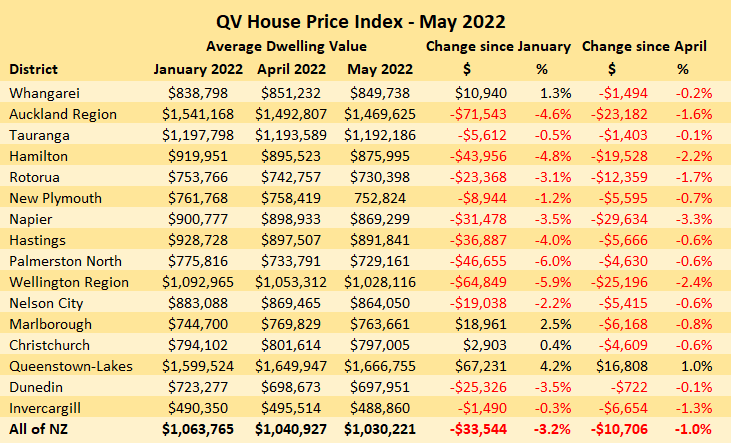

The average value of homes declined in May compared to April in almost all parts of the country, according to the QV House Price Index (HPI).

The HPI tracks average dwelling values nationally and in 16 main urban areas from Whangarei to Invercargill.

Average values in May were lower than they were in April in all of them except one, with values continuing to rise in the Queenstown-Lakes District.

The average value of all homes throughout the country was $1,030,221 in May, down $10,706 since April and down $33,544 since January.

The biggest declines in May compared to April were in Napier -$29,634, followed by Wellington Region -$25,196 and Auckland -$23,182.

The biggest declines since the start of this year were in Auckland -$71,543, followed by Wellington Region -$64,849 and Palmerston North -$46,655 (see the table below for the trends in all major centres since the start of the year).

"There's no question that prices are falling, especially now as buyers take the upper hand in negotiations," QV General Manager David Nagel said.

"It's really just a matter of how much further values will fall before finding the new equilibrium.

"Almost all of the country has passed the value peak of the cycle.

"This was originally driven by investors and first home buyers competing for limited stock, especially with the availability of low interest loans.

"That led to massive value increases to the more affordable locations, so it's no surprise these are the first values to get hit.

"But as the market downturn takes hold, even the higher valued properties have started being impacted now.

"With interest rates likely to climb further to battle inflationary pressures, as well as economic uncertainty with the Ukraine conflict and continuing supply chain disruptions, we've still got a way to go before the market bottoms out," Nagel said.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

70 Comments

"This was originally driven by investors and first home buyers competing for limited stock, especially with the availability of low interest loans."

Does this fully explain why house prices inflated from 2020 to 2021, may be.

Truth be told, I struggle to understand stats from REINZ, CoreLogic and QV. Add One Roof, Homes and Trade Me and its a cocktail mix to confound.

From the chart

The only region to buy a house for under $500,000 is in Invercargill. Newcomers to the cities will need to cough out at least a million, and holiday houses in Queenstown-Lakes, under 2 million.

Something is not right, I recall that cheap abodes could be found in Kaitaia, Taumarunui, Buller.........

Those are outside of the centres in the list.

Truth be told, I struggle to understand stats from REINZ, CoreLogic and QV. Add One Roof, Homes and Trade Me and its a cocktail mix to confound.

The best thing is to stick with the REINZ data - it's the most up to date and covers maybe 85% of all sales that occurred in a month and is reported 2 weeks after the end of the month. Ignore the others as they are 2-3 months behind the actual current market.

It was an irrational mania. The supply of greater fools has been exhausted. Now it's Minsky time.

🫧⤵️💥

Nationally, house prices increased by 49 percent in the 2 years leading to the market peak in November 2021.

So it's now in a correction phase - surprise, surprise.

Don't listen to the Doom Goblins here who plead it's an apocalypse, crash, collapse, meltdown etc. That's nonsense. Their agenda is to buy a house for next to nothing - but even if that happened, they'd still lack the wherewithal to get themselves into gear and do something.

TTP

Don't listen to the Doom Goblins

You use childish name calling in your posts but then expect us to heed your advice like you are a wise and savvy financial genius?

... quite the opposite of " Doom Goblins " ... some of us are ecstatic to see prices come back ... they got a long way to come down before houses are seen for what they are : An abode ! ... joy for regular Kiwi folk , who might be able to afford one now ....

It's basic math at this point that house prices have a fair bit further to fall given the whole reason people were paying exorbitant amounts was because the bank would lend it to them, and they could afford the repayments. Struggle to see how that's being a 'Doom Goblin'.

No matter how far prices drop still nobody wants to live in Palmerston North. At least those that haven't had a full frontal lobotomy.

Not even the allure of a chintzy 'penthouse' can do it. At this rate property brokers might have to rename themselves to property broke!

It must be hard to be the only person in the room, who see's this as a buying opportunity already......

TTP what is Doom a goblin as most people want house price’s to be more affordable. You are on your own if you want to see people in huge debt sound like you are bitter about something by any chance are you in financial trouble surely you would have seen this crash coming.

I think he's a mortgage broker based on previous comments (could be wrong).

So bigger mortgages = more money for him. Its like talking to an RE agent.

I don't think most people here are doom goblins, whatever that is. Simply just aware of the massive disconnect re recent prices vs historical and World avgs and also aware of the risks that brings.

Personally I see opportunities for major discounts starting in 6 months.

Vulture funds cashed up and waiting...

TTP is the head of a well-known real estate company. I won't say which, but they claim to sell their property with pride.

Affordable housing and the opportunity for future prosperity of young New Zealanders = Doom and Gloom.

People that believe this to be true are the real 'Doom Goblins'....lol.

They are a cross between Gollum and the Grinch.

Gollum traits - They think property is their precious and homes are there to be turned into their investments (when they are already wealthy).

The Grinch traits - They also take pleasure in ruining what should otherwise be a happy period of younger peoples lives (FHB's trying to get established and start families). "how dare you be happy when I'm old and unhappy and take pleasure from having control over other peoples lives by turning others into my rents slaves".

Pretty much in all asset class that were juiced up on cheap money

The vast majority won't even notice, just like they didn't when house prices sky rocketed.

This fall is a good thing and it needs to happen uninterrupted. But it won't, some politician or central banker will get the idea that they need to 'save the housing market'.... Ugh

It'll be jobs and the wider economy they'll try to save. By one of the few levers they have, which overlaps with housing.

Sustained, long term prosperity takes far longer to establish, and governments will struggle to be the author for that, outside of maybe trying to balance their books well enough to stay solvent whilst also providing for the population.

People have an annoying habit of wanting to eat every day.

The unemployment rate is 3.2 now, there is absolutely no need to save jobs. It's not high interest rate that is hurting New Zealand's economy, it's inflation, I've heard many business owners told me that how hard it is for them to cope with inflation and finding staffs.

I dont buy that they didnt notice when it sky rocketed. Maybe ask the local spa shop/pool builder/ford dealer/jetski seller.... The wealth effect has been a massive driver of a lot of local business for the last 3 or so years.

One could even suppose that it kept the light on.

Rockstar economy....

Needs or wants?

These are all wants. We are rapidly transitioning to needs only.

Interesting times, I import wants, we have seen 30%+ growth yoy in the 2 covid years, we are still cranking now. I really have no idea how bad it will get, Im picking pretty bad, back to pre covid numbers.

Well I agree, there will come a point when the govt feels they must intervene.

But this time it might well be different, if inflation is still surging and oil prices stay elevated, can we risk dropping the OCR and the value of our dollar with it?

My bet is they will get to a point where they see the only option is to go back to the money printer, which too will be inflationary and devaluing to our currency.

This is all been quite predictable and inevitable. You cant keep pumping a ponzi scheme forever. Successive govts have sacrificed long term stability for short term "wealth". But anyone with 2 brain cells to rub together could see that house prices increasing by 10% per annum while wages were increasing at 3% (over decades) would eventually come to this outcome. The craziness of the last 2 years has just accelerated the process.

pop!

This was originally driven by investors and first home buyers competing for limited stock, especially with the availability of low interest loans.

Seems reason enough to cut the accommodation supplement.

Pretty rough if you were a FHB last year and low interest rates finally made it possible to buy your first home after years of saving a deposit. Now the mortgage interest will me more than rent was and your deposit has evaporated.

That is rough. Silver lining though, at least there's no landlord snooping in every 6 months, moaning that you didn't declare that you own a hamster.

Haha, will someone think of the hamsters!!!

It's a Siberian Hamster.

Somewhat ironically that would be a legitimate complaint. Hamsters are forbidden in NZ. :)

BE QUICK!!!!!

Take your time

Hurry up

The choice is yours (don't be late)

doused in bleach (the mould that is)

Memoria, memoria

I would call this housing cluster f*%^ the biggest debacle of modern NZ history. The social and economic damage it has caused, and will cause, cannot be underestimated.

It’s the main reason why I will never again EVER vote for either of the major parties. Both have been completely complicit. And neither have any answers.

Since early 2020 some of the most brilliant economic and financial minds have been scratching their heads trying to see their way forward. And that's just trying to make a buck.

Thinking a democratically elected NZ government would do much better is somewhat naive. Just like covid, no government is going to be overly capable of navigating the current economic and geopolitical scenario.

I am not talking about the last year.

I am talking about the last 30 years.

Hard to say. In the 50s, the government started promoting higher rates of home ownership, perhaps that's not a sustainable model long-term.

So maybe 70 years, and we shouldve just had social housing. Hard to comprehend where we would be now instead. Happy workers?

The difference was they did it not by inflating debts ever higher, but by building affordable supply.

'most brilliant economic and financial minds have been scratching their heads trying to see their way forward.'

No, they haven't. They have deliberately ignored solutions that many other jurisdictions use to prove affordable housing.

All the things they have more direct control over, they mismanaged so we have no resilience to buffer us against all those things we have less control over.

They have answers. Labour will introduce more tax, raise the debt ceiling, and provide some free hand outs.

National will invite many thousands more Chinese to come stay.

The rest of us will buy the woke BS pumped on MSM and will start identifying ourselves as him/her/it/maybe.. and everyone will be kind.

Labour seem to be doing a lot of free handouts. Mahuta and cousband are in the Herald again this morning for more shady dealings.

Everyones on the gravey train Brook..we need a diversion, how about a new flag?

Nothing wrong with our existing flag.

We have a new winter fireworks night coming up though.

I will be looking at the stars Brook, trying to navigate life, by the way are you any good with Te Reo, as you mentioned you were of mixed heritage?

I prefer to learn more useful languages.

Sign language?

I will be improving my Dutch this year.

I pledge votes for life to any party who brings in the lazer kiwi flag.

I was ready to vote for that, then they gave us lame options.. no sense of adventure!

Politically it works though, homeowners vote for incumbent governments when house prices rise. It's as close to "free ice cream for everyone" as you can get.

Exactly. It’s been political gold.

But certainly not in the interests of the country, beyond the short term ‘sugar rush’.

Still sitting in cash mostly. The inflation rate makes it unpalatable but less painful than many asset classes. Can't be a coward when the market turns.

Me too.

I want TD’s at 4% minimum before I look to chuck some cash in to them.

Me three,

Cash offsetting our mortgage at the moment.

Probably the best investment you can find at the moment. You would have to find a term deposit approaching 7% to outdo an offset facility at the moment.

Ditto. Keep us posted when you think it is time to move.

I've never made much use of term deposits. My view has been that staying nimble benefitted me more than a low single digit return. I don't have any proof of that though because I use indexes as my benchmarks and not term deposits.

The process of OCR hike has just started overseas and can already see the hurt, wonder what will be the pain when it actually peaks. We too here in NZ are halfway as expecting to double from here (3.9%) or minimum 65% to 75% more to come (3.4%)

Check any news and data today, all pointing towards.....and central banks are helpless as unable to manipulate.

https://www.macrobusiness.com.au/2022/06/reserve-banks-scorched-earth-i…

https://www.oneroof.co.nz/news/dropping-50k-a-week-prices-slashed-on-th…

https://www.stuff.co.nz/life-style/homed/real-estate/300608852/foop-ale…

https://www.stuff.co.nz/business/128884850/is-the-nz-housing-market-dow…

In Australia too and below article explains that why interest rate rise will hurt more than 1990s when interest rate was 17%

https://theconversation.com/the-housing-game-has-changed-interest-rate-…

https://www.news.com.au/finance/economy/interest-rates/rba-interest-rat…

Some people's idea of a price drop differs to others. It is highly subjective and rather meaningless when you think about it. I see agents claiming a price of 859k was a drop when the owners had bought it less than two years earlier for 645k and the 2021 RV was 760k. Another house claimed "a massive price drop" yet was advertised for 85k over 2021 RV. Another claimed "a huge price drop" yet was price by negotiation?

Add Below to the list of news on our interest.co.nz

https://www.interest.co.nz/property/116281/forget-about-fomo-foop-now-r…

So everyone and everywhere is worried and predecting a crash...wil it be is wait and watch

Hutt Valley Market Update 6th June

Current Market Listings

600 houses on the market- down 13 on last week. For the previous 3 weeks listings has ranged between 610-620. This week was the first time listings declined below 600 since the middle of March

Based on the REINZ data which showed that 96 sold in Feb and 104 sold in March and 98 in April giving an average sale of 25 houses per week– 599 houses means there is 24 weeks stock on the market.

I am still expecting given the withdrawals and low number of listings for the number of listings to fall to around the mid 500’s by mid winter ie late June/early July before picking up again in August.

House Price Reductions

308 houses have a listed price

60% of the houses listed with a price have reduced their price since listing

The average markdown has risen this week from 85K to 89K.

Of those that have listed prices (pool 308) -39 have reduced their prices by 100K

7 have reduced their prices by over 200K, 2have reduced their prices by 300K and 1 now has reduced their price by 400K with the biggest reduction been 410K (a total 25% reduction)

The data continues to show the majority of houses listed are under 900K. The Median house price for all 600 listings is now 830K. (Steady on the last two weeks and the lowest Median YTD – previous low was $839K)

The latest QV valuations (valuations by QV which are updated every month and give an approximation of a houses value) have dropped $130K since Jan for the Hutt.

In April the QV valuation had dropped 80K – approximately 20K a month since the start of the year but this escalated in April – dropping 50K in one month.

Meanwhile Homes based on last weeks update is inline with QV and indicating there has been an approximate $130K drop on house prices in the Hutt valley– since the peak which they are indicating was early Nov 21. According to homes prices are back to June 21 prices – so flat with this time last year.

Houses sold vs houses removed

My records show 189 houses listed with a Price have sold YTD (up 18 from last week).

I have records of a further 151 houses (up 2 from last week) that have been removed from the market unsold YTD.

19 of those houses removed from the market have been listed on the rental market

Length of time on the Market

- 439 of the houses have been on the market for over 30 days - 73% (last week it was 445)

- 322 of the houses have been on the market for over 60 days - 54% (last week it was 299)

- 179 of the houses have been on the market for over 90 days – 30% (last week was 168)

- 110 of the houses have been on the market for over 120 days (last week was 107) - 18%

The number of houses on the market over 60 days is now over 50%. This has risen from 32% of houses in mid March (one in three) and just over 1 in 3 houses have now been on the market more than 3 months , almost 1 in 5 have been on the market over 4 months.

The time to sell continues to get longer and longer.

Rental Market

Meanwhile the rental market has 204 properties for rent (up 3 on last week), and up 75 on this time last year – when just 129 houses were for rent.

Average rental price reduction is back at $62 a week (down $9 on last week and up $13 on a month ago) and 40% have dropped their prices since listing.

As noted last week I have also been noting how many properties are listed for rent over $650 a week.

At the moment the percentage of properties listed at $650 is 45% - last week it was 43%. Still well below the 53% of houses listed over $650 on the 23rd March.

Why can't the professional journalists produce this kind of objective, unbiased, commentary on the housing market?

Most of them are based in the Philippines ?

Because the banks or real estate agents or government (who benefit politically from the wealth effect of rising house prices) pay their bills.

Cause that would take hard analytical work. And doesn't grab headlines.

Much easier to report what colour dress so and so was wearing on dwts...

You obviously have an interest in the stats and what they mean.

Id recommend having a look at Four Days with Dr Demming… a great book

Might add another insight

QV says, up in Queenstown 4.5% in 3 months.

This poor fella is showing >$200 drop in value over 12 months at 300 Point Chevalier Road, Auckland : acquired Jun-21 for $2.526m ; now asking $2.25m. Returns are diminishing in 2022 as quickly as they were made in 2021.

https://www.trademe.co.nz/a/property/residential/sale/auckland/auckland…

Good spotting MuckyMuck. In the old days you could expect to lose 10% if you sold a house within a year. The trouble is these days 10% can be rather a lot in dollar terms.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.