The housing market had a disastrous start to spring this year with the lowest number of sales in September for 12 years.

According to the Real Estate Institute of NZ, 4943 residential properties were sold throughout the country in September, down 10.9% compared to September last year.

In Auckland sales were down 15.8% compared to a year ago and in the rest of the country excluding Auckland sales were down 20.0%.

The last times sales were below 5000 in the month of September was 2010.

Prices also continued to slide.

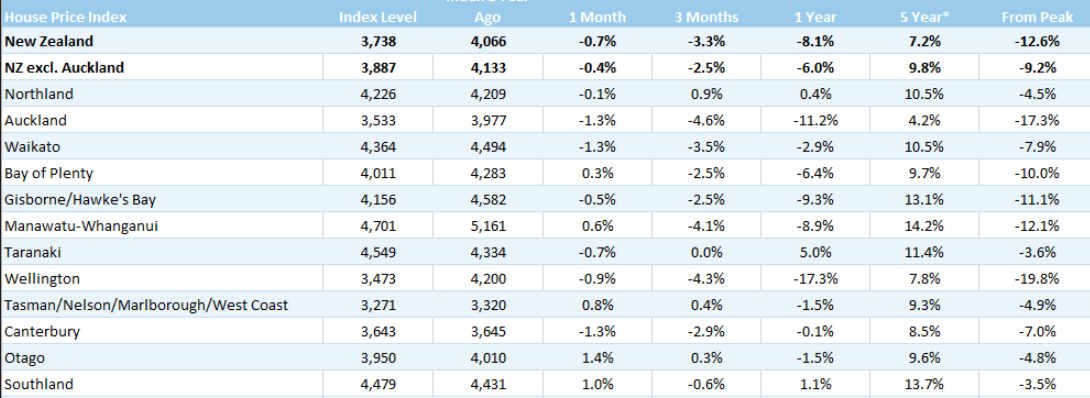

The REINZ House Price Index (HPI) , which adjusts for differences in the mix of properties sold each month, was down 0.7% nationally in September compared to August and is now down 12.6% from its peak.

In Auckland the HPI declined 1.3% in September and is now down 17.3% from its peak.

The HPI for the Wellington Region was down 0.9% in September and -19.8% from its peak, while the Canterbury HPI was down 1.3% for the month and is now down 7.0% from its peak (the HPI table below shows the trends in all regions).

However the national median house price rose slightly in September, to $811,000 from from $800,000 in August (+1.4%)

The fact that the median price rose while the HPI declined suggests there was a change in the mix of properties being sold, with properties in the upper price brackets selling more readily than those at the lower end.

Properties are also staying on the market for longer, with the median days to sell rising to 47 in September which was 10 days more than in September last year.

"Following an exceptional period of growth last year, spurred by government stimulus and closed borders seeing Kiwis invest locally, the property market is moderating," REINZ Chief Executive Jen Baird said.

"Owner-occupiers remain a strong buyer pool and agents in some areas report seeing more first home buyers, enticed by easing prices and less competition.

"However property prices are still unaffordable to many, particularly in larger hubs such as Auckland and Wellington.

"Agents also report seeing an increase in open home and auction attendance, which we would expect to see as we move into the warmer months.

"However, the September data, and reports from agents, indicates that the expected spring uplift is not as strong as anticipated," she said.

The comment stream on this article is now closed.

REINZ House Price Index - September 2022

Volumes sold - REINZ

Select chart tabs

Median price - REINZ

Select chart tabs

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

256 Comments

HPI reporting the day of! What a treat

Yes, thanks Greg!

Housing market on it's knees, praying and begging for it to be resurrected..

The dice is now slipping down the snake

Where's Nikki " Propeller Investments " Conner when you need her ... she'll explain that there are only ladders ... no property snakes ... up 100 % every 7 years ... ohhhh yessss...

Richard withy Raywhite

Does anyone know what the max peak to trough nationwide decline in the REINZ HPI was during the GFC? I seem to recall it being 14-15% but it would be good to know for future reference.......

https://www.interest.co.nz/charts/real-estate/median-price-reinz

$355K Nov 2007 peak

$320K Jan 2009 bottom

Thanks - but isn't that just the 'crude' median? Not the actual HPI value?

There was no HPI back then

HPI reporting the day of!

AdamJay, what does that mean? I see many readers like your comment, but I just don't understand what your sentence means, can you please explain?

Historically interest.co.nz has reported the REINZ property data the day of release, but waited until the next day to report on HPI, even though they're both released at the same time. This month we seem to be getting both at once.

Reporting of the HPI on the day of the release. Unlike how it has previously been reported the next day.

Hence abbreviated ‘day of’.

Imagine how much worse this is going to get when retail rates catch up with swaps. I don't know how they're still offering 1 year fixed at ~5.4 with 1 year swaps at ~4.75, but I can't imagine that situation is going to last. Must be a combination of low volumes + FLP.

They borrowed a load of money from FLP then found that they could not sign up enough new greater fools so will take a while to clear it.

I tend to agree. Which is to say: it won't last.

I think that's demonstrably wrong. According to RBNZ there is a total $15bn drawn and RBNZ c-30 says there is $17bn in new loans over the last quarter alone....

I imagine the main reason is competition, which is also keeping deposit rates down to offset the low home loan rates

That's still a good chunk of funding, even if not the lot. Clearly it would reduce their need to raise elsewhere in a meaningful way.

Debatable. It launched in December 2020, since that time there was $156bn in new lending, so less than 10% of that. Given NZers fix short, almost all of the ~$300bn in stock will have repriced since then.

It's also more likely FLP is used for floating type loans (<10% of the market) as opposed to fixed rates, since they'll want to have a swap in place for the fixed.

It reduces the blended rate that the banks are borrowing at. It isn't the only source of their borrowing.

I assume that as well as private term deposit growth, there will be money coming into banks from kiwisaver. Whether they really want it or not. Maybe they don't want it and that is why my Kiwisaver cash fund doesn't even pay what a private term deposit does.

‘The Property market is moderating’

Humour Gold!!!!

To misquote Paul Keating - this is the correction we had to have.

The word 'moderating' is not alarmist. Has the ol' Goldilocks "not too hot, not too cold" vibe about it. Useful if you don't want to scare people.

Reminds me of a bit I heard once on The Fresh Prince of Bel Air.

Big Phil's learning to dance, and talks about "shakin' his groove thang". Watching on, Geoffrey the butler quips:

If that's a groove, the Grand Canyon's a ditch...

Yo this is a story all about how, the HPI got flip-turned upside down. 🎵

Meanwhile over on stuff

"House prices inch up between August and September, Real Estate Institute data shows"

Haha

Hard to understand their agenda. Typical wokesters

They're paid by the RE industry to promote... that's their agenda.

Yep just another capitalist enterprise, despite their facade

From the article:

"The market has moved the other way and the scales have tipped so that supply outweighs demand. In this market, while we are still seeing a good rate of sales, they tend to be slower.”

But I thought there was a shortage of housing?

In which case how could the demand / supply relationship change without a huge source of supply (given one would expect demand must to hold up for a basic necessity if there is a shortage of it....)?

Is it perhaps possible that this ("big reveal" coming) has all just been a function of loose credit conditions?

But "deficits don't matter", mumble, mumble, "lockdowns are good for our economy" mutter mutter "inflation is transitory" mumble mumble MMT something, something.

Stuff is by nature biased as it provides paid advertsing. It needs to positively promote the housing market as thats where most of its revenue comes from.....and dont even start me on the Herald.

30% Crash In Home Prices by December, it's a Certainty .

Within Auckland, six of the seven territorial authorities had annual price decreases, with the North Shore’s the largest at 28.6% (to $949,000).

Prices were down annually in seven of the region’s eight territorial authorities, but South Wairarapa’s dropped the most with a 27.5% fall (to $700,000).

https://www.stuff.co.nz/life-style/homed/real-estate/130137138/house-pr…

30% Crash In Home Prices by December, it's a Certainty .

That's a mighty dent in the wealth effect to think I'm down $200-300K in a single year. If the wealth effect exists. I think Kaumatua Orr and Robbo are sceptical that it does. Only time will tell.

If you only own one house and can afford the mortgage, no big deal. You still have 1 house.

If you have multiple houses with decent leverage...I guess we pray for you?

If you only own one house and can afford the mortgage, no big deal. You still have 1 house.

This is not the 'wealth effect.' The wealth effect is the phenomenon by which consumption behavior is influenced / moderated depending on things like changes in asset prices. During asset price bubbles, many people will spend today rather than save for tomorrow. When bubbles subside, people are more likely to not take the winter holiday to Fiji or Queenie because they are more sensitive to their financial situation. As you can imagine, asset price bubbles are good for govts, banks, and the wider consumer economy.

The wealth effect is folk living it up confident that ultimately the next generations can pay the bills instead.

Coming to the tail end of that very generation. The one that voted against communist policies such as saving for your own retirement, and voted for policies that gave housing ponzi like characteristics.

REITS are multiple property owners with leverage. I think they're doing fine so your prayers have been effective.

NZ REITs have pretty gentle leverage, usually around 30% level. KPG are the one I follow most closely, they recently announced a ~9% reduction in NTA and the share price has fallen close to 50% from the pre-Covid highs.

Justifies a few prayers, if you invested a few years ago.

Individual investors who are more highly leveraged and lack KPGs diversity in income and interest rate hedging abilities could end up in much worse positions.

I should add, most NZ REITs are trading at a 20-30% discount to their reported NTAs. This could be seen as the markets expectations of how far their NTAs still have to fall.

I don't see why a leveraged residential property portfolio should be expected to do any better - possibly worse as the yields are so much lower. If it is operated with more than ~30% leveraged the results could be much worse.

Eh? Can you enlighten me how a 9 percent drop in NTA (equity) can translate to a 50 percent fall in capitalisation value. Either high interest rates, increasing overheads or flat to falling incomes (covid is over, so should not be less income). Commercial investments generally priced on net income, a lower shareprice makes sense but not as low as that.

Good question - personally I think the drop in share price is overdone and have been buying. But the fact is, the market thinks that a moderately leveraged portfolio of industrial and/or commercial properties is worth something like 30-50% less than it was just before Covid. It would be quite reasonable to see similar falls in residential portfolios once that market catches up.

Higher interest rates mean higher expenses so lower income, and the market also expects higher yield than previously to compete with rising bond rates. Income hasn't really been affected yet give or take the odd lockdown effect which is now fading away.

The wealth effect has been proven to be a fallacy, according to a bunch of analysis done after the UK proposed, then scrapped, their tax cuts.

"Irrespective of the source, spending unrealised gains is never a good idea."

Robert Shiller's work would suggest the wealth effect is real.

Well, it might not be what you want to hear but it's true, Greg says so too in the article above:

the national median house price rose slightly in September, to $811,000 from from $800,000 in August (+1.4%)

Awaits bank economists to update their predictions...

I don’t think ANZ updated theirs after revising upwards their OCR forecast to 4.75?

TA’s forecast of +5% for 2022 is looking worse by the month.

They will revise lower and point to higher rates and a worsening global economic situation...

Hell even JP Morgan CEO: Stocks Could Fall Another 20%...

By revisiing lower they probably help with clearance, by being someone you can trust with advice

rather then us DGMs on interest.co.nz, seems we are right this time, and if you had to choose one time to be right.....

Looking at the CAPE10 ratio, stocks could fall 50% from here. Housing also.

30% Crash In Home Prices by December, it's a Certainty. Will Wellington be the Winner ???

Auckland prices are down 30% in real terms... surely it can't go much lower.

What's stopping it? Building supply is still cranking and interest rates still rising. Nowhere close to an attractive yield for investors, especially if you need a mortgage.

At some point- maybe after another 5% of falls - buying will start looking more attractive to more people, especially if people understand higher interest rates won’t be permanent.

Why do you think they won't be permanent? Because inflation is transitory?

Yes.

I think high inflation is transitory. I think within 2 years we will be back to 2-3% as the norm.

obvious caveats apply - volatile, uncertain times etc etc

I think high inflation is transitory. I think within 2 years we will be back to 2-3% as the norm.

Back to normal ya reckon

Looking back a couple of decades we are only just getting back to normal.

https://www.interest.co.nz/charts/interest-rates/fixed-mortgage-rates

"Normal" is a downward trend.

https://d3fy651gv2fhd3.cloudfront.net/embed/?s=nzocrs&v=202210050145V20…

Care to add some context about why there has been a downward trend?

Trends don’t emerge out of thin air, trends begin and change with antecedents and structural changes.

I'm not doubting that. Just pointing out that "normal" over most people's lifetimes has been a downward trend, not a fixed number like 6% as mfd implies.

That is fair. The trend is strongly linked to the high house price inflation over the last few decades - the 'house prices double every X years' mantra.

For both trends to continue, looks like we would need negative interest rates before long.

Using the term “normal” in economic discussions is just introducing another bias.

Why should a trend that lasted our lifetimes somehow imply future longevity? Especially when the previous trend has clear antecedents that are now abating. We all assumed that infectious diseases were done after a multi-decade long trend that suggested that… and now they are on the rise again. Things changed, people lost faith in vaccines and governments.

In terms of financial trends, a huge piece of research was done by Thomas Piketty and published in “Capital in the 21st century”. I can’t remember the exact figure, but the return on capital was stable for centuries at around 4%. Hence why in literature authors refer to how much someone had per year when they didn’t earn a salary. This was because the 4% return return on capital was just that stable year in, year out, until death.

That was a much more enduring trend than the one you refer to and yet we’ve not seen that kind of stability in decades.

Why is that? Why did that change? These are the questions that we should be asking.

The long term trend you refer to was an anomaly over the longer term course of human history.

It’s every bit as much an example of recency bias as the ancients referring to Rome as “The Eternal City”. Every highly globalised economy humanity has created has eventually collapsed. The Rome economy collapsed . The Bronze Age economy collapsed. The Muslim and/or Silk Road economies collapsed. They were unsustainable, just as the modern globalised economy is. We talk now about “uncoupling”, “localisation” and “withdrawing from globalisation”. That is the important trend to watch. Post-industrial globalised trade is what created the current global economic system and underpinned its giant behemoth of a debt system. If we are withdrawing from that, then the trend is reversing. The debt cannot be repaid. And at some point, if it becomes apparent that the debt cannot be repaid then the whole house of cards will collapse. Could be now, could be in another decade or two, hard to know, but if we are really returning to more localised economies, the whole structure of economics will change. Population growth has been in decline for decades and this matches the decline in economic growth, another factor that is rarely mentioned but a very obvious and major trend.

Again I'm not refuting that. I didn't introduce the term normal in this comment stream. My issue is with the many posters writing "back to normal" and stating or implying an interest rate of 6 or 7 %. What I'm really saying is that there is no normal that we can fall back on so it's best not to make such comments. If someone feels they really have to use that term then they should at least acknowledge the trend over our lifetimes, which may or may not be at an end.

Yes. And I am not alone. But time will tell.

You think high inflation will persist beyond the next 1-2 years?

I'm worried we're facing a much bigger problem than just a housing market collapse. I'm worried NZ's housing bubble is just a symptom of a worldwide issue. I'm worried we could be facing a collapse of the whole system of money.

If some clever guys here can quell my fears I'd appreciate it.

Some fear is good. Personally, I'm hedging with gold and US$ denominated shares. Some people like crypto. IMHO, if the shtf, then the US$ and physical, tangible, assets that you can hold in your hands are still the safest places to be, especially compared to NZ$.

Probably can't go wrong buying canned beans.

I think the first step is to fabricate a plough.

Procure seedlings or seeds.

Next step is a water supply.

Onwards and upwards until you can make semi conductors.

I'm off to punch trees and build a crafting table. Those are the skills of my generation.

BYO nuclear power plant?

. . sure thing : I'll quell your fears ...

1 : turn off your internet ...

2 : keep calm ... carry on ...

. . you're welcome 🙂

So true Gummy, just stay off YouTube at the moment, every other video has the world ending in the next 2 weeks.

Many governments have been developing CBDCs. They've been in the works for a while now. But the regular person is unaware. You'll probably only know if you closely follow crypto.

They may be anticipating the failure of fiat.

Yeah, I think that is right - the old switchero to CBDCs from fiat that nobody trusts any longer.

And they have also been quietly marketing them as secure, convenient etc. - i.e. features we largely already have or improvements that don't matter much. They never reveal their plans on what matters - how quickly they will debase the shit out of them, which is why CBDCs will be just more of the same old sovereign theft.

Some people believe they are intentionally trying to crash the current Fiat system so they can move to a CBDC.

2-3% rates were historically unprecedented lows. 4-5% is the historical norm for what are considered low-normal rates. There is basically no chance, absent another giant calamity on the scale of a global pandemic, that we see interest rates in the 2-3% range again.

And don't forget the talk that central banks might decide that what they really want is 4% inflation, not 2%. In which case, higher nominal rates.

So how long is "transitory" to your mind?

1 year? 3?

Because this doesn't seem very transitory it feels high and sticky.

More people competing for renewables, electrification and carbon offsets......

@ house mouse

I think …

I think…

In other words you don’t really know , just stating an uneducated guess.

Well, it was a comment about the future. Nothing is provable.

At some point, yes. The potential buyers do of course need to be able to navigate a year or two of high interest rates (best case), and to convince the banks that they can.

I think there is a reasonable chance the falls will be more than 5% from here.

Yes but the wont be higher for a long time indicates dire economic situation ahead.... fiscally we cant keep spending money like

a drunk bnavvy on shore leave.... so even if things turn bad and rates drop dont expect National to try a economically stimulate NZ like Labour did. On that basis what exactly makes leaky could old high maintenance housing look like an attratctive investment vs carbon sequestrian or innovation in agriculture or other vehicles via stock market etc???

I have a gut feeling that this coming recession will be much longer then we think it will be, China no longer wants to play in our sandpit nicely.

Housemouse,

The only thing that is even remotely predictable about crashes is the psychology of them, which there is good data on. We haven’t hit the capitulation phase yet I don’t think and typically, smart money doesn’t buy back in until the worst of the crash is quite obviously over (and whilst everyone else is still reeling and freaking out). We are very, very far from that IMO. We haven’t even had any kind of plateau in the price depreciation yet, let alone capitulation.

Your suggestion implies and assumes rationality. The price appreciation wasn’t rational. The price depreciation never ever is.

GFC- Bottom of market occurred 15months after 2007 peak. Do you think that it will be about the same timeframe which would be early next year

The OCR before GFC was 8%. After GFC 2.5%.

Look at the graphs - we have barely dropped to 2021 prices. I would like to see the graph drop to 2017 and then the RBNZ bring in DTI. That way we can dislocate the property market from the effects that the OCR has on it as an asset class.

Correct still not down to the Feb 2022 which was supposed to be the July 2021 RV as yet here in Tauranga. Still see a bit of downward movement till Christmas then a holding pattern. The gains were so huge its just blowing the foam off the top.

I'm not sure how introducing DTI after price drops makes any difference. Incomes are going up - not down, so any DTI introduced will mean that any amount that can be borrowed will be increasing over time with wage inflation. Not connected to house prices dropping.

DTIs would have likely stopped the market insanity we saw a year or two ago by providing a cap to lending when interest rates plummeted. It's a tragedy we didn't get our act together and get this in place.

Hopefully we can get it in place before the next bout of insanity. The happy side effect is hobbling multiple property investors relying on leverage to build a portfolio.

That entirely depends on where the DTI is set. A DTI of 4 is out of the question practically but just run the numbers on Auckland median house prices and see what income you'd need and then tell me it wouldn't have a large impact.

It’s the best time to introduce it. Has no immediate effect but if prices ever start raising it will keep them in check.

I agree re the graphs..caughtinthemiddle..what are they trying to achieve with these dramatic headlines? We all know the story...house price increases were out of hand in NZ and did need to abate, just lets hope they don't drop so much many are hurt in the process. Drop to 2017 prices?...sorry think that will hurt too many.

As far as sales go...it's weird, I live in an old inner Auckland city area (western fringes) and houses that come on the market here do not seem to last long before they sell.

I dont think the slice of the market you're talking about is being impacted as much? People who were ready to spend 3-4 mil on a house yesterday will still probably ok with doing it tomorrow?

The fact that the median price rose while the HPI declined suggests there was a change in the mix of properties being sold, with properties in the upper price brackets selling more readily than those at the lower end.

That's not surprising at all - and exactly what I've been saying here the last few months. The top-end of the housing market remains relatively buoyant.

Notably, however, there are very few houses currently listed in certain up-market suburbs such as Ponsonby, Freemans Bay, St Marys Bay and Herne Bay (in Auckland). Similarly, in the desirable Wellington suburbs of Kelburn, Brooklyn and Mt Victoria, houses suitable for higher-income families are as difficult to find as ever - just ask anyone who's looking. Furthermore, many such houses continue to sell for premium prices - with new records not uncommon.

TTP

So as long as everyone lives in these suburbs, we'll all be fine.

But you would expect the top end to be the last sector of the market to be hit would you not?

And if the top end is all that's holding the market up doesn't that imply weakness not strength?

Go hard Tim. In a democracy, isn't it great that when a Property Broker chooses to marginalise themselves through deceptive behaviors, they can still voice their opinions in a public forum.

Let's celebrate😢

Hi Crash Crusader (aka Retired-Poppy),

Being so twisted/crooked, I assume you'll celebrate in your usual manner - swallow a nail and sh*t a corkscrew.

Trust you're not too constipated today.

TTP

I hope Retired-Poppy's guts are flowing freely downwards, like the property prices

Tim, you really are a one hit wonder. Same joke but different day. I am chuckling the second time for a different reason 😆

My diet is rich in fibre so nails just sharpin my teeth😁

Expect Property Brokers to be Advertising on the Radio how Prices are going up. They have actually been doing this lately. No Joke.

On ya TTP

The top-end of the housing market remains relatively buoyant.

https://www.corelogic.co.nz/our-data/mapping-the-market :

Over the past three months, 97% of Auckland suburbs have seen their median property value drop (or 194 out of 201). Almost 180 of those saw falls of at least 1%, and in 14 suburbs, the drops were 5% or more. Suburbs with >5% drops included Glen Eden, Papatoetoe, Henderson, and Panmure.

The falls over the past three months topped $100,000 in seven Auckland suburbs, all of them ‘upper end’ areas (median value at least $2m) – including Omaha, Shamrock Park, Onetangi, Palm Beach, Herne Bay, Oneroa, and Orakei.

I keep track of the Bank’s regularly updated value of my home in Aucklands inner East.

Since the November 2021 high, I’m down $470,000 or 14%.

I am still 5% up on the 31/12/20 value and 21% up on the 31/12/19 value.

It is not really a crash in my mind until we erase the pandemic.period gains. Bring it on, if it ensures JA is toast.

The bank has our place down 12% since our purchase price in December in Masterton.

Stop it with your bloody facts, Tim is trying to sell a story here, facts kill the fairytale magic

What makes a home "suitable for higher-income families"

A lack of toxic mold? The ability to retain heat? Dry inside when its raining outside?

You are missing quite a few of Wellington’s desirable suburbs . And Brooklyn doesn’t mix in with the two you are quoting

Ouchy ouch

With rates and inflation raising house prices will continue to fall, the big problem is Auckland and some other areas are still 10 x average couples income. For market to find a bottom price’s would have to reduce another 40% .

And that would just be to return to the long term average. It would be unusual indeed if this crash resulted simply in mean reversion, when almost every other crash in any asset class has sunk below the mean.

For market to find a bottom price’s would have to reduce another 40%

And then some.

We're beating the Irish. Guinness World Records application worth considering perhaps😱

The most house prices can fall in the shortest time!

Interest rates haven't even peaked yet!

Reverend Retired Poppy - thats correct. Interest rates have got a Long way to go up yet. And stay up.

As The Prophet has said in the Scroll.

10% Interest Rates Next Year, Guaranteed !

In fact, Future, the banks have become very tardy with increasing interest rates following OCR increases.

And the tight labour market means the vast majority of mortgagors can continue on....... Mortgagee sales are very rare indeed.

Also, financiers (banks and first-tier lenders) continue to be not just solvent - but prosperous - with no sign at all of failures as far as I'm aware.

There's a reasonable prospect that the downturn will bottom-out next year - perhaps as early as early/mid 2023.

Those who stocked up with popcorn will be particularly disappointed.

TTP

Honestly, for all our sake, I hope you are right.

I just don't know how you can be right.

Ya dreaming! Come back when you realise it's a nightmare,

Some of us just really like popcorn. No ragrets.

In a world of fast declining equity, there will be less fat to prevent an inevitable rise in mortgagee sales. It's an indicator that will become more obvious soon enough. Coming job losses will also contribute. Those looking forward to interest rates coming down again need to accept this is as a sad reality. Reducing inflation to 1-3% range will cost the heavily indebted dearly.

Your comments are correct. Lets add more depth and ask why...?

Banks are able to ignore the OCR and depositors returns, because of FLP which is lent at .25% to the banks by the RBNZ. Accordingly the banks don't need to value deposits - thanks again Mr Orr. This is due to expire in 6 December 2022. I would also note that in a recession businesses have only one lever they can pull - to shed staff. Accordingly exposure to the true rate of debt, and its impact fueling unemployment is just around the corner.

2023 has all the elements to Tank The Ponzi.

Popcorn.

FLP is lent at the current OCR not previous

New FLP ends in December 2022, then the tranches need repaying when they get to 3yrs I think. The rate is NOT 0.25%, it's OCR. And since it goes up, banks are unlikely to be using this to fund fixed rate mortgages. The $15bn too is pretty small in comparison to the whole market, so while it does have a dilution effect on funding costs, it's certainly not the biggest lever.

Who had the graph they were running with HPI adjustments for NZ vs IRE/US/Spain/Japan? Miguel? Be good to see an updated version.

has he been banned for posting better info then interest does?

One scenario is its starting to look like the low end speculator tax loss box is in trouble. People appear to cashing them up and redirecting into high end mansions. Would not want to be long on low end specu boxes on this with 2-3% fixed rates hoping to ride it out listening to Ashley saying how great everything is. Going to be a very tough year until the election.

Stash 1 mil cash to buy another 5 freeholds in 2023.

"Stash a million cash" That's cold comfort to skittery property speculators overloaded with an illiquid investment. It's frustrating when those fast evaporating gains cannot be locked in and banked😭

At least that’s an option here.

Of course not possible in your beloved, authoritarian homeland.

Correct me if I'm wrong , but isn't the PRC having a property bloodbath right now ... in between extended Covid19 lockdowns ...

Auckland HPI showing falls of close to $4,700 per week now. NZ wide HPI showing falls of around $1,700 per week.

(Rough calculations - taking average house price and subtracting 1.3% for Auckland, 0.7% for NZ)

This takes some of the bitter sting out of the $720/week exorbitant rent that we are paying. Despite years of government and RBNZ policy to hold renter's heads under the water, keep them poor and bleed them dry at every opportunity, the vampire squids are finally weakening.

With any luck this correction will bring decent, affordable, liveable rents back to New Zealand.

Record low Sept sales says it all, there are just no buyers at these levels, not even people wanting to make conditional offers to move homes....

Unless of course you bought a house 2 years ago now before prices went nuts and also saved yourself $100K in rent.

Good on you if you just own one house to live in. You'll be OK, even if values drop, you still have a home.

My beef is with the rentier culture, and all the vampire squids who charge $700++ a week rent, bleeding Kiwi families dry with their greedy, overindebted, rentier ways.

It is an embedded part of the Kiwi psyche. Kiwis need to look down on renters because it makes them feel good. They like to believe that landlords are "hardworking" "winners" who are "getting ahead".

Watch for a collective dropping of the guts when people realize that their people farming, rentier, ways are making them POORER by the minute.

Vampire squids are so 2021. Can't wait till rents start dropping.

Unless of course you bought a house 1 year ago and now have negative equity,a depreciating asset and ever increasing mortgage costs.

NZ average weekly rent is $530. Most renters wouldn't be paying anything like $100k over 2 years.

Rent is pretty much over $700 a week now in places you actually want to live. You pretty much need to earn $100K gross in 2 years to pay for that. Rent is now almost sucking the entire average take home wage of one person a year.

You pretty much need to earn $100K gross

That's not what you said though and you know it, stop being silly.

Earn 100k, income tax 25k kss 8k, take home 67k, pay the landlord over 36k. Earn 48k to pay rent of 36k. Some people just do not want to understand Carlos

I am glad for my few mates who don't mind me staying. Would love my own house as do not want to be still flatting like retired poppy

😆 You're confusing me with Tim who rents. Weak attempt at a Troll "Low Fly" 🐝

What a simplistic and misleading statement. Rent costs are often split between couples, or amongst flatmates.

for example, My son earns about 85k, and pays about $250 per week for a bedroom in a nice Epsom townhouse.

OK for young ones who want to flat. The situation is dire for anyone who is trying to raise a family. Rents are far too high.

Your son is a good earner. But teachers and petrol station attendants and cleaners and factory workers are people too. They also deserve to live in their home country in an affordable, decent home... and to be able to afford to raise children with a decent standard of living. Impossible with current rent levels.

Cost of renting isn’t usually the biggest issue, it’s when the place you are currently renting becomes no longer available and you have to move. Stressful if you have family and kids with established schools…etc.

Plus it costs to move house. Money down the drain (or GDP depending on your outlook)

Bullshit you need to pay $700. You can rent a decent waterfront 2 bed apartment for $630 on the Devonport Peninsula suburb right now. Homes valuation is $1.7M.

Correct, Auckland rents for a 3 bedroom house would average $600+/week, but even then its 3 years for about $100k of rent paid.

2 years ago isn't going to save NZ or the precious TGA market you constantly bang on about.

Keep puffing your chest out and enjoy it while you can, people will (and already are) saving 100's of thousands of dollars with more to come.

The ghost of Paul Volcker is on the warpath and NZ is just cannon fodder.

Saved a $100k in rent. Spent a $100k in interest servicing costs, rates, insurance, maintenance.

Net result. Zero.

IDK I've managed to keep myself in the same house over that time frame, the disruption and cost of moving, finding somewhere new to live, close to existing work or daycares/schools, doctors etc. May not be worth much to some but if you've been through it over and over again then it will be worth something to you.

That is a huge benefit.

We have moved 3 times in the last few years... it is expensive and unsettling... one landlord sold our house, then the next landlord was a grasping old bat with a filthy house with carpets from the 1980s. Finally found somewhere decent, but it's not easy. I don't know how other families survive. It is terrible for kids to have to keep moving schools... just because their parents are beholden to greedy, selfish, vampire squid rent seekers.

Friends of ours are fully employed renters in their 40s. Raising kids. 4 months ago they were forced to move (landlord wanted the house for family) so they uprooted their whole lives, moved the kids to new schools, went through all the cost and hassle of moving.... and then their new vampire squid landlord put their house on the market 🦑.

The greed and selfishness of renting to a family, then putting the house on the market! It is revolting. And it is normalized behavior in our society! That landlord clearly felt that they had a moral right to lure a family into that house, and then pull the rug on them. Our friends gave the finger to their landlords, gave notice, and quickly found a better rental just down the street. Their old rental will be sitting empty on the market. I hope it never sells. I hope their old 🦑 landlord goes bankrupt. That'll teach him.

Fitzgerald, we were the same. Moved on by landlords x3 in x3 years as each one sold out from under us. It destabilised our kids and their education every time. Our society considers that collateral damage of a property market party clearly. Children’s stability is less important than a specuvestor’s desire to cash out.

We purchased in 2019 and will not move again if we can avoid it.

Likewise. And more often than not the Landlord is trying to take a bite out of your bond for pre-existing damages on the way out.

People try to justify renting over home ownership due to the financial costs, yet people have no issue spending $100 - $200 per week more on petrol driving a car when they could get away with a moped.

That's the problem, landlords (not all but a lot of them) are not looking to house people, they are looking at a money making scheme, removing any empathy and human decency from what should be a mutually beneficial LONG TERM arrangement, and simply doing whatever is the least effort for them, and makes the most money regardless of the collateral damage. Now there are also lovely landlords who understand that a rental is a long term investment where it will pay off over time, sometimes they have to pay their own money into the mortgage to make mortgage payments meet, keep rents reasonable and long term they will be rewarded with long term happy tenants, less hassle and a paid off asset which yeilds mainly profit. I think anyone who bought in the last 2 years at exorbitant prices to be a landlord though will have massive payments to service and be looking only towards the money regardless

Well, they may be looking for the money, but they won't find any. Bahahahaha!

Could happen if the Landlord has low/nill debt. Most do not, so rent reductions would requires the Landlords debt servicing to reduce #nochance.

Accordingly the over leveraged rent reductions will only result from a mortgagee sale to an owner with less debt because Kiwis don't have it in their psyche to sell at a loss. So it becomes a bit of a Mexican standoff. NZ educated youth are voting with their feet to Aussie (less good renters). Eventually something has to give and the speculords are wound up by the banks chasing any remaining real equity #goodluck. After the fall out of 87, banks are scared to start a reality based mortgagee run, as everyone suddenly discovers how much the banks have suckered us all into being their little profit slaves by over paying/servicing/renting.

Warren Buffet: "The value of every business, the value of a farm, the value of an apartment, the value of any economic asset is 100% sensitive to interest rates. The higher interest rates are, the less that present value is going to be. Every business, whether it's Coca-Cola or Gillette or Wells Fargo — its intrinsic valuation is 100% sensitive to interest rates." (1994)

It will take time. And yes, it will take many vampire squid bankruptcies.

But I can now see a future NZ where houses cost half as much, and rents are substantially lower.

The govt will fight this outcome, of course, but will hopefully fail.

HPI showing falls of close to $4,700

HPI doesn't measure $, you're ill informed

Yes, that's why I added a disclaimer that it is a rough calculation only, and included the method.

Happy to see alternative numbers if anyone would care to calculate them.

"However, the September data, and reports from agents, indicates that the expected spring uplift is not as strong as anticipated," she said.

Who would have thought?

So is this officially a crash?

Its a soft landing, the hard one occurs next year

It's a hard soft landing. It will be followed by a hard hard soft landing.

Think of it like compass directions.

At least as long as industry insiders and moronic journos are running the narrative.

... I'm wondering if Tony Alexandar will revisit his prognostications , and offer up a less bullish outlook ...

Bears rule !

You can bet your bottom dollar Wellington is already below the -20% Crash Mark. Those numbers will be conservative at best. People on this site are already reporting values of their homes Crashing at -30% or more.

10% Interest Rates Next Year, Guaranteed.

we dont need higher rates the market is taking care of demand itself probably wise to stop now except NZD

The market is a cruel mistress, it does not care what you want.

... a "cruel mistress" you say ... like , a whip cracking leather clad dominatrix ? ... bring it on , ooooh yeah...

She is cruel, and seldom lubricates her dildo of consequence.

As long as the economy is in reasonable shape and unemployment is very low, there is no reason to not continue increasing interest rates in light of high levels of inflation. A crashing housing market is not a reason to stop unless it starts to affect financial stability. There’s no signs of that, yet.

Almost there for Auckland and Wellington, but to be fair they had the highest percentage gains on an already overpriced market so the higher you climb the harder you fall.

almost there ...lol .. what you smoking Carlos... ?

You guys must have missed the graph above, hardly a disaster as yet.

The vested interest brigade will deny its a crash, but yes its is one. Next year could very likely be a Property blood bath, especially if the Banks have to force capitulation on the it only goes up, interest only, stupidity they have been supporting.

Announce DTi already, and just get on with it....

Start a petition

Next year could be an all out nuclear war with no survivors but its just best to worry about what you can control. Property goes up, it goes down its a long game and once you own a house you don't actually worry about what it is currently worth, you just get on with it.....

The only homes we can afford right now within working distance are flats and apartments. Can you guarantee in some way that I won't have to live 30 years in an apartment?

No in the same way I cannot guarantee you will not get run over by a bus tomorrow, what's your point ? life doesn't come with 30 year guarantees.

That's pretty dumb. It means everyone who already owns gets the nice homes, while this generation has to make do with the scraps.

Well no, what you should do is just lower your expectations and buy what your parent's generation had. Oh wait, those properties are scarce. You'll have to ask them nicely if they will sell a piece of their rental stock for you to have as a home.

Now tell that to the recent buyer with a million dollar mortgage, a kid on the way and a re-fix at 7% on the way.

It's actually a little different these days. Especially for those that didn't heed the teachings of the prophet.

So is this officially a crash?

Officially a crash or bear market happens when there is a drop in value of at least 20%

Whose definition is this?

Stock market crash is typically rapid drops of over 10%

US housing market is generally accepted to have crashed in 2007-2009 and that was only 19% decline.

Bear market normally refers to stock market. Real estate declines are normally defined as property bubble popping.

It's a crash and is continuing to crash.

Crash is 20% or more.

When market falls by 20% or more it is officialy in crash territory.

Where is this definition from? 20% normally refers to bear market in stocks.

10% rapid decline is considered a crash.

So essentially there in Wellington and very nearly there in Auckland.

No. As long as we’re still above long term average it can only be considered a correction, although because prices got so far out of whack the correction still has far to go. Of course it’s possible, maybe likely, that prices keep falling below long term average…at which time it could be called a crash.

people have simply forgotten what should be normal

Given the significant global downturn underway, I don't think our economy has seen the worst of things yet. So likely property prices will fall further in 2023.

Good to see we agree Adam

Meanwhile the old dear next door and her tidy house in a great location sits idle after months - unable now to settle on her rest home apartment.

Sold your Rymans/Somerset shares yet folks?

My neighbours is in a similar chain in Waikato and has just pulled out of the deal with the retirement village as their buyer hasn't sold.

The retirement villages are going to have to cut their prices to get customers in - shouldn't be a problem, they were quick enough to put them up when the property market took off.

Except isn't a lot of their profit numbers at retirement complexes based on revaluing their properties higher each year?

yes these are the fourth D.... preDeath but has to sell

My parents are in the opposite situation where my mums mother passed away and no boomers can buy the apartment (Oceania Retirement) as potential buyers of the retirement apartment cant sell their house to get the cash to buy.

Hmmm good take.

1 year fixed mortgage rates are back to levels last seen in 2014.

Maybe the old dear should sell her house at 2014 prices. Give another Kiwi family a chance at owning a nice home. There is always a buyer if the price is right.

Maybe the old dear didn't really earn or deserve massive capital gains, just for owning a house. Maybe she won't get them.

Don't worry - according to NZ's greatest economic minds, the house price falls will now instantly stop so there are no drops >20% this year.

This is so bad even TTP wont bother trying to spin it

He will. Just listen carefully to his Radio Advertisements. Property Brokers are already claiming the prices are going up. One of his agents told me the market " bottomed out months ago".

the poor chap is so uptight that if he swallowed a corkscrew he would s**t out a nail

By definition : a financial crash is the collapse of a long term speculative bubble ...

... the NZ property market is on the cliff edge of falling into " crash " territory ...

If Ardern's dopey anti-farming policies go through , the burp & fart tax ... that ought to be the shock to the system which will flow across the entire economy & boot the property market over the edge ...

Why so upset about house prices declining? isn't that what we need? Stop being greedy. Boomers are proving they quite selfish in general. Not the nicest generation.

... you've clearly nailed the wrong poster : I'm rejoicing house prices falling ... very very happy to see FHB's get houses , instead of speculators .

They say that you can't polish a turd .... but , you can sprinkle glitter on it .... which may explain why Ashley Church was last seen scurrying off to the $2 Shop ...

I had a south african boss who once showed me a picture of people living in mud huts in Africa, they put cow dung on the walls and then polish it.... so indeed you can polish turd

To bathe in glitter?

No surprise there

"the property market is moderating," REINZ Chief Executive Jen Baird said.

That's a new way of noting a decline. The NZD is 'moderating'. The S&P500, NASDAQ, Bitcoin etc are all 'moderating'.

I sure wish the word 'moderating' meant what she hoped for.

Their lips are moving.. they are lying...

None so stupid as to call a bottom though......

They know the bottom is in once clearance of overhanging stock starts to occur, but with these interest rates and a 7% test on new lending, they know the market HAS TOO fall further to clear...

Biased, not relevant.

A young family member has sold recently and are coming to stay pending finding a house. If they read this they might be staying a while and maybe not even need a mortgage to purchase again.

I wish we could annotate that Auckland price chart.

- This is where the editor got grumpy about comments pointing out that mOrrons are in charge at the RBNZ

- This is where Albert2020 lost his **** because wise people warned him that "only an idiot would buy now"

- This is where the cockroach formerly known as Printer8 was telling FHB it's a great time to buy

Etc etc...

I agree would could have stuck a note on there when you said you were leaving NZ, that would have been just after the note on the extinction of the Dinosaurs.

It may not reconcile with your "alternative facts", but I could also stick a note where I made the mistake of returning to New Zealand only last year.

Of course, it's okay to make mistakes, so long as one fails fast, and learns. It's better than a lifetime of being a slow puncture in Papamoa.

- this is where Adrian Orr said that rates will be "lower for longer".

- this is where the RBNZ told savers that they would need to "go further out on the risk curve" in the future.

This is where Yvil turned from a property bull to a property bear

This is where CWBW disappeared from Interest, either because he got trapped in his dungeon, or because even he realised his BS could no longer be sustained

This is where Tony Alexander predicted prices would rise 5% in 2022

And we could just put a sustained line running through time for TTP’s spruiking BS!!!

This is where RexPat uttered for the first of a million times "worst PM & Govt in living memory"...

Building up a head of steam as we head into election year. You haven’t seen anywhere near the end of that phrase being posted.

... worst PM / government & RBNZ guv'nor in living memory ...

As long as there is balance, no one could argue that the Nats have possibly been the "worst opposition in living memory..."

Labour under Goofy / Shearer / Cunliffe / Little / Ardern had 9 wilderness years ... and wasted them ... they were totally unprepared & gobsmacked when Winston Peter's anointed them in 2017 ... even now , 5 years later , they still look like rabbits caught in the headlights ...

Yes and the Muldoon years were so much fun..

... agreed ... he was a shocker ... but we did get hydro electricity out of those years ... and he ended up funny as a cut snake as the narrator in the live version of the Rocky Horror Picture Show ...

GBH,miracles can happen,so in 4 years we will see who is leading the Nats into the 2026 after their 9 years ;-) ;-)

I have noticed Nicola seems to be doing more of the talking these days...

The prophet appeared at the same time CWBW disappeared.

The saviour arrived as the dark (dungeon) lord departed…

I wonder how many retired people took their money out of the bank, and put it into funds and kiwisaver. I know someone who did, and they have now lost quite a lot of capital. They panicked and pulled it back out to prevent losing any more and put it back in the bank where they can get a reasonable interest rate. It is tragic. It almost feels a bit 2008ish.

We've found out that the RBNZ gives lousy investment advice.

- this is where THE MAN 2 something something Christchurch something something

"You make your money when you buy under true market value"

I'm sure the decline in house prices is just transitory.

Q. What are your houses worth today? A. What someone can/will pay you for them today.

If you don't like that answer then hopefully selling is not a necessity for you right now.

The last time the 1 year fixed mortgage rate was 6% was Aug 2014. The national median dwelling price then was 420k. Median 2014 annual income from wages and salaries was 45K. Current national median dwelling price is 810k. 93% increase since 2014. Median 2022 annual income from wages and salaries was 62K. 38% increase since 2014

‘The expected spring uplift is not as strong as anticipated’

Lol

In many ways I am glad TTP is a properties broker, rather than a medical specialist!

Imagine being examined for something terminal by Dr TTP. "That's not surprising at all - and exactly what I've been saying here the last few months. You will have completely no movement of your body but the top-end, i.e, your brain will remain relatively buoyant. You will live to a tender age of 98"...

"Your cancer is in remission, but with spring in the air we will no doubt return to growth imminently"

But despite that -- the old herald and Stuff are shouting out and spruiking still ! Unbelievable

stuff.co.nz/life-style/homed/real-estate/130137138/house-prices-inch-up-between-august-and-september-real-estate-institute-data-shows

Shameless.

Disgraceful things.

Very orderly. Nothing to see here. Interest rates have nothing to do with property prices! It's a shortage of land and high immigration!

Race between Wellington and Auckland towards 30% fall.

So far Wellington is winning but never underestimate Auckland as it can overtake Wellington, who know as it could be a tight finish though bets are in favour of Wellington winning the race.

Waitng to RE lobbyist - so called independent economist and media experts to yarn a positive story.

Not to forget that NZ$ to US$ is also racing towards 0.50cents.

Too much happening.

Rememenber that our reserve bank governor's can take solace in : “Nothing is permanent in this wicked world, not even our problems. - Charlie Chaplin”

They coined the world TRANSITORY INFLATION but forgot to define the period as transitory should have been one quarter or two quarter but now it seems could a year or two or who know a decade - keep it open for the experts to manipulate.

Do any of you "astute" property investors out there, watch the exchange rate of the NZ dollar ? ...and its downwards trajectory.

That 1.3 mil Mt Roskill damp, south facing ex state sh*tbox you bought in Sep 2020 cost you then in USD around 871,000 USD .......and now today, taking off the 17% decline your "palace" is now NZD 1,079,000 .....or wait for it - with the strengthening USD its now USD 602,000 ....or a 31% decline

The financial standard of living in NZ is now going to drop even quicker, thanks to a small, "brainwashed" , narrow minded, extremely greedy bunch of people ..... what a disgrace that the government has let it get this far, and now the "worm has turned" and we will see, maybe not today, but in the very near future many of this "over-leveraged" group in the financial "scheisse" !

The price bubble was self inflating because you could profit from it. However the deflation is also self driven.

Look for the prices to really drop as those who have to exit do. Sort of a reverse snowball effect.

It’s interesting how the stress testing banks used to calculate mortgage is now working against the Reserve Banks intentions. They will continue hiking until people can no longer pay their mortgages. But buyers were stress-tested at rates of 8 percent, so until these rates are reached, their hiking won’t reduce expenditure too much. What a ridiculous and heartless policy.

Buyers weren't stress tested at 8%, in 2020/2021 it was 6%+/-

So the cracks should start showing soon.

Building companies will be the next in row

My friend just sold his Rolleston entry level property for $100k over purchase price 1.5 years ago. I don’t see price coming down much

Interesting. I wouldn’t be surprised if Canterbury prices don’t drop too much, seems like there’s a quiet migration of folks moving there from other parts of the country (could be wrong).

Nelson also. Housing-wise the top end of the market still seems to be selling at silly prices but the middleground is losing value and vendors are dropping prices in the last 4 weeks

I hope house prices continue to fall. I would prefer the Christchurch City Council uses a lower capital figure for my rates than the artificially inflated price I have now. Better to take an extra $150 / month off the mortgage than give it to the CCC to waste. Prices would also have to slide a lot for me to have < 20% equity, so I'm not concerned about my mortgage repayments going up due to LEM being applied, although I hear some banks are waiving that.

C'mon. Rates are set based on relative valuations. If everyone's value slides, then you still pay the same rates. You only pay less / more if your value decreases / increases in relation to other houses (resp). If you really want that $150 reduction, go demolish a few rooms and then apply for a revaluation.

Rates in Christchurch city are about twice what aucklanders pay. And the capital values are half so is there a causal relationship between them...sarc

I understand rates based on capital value are relative, but other suburbs are dropping in value faster than where I am, so I would be paying relatively more.

BTW. That's a ridiculous suggestion. Why would I waste my time and money making changes to my home that I don't want?

Some interesting stats. 5000 homes sold during the month. Yes it is slower than average but still not too bad.

The number of auckland homes to rent is trending down, first time below 5000 in a long time. The rental market is a leading indicator for sales.

I decided to buy a Condo in Bangkok, the price has been going up, so glad I pulled out of NZ, it's a sinking ship, it's not just housing, it's everything. Better to get out while you can before there is a mad rush for the gates.

An excellent opportunity for the savvy investor, I reckon.

Plenty of crystal ball gazing. Remember, you buy houses in NZ with the Kiwi peso. That doesn't seem to be worth that much anymore. If a house is for sale for 1 million dollars, there might be 1 buyer. If a house is for sale for 1 dollar, there will be a million buyers. The expensive to dirt cheap turning point can come quicker than you think. The government has plenty of debt and a period of high inflation benefits them, so what is going on is probably rigged.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.