It became just slightly easier for aspiring first home buyers to get into a home of their own in May, as the benefits of falling house prices at the bottom of the market marginally outweighed the effects of rising interest rates.

According to Interest.co.nz's Home Loan Affordability Report for May, the Real Estate Institute of New Zealand's national lower quartile selling price declined to $628,000 in May from $640,000 in April.

That reduced the amount needed for a 20% deposit on a lower quartile-priced home slightly, to $125,600 from $128,000.

It also reduced the amount that would need to be borrowed for an 80% mortgage by almost $10,000, to $502,400 from $512,000.

Unfortunately most of the savings in mortgage payments that would have been derived from a smaller mortgage were eaten up by higher interest rates.

The average of the two year fixed mortgage rates charged by the major banks increased to 5.10% in May from 4.96% in April (assuming a minimum 20% deposit).

The net effect of that was the mortgage payments on a lower quartile-priced home purchased with a 20% deposit declined to $629 in May from $631 in April.

In practical terms, the fall in house prices in May made it slightly easier for first home buyers to raise a deposit, while the effects of falling house prices on their mortgage payments were almost entirely offset by higher interest rates.

So first home buyers came out slightly ahead, but not by much.

Looking back over the last six months, the effects of changing market conditions on first home buyers have bene more mixed.

The REINZ's national lower quartile house price peaked at $670,000 in November last year and has since declined by $42,000 to $628,000 in May.

That reduced the amount needed for a 20% deposit by $8400, although getting together $125,600 for a 20% deposit will still likely be beyond the reach of many.

The amount needed for an 80% mortgage declined by $33,600 between November and May, from $536,000 to $502,400.

Over the same period the average of the two year fixed mortgage rates increased from 4.08% to 5.10%, which pushed mortgage payments up from $596 a week to $629.

So the trend emerging for first home buyers is that house prices at the bottom end of the market are declining, reducing the amount they need for a deposit and the amount they need to borrow, while rising interest rates are pushing up their likely mortgage payments.

With interest rates continuing to rise at a substantial clip, the trend noted above is likely to continue into the short to medium term, unless house prices start falling at a much greater pace than they are currently.

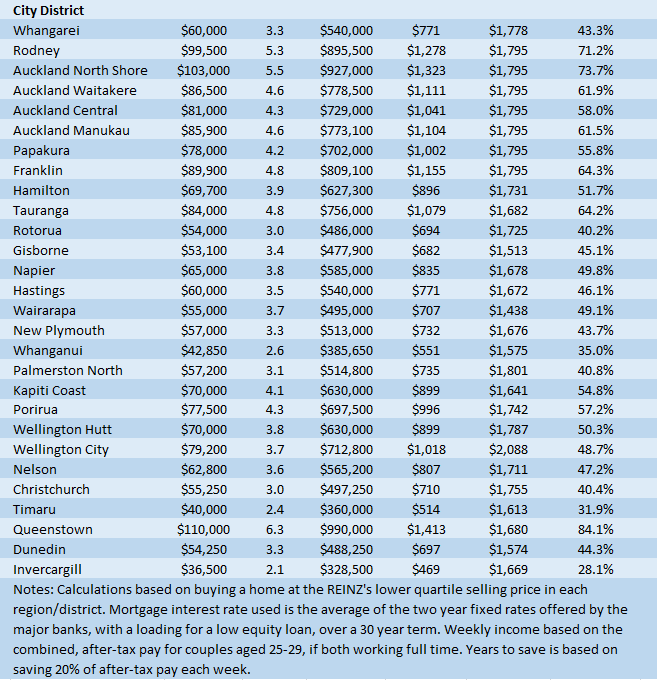

The tables below show the main measures of affordability for typical first home buyers in all of New Zealand's main urban districts, with either a 10% or 20% deposit.

The comment stream on this article is now closed.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

52 Comments

Great news. I'm far more comfortable with the risk posed by a FHB who is repaying a smaller home loan at a higher interest rate than a FHB who is repaying a mammoth loan at ultra low interest rates. I'm hopeful house price falls continue to outweigh interest cost increases.

Perfectly said, I agree 100%. This is exactly what NZ needs, also in overall financial stability terms.

I agree. This housing correction is benefitting aspirational first home buyers and also renters, as rents fall due to increased supply. Will National really reverse Labours policies and look to reignite the market for the benefit of wealthy investors? Isn’t the change in the market exactly what the majority of New Zealanders have been hoping for?

Although those with 7 houses won’t like it!

Critically any FHB who does not need to enter the market now would be crazy not to wait a few months irrespective of affordability. Prices are declining faster month on month according to the REINZ HPI and the market is in the process of correcting.

Now obvious to almost all......

Looking forward to buying at 3-4 DTI as a FHB once the price declines slow down sufficiently to bottom!

The endless dopamine hits of price drop notifications is frying my brain.

Wait a few months. The best is still to come.

In what country VM ?

Bit of a concern there Yvil to your overall property portfolio value ....especially with this current inflation.

Everything up .....houses down.

Motels are probably fine. At least unless the rental market is flooded or there's high emigration and emergency housing is not needed.

I'll buy your rentals for pennies on the dollar if you are selling.

what if they are using their KS as part of the deposit..most of those have dropped fairly significantly...

Your asset allocation should be highly dependent on your investor's profile and time horizon. If you need money within the next, say, 2 to 3 years, you should NOT have most of your KS (or any savings) allocated to shares or to any assets with high short-term volatility.

Cash, not conservative. Conservative is/has been the worst.

I would have an educated guess that less than 3% of kiwisavers change their allocation unless their provider prompts them.

Most wont know that they can do that or have much idea what the options are... or which to pick when.

Agree. And so easy. Quick phone call.

7% rates are a certainty.

-30% by Christmas. Guaranteed.

Kjeldorian. Reeeeeeeeeeeeee. 🐸

3% interest on a $700k is $21,000

7% interest on a $300k is $21,000

That's more than 30% so pretty safe bet you think?

Or have I missed something?

House prices falls lag interest rates increases?

You're talking IO though - if you consider P&I it's not that stark - though still pretty brutal.

Why why why would you first time buy right now. 800 k in mortgage debt and 90k of real money at risk for deposit. To buy something not very good somewhere not very nice. You can pay less to rent something better somewhere nicer. Lock in for a 1 year lease. If you have the deposit just keep it in a TD for a year and pickup a couple of grand in interest after tax. Then reassess in mid 2023.

Hutt Valley Market Update 20th June

Starting to see bigger falls in listed prices this week. Average price reduction at the moment has soared to 91K- back in April it was 67K

Two properties took a whopping 300K off their prices this week (admittedly the houses were at the top end of the market – but this is a 15% reduction in one hit) and brings pricing for this type of property back to late 2020 prices – erasing effectively the last18 months gains.

There are now 43 houses who have taken 100K or more off their price, 12 houses who have taken 200K and 5 who have reduced their price by 300K with the biggest price reduction being $425K.

There are also 3 houses I’m closely watching on the market that sold between March and June 2021. I’m interested to see if the owners get what they paid for the properties back or have to take a haircut – one paid a whopping 300K at the time over the March valuation and I suspect they will be pushed to sell it for what they paid for it. Another property is listed for just 40K above what it was bought for – enough to cover the original price plus the agents selling costs.

The other big news is the number of houses for sale that have listed for rent (these houses are showing as unsold) 8 houses have listed for rent that were previously for sale. This is only adding to the high number of rentals available in the Valley

Current Market Listings

594 houses on the market- up 7 on last week –whilst lower than in April and May when listed number of houses peaked at 652 houses in early April, there are still 2.5 times the number this time last year when 230 houses were for sale

Based on the REINZ data which showed that 96 sold in Feb and 104 sold in March and 98 in April and 96 in May giving an average sale of 25 houses per week– 594 houses means there is 24 weeks stock on the market.

House Price Reductions

306 houses have a listed price

62% of the houses listed with a price have reduced their price since listing

The average markdown has increased to 91K.

Of those that have listed prices (pool 306) -43 have reduced their prices by 100K

12 have reduced their prices by over 200K, 5 have reduced their prices by 300K and 1 now has reduced their price by 400K with the biggest reduction been 425K (a total 25% reduction)

The data continues to show the majority of houses listed are under 900K. The Median house price for all 594 listings is now 839K. (this is up 10K on last week)

The latest QV valuations (valuations by QV which are updated every month and give an approximation of a houses value) have dropped $130K since Jan for the Hutt.

In April the QV valuation had dropped 80K – approximately 20K a month since the start of the year but this escalated in May – dropping 50K in one month.

Meanwhile Homes based on last weeks update is inline with QV and indicating there has been an approximate $160K drop on house prices in the Hutt valley– since the peak which they are indicating was early Nov 21. According to homes prices are back to June 21 prices – so flat with this time last year.

Houses sold vs houses removed

My records show 209 houses listed with a Price have sold YTD (up 15 from last week).

I have records of a further 170 houses (up 16 from last week) that have been removed from the market unsold YTD.

28 of those houses removed from the market have been listed on the rental market

Length of time on the Market

- 430 houses have been on the market for over 30 days - 73% (last week it was 428)

- 311 houses have been on the market for over 60 days - 52% (last week it was 315)

- 197 houses have been on the market for over 90 days – 33% (last week was 186)

- 121 houses have been on the market for over 120 days (last week was 118) - 20%

- 72 of the houses have been on the market for over 150 days - 12%

The number of houses on the market over 60 days is now over 50%. This has risen from 32% of houses in mid March (one in three) and just over 1 in 3 houses have now been on the market more than 3 months , almost 1 in 5 have been on the market over 4 months and 1 in 8 have been on the market over 5 months.

The time to sell continues to get longer and longer.

Rental Market

the rental market has 215 properties for rent (down 17 on last week) and up 92 on this time last year, – when just 123 houses were for rent. The number of rentals has almost doubled on last year

Average rental price reduction is back at $52 a week – one property has dropped their rent $210 since listing from $700 to $410. 40% have dropped their prices since listing.

I have also been noting how many properties are listed for rent over $650 a week.

At the moment the percentage of properties listed at $650 is 40% - last week it was 46%. Still well below the 53% of houses listed over $650 on the 23rd March.

Wow! Those are some scorching numbers.

Thank you for your posts. In a better world we would have independent newspapers to provide updates like this.

Would you be able to possibly put together some info on the breakdown of rent prices to housing characteristics? Decent 3 bedroom places are pushing $700-$750 or more constantly, very little price drop in decent places from what I can tell.

Rents will take longer to drop. it will need an oversupply of rental properties relative to renters. Or renters that cant afford to pay and landlords fighting over the rest.

Both will happen in a few months.

Thanks, these numbers are really enlightening.

I't a big task the one you took!!

🫧⤵️💥

Great work. A picture paints a thousand words though, if you could link to a series of charts with all your historical data that would be amazing and - save you time in the long run by writing all this.

If FTBs are using Kiwi Saver to make the purchase they might have taken a hit due to falling share markets.

Squishy ...ATM everything is taking a hit ......any clues for a 5%+ gross return ?

Building supplies.

(Disclaimer: Not a Qualified Financial Advisor.)

many many things can give that return (or more), if you are keen to risk

You'll get killed with 5% right now, inflation is far higher.

Only 9.4 years to save for 20% deposit so at the end of 2232 FHB will have saved enough deposit let hope prices are still the same.

I think you made a mistake there.

2232 is when the loan is paid of. ;)

No mistake it’s says 9.4 years to save 20% deposit .

I think he meant the century is (hopefully) the mistake

Imagine if we had house price to income ratios of 3 and term deposit rates of 15% and mortgage rates of 21%.

Median Wage $60k. Median House Price $180k. 9.4 years to save a 65% deposit if saving 20% of after tax income.

A $65k mortgage at 21% interest rates would be $270 per week over 20 years.

They had it so tough back in the day.

Amazing how many mistook fortune of birth year for investment savvy, too.

I can hear the boomers go: "Yeah, but we were clever enough to be born during the best two decades, unlike todays young'uns who wanted to be born much later yet still reap the same rewards.."

The generation that rushed out to buy houses in their early 20's while having kids, and yet incessantly complain about how much it cost back then to service the loans they took out. Not the brightest bunch they were.

Yet they have the audacity to claim today's kids are the "me me me I want it now" generation??

With those numbers, what year are you referring to? Inflation obviously high, so 80's? If so, isn't your median wage too high?

I'm working on the 80's median wage to income ratios and interest rates, and applying it to today's median wage.

Today's median wage = $60k. 3 x that is $180k.

"Home loan affordability improved slightly for first home buyers in May despite higher interest rates"

Above headline is too early as house prices have not yet fallen substantially to make real deifference.

Accept that the trend is positive for FHB.

I agree. Can house affordability be regarded as better while the rate to service the median house's mortgage is still increasing? Or is affordability all about the size of the deposit? Doesn't make sense to me to say that affordability is improving!

So banks are quite happy to keep to a 20% deposit in a falling market are they?

FHB should just wait every month around a 20k reduction in Auckland.

The quality of the buying experience is getting better by the week. This is a good chance for a good look around in this type of market. Good luck FHB's.

Hi Greg how come the headline says “Falling house prices more than offset the effects of rising interest rates for first home buyers in May” whereas the article talks of marginally better and slightly easier? I associate hyped headlines that don’t reflect the content with the Herald or Stuff not with Interest.co. Regards Russell J

Few FHBs I have been talking to including 2 at work who have recently purchased, they don’t seem too concerned about the declining market and all very determined to get into home ownership and lock in the “lower rate”. People surely think differently but good on them.

"...lock in the lower rate"

Lets use a very simple example of why a lower loan amount is better than a lower interest rate. Put another way, why waiting for the price to fall before buying is better than locking in lower rates.

Loan A is $700k at 4% interest for a 25yr term. Fortnightly repayments will be $1,704 and the total all in price you will pay over 25yrs for the house is $1,107,600.

Loan B is $350k at 8% interest for a 25yr term. Fortnightly repayments will be $1,246 ($458 less) and the total all in price is $809,900 ($297,700 less).

Thus half the loan at double the rate is still far better for the borrower. Borrowing less has and always will be the best strategy for owner occupied purchases. The above also completely ignores the fact that in NZ the average loan is fixed for 2yrs or less so the rates are likely to change, if they went higher by say 3% (so 7% and 11%) then Loan A repayments rocket up to $2,282 (+$578) and total amount $1,483,300 (+$375,700) whereas Loan B repayments increase to $1,583 (+$337) and total $1,028,950 (+$219,050). If rates went lower then they both win.

Your colleagues are fine to not care about price declines if they have a long term view and can deal with the possibility of negative equity but surely if they have the opportunity to hold in the current market and therefore buy at a lower price and therefore save themselves a truckload money, then they do it. Buying now makes no sense at all.

It's also a lot easier to maximize the up to 5% balance owing lump sum payments on a lower loan amount, paying off the mortgage considerably faster. Or making a chunk lump sum payment prior when you're up for a refix.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.