The value of residential property is continuing to decline in most parts of the country, although the low volume of sales means the figures may be lumpy for the next few months, according to Quotable Value.

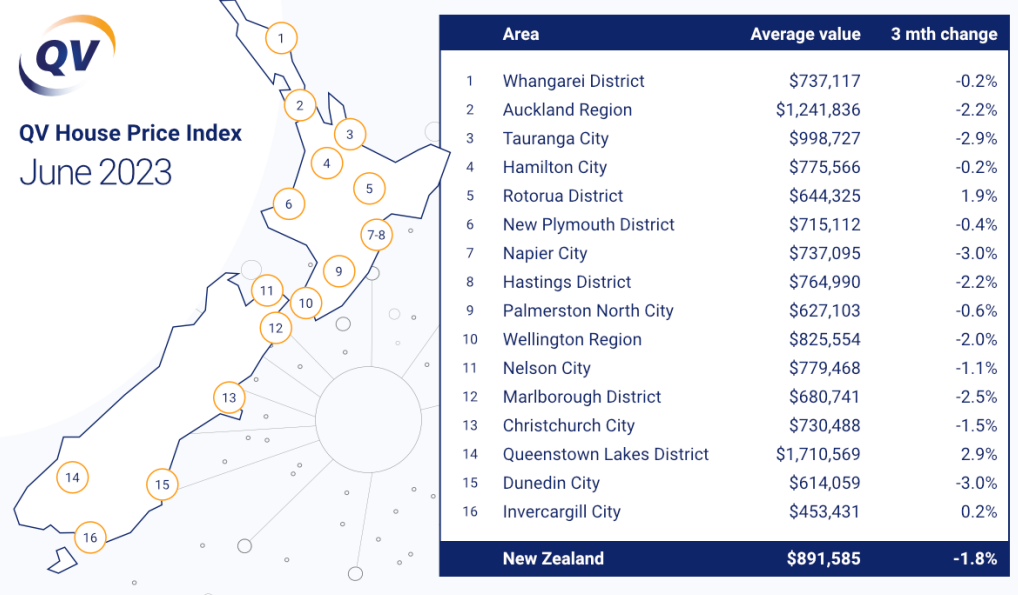

The QV House Price Index (HPI) declined by another 1.8% nationally over the three months to the end of June. That follows a 3.4% decline over the three months to the end of May.

The biggest declines to the end of June were in Napier and Dunedin, with average residential values down in both cities down by 3.0% over three months.

They were closely followed by Tauranga -2.9%, Marlborough -2.5%, Auckland -2.2% and Hastings -2.2% (see the second chart below for the full regional figures).

However QV said the current low rate of sales could make movements in average values more volatile.

The volatility is already showing up in the HPI's monthly figures, with the national average showing an increase of $2655 between May and June. However, the only major urban districts to show average value increases were Rotorua, New Plymouth, Palmerston North and Christchurch.

The average dwelling value in the Auckland region declined by another $16,685 in June, taking its decline over 12 months to just over $200,000.

Tauranga was knocked out of the million dollar club last month with the average value dropping by $5420 to $998,737.

The record run of increasing residential property values in Queenstown-Lakes may also have come to an end with average values there falling for the second month in a row.

The first table below shows how much average values have changed over one month and 12 months in all major urban districts, with the national average declining by $119,603 over the 12 months to the end of June. The average value in Auckland has declined by just over $200,000 for the same period.

Compared to the peak in values at the beginning of last year, the national average value has declined by $172,180, and the average value in Auckland has declined by $299,332.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

132 Comments

Bugger I guess that's knocked all the froth off the top that never actually existed anyway, unless you bought a house at the peak that is. Decent quality homes are still going to get above current RV prices so I wouldn't worry about it if you were smart.

Well according to the auction data - 77% of homes are selling below their RV - so there must be a tight definition of a 'decent quality' home.

And most of those are in the last year compare them to the valuation of 4 yrs ago and you are still doing well. If you buy and sell property in a couple of yrs then you shouldn't make money its a long term

There is now. We have known about all the rot boxes that were built for a decade but now we have the slip and flood prone areas thrown in as well. You have always paid for "Elevated" property, but now you are really going to pay for it. This takes out a significant number of properties. Take out a number of coastal properties that are now watching their back yards disappear as well and you have a short list.

"but now you are really going to pay for it"

You will only pay a premium in relation to other properties. So as more houses are added to the junk list and their real value is revealed (i.e. much lower than people thought) overall prices fall even more. So yes, you're paying a premium but a 20% premium on average values that have halved is still lower.

"the froth off the top is removed"... now the rot is exposed..

"The biggest declines to the end of June were in Napier and Dunedin, with average residential values down in both cities down by 3.0% over three months."

"They were closely followed by Tauranga -2.9%, Marlborough -2.5%, Auckland -2.2% and Hastings -2.2% (see the second chart below for the full regional figures)."

Property Brokers Realty in Hawkes Bay are currently advertising like Mad on the radio for new salespeople to join their team. I can see why !

10% Interest Rates This Year, Guaranteed !

Were you swimming naked in beer Dgm ?

Is that all you can come up with?

Shows how impotent you are..

anyone who relies on RV's for a guide to current market value is foolish. The only thing reliable about them is their unreliability.

Wrong. Its a psychological price that comes into play for both the buyer and seller. Buyers don't want to pay much over it and sellers don't want to sell under it. RE's will tell you it doesn't matter what it is because they just want the sale.

What a load of baloney!! A ‘psychological price’!…. if you’re using that number for absolutely anything then you’re a fool. Know your market, know the value and comparative values of other properties and judge accordingly. The RV/ CV whatever has NO relevance on the pricing/ value of a property . Good luck Zwifter!

Palmerston North bucking the trend...

Same as Christchurch, Timaru Waimate West Coast. But hey the majority on here think NZ only revolves around Auckland and or Wellington. And if you brought in those places in the FOMO period then you deserve to lose your shirt the smart ones waited as the writing was on the wall

People have been telling us for over a decade a decent correction was coming and it never did. So you would have sat on the sidelines paying rent for a long time by that logic, with only you smug "look how smart I am" to show for it.

Not sure who this Colin fella is but he seems to be an expert in everything. Probably one of those guys that you try to have a conversation with, but he keeps interrupting with "yeah I know".

Colin from accounts?

Least I have the b... to use my true name and not hide behind some pseudonym scared to identified

I was going to use my real name, but I didn't want people to know I'm Chuck Norris.

Chuck Norris doesn't mark-to-market. The market marks to Chuck Norris.

You wanting a side job for 2 degrees then

Haha, they haven't got a Chuck N yet

Exactly. People should use their real names. /s

I know a guy named Hugh Wang. Good fella.

his real name is Wang Chung.. Everyone Wang Chung tonight!

That's rich coming from you

People have been saying it for ever. Remeber when a f.. wit mayor of Auckland use to say everybody in NZ either lives in Auckland or wants too. 30+ yrs ago people l knew said why the hell do you (wife) want to shift out of Auckland to Taupo its sooooo..... cold down there. Well both of us were in trades yet couldn't afford a house in Auckland that's well over 30 yrs ago . Be careful who you take/listen to remeber an economists who upto a few yrs ago use to say never buy a house put it in the sharemarket. That didn't turn out well for him. There is way more opportunity now than ever buying property for the younger generation might not be the thing it might be bit coin or some internet opportunities which wasn't around when I was younger.

100% nail on the head there Colin. Younger gens that understand a drop of economics and politics are not throwing their life into over-valued housing in this country. This year, rain for months, flooding and crime is through the roof, alongside COL. Eggs are no longer a cheap stable.

Why would you risk 40 years of your working income for a shoebox that has a good chance of losing it's entire value because of flooding, crime or govt changes in legislation outside of your control.

Bitcoin is mocked often by many on here but it's pure and showing it's strength. If you like it or not, it doesn't care and it's here to stay and will slowly start consuming property, bonds, stock market wealth.

Gold rushes do not last forever, NZ has exhausted the property ponzi gold rush. In saying that, it could very easily go on if the govt props it up to the detriment of society, but the exiting of young kiwis will continue to rise, so will crime, decline of birth rates and hopelessness.

I wish I would be alive when these 20 to 30 yr olds are grandparents to see how they react when their grandkids say you had it so good. You were able to do this and that we can't do this can't do that. Least the my generation and younger had a high chance of living pass our 21st birthday cause our parents grandparents were usually off fighting a war somewhere

Can't fault that statement. Another reminder that stopping to take stock, reflect and be grateful, even for the small things, is necessary to keep a positive mindset.

This generation will be the first in known history to have less than their parents, good to reflect but have to be real too. While older generations are in power and still abusing the system to gain wealth, the younger gens are hopeless.

Sad outlook, declining birth rates has to be the saddest of it all

"I wish I would be alive when these 20 to 30 yr olds are grandparents to see how they react when their grandkids say you had it so good"

I think we would all be ashamed if we are still alive then. Our ecosystems will be fucked, imagine telling your grandkids that your generation was responsible for the fact they will never see a butterfly in the wild or that wild rhinos and elephants and tigers and whales and dolphins and all sorts of wonderful creatures used to roam the world but we killed them all off because we wanted more plastic shit from China and more cars and roads and second homes and 4th bedrooms and another pair of the latest jeans.

I think the feeling we would all feel was a deep sense of shame. I imagine it would be similar to a former slaveowner talking to his grandkids partner who descended from slaves.

And then that very generation has the gall to jump on social media and share memes about how they had milk in glass bottles as kids and weren't part of the "throwaway" plastic society. Uh....hello? Who ditched the glass bottles? It certainly wasn't kids these days.

Still beats being dead in some trench in a foreign land fighting a war you don't want to fight in and your parents never having a body to grieve over.

Ease up mate - instead of being spiteful, perhaps it's worth us all considering the future for our kids and grandkids and working to make that better rather than bickering over who had it better when.

I noticed another comment of yours around welfare payouts, so rather than comment on that, I'll just leave this healthy reminder here.

Not being spiteful just factual. And I am well within my rights to my opinion just like you. Maybe because we have tip toed around alot of subjects and not wanting to offend one person is maybe why NZ is in this predicament that we are.

"It's PC gone made that is killing our country". The argument of the intellectually lazy and ignorant.

The desire to leave NZ for greener pastures is no longer limited to young workers looking to get on the property ladder. Aussie going through some major economic transitions in the energy, infrastructure and mining sectors and has the potential to poach more experienced workers from NZ Inc.

Some guys at work were talking about changes to the Aus migration policy where you are almost guaranteed a PR on securing a job in an area of skill shortage. Recent skilled migrants don't even have to wait long enough to get their NZ citizenships before crossing the ditch, just some NZ work exp under their belt might suffice.

I'd love to know more about how common this is, have heard of instances of friends that know of workmates, neighbors and friends that have left NZ as soon as they get their citizenship, we're a stepping stone for many, don't blame them though.

completely agree re Bitcoin, we are teaching our children to stack sats and forget about NZ housing. The willingness of people in the country to make a buck off the needy by withholding something that is a basic human right (shelter) makes me embarrassed to be a kiwi sometimes.... I hope the housing market burns one day the same way it has in Japan.

Well the jobs do revolve around Auckland and Wellington.

Maybe Auckland, but CHCH surely has more jobs than Wellington as it has a higher population?

Christchurch is also full of Auckland Millennials buying up property (this coming from a CHCH Millennial). It's great imho. Chch demographics are changing for the better. Give it time and Auckland will just become one very expensive retirement village.

Wellington region has roughly same population as Chch, but average wage is far higher in Wellington.

And what is in the Wellington region let's see......mmmm...oh that's right over paid underperformed civil servants. The Wellington region the least productive region in NZ. Canturbury the second .out productive region behind Auckland but as a above post points out most major businesses are based there but actual income is generated elsewhere. Re Wellington about time the MPs looked at their own productivity rather than tell everyone else to lift theirs

Well if we're talking about the 'Region' then Christchurch still comes out ahead in population, if you include the commutable towns in Selwyn, Waimakariri and Hurunui. :p

Fair enough on average salary, but this is also falling. In the age of remote working, there is no reason for Govt departments and agencies in the future to have all their staff physically located within walking distance of the beehive. So i would expect this to wane in the years and decades ahead as well. When you strip that back, there is not much else Wellington brings to the table in an economic sense sadly.

Heaps of future job prospects for people in Wellington, what are you talking about;

Water engineers

Transport logisticians

Walkway and cycleway pavers

How to kill off access to a city center in the name of "getting people moving" - icians

Bike repair shop operator (mostly closed actually due to inability to actually get to the bike shop itself)

Rally car drivers needed to operate emergency vehicles in and out of the main hospital without running over a bike

Bus drivers to drive busses on and through cycleways.

Cyclists to not actually use the cycleways anyway

Also need more bouncers in restaurants and bars - to catch the people who don’t pay their bills

And so is the welfare cheques. From unemployment to health care( cause there is no obesity) to housing supplement etc etc. Take the amount of tax created in each region then minus the amount of welfare debt then we would really see who is the power house. Also take away the headquarters and show were The actual region the income is created like Fonterra and then a real picture will emerge

I thought you liked your landlord subsidy?

"And if you brought in those places in the FOMO period then you deserve to lose your shirt the smart ones waited as the writing was on the wall"

And that sums up the great Kiwi attitude to fellow citizens just wanting a home to hopefully raise some kids (if they can afford it)

Just like pre 87 and 2008 sharemarket crash when everyone was buying shares and telling everyone you can't lose your shirt. Alot of people on here say now we told you so when the market was running hot back then that it would correct which it has.

... flipside: The literal RBNZ Governor was telling the market and banks to prepare for negative rates. The Prime Minister walked back on all commitments to make housing cheaper. Almost every power structure in the country was sending major signals they would not let prices fall.

People have been saying property is overvalued for years because it probably was, but how many years do you sit on the sidelines and how many governments do you watch back-flip on making things cheaper before one spikes prices by 30%? At some point you just have to suck it up and get on with things, and that's what many people were facing.

Up until this point, there had not been a prolonged walk-back in prices for over ten years. A traditional economic cycle is understood to be seven years. Stopped clock logic is just that.

Dude, we know you bought at the peak, it was a bad financial decision. Stop looking to blame everyone else. The IMF had been warning for over 10 years that the NZ property market was overpriced, the signs were there to see 🙈.

And if you brought in those places in the FOMO period then you deserve to lose your shirt

Deserve is going a bit far Colin, many were swept up by poor advice from people in professions with no liability if they are wrong. While personal responsibility always is front and center, there will be many who lose their houses from being sold down the river by so called experts and advisors. No abdicating responsibility here from saying so, just bringing a light to those who may have bought a first home and now be stressed out the wahzoo doing all they can to keep a head above water. Speculators on the other hand....well they can take a bath in all of the untaxed capital gains they already have to fall back on. Fitting that prices increase by double in the space of 12-18months then when they drop back off the wailing begins.

I feel like this list also needs to include the PM, Finance Minister and RBNZ Governor - three of the biggest talking heads in the country when it comes to setting the agenda for future house price direction. This went a bit beyond the usual real estate agent spruikers in the Herald/One Roof trying to pump the market like we see normally.

Nope completely disagree. Orr was saying housing market was a problem and prices were overvalued, so was Jacinda and so was the finance minister.

You heard what you wanted to hear.

25 February 2021 - Adrian Orr

“We’re saying look, taihoa (wait) here folks, there is no free lunch, there is no one-way bet in any investment. And when prices are so far stretched beyond the earnings of the household, that is a sign you’ve gone too far.”

Asked for his take on the impact of house auctions on creating a bidding frenzy, he said buyers needed to stop and reflect on their earnings capability.

“Any type of market that creates a frenzy or the FOMO - the fear of missing out – does create irrational behaviour, so don't get caught up in it. Understand yourself, understand your earnings power, that’s unrelated to who's standing in the auction beside you, and hold strong.”

https://www.stuff.co.nz/national/politics/300238808/reserve-bank-govern…

"And if you brought in those places in the FOMO period then you deserve to lose your shirt the smart ones waited as the writing was on the wall"

Rapidly rising house prices combined with the repeated messages in the media by property promoters / self labelled property market experts may have resulted in buying of residential real estate.

Here are some of the repeated messages:

1) May 2021: Ashley Church: We're deluding a generation of Kiwis with talk of house price crashes

https://www.oneroof.co.nz/news/ashley-church-were-deluding-a-generation…

2) Nov 2021 - Here's why it might be fruitless to pin your hopes on a house price crash

3) Dec 2021 - Tony Alexander - 19 reasons why there's no crash

https://ndhadeliver.natlib.govt.nz/delivery/DeliveryManagerServlet?dps_pid=IE79655584

4) Feb 2022 - Ashley Church: Don’t expect higher interest rates to crash the housing market

https://www.oneroof.co.nz/news/ashley-church-dont-expect-higher-interes…

5) April 2022 - Ashley Church: Four reasons the housing market won't crash

https://www.oneroof.co.nz/news/ashley-church-four-reasons-the-housing-market-wont-crash-41212

6) May 2022 - Ashley Church: Do we now have evidence of a housing market crash?

https://www.oneroof.co.nz/news/ashley-church-do-we-now-have-evidence-of…

7) July 2022 - Catherine Masters: Why the New Zealand housing market is nowhere near crash point

https://www.oneroof.co.nz/news/why-the-new-zealand-housing-market-is-nowhere-near-crash-point-41842

May be just volatility driven by low numbers, Manawatu Wanganui region has taken some large drops since peak as is seen in the long term price drop.

Check chart..not as much as Wellington or Auckland? (I brought in 2018 and still well up)

Still up *so far*

Yes there is lag in the regions, but those areas that inflated solely because of emergency interest rates ( Wanganui, Manawatu and Wairarapa all joined in with the crazy rises of Wellington), are all correcting it’s just the larger centres are correcting first, market has seized up here in Wairarapa as sellers asking prices don’t match what buyers can now afford, it will take capitulation on the part of the vendors to start sales up again in any meaningful volume.

Couple years back someone in our office was very excited after buying in Gonville, Wanganui site unseen. The path to riches.

.

I recall even in late 2021 when we traded up in Masterton, our selling agent mentioned they were locked into a 7 chain of sales. Each conditional on a sale of home, with a FHB at the end on a subject to finance & satisfactory builders report clause. I believe the FHB was a late comer so other vendors had been waiting for some time already.

It eventually all worked out, but if that FHB fell through then it could have gotten a bit disastrous. Sales started drying up around that time, we had slim pickings on our sale and nearby listing stagnated.

It eventually all worked out, but if that FHB fell through then it could have gotten a bit disastrous.

What a terrible shame, a REA 'losing out' on bonkers commission from horrifically overpriced housing at the expense of a FHB. Nevertheless the chain of sales is quite evident today as well.

I 'brought' in 2021. If I look at homes.co I'm up 20%. If I look at ANZ/Valocity I'm down about 15% (was 25% down a couple of months back).

DP

Palmerston North bucking the trend...

That won't surprise those who are well informed about the housing market......

Others will duck for cover.

TTP

With interest rates at 7%, this fall in prices is insignificant. The governments all over the world have tried to intervene in the property market in past 40 years when ever the prices were falling.

This has created an uneven market with too much debt and higher risk of a catastrophic failure.

This is a collective failure of the greedy generation around the world who used housing to feed their greed of making more and more money. Now the next generations will pay the price of buying at very very high prices and remain slaves of banks and their owners for their life time.

The result of this wealth gap is showing with more and more of younger generation going into crime, drugs, ram raids etc. Governments instead of putting money into education and equality have used that debt to prop up the housing market to feed the hunger of few greedy rich people.

When you debase currency like we do, anything scarce and of need becomes an asset fueled market. Sadly property is one that derives value from the poor and extracts it to the rich.

It's the opposite of capitalism when a market is un-accessible by many, but insanely powerful by few.

Bang on. What the vast majority of people still havent figured out is that houses have never got more valuable, except for small increases. Our dollar has just been getting significantly less valuable over time. More of those $$ are required to buy the same property. The covid money print and asset bubble just played out so quickly it's easier to see.

Anyone who has had the metal to buy in Auckland this year amongst the always temporary gloom will be laughing all the way to Matakana in a few years!

or floating

Matakana? You mean that sandbank with expensive properties built close to the shore line that's in danger of being washed away and then looking like the Esk Valley at some stage in the future? That Matakana?

That is Omaha. Matakana, nestled behind some hills with surrounding native bush. Green paddocks, a few vineyards and surprisingly some gorgeous tiny inlets. Magical place to be. Great offroad running, and if you want a quick surf 15mins to Tauwharanui. Wifi suits WFH.

And to date, no tagging.

Financial gravity applies. Let's see what the next twelve months brings.

Stagnant interest rates and lower prices

Auckland dropped $16,685 for the month. That's 6 months savings from an average income family. Lot of people that I deal with has negative equity and banks are slapping them with Low Equity premiums which will eventually break most of them . NO sign of stabilization in Auckland, Tauranga and Wellington.

You make it sound like banks are applying LEPs after they have already had the mortgage for a while already? Is that what is happening?

Banks go through and try to find people who has gone from 30% Equity and dropped it to say 15% Equity and try to apply low equity premium, they have done same during 1987 crash. They have to keep the margins high during tough times. Normally target people with some equity as people with no equity might want to not pay at all.

Ouch! Banks..want to lend you an umbrella when the sun is out..

Exactly, has happened to my colleague.. bought last year, when 1 year rate came up for renewal, since the value of his property is now lower, he was impacted

Brutal. Should have fixed for 5 years. That extra .75% can make a big difference.

And he's expecting his second child

.nBRUTAL is the exact word

What bank are they with? I had wondered whether this was going to happen to people, but someone pointed me to an article where ANZ committed to not doing this (not that they wouldn't go back on their word if things got tough, but I would have thought the optics would be poor).

Given we're starting to see an uptick in the number of news articles about people facing mortgage stress, I'm surprised we haven't heard much more about this if it is in fact happening to people.

ANZ. The YES bank

I'd be dubious about that. All banks have come out publicly (including on this site) stating for someone refixing with the same bank (not refinancing) LEP will not apply if your "equity" had dropped below 20%. If that has happened to your friend then interest should do some investigative journalism and find out why that contradicts the public statements by the main banks.

*** Edit: Just heard back from my broker. If you got the loan with LVR >80 and your equity has dropped further then the bank may apply a bigger margin. They wont add a LEP margin if you started the loan with LVR <80 and equity drops into LVR >80

Auckland dropped $16,685 for the month. That's 6 months savings from an average income family.

Or approx 9 years of savings for the average house price fall of $300,000. That's a few winter holidays to Fiji gone.

Its a crash now not a correction

Its a crash now not a correction

A crash is quite subjective. No clear definition. Can be debated around the water cooler until the end of time.

A crashrection then...?

Maybe Corash?

😏

A smirk? It's a smirk?

"A crash is quite subjective. No clear definition."

FYI, a definition from Ashley Church:

"But what constitutes a housing market crash? ...... I define a property market crash as a 20% drop in the median sales price from market peak, and which lasts for more than 12 months."

https://www.oneroof.co.nz/news/ashley-church-four-reasons-the-housing-m…

Do these figures account for inflation? If not then this is real crash..

How come the main page title says, "Average value of Auckland homes now down by just under $300,000 from last year's peak" when the text claims, "The average value in Auckland has declined by just over $200,000 for the same period." ?

Oh I see almost 300k down from 18 months ago. 100k every six months!

I’d wager that the ocr has not peaked. The USA Fed looks like they will keep hiking the OCR and guess what will happen? We will have to follow suit. The USA doesn’t give a toss about Nz house prices. Let the party begin. 🍿 💺

The big difference with the Fed is they can keep hiking, because people are generally locked in for 30 years on the same fixed rate so it's not damaging like it can be here.

What tends to happen is people are locked in to where they live. "Golden Handcuffs" etc

Good comment.

Their system is such an interesting comparison to ours , due to their ultra long terms ( often 30 yrs )

In nz we often want banks to offer way longer terms like the USA, but for the USA decent movements in their rates can freeze up their whole housing market like we are seeing now. But also lessen the feds impact.

The rbnz won’t want that.

I think a longer term solution for nz is to offer longer rates. But also to control the economy with dual actions rather than just one blunt tool. The other tool could be to raise kiwi saver contributions as this captures a much wider net, plus actually keeps the proceeds in the hands of kiwis long term rather than gifting it to our Australian owned banks.

Yes someone on here a while back did mention that increasing compulsory superannuation contributions could be a much better tool than bluntly raising the OCR and sending a bunch of homeowners underwater or bankrupt.

Only issue is if increasing Kiwisaver contributions results in the same crippling outgoings as an OCR hike, then the end result could be the same i.e. can't service the mortgage because of Kiwisaver contributions. A little bit of data sharing and a formula should help, if mortgages are tied to IRD numbers then it's just a case of netting out the mortgage payments first and applying contributions amounts off the remaining income.

My friend has got 8 rental properties with mortgages. I asked him if he was worried about the increasing interest rates ? He said Not at all !

All 8 properties are in America, all have 30 year loan terms, all will be mortgage free by the end of their term.

He sleeps very well.

He lives here in NZ and says he cannot believe how people are going to cope with the increasing interest rates.

Naturally I said yeah, just wait until you see - 10% Interest Rates This Year, Guaranteed !

When the Fed raises rates we get smashed !

The Prophet and the Late Great St Landers of Cheaper Tomorrow Tried to Warn the People.

On the RNZ article for this story i couldnt help noticing the last paragraph:

On investor activity, Wilson said he had been hearing reports from real estate agents and that a growing number of investors were beginning to re-enter certain locations that they viewed as offering good value for money, although he emphasised that this was not yet a widespread trend

Here's a guy from QV that is supposed to be presenting data, which is gloomy for the industry, but then he can't help adding in some hearsay just to prop up the narrative that things aren't that bad.

WHEN THE CRASH IS THIS BAD.......Never seen these values decline in NZ history at these high sustained, month on month rates.....with no bottom in sight.

WHEN THE CRASH IS THIS BAD...... The RE industry " They just have to lie"

Stay on your meds mate.

if it isn't lying, then what is it?

Sorry to hear of the Neg Equity Zwifty......

Dont worry your Hero Tony Alexander will promise you "A good 5% gains soon" and a "doubling every 7 to 10 years " "its sure as eggs mate"

TA Dross, drips from the corners of your bible "Onewoof".

Old Tones will spring forth again and wisper you some "Sweet Spruiker nothings into your ear"

Never fail Tones will be back soon..........for more of his failed fortune cookie stories....

All signs of an ailing person due to stress.. take care zwifty

All good here mate, back on my bike for a ride after 3pm on Zwift. Would be good to see more Kiwi's online and keeping fit instead of talking total shit on here.

Way to go, mate

Do you sell used cars for a living?

That’s not good. These are “public servants” and should be completely unbiased. I have seen no data that suggests investors are back in the market ( not even from Tony Alexander), QV should not be indulging in heresay feedback at this stage and should concentrate on actual data.

Maybe public servants with a portfolio or side hustle of their own?

"I have seen no data that suggests investors are back in the market"

Anecdotally, a property trader specialising in properties in South Auckland commented that a number of property traders are more active in the market having their confidence boosted to re-enter the market with the "housing market has bottomed" narrative.

Some of these property traders are going into joint venture arrangements with those looking to invest their available cash / available borrowing capacity.

Good for them - optimists. I've always thought the property black hole would suck up every bit of wealth NZ can earn, save, borrow or immigrate. The hose is a bit crimped, but a bit of twisting and squeezing is still adding a few more spurts of excitement.

Popcorn.

"Brothers said interest in both these properties was more likely to be from professional renovators or tradies who know what they’re doing and can focus on a likely sale price."

https://www.oneroof.co.nz/news/vendors-no-longer-in-control-brutally-ho…

How can the 1 months change across all of NZ be up $2655, when most of the regions (including Auckland, the largest) are significantly down?

There are no green shoots this winter...... We might start to see the MSM use the C work if things keep falling 2% per month in Auckland....

If the C word you're referring to is "crash" - it has already been used here.

1) Tony Alexander - 19 reasons why there's no crash - December 2021

https://ndhadeliver.natlib.govt.nz/delivery/DeliveryManagerServlet?dps_…

2) Catherine Masters - July 2022

Why the New Zealand housing market is nowhere near crash point

https://www.oneroof.co.nz/news/why-the-new-zealand-housing-market-is-no…

3) Ashley Church - April 2022

Four reasons the housing market won't crash

https://www.oneroof.co.nz/news/ashley-church-four-reasons-the-housing-m…

4) Nov 2021 - Here's why it might be fruitless to pin your hopes on a house price crash

https://www.stuff.co.nz/business/300449314/heres-why-it-might-be-fruitl…

Hang on, why are some of the data points 'Districts', others "City' and others 'Region'.

Is this cherry picking a little bit? What constitutes Christchurch 'City' - is it the council area? If so does that exclude Rangiora, Rolleston etc?

Same with Nelson 'City' etc. What about Richmond or Tasman? Does the West Coast also fall into this?

It might be all covered within the noted areas, but its not that clear.

I always use pre-pandemic as my guide because that was prior to QE/LSAP and fiscal measures driving assets to the moon, houses where around $700k in Q1, 2020 which today would be $810k thanks to inflation.

Consequently houses are likely overvalued by about $80k assuming that inflation/interest rates ever dropped back to pre-pandemic. I suspect, in reality, they have further to go.down because government is still deficit spending and inflation has been very persistent.

Q1 2020 average 2 year fixed mortgage rate 3.5%. A $560k mortgage @ 80% LVR = $2.5k per month.

For that $2.5k per month, you can now borrow $400k @ 6.5%. @ 80% LVR = $500k house.

But the average wage of mortgage holders is higher now than in Q1 2020.

Sure are. Considerably higher if you were to believe the following. From $33 per hour, to $39 per hour or 18% higher.

https://tradingeconomics.com/new-zealand/wages

So we increase the mortgage by 18% = $472k = $590k house @ 80% LVR. That's assuming cost of living increases haven't eaten a bigger portion of those wage gains.

The average wage of mortgage holders is higher than the average wage of the population at large.

But is the average wage higher than the average wage of a mortgage holder? I.e. is the figure skewed by people who don't really have mortgages because their incomes are sufficient and/or they bought a long time ago?

No, it's skewed the other way by people who have never bought a house.

That's assuming houses had the "correct" value in Q1 2020. I remember 2015 when the general consensus outside the RE industry was that houses were severely overvalued vis-a-vis incomes. If they fall further it'd be just a reversal to economic normality

Agree. An objective view on the average house prices, shows that the prices detached completely from annual earnings growth from 2012 .......so 2012 to 2019/20 was massively overvalued!!

When see that 3 to 6x DTI is an accepted "ok to elevated" home value range. Outside of 6x should not be accepted or paid if you want any good value.

Average NZ Household income is 117k......

Anyway, anyone holding a property and expecting oodels over 6x will likely have a close haircut next year.....when the RBNZ sets a Max DTI stake in the sand.

5 or 6xDTI.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.