The average value of New Zealand homes is currently declining by more than $1200 a week, according to the latest data from Quotable Value.

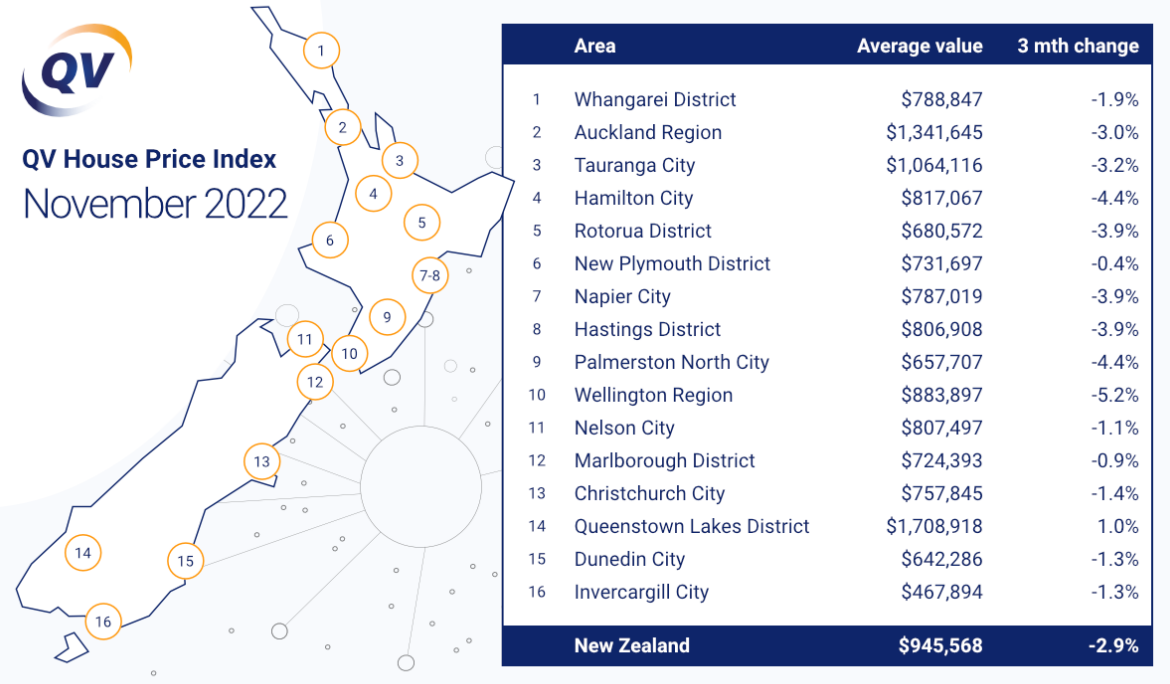

According to the QV House Price Index, the average value of New Zealand homes was $945,568 at the end of November. That's down $5472 from $951,040 at the end of October.

That means average values are currently declining by about $1262 a week.

However between the end of January and the end of November, the national average value declined by $118,197, equivalent to almost $2750 a week.

That suggests while property values are continuing to decline, the rate of decline is slowing.

Over the three months to the end of November the average value of New Zealand homes declined by 2.9%, which was less of a decline than the 3.9% fall recorded for the three months to the end of October.

QV says the biggest value declines since the beginning of the year have occurred in Wellington -18.7%, Palmerston North -14.5%, Hastings -12.5%, Auckland -12.2%, Napier -12.0%, Dunedin -11.5%, Hamilton -11.3% and Tauranga -9.3%.

Queenstown-Lakes is the only district to have gone against the trend, with average values there up 5.4% since the start of the year.

The table below shows average dwelling values in the main urban centres throughout the country at the end of November and how much they declined over the previous three months.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

71 Comments

property values are continuing to decline, the rate of decline is slowing.

QV data is not the latest most up to date... this train is bound for glory, this train

You really possess a lot of Wishful Thinking HW!

I am hoping that it keeps me young and handsome. Mirror mirror on the wall.... 🤡🤓

Supertankers turn slowly, then pick up speed. Big falls to come next year.

Don't bank on it ITG... BAU is around that corner

Core logic data is behind the curve. Wait until tomorrow to get more exacting numbers.

According to the QV House Price Index, the average value of New Zealand homes was $945,568 at the end of November.

Tell them they're dreaming, mate.

118k less than January.

Average Kiwi house is worth 500k, tops.

I'm not even going to start looking at open homes until there has been at least another 300k average fall.

Just turn up now and argue it out with the agent.

The best agent is a hungry agent.

They are not hungry yet.

Then you will never buy a house.

Yes, that's the conclusion I reached a few years ago - they seem to be just too desirable and expensive, and I can't compete, even if it made sense to. I can't think of any scenario that would result in me buying. You guys enjoy the coming frenzy if there is one.

Rates will go higher or stay the same once this works into system house price’s will probably continue to fall. The people who borrowed when rates were at emergency levels when they need to re-finance over next year or two could find themselves to be way over leveraged. Having a million plus mortgage at 7% instead of 3% will put a huge financial burden on many which will accelerate house price falls.As most people in New Zealand would not be able to get a mortgage for 950k from scratch at 4 x income.

I agree with you, but feel a number still have their head in the sand and until that days comes when it rolls over to a 6 or 7%, only then will reality sink in. A spoken to a few who are hoping the rates may drop back down a % or two by June/July next year....nothing like wishful thinking I suppose.

What's 4 x income got to do with anything?

Idouttit surly you know what DTI is, try getting a mortgage at 4 x income not easy these days. So household would need to be making 220k to purchase at 3 bedroom box in some rundown area of Auckland plus have 10% deposit saved this would be 85k more than average wage couple would be earning. Hopefully now you understand what your income has to do with getting a mortgage.

Thanks @DTRH for the insights. I indeed know what DTI is. I am just not aware of any bank that is imposing a DTI requirement as low as 4. Can still get at least 6 with no issues. You need to go see a better broker!

This would be why some many people are over leveraged. As house price’s crash and rates rise banks will put a stop on people borrowing way more than they pay back over next couple of years you will see more people in financial difficulties and mortgagee sales, banks will make sure they are on winning side of the ledger. No point crying to them if you have borrowed beyond your ability to pay.idoutbtit hope you haven’t let some broker talk you into over extending the budget.

From the QV summary:

Wellington down -18.7% since Jan; -5.2% this quarter.

Within that, Hutt City down -22.6% since Jan; -7.1% this quarter.

Upper Hutt down -22.2% since Jan; -7.8% this quarter.

The Hutt Valley was way over cooked . Much more to come there

The most interesting thing I read in the article is that the values are declining but rate is slowing down. The true impact of rate rises is still to be felt and the values are already declining and someone with great insights already saying that rate of decline is slowing. Are they telling the truth to the prospective buyers or selling fake dreams?

I read an article a couple of days ago that the house prices in NZ are still way way above the average salaries and it doesn't really make sense to get tied to a fixed asset if you are young and world which is now open and full of opportunities. The previous generation is getting old and fading away around the world, the young kiwis should develop wings and grab those opportunities.

✈️✅

Meaningful, insightful, strategic and objective analysis on the housing market is missing in action big time in this country.

AFR has good insights, unlike The Herald, they do not make a lot of money via Real Estate advertising.

I wonder if the observed slowdown in the house price declines may be attributed to the season, as springs tends to see an uptick in sales. As things move towards winter, it’ll be interesting to see if house price falls pick up pace again.

Yes. Another potential distortion is that we are looking at average sale prices, not HPIs. So the mix of properties selling (posh or shit) could be pushing it around.

Election next year... we've had an immigration flip flop, what's next...

Prime Minister Jacinda Ardern has asked her Cabinet ministers to reconsider their policy priorities over the summer break, signalling contentious policies may be cut for the coming election year.

Will Jacinda be back to this next year...

Jacinda Ardern says 'sustained moderation' remains the Government's goal when it comes to house prices, as people 'expect' the value of their most valuable asset to keep rising

https://www.interest.co.nz/property/108301/pm-jacinda-ardern-says-susta…

Standard 3 bed stand alone house on 600 sqmt in Pakuranga/Howick and near around - pre pandemic was going for mid 800s to million had gone up to between 1.35 million to 1.5 million (Crazy) and are now still between 1.050 to 1.150 million.

In Manurewa and Mangere it had gone up most from $600k - $750k to 1.1 - 1.2 million and now has the biggest fall and are now between $800k - 950k

Another 10% fall will bring back...some sanity.

Still wouldn't even call that sanity. Manurewa and Mangere are holes, especially with crime rise in last 2 years.

$700k to live a 2 bedroom hole with unsafe noisy neighborhoods.

Very big generalisation. Do you live there, do you visit? High profile crime is occurring all over Alk, let's ignore white collar for the time being.

Not sure about manurewa but mangere is changing very fast, massive building of houses and infrastructure. Massive employment centres around the airport. Lots of new migrants and young people.

Anyone who purchased a 3 bedroom house for a million plus will be watching value disappear very quickly most savvy investors have sold as the housing game is finished and any who purchased at crazy levels will be left way over leveraged for years.

Housing bubble cycle:

1. Rising prices

2. FOMO

3. Euphoria

4. Denial

5. Disbelief (I think the majority of folks are still here)

6. Panic

7. Bust

We are almost at 5 now 🤏.

Reality has still not checked in with those that have paid too much for their house at auctions in 2020 & 2021. It was inevitable that interest rates were going to rise but they just went ahead with no logical thinking and loaded themselves with debt to the eyeball. Bidding beyond what the houses were instrinsically worth. Imagine paying $1m for a house in otara with a section. Now interest rates at 7% alot are going to either have dramatic change In lifestyle to keep their home or a forced sale. The deposit that took years to get will be gone just like that with no house to show for it. Especially if unemployment goes up as the RBNZ wants it too then be prepared for mortgagee sales.

The YTD has all just been a bit noisy in the property sector, hasn't it!. And that really summarizes it - whatever the change in prices we currently see, it's all just noise.

It's when it all goes quiet that we'll get a truer picture of what's transpired.

A couple of weeks old now, but there is probably some merit in his thinking:

Roubini warns that the debt crisis of our lifetimes lies ahead. Every possible remedy to this looming debt disaster brings its own perils: the paradox of thrift, the chaos of defaults, the moral hazard of bailout, the wealth or labour taxes that kill investment or hit the most needy, the inflation that wipes out creditors. Roubini doubts that our current crop of central bank governors are up to the challenge.The strong likelihood is that they will do nothing to stop stagflation — the painful combination of stagnant growth and rising prices — that will make the 1970s look like a warm-up act.

https://www.ft.com/content/3be78531-a7f9-4045-9ac8-88ca64210f59

Still years for this to play out. Plenty more noise ahead.

I still really struggle to agree with the valuations set here - I would hazard a guess to say these don't fully capture the most recent home loan interest rate changes?

What I saw as a standard scenario last year:

- Buyer X has a deposit of $200K

- Buyer X can afford $1550 per fortnight in repayments (Median household income / 3)

- Home loan Interest rate is 3.00%

- Buyer X can facilitate a loan of up to $800K

- Buyer X can now bid up to $1000K on a home

What I see as a standard scenario in the current environment:

- Buyer X has a deposit of $200K

- Buyer X can afford $1550 per fortnight in repayments (Median household income / 3)

- Home loan Interest rate is 6.50%

- Buyer X can facilitate a loan of up to $525K

- Buyer X can now bid up to $725K on a home

Thus, an expected 27.5%~ decrease in overall buying power, and subsequent property value.

This doesn't even go into the number of buyers relying on 10% deposits, to which increase rate increases affect their buying power much more than the above calculations.

Exactly!! Property prices have to keep dropping to meet the true equilibrium at where seller meet buyers. Buyers don't have to buy but seller can be forced to sell. This whole saga comes down to affordability. At 7% these property need a good price drop to sell. Unless it's a cashed up buyers which aren't the majority.

A cashed-up buyer happy to use their capital on a poor investment. There will be some of course.

Well done on posting an intelligent comment Steve!

I agree but think the real story at the end of the day will be buyer Y who had a house in Auckland that appreciated from $800,00 to 1.6m, reborrowed $800,000 against the paper gains and used it to buy two 2br townhouses off the plan in Christchurch for $750,000 each on interest only 3% loans because they went to a 90min webinar and were shown a graph showing prices going up 7%pa into infinity. We tend to vastly over estimate people’s financial nous when it comes to these matters I’m afraid.

Those seminars have been delivering on their promises for the last 17 years or so. I simply wondered how such promises could continue past the abilities of kiwis to afford the prices that were always going to increase. When interest rates hit 3% I felt a bit foolish for not being part of the party. But that was brief, eh?

The next unknown is - what will the common property investor of this last 17 year period do in the next 12 months when they rediscover their asset values and high interest holding costs? Dig their heels in, or quietly slip out, or collapse in desperation...

To get an idea of what the recent property investors will do, let's look at their total debt to incomes (TDI).

In September 2021:

10% of investors had a TDI > 9

37% had a TDI > 7

68% had a TDI > 5.

That is a lot of risky loans. At current mortgage rates, you could easily make the argument that 37% of those loans are "risky" or even "subprime-y". If rates go even higher, then that 68% on TDI > 5 are looking pretty shaky and risky and subprime-y too.

What will they do? In the absence of any more stupid interventions from the RBNZ, they will need to deleverage.

The government and the RBNZ and the banks can try to prop up this stinking pile of overleveraged folly for a bit longer. They probably will try to prop it up again, as they did during covid. But at some point the pile of debt becomes so stinky and huge and risky and unsustainable that it just collapses in on itself. Especially as values lowers and LVRs start getting blown out the wazoo. At 6% mortgage rates I'd say that we are just about at collapse point. Another couple of nudges from the Federal Reserve and all those "savvy investors" with DTIs > 7 are going to be toast.

https://www.interest.co.nz/property/113230/new-reserve-bank-debt-income…

I spoke to one of my investor friends yesterday, who was really happy they managed to refix for 2 years at just over 6% just before the last OCR rise. This is not a specuvestor - they provide a service, and bought their portfolio over 2015-2017 with no intention to sell - but they said they are toast if their rates hit 8%, and are currently working 3 jobs + taking rental income to keep it all afloat.

They're quite literally praying that rates have dropped back in 2 years, and they have no unforeseen circumstance between now and then. Main saving grace is they went in with cash instead of using equity.

Sorry Chaos, but your friend is a specuvestor.

They clearly paid too much for their "investments" and are part of the rot that caused house prices to go far beyond sensible.

Well, our definition of specuvestor obviously differs.

To me, it's someone who bought for capital gains, and are 'speculating' on prices going up. Sometimes, they might say differently, but true intent is shown when they eventually sell.

Don't get me wrong, I dislike investors who bought for yield off someone else's income - surrogate mortgage slavery, in my mind - and my friend and I are at significant odds over the ethics of his chosen investment. But I know they didn't buy for capital gains, so they are not, to me, a specuvestor.

Or do you consider everyone who has benefited from leveraging capital gains a specuvestor (including OO upsizing)?

No doubt, all who bought in the last few years, including my friend, overpaid. But it was still rational behaviour.

What's a "specuvestor" ? (apart from someone you just don't like)

Anyone that is now being exposed by a)higher rates, b)having to actually pay tax, or c)both. Clearly purchased for capital gain in a rising market frenzy of cheap debt where normal yield didn't make sense. They are in effect the risk proxy/front for bank profit/renter exploitation. Will the banks let you fall further and further behind over the newt couple of years. I think not by hay....take your chances.

Smart money sold at peak debt stupidity, or used the window to pay down/eliminate debt.

They are obviously under geared then .

Hardly “investors”

Rates will peak and go back down to the 5's or 6's in 2 years time so he will be fine.

Your friend should sell one or more of his investments. If he is getting stretched and stressed (working 3 jobs seems crazy to me).moto me this seems a rational response, rather than trying to hold it together and praying nothing goes wrong. And, if he brought back in 2015-17, then he will have ample capital gains to release.

No one showed up to the auction :(

Exactly.

And it doesn't matter if the prospective buyer can service that 525k loan - can they actually borrow it? When you add on the stress test (I've just added 2% on to take your example to 8.5%), that is reduced a further $96k down to $437k. But tbh, I don't know if the banks are doing that or not, since I'm not actually looking to buy. As I posted a couple of days ago - our $2000/fortnight rent (to use your payment schedule) translated to a loan of $564k - and we're far above a median income family.

But really - a median income household is not purchasing anything these days. and hasn't for years. Sure, there have been some stories floated by the MSM in the last couple of years - but on closer inspection all those stories revealed something exceptional conveniently ignored.

Yes this QV data is on settlements so can be 6 to 12 weeks out from the time of purchase ( unconditional contract). The best place to find current prices is on the auction page here on Interest, comes out on the day of sale. Last I looked some ( not all) properties selling 20-30% below 2021 CV in Auckland.

Most comprehensive and reliable data comes out in a day or two ( or is it today Yvil?). This is sale at time of unconditional contract for the prior month so is quite current ( data is 2 to 6 weeks old). Where I am, lower North Island, the webpages publishing estimates and sales are getting less and less useful, sale prices are not being added and estimates are being influenced by “agent assessments” being added into the data.

I understand some banks will loan more than 30 % of income. I was astounded back many years ago when my bank manager explained the bank worked on basis of ( from memory) $350 per week left for living expenses after all loans were accounted for.

Where I live house sales are few and far between. Especially $1 to $3m. Who wants to borrow as rates rise? The Banks are lending less as they get tougher. As sellers blink and take the offer before them prices will reduce even more. It is going to be a tough time for some. Why did they borrow so much when those low rates were going to eventually rise.

Agree, who is complicit in this? Is it the banks or mortgage brokers who have been pushing all this borrowing? My son and partner went to purchase at the very beginning of the pandemic. They needed a $500,000 loan - their mortgage broker tried to persuade them to borrow an extra $100,000, who knows why I guess 5o do improvements to the house. They didn’t thank goodness.

Had a similar conversation with my lawyer when sorting out a mortgage in late 2019. First number given to me by my bank was $580k, including deposit. Lawyer said that would put me in competition with every other FHB and property investor looking to buy due to easy money to be had at the time.

Went back to my bank, saw they had made an error and were assuming we would still be renting, so came back with $720k as the new number, and we dropped $700k of that on a 5-bed property that most FHB's and investors wouldn't even consider. $140k deposit and $560k loan.

Did I contribute to the problem? Possibly, as the RV was $640k, but at least we weren't paying $580k+ for a property with an RV of $350k. There were auction sales for houses half the size and in far worst condition than what we bought for almost the same money. It was a crazy time.

Hopefully you will be just fine, could be worse you could have a $800,000 mortgage. Good thing is 5 bedrooms gives you plenty of room to get flatmates in to help with mortgage payments.

We are doomed Captain Mainwaring

Don't panic, don't panic.

So what if they dropped $118k since January 2022? They are still up $217k since January 2020. And for what? Doing sweet nothing, as far as I can tell.

Sure. You could be in trouble if you bought at the beginning of this year, but why would you? The writing was on the wall with regards to OCR increases, which translates to mortgage rate increases, reducing demand, hence house price falls.

I agree with most of the commenters though, that house prices need to drop further before you will be able to buy that January 2022 priced house for a January 2023 mortgage.

As Supersonic_steve estimated in his post; a household could have bought a $1 million property last year but can now only buy a $725k property. However, that $1 million property is still going for $900k, so is no longer affordable.

Still on the upside even out to Sept 2020 if you purchased then. Factor in the $30K PA in rent savings as well and you are still way ahead.

I agree, if they had bought that $1 million property and fixed for 5 years at 3%. If they fixed for 1 or 2 and are rolling off into 8% territory then they would have trouble servicing the mortgage.

Suppose we have to wait for another influx of chinese ans indian millionaires to buy up all the investment properties cheap

Talked to a commercial agent today. Asked about yield, and he tried to tell me that Commercial value had nothing to do with yield. I guess in the last ten years its been so one sided with speculation ignoring yield the poor young bloke had no idea the two could be related. For development rich land bank sure. Anything else has to beat money in the bank by some margin other wise why take the risk. Especially with a recession on the horizon.

Slightly unrelated topic.

Anyone here knows Mr:Des ?

Red fingerprint man refuses to pay mortgage as bank didn't lend him 'real money' | Stuff.co.nz

Main types of arguments

Despite the wide variety of pseudo-legal arguments and fresh iterations, they generally run along one of the following lines:

- The bank did not advance real money (or physical currency) to the borrower. Rather, all it did was make book entries or electronic transfers, in effect creating funds out of thin air. Thus, if no real money was advanced, a customer cannot be required to repay it.

- On signing a loan agreement and establishing a mortgage, the customer’s signature converts the loan contract into a financial asset (promissory note). This asset is the property of the customer since the customer created it by their signature, and the lender is liable to the borrower for the value of this asset.

- A bank cannot require repayment of a loan unless it provides the original signed loan and mortgage documents, referred to as “wet ink” documents. The customer may challenge the bank practice of scanning documents.

- The customer purports to revoke the power-of-attorney clause in the mortgage document, which they suggest means there is no debt to repay (see case note).

- An individual has two personas, one of flesh and blood, and the other a separate legal personality (the "strawman"), and all debts, liabilities, taxes and legal responsibilities apply to the strawman rather than the flesh-and-blood persona.

- A loan is not valid unless it is drafted in a particular way, stated as in “Correct Sentence Structure Communication Parse Syntax Grammar” (C.S.S.P.S.G).

There may also be certain phrasing in correspondence that indicates a customer is presenting pseudo-legal arguments, for example:

- Without prejudice. Notice to Agent is Notice to Principal; Notice to Principal is Notice to Agent.

- No assured value, No liability.

- Errors and Omissions Excepted.

- Without Prejudice – Without Recourse – Non Assumpsit.

Correspondence from a complainant may also contain fingerprints in red ink, stamps or seals.

Pseudo-legal arguments have not been upheld in the courts in New Zealand or overseas.[1] No court has ever ruled that a loan agreement or mortgage is invalid on the basis of such arguments.

Lunacy. Similar to sovereign person rubbish. Sadly, mentally I’ll and credulous people like this are easily exploited by grifters.

There is a big concentration on house prices. But what about the effect of higher interest rates on rural land prices.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.