Auckland flatlined - we still had inflation, but much less. Q1 2016 to Q3 2019 should have seen a rise from $850 to $900k. Did it?

Normal market behavior is to overshoot tops and bottoms. Thus I have every expectation that this time will be no different and, with higher interest rates, increasing unemployment, high stock levels, boomers cashing in past gains, and the fact we're in a Recession ...

Ain't nowhere to go but further down until the RBNZ comes riding to the rescue with some economic common sense.

FHB buyers should not be put off from buying though.

Be patient, negotiate hard, sniff out the bargains (the D's) and, whatever you do, don't max out your borrowing levels (e.g. keep the mortgage to 20 years, or better still, even less!). Why don't max out? Simply because the massive capital gains past generations got won't come again for another 30+ years. (See my posts on higher density changes.)

So basically Auckland houses have matched inflation since 2016 (albeit with a roller coaster ride in between)? Which is great, but even in 2016 they were unaffordable.

The wise FHBs aren't buying the average, or median.

Wise FHBs are buying at the bottom end so they :

- don't line a landlord's pocket,

- while paying just a tad more than they were paying in rents,

- while they are still used to having flat mates,

- while building up equity because they've kept mortgage term short!

The cool chill of reality is starting to bite. Oh the humanity for the Debt Grubbing Middlemen, you are just the risk proxy for endless bank profit. As you are about to find out...

@Greg can you please post both Index's that split the Auckland and Wellington areas into the relevant sub areas, i.e. North Shore, Papakura, Rodney and then Wellington - Upper Hutt, Lower Hutt etc?

It's available on the REINZ web site here:

https://www.reinz.co.nz/libraryviewer?ResourceID=666

(Click the download button).

As with equities, an all-in "buy trigger" is when price declines have wiped out 5 years of price gains.

In real terms, we're not far off that. Further nominal declines will be brutal though.

New Zealand has 44,000 small businesses that employ between 6 and 19 employees.

Accounting for 441,000 jobs. These are real businesses (small but real) and real jobs. The business lending for this sector is secured against property. Usually the owners home and any other property they may have.

The EMA is receiving increasing enquiries about restructuring. Our economy is being protected by our convoluted employment law. Look out to sea. That small ripple off in the distance that is moving towards shore will eventually break as a huge wave and wash a lot of people away.

It will happen in the time it takes an RBNZ bureaucrat to put down their Dom Post and pickup their morning coffee.

Taking a break from the property spruiker vs doomer war, I have a "practical" question to ask of the brains trust on this website.

We are currently smashing out our mortgage as quickly as we can, sitting at about $350k of borrowing on a $750k value property we purchased in 2021. At current rates (of both interest and payments) we will be paid off in 5-6 years.

However, the smashing-out of the mortgage means we are investing less into the likes of funds/Kiwisaver, and also cash, than we otherwise could (still doing some of each).

Would the potential of a stagnant, perhaps longer term declining property market change your approach here? Obviously the saved interest is a quantifiable return, but hard to know if we should "balance" our strategy a bit more.

NB we have no interest in buying investment property - any equity might be used down the track to get us into a bigger family home and we then sell the existing one.

I prefer (once I have employers kiwisaver contribution) to put the rest in funds that I can withdraw from if needed, see fisher and milford etc....

maybe a bit of gold and btc... but I totally agree just having savings in house could be painful going forward

You should be happy you don't have a significant investment in retirement shares in NZ, or Fletcher's. Both have tanked as the ponzi turns south because they are both in essence property speculative gain driven. Then look at the likes of the tech market in the US. All carrying crazy PE ratios that don't make sense unless there is a greater fool.

Summary - I would keep smashing the mortgage, renew a component onto a floating overdraft that you can access at will. Learn more about what drives value in stocks and see what the future brings. Good luck.

Along a similar vein to other commenters, I'd recommend holding an emergency fund in cash, maximising the employer contributions to Kiwisaver (3%) then using every other available dollar to reduce that debt.

There seems to be a consensus that interest rates will drop sharply at some point, when the sh*t hits the fan in the economy. Whilst I can understand that opinion, given recent history, there is a good argument that the cost of capital will only increase over the next decade.

The last of the baby boomers are all retiring over the next 6 years, shifting out of capital markets and into less volatile investments (cash, treasuries, bonds). The next cashed up generation (X-ers) are only a fraction of the size, and the millennials are still in the growth and spending phase, yet to accumulate enough to invest in the capital markets. Superannuation funds - a huge contributor to the pool of funds available for borrowing - will be shifting (if they haven't already) from net collection into net dispersal, requiring a higher percentage of their holdings to have predictable, stable returns.

All of which could mean that debt servicing cost is only going to get higher.

"I'd recommend holding an emergency fund in cash"

Sorry. I vehemently disagree.

Better to get a revolving credit facility in place to use in an "emergency" and smash the mortgage with any and all spare cash.

dumbthoughts,

Your question is a good one. And everyone with a mortgage faces the same question at some stage.

What it comes down too is whether the repayments you make each period would earn more as investments. A mortgage repayment carries a guaranteed rate of return. Investments do not. (Investment in training/education to get higher income can be guaranteed in many instances. And investment in the education required to answer your own question - mainly your own time - will be handsomely rewarded given libraries are free. I never use the internet for answers to such questions. Ever!)

The maths for mortgage repayments vs investments is complex as additional principle repayments made now avoid compounded interest in all future periods. I.e. it matters more making those principle repayments in the first 5 years than it does in the last 5 years. Further, quantifying the risk/reward parameters of an investment isn't easy either.

Buffet made a suggestion along the lines that really great investments turn up every 5(?) years and when they do, you'll immediately know it as you've gain sufficient knowledge to understand the investment well. My experience is similar. I've many years in ICT so when Xero floated at $1 and hovered below that I slurped up below issue price. I sold at about $40 a share when they entered the NZ50 and they couldn't be had for sensible money (index funds had to buy). I had the knowledge, the cash and patience. All three are an investors best friends.

Good points on investment.

But the main problem with using a revolving credit facility as an emergency fund, is that the emergency itself may break the facility agreement. E.g. your income reduces to zero suddenly, the bank may reduce, or completely remove, access to the line of credit.

Every revolving credit/flexible home loan/HELOC agreement will have a clause in it regarding your financial position changing for the worse.

I'd class a sudden, unplanned loss of income a disaster!

But yes, using a RCF does run the risk of the bank removing it suddenly. That said, that's never happened to me or anyone I know. Even a year without income when I took a break to do some more university courses didn't seem to bother them. I guess my asset mix guaranteeing the RCF gave them some comfort? I have no idea. They never asked.

Same but I think its about equity position....

I'm reasonably risk averse, and see a mortgage as a liability. Smashing ours as quickly as the wife will allow me, roughly $500k remaining and repayments are at 15 years. But she has different ideas and wants a new kitchen, so there's $1k per month being put towards that.

Guess it depends on what has the greater compounding factor? A dollar off the mortgage today or a dollar into the investments? Include inflation into the calculation.

The thought just occurred to me that buying the kitchen now instead of smashing the mortgage could be argued to be a buy now AND pay later scenario, by means of longer time to pay of the mortgage and hence higher total interest paid that, possibly, could total the cost of the new kitchen which would be in effect paying twice. Rabbit hole territory in this line of thinking XD

Rather than commenting individually, I'll just say thanks to everybody below for their excellent feedback and advice.

I think we are likely to continue on the current course, but potentially 'moderate' somewhat once the mortgage has reached a level where on a lower level of household income (i.e. accounting for a job loss, additional child or whatever) we could still feel comfortable.

Paying your mortgage is effectively giving you guaranteed 7% after tax return. Not many places you can get that.

So whatever your employers will match into Kiwisaver (which is a 100% return) and the rest on the mortgage. Fastest way to pay it down is revolving credit the amount you can pay off in a year then 1-year fix the rest. Repeat each year until gone. I paid off a 30-year loan in 5.5 years this way. Also goes without saying that if you have any other higher interest debts, you should pay all these off first.

I am big on KiwiSaver. But best to knock the mortgage down first. Then continue with building KiwiSaver.

Less mortgage = more options.

Auckland down 21% from peak thats a huge amount of value which some people have lost.the 5 year total is still positive but will quickly disappear as the next phase of crash speeds up, so 2019 price will soon be with us and if downturn continues 2016 price’s will be next stop.

Well, given that prices were pretty much static over the intervening period, 2016 and 2019 prices could be considered the same thing.

Bring on 2016. With 2024 incomes this about makes sense unless your a speculator moaning about vapour losses.

Long may the decline continue.

we need to get back to reasonable house price / income ratios

Poorer month but nothing to fret over. Auckland is the worst performer and even that us up 1.9% from a year ago. OCR cuts are just around the corner so cannot see a further crash.

Those with solid equity, and good income to debt position will agree. Those with neither of those things should have cause to fret.

Drop of 1.6% in the month the up by 1.9% in the will be gone by June and say goodbye the 5 year gain by end of the year. I can’t see the OCR dropping much if at all as the NZD will tumble very quickly pushing inflation back up. If the US fed drop rates we might be able to but they will probably keep them around this level otherwise who will buy US debt on lower rates.

Agree with all points. When low wage immigrations realise there is no work or citizenship and just an endless treadmill for their landlord they will leave.

Living in the land of Hopium there Baptiste.

This crash is just getting started and while mortgage rates are above 4%, the Ponzi is dead. The Tyres are slashed, this ride is going nowhere!

Most regions will end down -40 to -60% is real terms (Auck and Wgtn are there already) come the bottom in 2027/28.

Maybe the regions are not granular enough for this to give meaningful data: living in Otago, it lumps in Dunedin with Queenstown lakes - very different propositions in terms of wealth and affordability ratios.

Yeah this has always been a glaring weakness of the generic "Otago" category.

Same as how with REINZ they always seem to lump Nelson in with Marlborough, Tasman and West coast, or at least Nelson/Tasman together. Nelson is a small area relative to Tasman which covers down to Buller, south off Nelson Lakes and over through Golden Bay, thus skewing the data..

Similarly for Waikato which lumps in Coromandel (Whangamata, Cooks Beach, Hahei, Whitianga Waterways etc).

I have been keeping an eye on some areas . Been absolutely baffled at some of the price expectations. Is it poor realestate staff ? People just refusing to face reality. Some properties on the market for a year at prices above the peak. I'm actually seriously interested how are people looking at the fundamentals and saying my house is worth 10% more than peak

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.