Average dwelling values stalled at the end of 2023, according to the latest figures from Quotable Value.

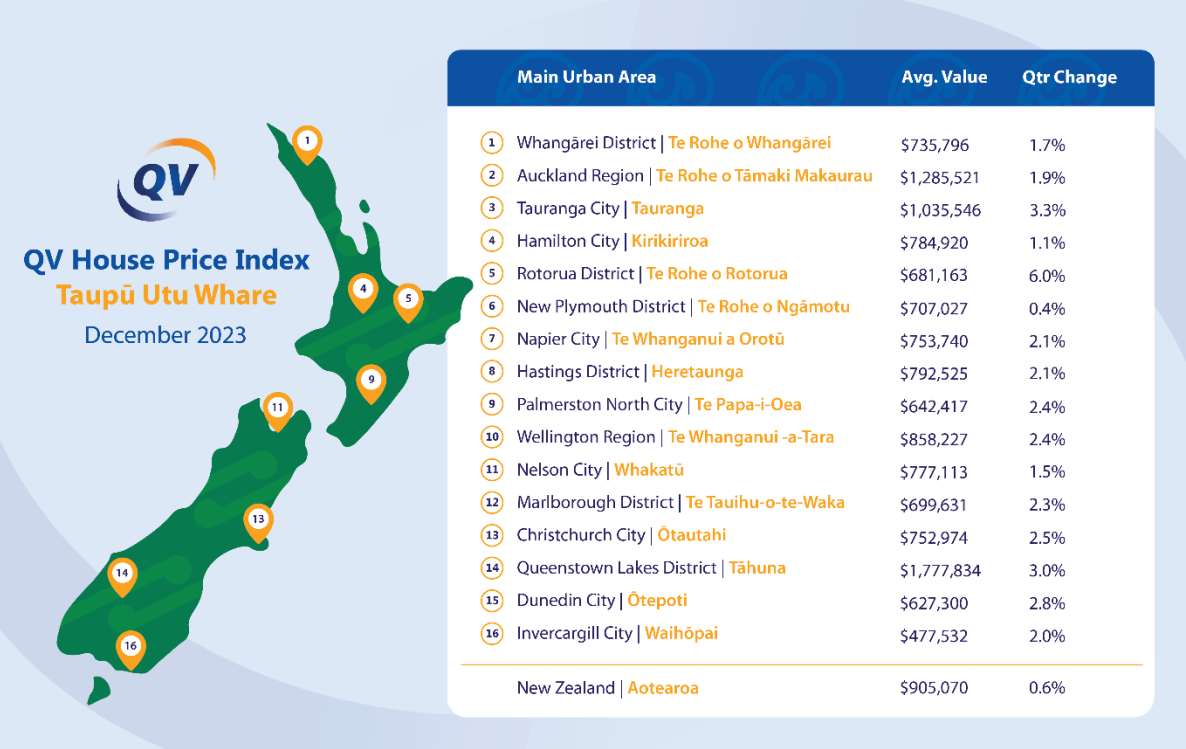

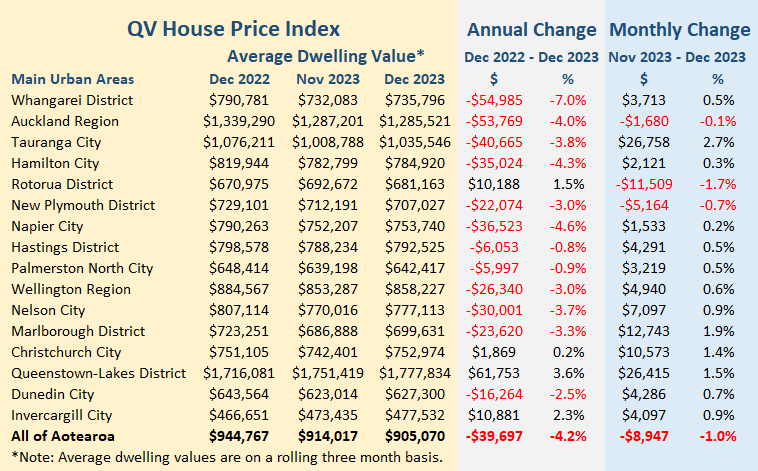

The average value of New Zealand dwellings was $905,070 at the end of last year, down by almost $9000 (-1.0%) compared to the end of November and down by almost $40,000 (-4.2%) compared to the end of 2022, according to the QV House Price Index.

However over the December quarter, the average national dwelling value increased by 0.6%.

Average dwelling values finished last year lower than they were at the end of 2022 in all but four regions - Rotorua, where the average value was up $10,188 (1.5%) for the year, Christchurch +$1869 (0.2%), Queenstown-Lakes +$61,753 (3.6%) and Invercargill +$10,881 (+2.3%).

The biggest declines in average values last year were in Northland -$54,985 (-7.0%) and the Auckland Region -$53,769 (-4.0%). See the tables below for the monthly, quarterly and annual changes in average dwelling values in all main urban areas.

QV's December report said there had been a "general stalling" in home value growth in the December quarter of last year.

QV Operations Manager James Wilson said the latest data demonstrated how volatile trends could be, given current market conditions.

"With relatively low sales volumes in many markets across the country, it doesn't take much change in activity to change the overall value performance," he said.

The stall in dwelling value growth coincides with a slump in new residential listings on the market, with property website Realestate.co.nz reporting the number of new listings it received last month were at an all time low for any month of the year outside of the 2020 Covid lockdown.

The comment stream on this story is now closed.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

31 Comments

The stalling will turn to 'falling 'from next month.. the initial hype has faded

If only many New Zealanders had the financial acumen to invest in property when they were toddlers!

Something doesn't add up. The graph says the average dwelling decreased by $9k in December. But 13 of the 16 regions show a monthly increase. The only region that exceeded the 'average' decrease was Rotorua with an 11k drop in December.

What am I missing? It looks to me that house prices are still rising.

I was about to mansplain the way that can happen when comparing aggregate statistics to their components, but I agree, doesn't seem to add up. Maybe some peculiarity with the use of rolling 3 month averages, but again I can't see how. Perhaps some stats guru can explain?

I was about to mansplain the way that can happen when comparing aggregate statistics to their components

Do you think all the other people contributing to this article are women who can't work their way around indexed sales data?

Is that a serious question?

You're the one doing the 'mansplaining'. Ball is in your court buddy.

Please don't make me explain the use of the term 'mansplaining' in the context of a self-deprecating comment about one's tendency to mansplain, arrested just in time to avert actual mansplanation. The irony would kill me.

Postulation:

The "All of Aotearoa" values aren't just an average of each column, they're also weighted by the number of dwellings in each region, so (for example) a $1,680 fall in Auckland far outweighs a $3,219 rise in Palmy North.

The numbers do seem a bit strange to me too though, surely there aren't so many dwellings in Auckland that they can outweigh the increases in Christchurch, Wellington, Tauranga and Hamilton combined.

(Apologies for the continuing edits, I'm still waking up.) So looking at the columns, the HPI values for each region are correct for those regions, but the All of NZ value is not an average of the values above, it's the overall (weighted by number of dwelling per region) - the average of the raw regional values is about $100K lower. However, the annual and monthly "All of NZ" values are not based on the columns above but on the rows to the left. It's misleading to put them in the columns.

The All of NZ figure probably includes the stuff outside the "Main Urban Areas", eg, all of Manawatu that is outside Palmy. Still hard to reconcile when there really won't be many properties in those areas.

Yeah for that to be the reason there would need to be more dwellings in Rotorua than the rest of NZ put together.

My theory is that the areas that are dropping are not represented in the list shown. The list is “Main Urban Areas”, I think the rural regions are behind the cities in the property cycle and are still dropping - prices continued to rise in these areas through the time they were dropping in Auckland and Wellington. I live in one and we have yet to see asking prices really drop, so not many sales happening here unless the vendors are really serious about selling.

That has to be an error. There's no way that makes sense.

Not suggesting this is why in this particular case as I haven't delved in to it, but this is possible if the number of dwellings in lower cost areas has increased at a higher rate than higher cost areas. Consider this overly simplified example:

- Region A has 10 houses with an average value of $500k

- Region B has 10 houses with an average value of $1m

A quick calculation suggests the average house price is $750k, calculated as (10x$500k + 10x$1m) / 20

Now let's say there's a development finished in region B, and they build 5 new houses. These are nice new builds, worth $650k each. Meanwhile Region B has the same number of houses, but they have appreciated slightly and are now worth $1.025m. So:

- Region A now has 15 houses with an average value of $550k (an increase of 10%)

- Region B now has 10 houses with an average value of $1.025m (an increase of 2.5%)

Yet because the weighting has increased on region A, the average house price is now (15x550k + 1.025x10)/25... or $740k. Average prices have decreased by $10k despite the average price increasing in every region.

Something doesn't add up. The graph says the average dwelling decreased by $9k in December. But 13 of the 16 regions show a monthly increase

Because you're assuming that the methodology is based around basic arithmetic computations at its core.

Most people go straight to the headline numbers without actually understanding the methodology or data composition.

Thinking fast. Thinking slow.

Agree someone needs to check that - clearly still rising from Nov to Dec except Rotorua!

53k off the value of an auckland home is more than 4 percent off the owners equity if leveraged.

Now that's gotta hurt

I guess that depends if you purchased recently or not and if it is a home or an investment?

53k off the value of an auckland home is more than 4 percent off the owners equity if leveraged.

And. If people subjectively feel their houses have lower price tags, this impacts on things like whether or not to get that spa pool or reach for the bright package of the craft beer on the supermarket shelves.

Given Luxon's time at Unilever, he will understand this. Princess Xindy would understand at a superficial level.

Green shoots my ass

The TA and AC pumped up puff pieces talk of green shoots have been doused with the neverfail defoliant of HIGHER FOREVER INTEREST RATES.

NEXT property toxic defoliant that takes out the 5 to 10 year old wood will be the imposition of DTIs and the 2 Year Brightline.

A never fail mix of Woody Weedkiller, Glyphosphate and Agent Orange!!!

An Anni Hirrobalis year for an exposed property ponzi in 2024.

More developers and development land hits the skids, as the Govt stops the KO bailout chest.

TA HAS ANOTHER YEAR OF EGG DRIPPPING FROM HAIR AND FACE.

TA HAS ANOTHER YEAR OF EGG DRIPPPING FROM HAIR AND FACE.

I read that as "...ego dripping from hair and face." Still works, I guess.

Egg? I just call it drivel XD

Whatever the fine detail shows, it's clear house prices are not rushing up.

That's really really good. The house price explosion of recent years has been New Zealand's big social disaster.

Best thing for New Zealander's would be big rise in home ownership, early ownership and mortgage free early as well.

If house prices don't rise then National might get impatient and boost first home owners grants in the name of "helping first homeowners and young families" blah blah...

The road to the bottom after any major market correction has many signs of false bottoms. (And I should add, in real terms, there has been no rise whatsoever. i.e. wages and inflation have gone up by way more than house prices.)

A few DGM's starting to get nervous at the market turn around I see.

Get with the program mate - NZ residential property (especially Auckland) as an investment, if you haven't started already, is a lost cause.

I hear on the wireless, that the great Nikki Connors is plying her trade again - I wish her all the very best, but you new punters, please do your homework ....and some basic math over the long term.

Anyway, I'll be using my crypto profits to top up my income - c'mon all your property spruikers, you all know it's been the best performing asset class over the last 5 years.

The vested are so invested they have acute blindness to alternative scenarios. I do think that if the RBNZ starts to cut rates they are selling out the next generation in favor of Bank profits and thus FIAT speculation.

The next two quarters will be telling. See what happens.

LETS BOOK A CHECKIN IN AUGUST 2024 together - Zwiffy.......when a few more ladder rungs get smashed out of the NZ Housing Ponzi.

@Zwifter your use of the term "DGM" needs a revision, as there are people on this site that have enough intelligence and "street smarts" to know pretty much categorically, that this NZ (& most of the western world) "property speculation bubble" is now OVER.

As I have said many times in the past , residential property investment can be a brilliant investment, with good gains for cashflow, and in "property myopic" Nu Zullin" you can get around capital gains tax as well.

But all good things must come to an end - sorry mate. While I had the sense to get completely out of residential property investment (2020 - USA & 2016 - Auckland)

Have you ever asked yourself why central banks all around the western world started raising interest rates ? - they basically want to deplete as much as possible of the western world's disposal income, and have to force you to live off your savings and credit. While this affects neither the very rich or the poor - but the middle class working slaves for banks and corporations.

Forget about lower interest rates too, as they mean an economy is not creating enough affordable credit, for the banksters to be kept in clover !

I am always very weary of property spruikers, especially now, as it just shows to me, you are totally relying on property for income/business and/or it's your only form of investment/savings.

Diversify while you can !

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.