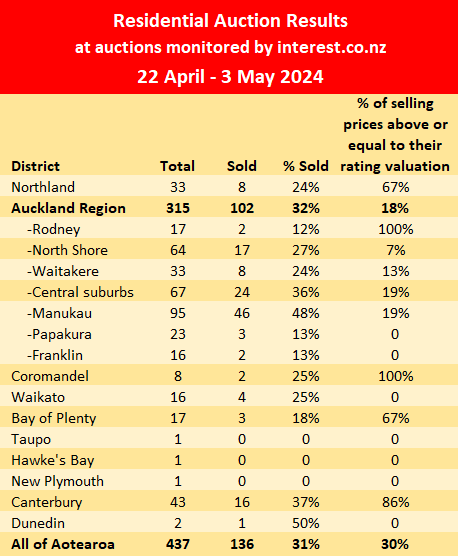

There was a jump in activity at the residential property auctions monitored by interest.co.nz last week (22 April - 3 May), with 437 properties offered up for sale.

That was a decent jump from 364 the previous week but still well below more than 500 properties that were auctioned each week of the peak selling period in February and March.

Although there was an increase in the number of properties on offer, the sales rate stayed pretty much the same with 136 selling under the hammer, giving an overall sales rate of 31%.

It has now remained within the fairly tight range of 28-31% for the last six weeks.

Activity in the auction rooms now seems to be reflecting the overall market, with plenty of properties for sale but sales being harder to achieve with buyers being choosy and remaining cautious on price.

Details of the individual properties offered at all of the auctions monitored by interest.co.nz, including the selling prices of those that sold, are available on our Residential Auction Results page.

The comment stream on this story is now closed.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

73 Comments

25% sold, 0 above CV in the Waikato...

Yep. The flood is cashed up Jaffa's and Wellywooder's has dried up. Lifestyle land in the Waikato hold your breath...

Thats 31% down here in the front, do I hear 32%, good value at that level... anyone?

Its not that people don't want to buy, its that they cannot qualify for funding. Those that have to sell are going to take a vaporware bath. Paper becomes vapor...equity.

The completion rate/ sales rate might rise soon then, it signals down trou prices

I agree Averagman. To put it in layman's terms, prices need to come down to a more affordable level. This affordable level is where the support is and on current trajectory it will take some time. Some Spruiker's conveniently struggle with doing the math on this.

Did some math below R-P .....we'll let Flying high et al digest those figures for a moment ....

Look who's back in for another walloping, its Captain 40 percent and CRAZY side kick

Got something for sale mate ....

No, Crazy

So can you put a "positive spin" on my figures below - look forward to hearing it :)

Do you think I care to counter your spin. You can hold any opinions or interpretation you wish, its a free world.

I would say pick any number you like but don't pick 18.33 then ask others to decipher your numeracy

...18.33 properties sold at CV or above ..

Flying high .....are you disputing my figures, from the table above (for Auckland only) - be only too happy to be corrected.

Affordability is one way of looking at it.

The other is to ask why prices reached the levels they did. In my opinion there are two main reasons. Expectations of capital gains and low interest rates.

So... what are current expectations with regard to capital gains and interest rates coming down? Both not good would be my estimation. Therefore the main justifications for recent property prices are gone.

What will justify prices going forward? For investors it will be yield. A long way down for that to make sense. For a FHB the cost and personal benefit relative to renting. Again, a long way down on that basis too.

Some major regions (e.g. Wellington) could easily be 50% down from peak in real terms before prices become justified on any basis.

Good post!

The majority of readers out there can't contemplate a 50% drop in house prices. But I can vouch that they can, as I experienced such a drop in 1979. I had bought my first house in 1967 aged 19. I paid $11,500 (in new decimal currency) for a tired old house on a 1/4-acre section on the main road of a southern Auckland suburb just north of the main shopping centre. I remember having a saved deposit of about $3,500 from an afternoon paper round and odd jobs, and borrowed about $8,000 from a solicitor's trust account. I was talked into the purchase by my father who was at the time a reasonably successful real estate agent after leaving teaching.

I had a bad experience renting it to the black-sheep son of a Pukekohe businessman and his wife and three sons. I left it in the hands of my father to manage and went on a year or so's OE. On my return I found the inside of the place was virtually wrecked, the more so because I had put much time and effort into doing it up. My father had never inspected it while I was away. So, I had to set to and start over doing the place up again and then renting it out again, this time to a couple with four children.

I must confess that I never did feel comfortable being a landlord, especially to families with children. I new it must be a struggle for them to pay the rent and all the other expenses. Now at the age of 76 years I have come to the conclusion that if you're comfortable being a landlord then deep down you must be a hard-hearted bastard and not the kind of person I'd readily take to.

Anyway, I digress. In 1978 the motel owner next door offered me $44,500 (thereabouts) so I sold it to him and was glad I had relinquished being a land-lord.

However, at about the same time my father had swapped the family home for a bungalow with a large section opposite the place I had sold. He convinced me that I should put the funds I had netted from my house sale into the development of this land which would accommodate about fifteen home units. So we had plans drawn up and with a little extra help from the ANZ we proceeded. We struck drainage problems just as the footings of the first batch of three units were due to be poured. It turned out that part of the section had been a filled-in creek. The council inspector stopped the pour and made us get an engineers report on the ground stability. This report required us to sink a number of concrete piles at intervals into just about every section of the footings. This unexpected expense put us months behind, and, to make matters worse the rain pelted down for weeks on end and the drillers and concrete trucks had a heck of a time trying to get the job done.

And so the job dragged on well into the winter of 1979. While I actually managed to get materials and tradesmen at very good prices, that was only because unbeknown to me a recession had stealthily set in. The weather delayed the build and the ANZ bank manager was soon visiting the site with a worried look on his face. Finally he said, just as we were finishing the build that we must sell them straight away to repay the loan. They proved difficult to sell despite their prime location and in the end we could only get the value of the money we owed the bank.....$90,000 from memory. A year or so earlier we could have sold them for nearly twice that and it wouldn't be for another 15 to 20 years that those prices were seen again.

So yes, house prices could indeed crash from here on in. And a 50 % or so drop in price could be repeated.

Interesting stories SW, the example of your house doubling and then doubling again in value over an 11 year period to the late 70s is very relevant indeed. It echos the discussion regarding a quote posted by Retired-Poppy that said looking at the whole 1970s decade, house values kept pace with inflation of 322 percent for the ten years. The avg house more than tripled in value

High inflation leads to "rampant" house prices. Sorry it fell apart for you after that, you would have been the next Olly Newland or a name you've mentioned before John Hynds of Hynds pipes

Thanks for your interesting story. As a young kiwi living in London in early 90s I saw several friends mail keys to banks when they found themselves underwater and unemployed due to reckless lending/borrowing and recession. I’ve never forgotten it, and see all the same signs in NZ now…. There’s a long way to go (down) before NZ’s 20 year property ponzi is unwound.

I am interested in your story but also interested in your conclusion that house prices can lose 50% of their value. While I agree with you theoretically, none of your story supports it.

Your first house quadrupled in value over a few years, despite being trashed by tenants.

Your second investment was a development which failed to add value because you discovered the soil was loose fill. I would say that is the main reason money was lost rather than the market forces. Concrete piling is nightmarishly expensive.

No, only the owner of the adjacent motel would have paid that price was because the purchase effectively increased his motel land holding by about 33%. The price he paid would be nothing if he wanted to build more motel units. In the event he never did, he just used the house as a semi-permanent overflow rental. It wasn't until I passed the place in 2021 that I saw that the house was on a house-moving trailer at the front of the section ready to be removed. I passed the section some months later and saw townhouses being constructed by Indian builders. Even when I first owned the place the sections along the main road were zoned for high density housing and for motels, vets, etc..

The inadequate fill over what was once a creek and the inclement weather delayed the build by months. So, yes, that was a contributing factor. But it wasn't the main cause. The main set-back was the recession creeping up behind us and then suddenly striking with no warning. In retrospect, it was probably caused by the oil supply shocks in the mid-70's. Up until then the market had been very buoyant from the early 1960s onwards. Also, the suburb had been seen as a nice place to live as a new classy area opened up on the east side. Unfortunately, the powers that be decided the west side was ripe for exclusively low cost housing and the ghettoization began very slowly at first but then snow-balled from the 1990s down-grading the whole suburb.

Hi Greg, is your auction data available in spreadsheet format please? I do a lot of scrolling through it each week. Would consider paying for such a service..

thank you

Those houses are beautiful! Where was the photo taken?

Looks like Five Dock in Sydney

Five Dock may also be Five Million Dollars from the looks of those homes

Fairly standard Australian Federation/Californian Bungalow architecture. You'll find them everywhere.

30 Ngaio street.

Sold May 2021 for 2.715 million

Now asking over 2.1

The reality on the ground, as apposed the flowery language of re Real-Estate lobby

https://www.trademe.co.nz/a/property/residential/sale/auckland/auckland…

Looks like it could be a competitive tendering process. i.e. a slow motion auction. Will be interesting to see the final sales price.

And even with that reduced price it has an estimated rental yield of 2.7%, so it is still at least $1 million over priced.

Why would anyone want to buy this as a rental?

Does it matter? If renters wouldn't pay a decent yield, doesn't that make it overpriced?

Investors are only a small per cent of buyers. If someone loves the home and the location as an owner-occupier, then they will offer what they have available.If 2 or more owner-occupiers want to buy, then that will push the price up.

If you can rent a house for less than half of the interest costs of buying one, why would you buy one (unless you are expecting big capital gains)?

Less than half the interest cost, where? I rent places out and I can tell you right now I'm blown away by some of the rents I am getting.

Why would someone one buy? So they can have a pet, paint the walls in their childrens rooms, not have landlords doing inspections, not constantly worry about receiving notice to move. You may want to live like a scarfy but many don't.

According to Trademe, this place would rent for ~$1130 a week. If you buy it for $2.1 million, the interest on the loan would be ~$2,746 a week. Add in rates / insurance / maintenance / depreciation and its probably 3x as much to buy it.

Seems expensive just so they can have a pet, paint the walls in their childrens rooms, not have landlords doing inspections, not constantly worry about receiving notice to move...

I doubt very much you can rent a 3bed double garage house in Orakei for $1,130 p/w. I also doubt very much it sells for $2.1m, using the same logic a $1 reserve property auction is worth $1.

Are you thinking more or less than $2.1m? Normally enquiries over would mean they want a bit more than $2.1.

I don't know about rents in that area. But here is a 5 bed in Paritai Drive for $1250: https://www.trademe.co.nz/a/property/residential/rent/auckland/auckland…

All 1st world problems... Pets are a liability (many owners don't realise that, the 5mn walk you give your dog is NOT appropriate for its well being), never heard of traumatised kids not having the colour they like/want on the walls, inspections are 10mn every 3 months while you're at work, notice to move will cost you a pack of beers for your mates. None of those are serious matter, we're not in a country at war or suffering from famine.

unless you are expecting big capital gains

This is the crux of it. It's likely that we aren't far off the common person giving up on this idea. The effect on prices will follow the change in sentiment.

Maybe fewer people expect big capital gains, but around the water cooler I am hearing a huge amount of denial from vendors, or soon to be vendors. It’s as if they have ignored the fact that prices dropped nearly 20% in Auckland.

very interesting psychology around it all

Great comment, and hope you’re right. When most people realise magic capital gain is over the next leg down for prices quickly follows.

Yeah. We are renting a place with a valuation (according to Homes) of $1.8m and paying $850 a week.

The interest if it was 100% debt financed would be $126,000 p/a then add in insurance and rates. Obviously the landlord is not 100% leveraged but could have had his money earning interest elswhere if not in the property.

We are paying c. $44k a year. So basically getting subsidised about $100k a year from the LL at the moment (excluding any capital losses).

From the LL perspective they have owned it a long time and want to renovate the property and live in it long term but it works for us in the meantime!

Apartment down the street recently sold for $1.6M, apartment next door (exactly the same layout) rents for $670. It was bought by a recently widowed cashed up retiree. As far as I can see these are the only people holding prices up.

I do feel sorry for some of these people. Not many people can afford to lose $600k just like that.

Um ... It hasn't sold yet!

They probably didn’t lose anything unless they bought in last few years. Only the crazy expectation of tax free gain.

Lets assume it sells to this or thereabouts. How many of such transaction would it take to trigger a sufficient algorithm reset to make homes and oneroof even remotely accurate...?

Popcorn

I don't know how the algorithm works. I don't trust them. Do agent appraisals effect the algorithm or does it only effect that specific property? Does the algorithm exclude outliers? How does it determine outliers?

https://www.oneroof.co.nz/property/auckland/saint-heliers/7-brookfield-…

This sold for 2.58.... One roof values it at 3.13

Will this be considered an outlier and not effect the algorithm? Who knows...

Still way overpriced at 2.1 and CV's suck. Why do we even have them..

I would love to hear your reasoning for this opinion.

The capital value, is the value of a property for rating purposes, not the current market value of your home.

Agents just love to weaponize them, but always tell the buyer not to, if you query the asking price..

Someone will pay the overvalued price for this property. Why? Just because they can and they want it.

For Auckland - 315 properties went to auction ....18.33 properties sold at CV or above ...so a 5.82% chance of a return of the CV or above ..... keep polishing the turd RE agents ...just shows only 1 in 17.18 properties were actually "priced" for the market.

And even this probably paints a rosy scenario as

- we don't know by how much they are selling under 10-20-30-40%???

- nor do we know whether there has been any improvements since the CV was set.

#crazymath ✅

#flyinghighcannotdothemath❌

No worries Captain 40 percent down, yet still 322.4 percent Up

Oh what a paradox

#flyinghighstillcannotdothemath❌

Dimwit

😆🤣

You're just a stirrer with serious issues

Having just perfectly described yourself and with evidence of poor self control what on earth will you call me next?

Void of vital facts and basic research it's okay for you to out others yet you lash out with snide remarks and name calling when it returns to haunt. On several occasions recently you've made a complete fool of yourself trying to "out me" as you put it.

It clearly gives you a rise twisting my posts to mean something other than intended.

Just sayin.

Week ending 5 May 2024 in Oz - clearance rate 73.5%

Just saying!

Your point is what exactly?

Just an observation!

Just saying!

It is quite interesting / curious. Given some quite similar circumstances to here

More realistic vendors…. Been looking in Auckland recently and 70% of vendors are still in lalaland. Which matches the clearance rate…

Paying rent today is not far off a mortgage payment

3 beds $800 a week

You're not looking at the full picture John.

Step away from the microscope.

No. wrong.

Renting is way, way cheaper than 80 to 90% mortgages.

Yip, renting is way cheaper.

By the way, where were you on 17th April after the CPI data came out? You were predicting higher inflation, if I recall correctly.

Paying rent today is not far off a mortgage payment

3 beds $800 a week

Got any evidence to support that assertion?

Do the calculations on this one.

https://homes.co.nz/address/christchurch/sumner/24-dryden-street/o9wYg

For mortgage and rent to be equal, need a max mortgage of 45% LVR.

Dp

There are prints going through on property , like 27% off CV for a stunning Herne bay villas.......

as in the last month, barfoots ardmore rd

The 50% average peak to trough price prediction is on.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.