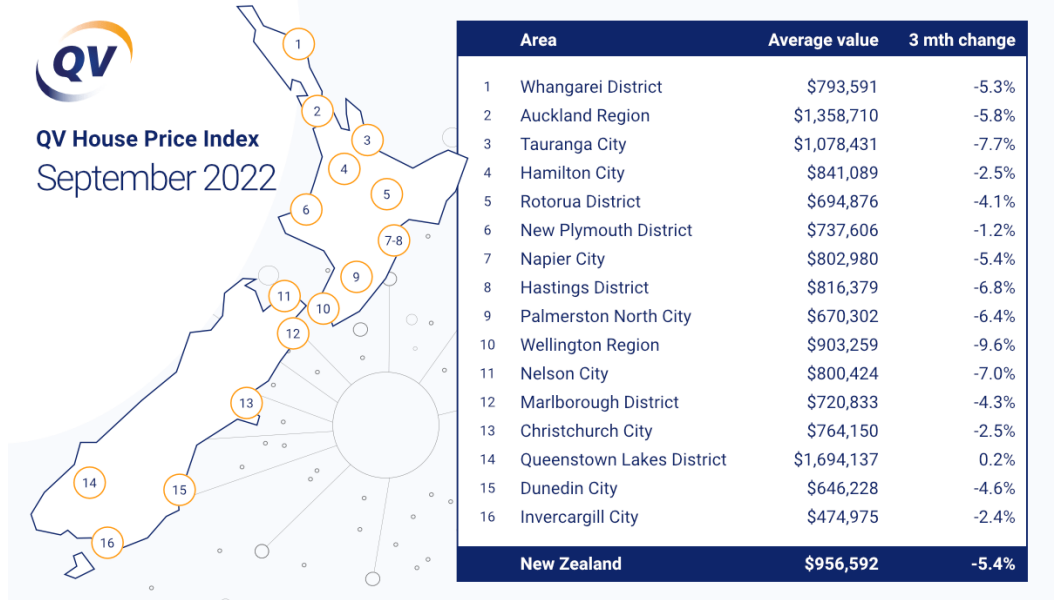

The average value of New Zealand homes has declined by more than $100,000 since the start of this year, while average values in Auckland and Wellington have declined by almost $190,000.

According to the QV House Price Index (HPI), which tracks the average value of dwellings throughout the country, the average value of New Zealand homes was $956,592 at the end of September, down by $107,173 compared to January.

In Auckland the average value was $1,358,710 in September, down by $189,458 since January and in the Wellington Region the average value was $903,259 in September, down by $189,706 since January.

All districts tracked by the QV HPI had substantially lower average values in September than they did at the start of the year, except for Queenstown-Lakes, where the average value was up by $94,613 over the same period to $1,694,137.

Other areas where average values had declined by more than $100,000 since January were Tauranga -$119,367, Hastings -$112,349 and Palmerston North -$105,514 (see the table below for the full regional figures).

Average property values across the country were also 2.1% lower at the end of September than were at the same time last year, the first time that national housing values have declined on an annual basis since June 2011, according to QV.

QV General Manager David Nagel said he expected average values to keep falling.

"The Reserve Bank's decision last week to raise the OCR by another 50 [basis] points all but ensures that the path we're on will continue for the foreseeable future," he said.

"Interest rates rises, credit constraints, the increasing cost of living - it's a sure-fire recipe for declining home values.

"Plus there's still new houses coming onto the market up and down the country, putting further downward pressure on prices almost everywhere."

The comment stream on this article is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

108 Comments

And there it is. Year on year drop for the first time, and impossible to spin this any other way.

Never underestimate the art of likes of Tony Alexedr's ........so called independent economists and lobbyist.

Will not have to wait long by tomorrow should hear some twist

If you divide the mean from the mode, proportion to gold value on 03/10/22, use that number and times usd, then add in Orrs salary but if you bought bitcoin in 1965, then prices are up 11% this quarter, the bottom may be here, its totally up to you but you may miss the boat again young person and it could be all your fault.

You forgot to multiply the outcome by the number of spanners in a sidchrome tool set. Armature mistake!

A uniform percentage decline in asset prices is actually a good thing if you're trading up. You buy on the same market that you sell, and the more expensive house that you want to buy will have depreciated more in nominal terms that the one that you sold. Of course it depends on how leveraged you were to begin with.

Except this is old news and has already happened back in June/July according to the more accurate REINZ HPI data. They reported yesterday we're 8.1% down YoY.

House prices drop, cool. But I am a renter and haven't seen rents dropping. Maybe they just keep rising with inflation

Pretty much, yep! Rents rise and fall with incomes, not property prices, in a supply-constrained market for an essential good like housing.

You can expect rents to drop or slow their increase when we have a recession, because incomes will drop due to joblessness and less bargaining power for workers.

I dont know, probably landlords are like any other shopkeeper and put prices up anyway. Shopkeepers know sooner or later people have to have somewhere to live, something to eat and something to wear. Maslow.

Flying High, are you really a renter? Thought I'd seen you post before about owning multiple properties, including some in the USA?

... could be wrong of course...

Multiple properties. I wish.

I don't get it, what is the hysteria this morning ... started by retireed person and carried on by yourself. Fearful like the Black Power wanting to be reassured of a new recruit?

I have already confessed that I own a rental in another city.... Dont call me Sam Uffindell. Now its your turn and retired person turn. Oh that's right he already distanced himself as not a tenant. Liar.

Smoke screen. The key here is, unlike your desperate self, I don't need to lie to get my point across. You're making stuff up. The truth is easier to remember ok😊

You're coming across as cornered now 😁

Too embarrassed to admit spending your hard earned retirement money on rent, and getting angry to deflect. Keep it up boomer who didn't think ahead or went broke or divorced somewhere along the years. Whats got you so worked up, and since you brought it up, are you sure that you aren't Fitzgerald?

Hang on... you are looking down on RP for "spending hard earned retirement money on rent" ... and yet you are a renter yourself?

You imply that they should be embarrassed to be renting... and yet you are a renter yourself?

Seems strange.

Probably come back with some fabricated story about how much of a genius he is because he rents and invests his savings in high returning stocks and will buy a house with cash when his foolproof plan bears fruit in 5 years time.

Renters can be more independent than home owners. My wife and I were renters for about 5 years before we bought our first home in 1997. We paid cash. As I've said here before, we have never had a mortgage. I have never calculated the amount of interest (dead money) we have avoided in doing so 😊

What an ugly thing to write! Behave.

All sorts of things can happen to people in life...so be kind or don't post.

I think it's all the same comes down to price, market, niche, supply and demand with a dash of perception.

We sell e-commerce products online we find a niche where their is high demand and low competition and good margins. Then we differentiate to stand out from crowd and offer a premium product so we don't fight on price.

To me most shop keepers have a lot of competition and low demand unless it's a local new world. Some are in great locations. But it's not cut a dried.

Whereas landlords if there is an oversupply of houses and demand is low, with no diffentiation, there's only one way for it. Friend of mine renting awesome house, because landlords wanted to sell, but couldn't get what they wanted and that was 6 months ago, things will get worse when more people need to move but can't get what they want when trying to sell, they all think it's a blip. Sounds like the Rolling Stones.

can't see rents dropping if they going to open the borders

What about the new homes built in record numbers and the zero pop growth last two years, rents still increase 5 percent or more. Probably, I think the govt has wrong settings for interest rates, and tax deduction. But we do get a heatpmp

Flying High (AKA-buylowsellhigh) Why are you masquerading as a renter when you are not?

Perhaps its because you and Tim share the same insecurities...

So let me understand this. I am insecure, yet you are in a spin of who I am and what I am.

Very ironical and very defensive.

I'm prepared to coin it! You're suffering from "Landlord Syndrome"

Why deny your now outdated investment strategy?

Hope you can understand this😁

Congratulations if you've been holding off buying this year. You've saved yourself $10k per month.

In Auckland since January - appox 40 weeks, so people who overcame FOMO has saved $4750 per week.

Question is not if it will continue but the speed of fall, will it be similar or more with dominio effect yet to set in and all data, news, opinion suggesting that worst is yet to come and next 6 to 9 months will be........

Don't forget the interest you would also have to pay on that $10k over the life of a standard 25 year loan. Probably somewhere around $18k per month...

Now wait another year and you’ll save another 200k

I see some older homes, with renovated baths/kitchen, asking for the price of a new build. And a few more rentals, in need of repairs, too.

Are those old ones in the same suburb and having the same land area?

Yes it used to be that the costs of needed upgrades was deducted off the purchase price of a house. During the frenzy of the last two years with multibids etc this did not happen. An agent told me in that time that “people don’t care about upgrading needed”, must say I saw some terrible properties with big issues sell for high prices.

I’m not sure this behaviour has rolled back completely yet. Plus Kates previous comments about RVs is part of this…. RVs don’t take any depreciation/ determination into account. We now have numerous websites using RVs as the base in regularly updated “valuations” that some buyers are still putting way too much confidence in.

It was absolutely insane out there previously. I attended auctions for what I knew were complete bowlers and that previously, people wouldn't have touched with a barge pole, yet desperate buyers were suddenly paying moonbeams sprinkled with stardust for, under the firm belief they only needed a minor reno. The only upside I can really see there, was it gave owners of leaky and otherwise worthless homes the chance to get out, without losing everything. I have wondered if some of the RBNZ / Labour inaction we saw, was because it might have been recognized that the only way out of NZ's leaky building financial quagmire was through skyrocketing house prices?

Moonbeams sprinkled with stardust where settled as NZD into my account on settlement day.

I look forward to buying residential akl property when average prices are no more than about 5x average income. With a reasonable 10% deposit that's about 600k. Still a long way to go.

Dreams are free...

Given that prices have probably dropped 20% already thats only another 30%. Not unheard of in bubble popping periods. I feel I'm being quite generous to speculators.

Once the printers are turned back on wait till things get very messy next year, dreams may come true

It doesn't matter how messy things get. If inflation stays high they will have no room to turn the printers back on. Even if inflation comes back down somewhat, after causing all this economic pain in order to rein in inflation, do you really think they will simply undo it with further money printing? Sadly, while I think that would be madness, I can't actually rule it out.

All you have to do is look over to the UK for am example... No one thought they would turn the money printer on but they have.

Good.

".....- expects them to keep falling" " Are the key words and more stressfull for many than $1900000 fall in Auckland.

With the fall till now, only the froth has been cleared and the real fall will be now, when it happens and will be more visible, as now that froth has been removed.

How is it that Napier has gone down 97K and yet Property Brokers is advertising on the radio that prices have been increasing over the last 3 months ?

"Property Brokers country ... robbing me with pride."

Kevin Wagg from Property Brokers is specifically claiming the market "Bottomed out in May". And the market has been increasing Month on Month !

But how does that line up with Q.V claiming the market has gone down -5.8% over the last 3 months ?

https://www.interest.co.nz/personal-finance/117534/qv-says-average-nz-h…

The same Property Brokers that has been fined millions of dollars for deceptive and illegal business practices?

Well first of all, they're lying.

I wonder which party are lying that you are referring too ?

While doing my Apprenticeship under The Prophet I would laugh at some of his jokes. Hay - What has more Spin than a Turbo The Prophet would ask - A Property Broker lol lol lol lol.

For a Prophet he sure had a Wicked Sense of Humour.

May he RIP

Take a punt at where the mic was when they recorded that ad.

A few more of these $100k+ drops, and we should be all good

Yet they still say 'Buy when you can afford to' Yea, like the ones who shot themselves in the foot, right at the peak which was at the start of the year, eventually property does appreciate in value over time… But how long does one live for, imagine saving up the $200k extra you paid or owing.

The people who say 'property does increase over the very long term' also say 'nobody can predict the future'.

Yes, prices are dropping, so what?

They will rebound in coming years and surpass where they have recently dropped from - why?

Because of the rising cost of building materials and labour. Existing housing stock must therefore be worth more.

So, right now the cost of building is rising and house prices are falling. Isn't that impossible, unless you're missing some important drivers of the market?

How long do you think this impossible disconnect can persist?

To get you started - consider the role of the price of land. This is the majority of the price of an existing property in our more overpriced suburbs.

Exactly, it's the price of land that's dropping while the price of houses keeps increasing. Eventually a new equilibrium will be reached.

New builds should be seeing relatively smaller drops as their land-price-to-house-price ratio is lower.

Exactly. Well put.

Amount of land is also dropping

This appears to me to demonstrate an attempt to rationalise and bargain with processes that are not entirely rational.

There have been numerous global markets busts where assets have been sold for less than they originally cost or were worth (all markets, not just housings obvs).

Absolutely blows my mind when people insist that markets universally operate rationally. They just don’t and the research very clearly proves this.

Emotions and sentiment are every bit as much a feature in inflation/deflation as anything else. When markets are volatile, when people are highly leveraged and exposed, some people panic, or cut losses, or they simply cannot afford the debt regardless of the cost to build. It’s not about a rational decision. If you can‘t afford your mortgage your have to sell, if lots of other people also need to sell, supply/demand pushes prices down (regardless of the cost to build). And there has to be a buyer at the price point. There is no law that states that something must be sold at a profit.

Businesses fail without appraising basic fundamentals yes, but business fail all the time, losses have to be realised all the time… why do you assume somehow the NZ housing market is impervious to this? Many people spend money in anticipation of sentiment that simply doesn’t exist when they come to sell….and offloading becomes more important. You guys really need to read some behavioural economics research.

I’m not saying this will happen but just that it’s utterly insane to deny what we actually know about market behaviour, previous housing crashes and assume that everyone will act rationally. If people were rational they wouldn’t have taken on debt at x9 and x11 their income assuming that interest rates would never go up.

It has been convincingly shown that it is the availability of cheap credit as well as policy that favours house purchasing that causes house price rises. Now the the cost of borrowing, which is only going to increase in the short term, is pushing house prices back down again. Hopefully we will find a happy place where an average salary can pay an average mortgage on an average house.

It doesn't reflect in the market here (Hamilton's northern suburbs). IF it ever materialises then that would make me feel a little better not having wasted months of rent while hunting. That said I'm serioulsy considering having a break from it, sellers aren't ready yet. Carlos67 is going to say I'm the dreamer here, but again, once I lead an auction why would I go higher? If my offers were such bargains surely someone else in the room would overbid.

We're the same. Top bidder at a property back in june...passed in, owners went on holiday for a while and property will be back on the market soon. Don't know if we'll bid again (under our initial bid....which was substantially under their reserve) or just wait. Rent sucks..but so does interest on a depreciating 'asset'

Rate’s will not be going down to ridiculous levels again we are going to have years at 6% to 9% mortgage levels .House prices will continue fall as average wage couples have no chance of purchasing a property in Auckland and many other areas. If you are over leveraged and with speed of house price fall’s negative equity will soon be a problem for many, the doors are closing sell what you can quickly or you will be left holding huge debt bag for years

On these figures, Auckland is off 12.2 percent (189/1547).

Though falls are not done yet, based on earlier giant gains 12.2% is a soft landing.

Hard to see that there will be a lot more downside in it as there is seller resistance and not the urgency to sell. Case in point... Retirement villages are struggling to shift units as old people simply refuse to drop their asking prices. Even though old people are the ones in the best position with the most equity. They can see that by capitulating they will have less net funds left after paying out the mortgage and paying for the LTO.

So who exactly will be prepared to meet the market?

Very hard to call the quality of the landing before we've touched down. We're still descending in the fog hoping the runway isn't far away at this point.

I reckon we are at about 35,000 feet still. long way to go. nobody's ears have started popping yet.

Somebody always needs to sell. Death. Debt. Divorce.

Nobody ever needs to buy. They can always rent in the meantime.

The sellers will meet the market.

Maybe death, maybe divorce. Not debt

Buyers have a timeclock as referred to by Warren buffett during the gfc

HW2 the debt refers to the sellers debt not the buyers. And yes, debt costs rising is a very common cause for why someone is forced to sell.

Debt costs are escalating quickly and many people will not be able to keep up with those costs for as long as they persist. Those people will sell, some will sensibly do it sooner rather than later, some will be pressured by the bank.

This is something that happens in every single housing correction, especially after an irrational bubble and when precipitated by changes in interest rates. The people who sell because of debt are usually those who are highly leveraged (investors, FHB and those who have used their housing equity as a piggy bank). It’s quite easy to look at the RBNZ dash board and appraise how many people are highly leveraged and how many will come off the cheaper rates over the next 18 months. Inflation is also eating into affordability.

Very clearly debt will force many people to sell and add to the existing glut that are not clearing.

We are heading towards the wall and people saying is it a crash house price’s are only down 12% to 20%, once we hit that wall anyone who survives will wish they got out at 20%.

yeah, there is that old property saying "now is always the best time to buy"

i guess we can now change it to. "now is always the best time to sell" ;)

Maybe you are right. I dont think so but we can all dream.

For the old people who do not sell at least they have an asset. How much will an LTO be worth in future

For the young families that decide to keep renting, it costs them 100k in earnings over two years.

That is not a useful metric HW2….. to accurately make a comparison you have to factor the cost of the homeownership (rates, maintenance and mortgage interest payments) from that same time period at the price point purchased and the current interest rate, then adjust by inflation, and THEN you compare the rate house prices are dropping vs what you might spend in rent to determine if you are better off renting or buying.

For the young families that decide to keep renting, it costs them 100k in earnings over two years.

Don't forget, they are avoiding paying interest on a mortgage in that time.

Some napkin math:

- 100k over 2 years = $960 per week.

- A house renting out for $960 per week is worth, I dunno, maybe $1.2mil?

- 20% deposit = $240k (good luck) so we are paying interest on $960k

- 6% interest on $960k over 2 years = over $100k. Add on rates, insurance, maintenance and you're prob closer to $150k.

- If house prices decline a further 10%, we lose $120k in capital.

So we are now out of pocket $270k for buying now versus the foolish young couple who paid $100k renting. What was the point you were trying to make, exactly?

You can rent a 2 bed apartment in Devonport Peninsula for $630, homes value 1.6- 1.7M.

For $960 a week you can rent a $2M house easy.

You said this yesterday and were also wrong then. Why repeat it?

Oh gee what's happening in my absence. The cretins are about to mutiny.

700pw rent over two years means "100k in earnings" at an average tax rate of 28 percent.

A higher marginal tax rate of 33 or 39 percent will require even more gross earnings.

Its tough out there in the real world

Just checked my 60/40 portfolio which is down $110200 since Jan. I am still adding to this and if I wanted to I could sell some. So how do you do that with property (which I maintain is a utility NOT an investment)? How do I DCA in to a AKL residential house? How do I sell the sliding doors to the deck if I need $20k or so? Certainly the weak NZD has been helpful as most of my funds are US ETFs, however its all good news when unit prices fall (and in buy mode) yet when house prices fall its all shock horror. Well you've still got your house and likewise l've still got my units, but unlike you if I really needed a few $ I can sell a few units, good luck with putting that sliding door on trademe.

Just checked my 60/40 portfolio which is down $110200 since Jan

You've played a prudent game with the 60/40 based on the mainstream financial concensus. Unfortuantely, the 60/40 portfolio is now toast. It has been marketed to primarily boomers, but its use-by date has gone. People like yourself good sir have been sensible by adopting it. People do need to challenge the mainstream advice more. As we see now, things have been completely turned on their head.

Yes, I have read about the 60/40 pros and cons however my other half is not a risk taker so I think its prudent! The other number is the 4% rule, seems that is out in favour of the 3.3% rule, with that adjustment I've just got 2-3 years before I can wave goodbye to PAYE.

If i reflect on how many times over the last couple of decades I've heard on the evening news about property price increases, i can only assume this bear market will have a few years to run yet - bear markets typically run for 1/3 to 1/2 the duration of the preceding bull market. In addition, if we consider the global recession that is just starting (confirmed in Europe), food and energy crises thanks to war in the Ukraine and the global long term interest rate cycle, we could be in for a lost decade where property prices stagnate or keep falling in real terms (inflation adjusted). Very pleased i don't have much debt.

who thinks OCR goes up again on Nov 23rd? I'm picking another 50bps.

Could be higher than 0.5% in November, reason being the RBNZ do not meet again until Feb 2023 so unless they want an emergency meeting before then it will finally go that 1.0% jump.

Could be lower if rbnz listen to people

Rbnz always overplay their hand so am not expecting a backflip

Using the average to calculate a price drop is the lazy way to make a headline. To do the job properly each sector of the residential market needs to be analysed.

Drops in value for regular houses on good sections hold their prices far better than plaster homes on similar sections. Units vary tremendously depending on structure, size and the neighbourhood. Apartments also vary a great deal with luxury examples selling for mega dollars, while dog boxes sell close to zero. Houses in the areas where the deserving poor dwell tend to drop further than those where the well to do reside. Produce these figures and we will be better able to see where losses are the greatest and where the tea cups are hardly tinkled.

You're right about the apartments. We almost bought one at the low end just for fun. Freehold and for very little. In the end I was wondering about whether it was worth the hassle, so sidestepped it.

If someone had time to mirror the Case-Shiller index methodology here,in NZ, same house reselling ,unimproved,across all markets,that would be far more precise.

It's bound to have a few years more declines in it. We will need to look at the next article that breaks down the total mortgage book ,into 1,2,3, and 3 years plus fixed rate mortgage percentages and floating rate percentages,to get an accurate depiction of when and how much ,debt is pricing higher,and by how much higher Then there is a lag between when the newly increased mortgage payments really chew through any household budgetary slack and any other savings buffers. And a further lag as stressed mortgage payers try to wangle a non- disastrous exit. That's a very long unwind. Peak mortgage stress ,driving selling decisions might be 2 more winters away from now. Accelerated by a recessionary jobs market ,if that also happens . I can't recall GFC crunch really biting until 2010/2011, and this reset is looking bigger and deeper. Could be as long as 3 years to a bottom turn. I am reading a lot of wishful thinking here,that it will be a lot earlier ,a lot milder. Lending statistics need to be looked at,for real conclusions.

Agree with you jimmyH. I have come to a very similar hypothesis.

That is how I would see it, if I could write half as well. Exactamundo dude. Mmmm beer. Long decline and a longer plateau for me, it was such a high ride up, hope some people have seat belts on it's going to be a ride down.

https://www.rnz.co.nz/news/business/476563/national-average-house-price…

The article mentions that home owners who bought last year will have a bad time when they sell but FHB, who bought recently, why would they sell (if any, percentage will be very minimum) and those selling are Flippers/ speculators, so are more concerned as who loses in casino and that too many speculators over last few years must have made tons and knew that will be stuck in last but overall are still in plus.

It has just started. The real fun is going to be next year. Remember that housing is a relatively "illiquid" market and it takes time for it to adjust to changed circumstances.

...if you borrow at 1% you can suddenly ‘‘afford’’ a $500,000 house - you can quickly become ‘‘wealthier’’ even though your salary or ability to generate long-term cash flows hasn’t changed! Here is a list of the top 20 countries for total (private + govt) debt as % of GDP. Link

Comparing September values with January values is silly, either you compare the same month from a year ago to see a long term trend or you compare to the previous month to see the most recent direction of the market, but picking a different month makes no sense apart from trying to sensationalise a headline.

It's (edit) not silly. It's showing fall from peak and shows velocity of fall.

I didn't say you were silly.

So did we compare the change of value from the all time low on the way up? Did we compare today's house values to the ones 30 years ago? No we didn't

People were comparing today's home values to 30 years ago all the time on the way up.

Yes they were.

Plus it's also useful to measure from certain points when a trend changes direction YOY is just as arbitrary as 7 months ago in some ways.

Exactly. We want to know about the data for the current trend, not the trend that preceded it.

Anyone who wants to include historical price rise data into current falling trend data is just trying to obfuscate.

Sorry that was a typo, was supposed to say It's not silly". Corrected now

And running parallel to this is the worry that on the TV program 'The Block,' contestants were not making any money.

Great TV I say, The look on their faces. Priceless. The TV company couldn't even fake a good outcome.

To paraphrase the great building philosopher, Gnarls Barkley, 'Bless their soul, they think they are in control'

If there was ever a lesson to be learnt about building and the human condition, it's that program, but not the lesson everyone is taking from it.

And running parallel to this is the worry that on the TV program 'The Block,' contestants were not making any money.

The Block will disappear from the screens. Attention to this kind of entertainment content was so predictable during the uber-bubble.

Bloodbath here also across the ditch.

I was looking at an apartment in Pagewood here in Sydney, 3br, 2 carparks on the 12th floor with view across the city. It was listed and sold last year for 1.75m, now on the market again for 1.405m..

I was looking at an apartment in Pagewood here in Sydney, 3br, 2 carparks on the 12th floor with view across the city. It was listed and sold last year for 1.75m, now on the market again for 1.405m..

Problem is that these kind of places are common in Sydney. All with price tags that don't make any sense in the current and future economic climates. Places like Sydney are potential Ground Zeros for a property crash.

In Sydney houses are beyond the dream of many FHB or middle class earners... Apartments is only possible solution!

Unless one willing to sit on public transport for 2 hours!

In Sydney houses are beyond the dream of many FHB or middle class earners... Apartments is only possible solution!

They're running out of tricks to keep the charade up Chairman. Disruptions to the steady flow of lucre out of China isn't helping.

Kia Ora Chairman,

I'm familiar with that area of Sydney, although i'm in NZ now. I recently stopped in Sydney on a connecting flight. Coming in to land, I couldn't believe the amount of multistory development in the suburbs between the CBD and the airport. Zetland went years ago but the rest are just chock-a-block (pardon the pun) full of unit blocks. The population increase must be significant. The traffic was horrific in the early 2000's, I can't imagine what it's like now.

Try Wellington, some better prices down there, if you can cope with the weather, and don’t mind a high maintainable house ….. oh and maybe a walk up or down to your home.

https://homes.co.nz/address/wellington/wadestown/25-wilton-road/MkpNB

Maintenance

My last two flats in Wellington were at Devon street (Aro Valley) and then Bolton Street..bloody steep streets to walk home!

A house just down the road was sold 8/9 years ago for $279k.

Now on the market for $715k.

Owner very enthusiastic,no sign of concern from him about falling prices.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.