The tide is turning on the housing market according to Realestate.co.nz, with the number of homes for sale rising strongly while asking prices head in the opposite direction.

The property website had 27,050 residential properties available for sale at the end of April, up from 15,838 at the same time last year, an increase of more than 11,000 (+71%) compared to year ago.

The increase in stock levels was nationwide, with the regional annual increases in properties available for sale ranging from 21% in Central Otago/Lakes to 175% in Manawatu/Whanganui.

So it appears buyers have no shortage of properties to choose from at the moment.

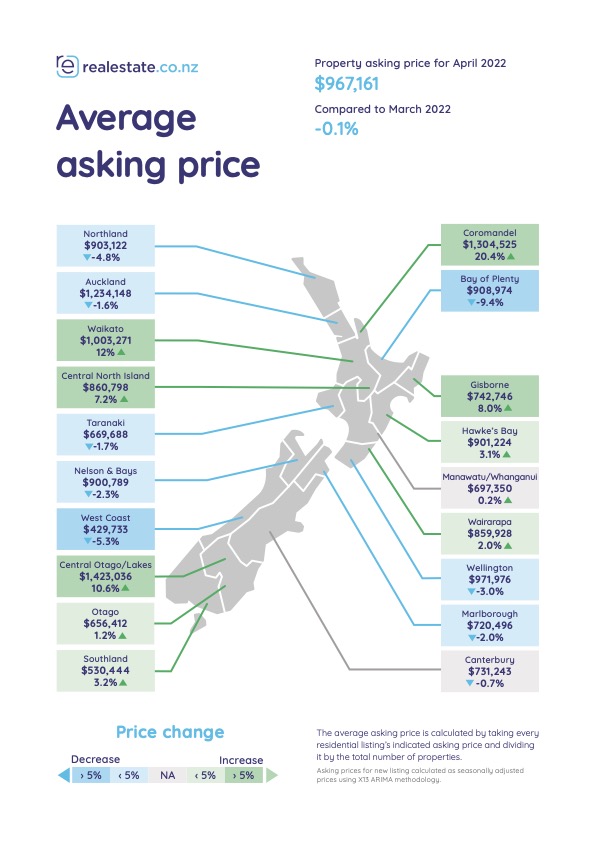

At the same time asking prices have started declining, with the national average asking price falling for the second month in a row from its peak of $1,012,755 in February this year to $972,141 in April.

The fall in prices has been particularly strong in the Bay of Plenty, where the average asking price has declined from its peak of $1,055,492 in December last year to $903,606 in April this year.

Prices were lower in April compared to March in 11 regions and up in eight, with four regions sitting in record asking prices.

In Auckland the average asking price has dropped from its February peak of $1,303, 553 to $1,231,996 in April.

In the Wellington region the average asking price has dropped from its February peak of $1,033,528 to $986,363 in April, and in Canterbury the average asking price peaked at $755,597 in March this year and dropped back to $730,544 in April.

"The tables are turning on New Zealand's hot property market," according to Realestate.co.nz's April report.

Realestate.co.nz spokesperson Vanessa Williams said the heat had come out of the market.

"We have become accustomed to urgency in the market, with multi-offers and high competition being the norm," she said.

"Right now however, buyers have more time to do their due diligence and make an educated decision on their future property."

The report said Auckland and Wellington were already buyers' markets and the regions poised to follow suit were Hawke's Bay, Manawatu/Whanganui and Otago.

The comment stream on this story is now closed.

154 Comments

Oh dear, how sad.

My slumlord enjoys sucking massive $$$ from my budget, and in return gives me the privilege of living in a rotty old sh/tbox with revolting carpets.

I will enjoy seeing her lose hundreds of thousands of dollars this year. I will be gleefully cheering this crash on from the sidelines.

Let all the rent vampires burn!

What a sad attitude mate, if I was her I would boot you out on the street. Don't like the place ? buy your own or suck it up.

Haha how is that a bad attitude? If I said I hope the supermarket duopoly crashes and burns and prices come down so people can afford to eat, is that a bad attitude? Or should I just go out and start my own supermarket for myself?

Carlos is only happy when he is nasty to people less fortunate. What makes him tick?

You can see why Carlos lives alone.

No Carlos I'm not going to "buy my own" and be a slave to the bank for the rest of my life.

I will buy when houses cost 3 or 4x income, and a person can pay off the mortgage before retirement and be a free man.

This whole sick society that we have built is centered around taking a section of society and forcing them into slavery. It is either rent slavery, or mortgage slavery.

Screw that. The system is about to burn to the ground. I'm staying as far away as I can until the smoke clears.

... good plan ... next year the Gnats will inherit an economy mired in debt and inflation , the Labour wastrals will abandon us to take up sinecures at the U.N. & on climate change committees ...

Well, than you're likely to remain a slave of a landlord for the rest of your life!

Yes, mortgage slavery is a thing and it would be awesome if everyone could buy their own home for their own money but this and the big crash you're waiting for will never ever happen!

What's more likely, we'll end up in a Mad Max scenario after a nuclear exchange and you can squat some ruins and call them your own.

No sane govt will break the status quo and throw away all these "retirement savings" & "created wealth" which means employment for a huge chunk of NZs.

If houses would get "cheap" again (like 3-4 times your income), it would firstly require massive unemployment and wages would adjust downwards accordingly.

The only way to fix this unaffordibility issue without making life miserable for most New Zealanders is to slowly errode house prices by making them go sideways and let wage inflation catch up.

This would likely require several decades / generations so you might now want to hold your breath!

If people can’t afford to buy who will at 12 x average couples wage in Auckland looking like big drops in house prices will happen and with interest rates still on the up could easily be 50% over next year, anyone who purchased in last 3 years will lose deposit and be in negative equity but a lot of them would have made huge amounts on way up. Maybe everyone in Auckland get pay raise too 200k

Have you seen the swap rates lately?

The government is not driving this bus. The RBNZ is not driving this bus.

The closest thing we have to a bus driver is J Powell, and he is taking this big ol' overinflated debt bus right off a cliff.

Also, what kind of a cruel person would tell someone that they are going to be a slave for the rest of their life? It is horrid to see what greed and the pursuit of "wealth" can do to our souls. The crash is going to hurt. But the glimmer of hope at the end of the long painful crash will be if average Kiwis can own their own homes again. A house at 3-4x income is not "cheap". It is normal and in line with house prices in every other comparable economy.

You mean the swap rates that are flat from 3 years out to 10 years according to the interest.co.nz data? (Technically inverted from 4 to 10y period)?

What does that imply, when people will do a 10y swap for a lower yield than a 4yr swap?

Don't like the younger taxpayers? Pay your own landlord subsidies and pension or suck it up.

Well said Fitzgerald.

We live in such a criminal system where we have encouraged and rewarded landlord leaches. We have allowed banks to lend money into existence, just create the money other people have to work for to allow landlords to buy second and third homes, deduct interest so they run at a loss and get refunds on PAYE that they may have paid and for the most part not pay any tax on the capital gains caused by central banks fuelling the fire with emergency interest rates. And we wonder why we have social imbalances.

It’s disgustingly, it’s apathetic but as I heard the other day; good economics doesn’t make for good politics.

Well, you'd better hope that 7 houses Luxon doesn't get voted in next year otherwise we're back to tax payers subsidising landlords to take out big loans.

Essentially what we've done under labour recently.

Conehead Properties ?

How long have you been in the joint, I am guessing 30 to 40 years as those carpets were revolting to look at after a long night on the town

You are looking at this the wrong way. This is good news for your landlord. With falling prices, their yield increases.

Which means they can afford to drop the rent.

hahahaha

In General, you don't want the rent to drop, as much as the prices fall, because if we aren't going to get any capital growth, it has to be offset with a higher relative yield, which is preferable to what we have had, which is stupid speculative rentier capital growth, and a poor yield based on that non-value-added speculative gain.

So when the price bottoms out, whenever that is, what the Govt. needs to do is have land-use policies in place so we don't get another boom repeat.

End result would be lower more stable house prices, with rents being slightly less than they now are, but relative yields better.

Great post. DTi or other required at the bottom to stop the stupidity that would be a repeat of this policy. Holding fellow kiwis hostage over the basic human need of shelter, just to provide endless profits for global banking interests is parasitic.

The only known land-use policy intervention that will work is to remove most of the restrictions that prevent building both up and out.

Jurisdictions that have these presumptive rights to build are still approx 3x median income in spite of any of the reasons we give for our high prices.

You must be thinking that low int rates will make a comeback. Isnt low int rates what drove the market boom,

Low-interest rates only make a difference when land release is restricted. Since low-interest rates stimulate demand, in jurisdictions where land policies allow supply to equal demand, the supply of housing can increase while enabling the price of housing to remain low and stable.

Sounds like its time you moved out and rented a place thats not so shiity or rotting, can you not do this?

Do yourself and your landlord a favour, move out...no one is forcing to stay there - you sound miserable.

Im a happy renter, Ive a decent landlord, paying less than it would for me to have a mortgage.

Geoff this is not the right victim mentality, you may have wandered into this thread by accident but a quick pointer to how this works, landlord=bad renter=good.

I would be interested in your opinion in "no-pets" ads.

For me it means that usually that landlord is a bad person.

Now there is a new one "no-vapers" (I'd like this one to be explained to me, is like to say no cooking)

I didn't see a "no-kids" clearly yet, but I have seen "professional-couples"

Yes, most landlords are not nice peps, that's a fact. Or I (and most of people I know) have been exceptionally unfortunate with ads.

I am renting from a very nice lady right now, but I needed to find her between several very unpleasant specimens.

I have run no-pets adverts for some of my apartments. I understand that in your opinion this makes me a bad person and I think that unfortunately says more about you and the shallow way you generalise people than me.

As you clearly do not own property let me help you understand why this is necessary.

1) it is against the body corporate rules of the property (that is the owners rules for behaviour) and so renters cannot have a pet. (nether can actual owners who have paid enormous sums to actually own the other properties in the complex). Why is that a common rule? Because people cannot be trusted to manage their pets and they spoil the environment and common areas for other owners who do not want pets.

2) Because people cannot be trusted to manage their pets and they spoil the carpets and other furnishings in the property.

Where I have allowed people to have cats it has been because the were good long-term tenants and had earned my trust by looking after my property.

Stay with your nice lady is my advice.

Hooray for a sensible comment at last.

I've got the pop-corn ready

It's sad that you feel your landlord enjoys that you are paying big $ for what you're far from happy living in.

I must point out that not all landlords (if many at all) share the same enjoyment as you think yours and others may do. It's far from just interest rates rising a landlord has to keep up with. Insurance for one is huge, council rates, electricity, water, phone/net, ongoing maintenance and compliance. These responsibilities seem to go unnoticed by a lot of renters.

Have you had a conversation with your landlord about your concerns? Not all landlords are 'rent vampires' and I'm sure the majority of landlords would prefer spending few $ to secure a tenanted property/room rather than having it vacant or a highly disgruntled tenant.

.

Funny how this happens: when prices are crazy high no one wants to sell, and when they drop all of a sudden there is plenty of new stock. Its like some kind of inverse market where supply is increased when prices go down.

Actually it makes perfect sense, it's greed and the human psyche.

I think what you've described is trademark bullish and bearish activity.

Buy and hold on on the way up, sell on the way down.

The only difference is that it's difficult to spot the top and bottom of the market as we can only judge by past sales that have gone through. If you brought forward all of the future sales of current housing stock to today, ie if you could sell houses as easily as you could sell crypto, you may just see the rare native NZ Bear.

Still not seeing asking prices fall in Tauranga. I must admit we are looking at the upper end of the market in the $1.2 to $1.5mil bracket. Still got the same 20 places on the watchlist and what I can say is that they are NOT SELLING at prices $200k over the new RV. Sellers need to get more realistic, the market has turned. There is now a record number for sale on TM at 1,131 which is the highest I have ever seen. Overall prices have still been increasing down here on actual sale price but those vendors that are still holding out for Dec 2021 prices are having to stay put.

I know someone in AKL that just got a house in Meadowbank 300k under the reserve after auction fell over, its happening but that number wont be made public until 2 months after settlement, RE not telling buyers what stuff is actually selling for...... Sellers not hearing RE

Got family looking to buy and sell. Dealing with REA bulldust is their worst nightmare, they live in a fantasy world of cliches and corrected answers to any question.

Look at the average IQ of your typical agent and it shouldn't surprise you. Its not “stunning”

How many offers or auction bids have you made. Sooner or later you will strike a willing seller

How long are you thinking you will wait? We had 21% uplift last year so we need that (+7% for inflation) to get back to a year ago. Not suggesting you buy at the moment but do you have a required % drop in mind before you would buy?

read - capitulation is coming https://www.zerohedge.com/markets/drawdown-delerium-bezos-warns-markets… this stock crash is going to smash us all, the bubbles are over!

I agree, I have a bad feeling about what is coming and its only months away. Not sure about anyone else but the spending has really dried up, you cannot give things away on Trade Me these days. A couple more big rate hikes and the market will capitulate. The question is, is it even avoidable now ? The FED will be forced to raise rates. Could be a bit of a nasty reset.

Zero Hedge has predicted one million of the last zero financial armageddons.

They will be right one day though. Stock up on gold, food, and ammunition.

Warren Buffett has invested an extra $US 50 billion or so , recently ... Berkshire Hathaway is full up with basic commodity stocks , insurance & rail roads ...

... who'd believe , the great Warren , or Zero Hedge !

Both Buffett and Charlie Munger have made hostile comments toward bitcoin in the past. Most famously, Buffett said bitcoin is “probably rat poison squared.” Munger doubled down on that sentiment Saturday.

“In my life, I try and avoid things that are stupid and evil and make me look bad in comparison to somebody else – and bitcoin does all three,” Munger said. “In the first place, it’s stupid because it’s still likely to go to zero. It’s evil because it undermines the Federal Reserve System... and third, it makes us look foolish compared to the Communist leader in China. He was smart enough to ban bitcoin in China.”

Crypto's are a Ponzi scheme, nothing else.

19000 crypto currency’s once inflation has ripped throughout world go try and buy food with Bitcoin. Once governments create own digital currency Bitcoin will be outlawed in USA just like in China.

Yes, buying (and keeping) great businesses are the best hedge you can have.

Over years systems will change and Bitcoin will just be a relic. Gold and silver have always been of value

I think it is Warren Zevon rather than Warren Buffett we should be listening to.

Stock up on Lawyers, Guns and Money

'I went home with the waitress, the way I always do

How was I to know, she was with the Russians, too?'

https://www.youtube.com/watch?v=F2HH7J-Sx80

Tiger is that you?

Brock, I know right? So many alleged serious commentators share links to Zerohedge. I shall fall over if anyone ever links to the FT or Economist.

5.5% drop in the average Auckland asking price in a month is significant. The auction clearance rates this week will be more bad news I suspect. NZ's OCR will be driven higher by the Fed's tightening - nowhere for Orr to hide. The housing market is going to take a beating.

To be fair the asking price drop is irrelevant. The asking prices down here need to drop 10% because they just think the market has kept increasing from Dec 2021 like it did all last year and its simply not the case, its flatlined at best. Either owners or RE agents are out of touch, if you want to sell you need to look at the new RV.

In my opinion, prices are 20% lower today than the peak - so already a mini-crash. You would be nuts to pay anything less than 20% below asking today, that's where the current stock will clear. From there, if we get the interest rate track forecast by the swap curve a minimum of another 25% lower - so back to 2017/18 price levels (40% lower).

Some of this will come about by Kiwi weakness as I am looking at prices in TWI terms. The RBNZ/Treasury have messed up and senior management should collectively resign.

Kiwi $ is looking very weak.

... its weak this week , and liable to get alot weakerer over the next 12 months ... I have a niggly naggly feeling that the 2023 election will be a reverse image of 1984 when the Gnats were ousted , leaving an economy on the brink of a complete meltdown ....

The Nat's should get back in, the average person will not be doing well by that point.

They will need a least some policy by then as deleting a public holiday and moaning about our terrible Covid response wont budge plenty of voters?

Given how bad Labour are and how dire the economy will get, the Nats don’t need to do much, other than appear semi-competent.

throw in some income tax cuts, and they a high chance of winning.

True the boomers class love a good tax cut and kicking cans down the road..

Labour just need to do a surgeon key and give tax cuts, probably at the bottom end. What do National have then? Any principals apart from neo liberalism?

Principles:

1. Working folk pay the taxes

2. Speculators don't pay the taxes

3. Distract the working Kiwis with small tax cuts, but mainly for the highly paid ones

4. Talk about being good at economics and business.

1. Agreed, the top 4% pay 30% of the tax, 50% of the tax base pay effectively no tax at all after benefits.

2. Speculators pay 39% tax in all probability on speculation.

3. Yes this is true, tax cuts are largely marketing and yes mathematically those who earn more will always gain most from flat tax decreases.

4. In the socialist republic of Aotearoa we have a very progressive tax regime, ignoring the fact that one person can only consume one person's worth of government resourcing (awkward), this uneven approach has served us well thus far.

1. What's that, working people paying income tax rather than where much of the money is made? Yes, correct, as noted.

2. LOL. Yes, because simply pretending not to have ever bought for capital gains so as to evade tax has never happened at all over these last decades, and even voluntary bright light compliance is spectacularly high and never complained about at all.

In the socialist republic of Aotearoa the working folk pay the bulk of the taxes while investors have freeloaded for a long time, while also receiving >$4 billion landlord benefits and universal welfare benefits above a certain age. Quite the parasitical model, living off the working folk.

The bright line test is not voluntary unfortunately and in any regard I would not complain about this capital gains tax that isn't one.

I am interested in how you think investors have freeloaded off anyone? Where do investors get their capital if not from their own, tax-paid labour?

Sounds like you may be unfamiliar with how things have worked in NZ with rising property values providing the untaxed deposit for the next property - but that is how. So while an initial deposit may have come from taxed productive work, subsequent ones in many cases have not, and have not been taxed.

And New Zealand has simply not taxed this and realised capital gains for the longest time, despite buying and selling for capital gains being a taxable activity here even prior to the Bright Line. Tax evasion en masse as a result and most wealth being made this way, while working folk have paid the taxes that fund society and its services used by all - including over $4 billion in landlord subsidies per year.

Property has been coddled, and productive work penalised. Investors have been able to live in and benefit from society that productive working Kiwis are paying for.

“…other than appear semi-competent” looking back at their recent history of scandals and coups, this could be a stretch for them. I am not sure if a party that labels the poor as “bottom feeders” is quite the right choice in our current economic times. The housing frenzy has benefitted a minority, it is time to help the majority.

When did " The National Party" call anyone a bottom feeder?

I wonder what the definition of buyers market is? Buying a 50 year old uninsulated box next to a gang pad for $1 mil is a buyers market?

. . I thought that too ... prices fall from being 100 % overpriced , to 95 % ... and it's called " a buyers market " ...

Are we surprised that real estate agents have less respect than used car salesmen & politicians ... so puffed up with their own arrogant B.S. and pet cliches ...

REANZ went to the CPI school of rounding. Lets just say 10000 homes on the market in Auckalnd. How many of them are brand new? Representing the investments of developers and those who fund them. Carrying costs slowly eating away what profit was left after they got screwed on the costs of building materials.

Regional cities like Wanganui had been zombie towns for decades.

They were then pumped by immigration and the resulting demand for housing.

However, fundamentally nothing had changed - there is was no thriving trade and commence drawing people in.

It was artificial. They are now left with the same resource base but with many more mouths to feed. Ditto NZ.

Wanganui used to be such a cool little town to visit ... but now they've got the " h " ... it sucks ... Whanganui ! ... pahhhhh....

This kind of comment is not ok.

lighten up cous.

... o ... wy not ? ...

Whanganui is a fantastic city. I don’t live there but my son and his family shifted to there two years ago. He bought a house there pre first lock down which in hindsight was a good decision. It’s a large section with a very nice bungalow on it in a leafy street. What is interesting is the large numbers of young families who have shifted back there from places such as the UK and San Fran. Why? Great housing, great schooling and very pleasant lifestyle. And don’t go on about gangs. Everyone has some part of that national problem. And a very nice climate to boot.

... I think theres plenty of jobs around , too ... several good manufacturing factories .... yup , it's an overlooked sweet little spot ... been twice & felt very warm & safe ...

No patched gang members in my home town. Not all towns have them.

Well, Whanganui means big bay. Wanganui means big Wanga.

Says you? Are we lining up GBH for some cancelling? Ohh I love the smell of melted gummies in the morning?

actually the h stands for hot - it's certainly a lot warmer than it used to be, often the hottest in the motu and the awa is blue blue

I had a Tui, in Wanganui!

... a bird , or a beer ?

Wheah, whight.

Good call

Am I naively looking at this as the market transitioning from investment to home owners? transitioning from tape measure to compass? I suspect there is a large gap between the two.....which will be filled by cash/equity rich investors who are hoping for one last sale... to home owners coming to grips with the fact they can't pay off thier mortgage in thier lifetime. Is the market to big to crash? If it is then we are committed to rising in-equality and therefore more social disorder. I have a friend.....her daughter has been offered a university biology scholarship as she is in the top 10 for her age nationwide......she has turned it down as she wants to become a real estate agent.

Balance - Your friends daughter can’t be very savvy re real estate IMO! Now is a really bad time to start in real estate. The boom is over and properties aren’t selling. Only very good and very well established agents will make decent money. Virtually all newbies and the lazy and incompetent will languish and eventually exit the business. Firms will still advertise jobs RE jobs though as they don’t care about that.

The young'uns are all like that - and I was like that - because you want to make big money fast. The more the make, the faster you lose it all until you become a bit more mature and dial it down a WHOLE LOT.

Would be smarter to hedge. Take the scholarship, study for the RE cert on the side, as it shouldn't be that hard to get.

The worm will have turned everywhere, stats lag is just not showing it.

The rent funded capital gain seeking frenzy, fueled by the lowest rates ever in NZ, has conspired to create the highest of tide's for land speculation in NZ. All other fundamentals are against it, income, immigration, record new construction etc etc. Add to that a endemic culture of tax avoidance and exploiting the basic need of shelter have created the highest house prices in the world. In little old NZ.

If it wasn't such a joke it would almost be funny.

It doesn't really matter what house prices are when you've bought your home for you and your family to live in. Even if it does go down, it'll go back up because all governments - including NZ - are pushing for more and more immigration. More people will just drive more demand and higher prices.

Colin - I wouldn’t bet on it going back up any time soon. Restoking the boom may not actually be possible now. It’s likely we will have low or negative net immigration for a long while as people leave for better opportunities overseas. Also these’s a massive number of new builds coming onto the market. Finally, FOMO and speculative demand, which fuelled the boom has evaporated along with the likelihood of capital gains.

Many people do not realise that the downturn after the 1970s boom took 16 years to recover from - almost a generation. This crash was masked by very high inflation, but real prices dropped 40%.

As Keynes was reputed to have said about the 1929 stockmarket crash, “The market can remain irrational longer than you can remain solvent”

solvent*

Thanks - fixed now

... I heard some employer chap on weekend radio , crowing that the borders were now open , that local employees need look out as bosses could pick and choose from the best overseas workers & new migrants ...

And I thought of " The Castle " movie .... " tell him he's dreaming ! "

... the borders are open both ways !

Michael Reddell reporting largest net outflow in 2 yrs for April - 19,708

It begins.

✈️ ✅

I actually think the the US will be a better bet for most than Aus, not that Aus is not a far better location for the young but it cannot match the US for opportunity and lower cost housing. A green card is not as hard as people think if you have the right skills.

The US is a wonderful place. If you're able to get a visa it would certainly be an awesome experience for a few years.

Wow...Someone might want to watch out for that fellow. Doesn't sound like a great person to work for. There are better employers out there.

Could be some good buys out there... fear is in the air.

... fear in the air is no where near a buying opportunity ... when the blood is flowing in the streets & gutters , buy ... peak gloomsterisation is a long way off ...

Indeed. On the bubble graph well into the "blow off" phase. We have just passed the final "bull trap", and we are now in the "fear" stage. Next is "capitulation" and "despair". When the outer skin of smug investors "Im so greatness" has rotted off, then the jucy tit bits inside are presented. Will keep stacking the vulture fund.

Kaarrrrkkkk.

I'm personally looking forward to the juicy tit bits :)

Steady GBH, I know we don't want to catch a falling knife but there are real price floors that take time to lower, the price of new house construction, mortgage repayment hurdle rates etc. If you need a place to call home getting in at new lower levels might be safer that waiting until the turn?

Well... is your money, feel free to use it.

Or was it an invitation? In that case I guess I'll still pass for another 12 months circa.

You ain't seen nothing yet...

attn Guy Mordaunt : could you please stop spamming my airwaves with your desperate & specious BS

Hope there's no popcorn shortages, she's gonna be a Grand Ole Opry.

The asking price data is very noisy and really only tells us what sellers *think* they can sell their property for.

What’s more interesting is the rising levels of stock. This is up in every region across the country, and some of the percentage changes are very notable.

The asking price is more interesting when everything is selling like hotcakes. Selling prices of listings that are months old only tell you what people are NOT willing to pay.

There is a lot of doom and gloom in these comment threads.

I notice that Printer8, CWBW, Luke83, TTP and their ilk are nowhere to be found.

I'm here in New Zealand BL, busy making money and realised I wasn't taking my own advice of remembering that this chat group is full of people with their own agendas with nothing to offer. Just read the comments on this today... What a joke, Bunch of moaning bi$&# .

Very good. Property prices still up 5% by the end of the year?

Yea I think some areas will see that, happy to say most probably won't though. However it doesn't matter what I say or anyone on here as its all bull sh&$ I hope the market stays flat for 2/3 years and gives us a more even market, however sadly I think we will be lucky if it stays flat/down for more than this year. Just my opinion. Spent several years living in Aussie so I see the appeal, however it's not for everyone for a multitude of reasons. Plus those hook turns in Victoria are confusing as hell hahaha

I think the prices will come down, but FHB's will still struggle to get on the property ladder. The affect of 7% inflation on their wages is a head wind that will not help at all.

Yea that and increases in rates are not great, we'll compared to last few years. Will settle down later this year, hopfuly few years of a more balanced home market

I notice that Printer8, CWBW, Luke83, TTP and their ilk are nowhere to be found. [Broke Landers]

You're wrong as usual, Broke Landers. I'm here.

You're also wrong about the prospects for the housing market....... It will prove to be far more resilient than you ever dared consider.

If I had property, I wouldn't sell. It's still a great investment for the future - especially in Wellington and Auckland.

TTP

I wonder how many have noticed that the property cartel has carefully avoided the use of the colour red in their charts.

Prices go up. It's green!. Prices go negative sideways. Its blue!

But never ever red. The horses must not be frightened.

Yes it is the DGM's day in the sun, and despite not quite getting any actual results worth celebrating (we are long, long way from starting to reverse the gains from last year alone -21%) we are partying like its 1999 lol

Get the violins out for these dreamers..

https://www.stuff.co.nz/life-style/homed/renting/128473376/roll-back-ch…

excerpt:

"To solve these problems and fix the crisis, the federation had developed a plan, King said. It will be released for discussion on Monday.

Part of the plan revolved around lowering costs for landlords to encourage supply and lower rents, and the federation proposed many ways to lower costs.

These included re-allowing interest deductibility, repealing ring-fencing provisions, returning the bright-line test to two years, taxing rental property at a 10.5% income tax rate, and making private tenants’ accommodation supplement equal to social tenants’ income-related rent payments."

"Other cost proposals included that landlords be able to charge interest or a fee on outstanding rental payments, making the cost of installing insulation and energy efficient heating tax-deductible, and that landlords should retain the right to charge a market rate without rent controls."

Are these guys investors or beneficiaries?

Property investors are one of the biggest beneficiaries in the country....yet oddly many like to tell their customers (renters) that they are lazy and lack the drive to 'get ahead'. Meanwhile he landlord takes their wages and expect tax payer funded accommodation subsidies and lower interest rates to cover the losses on their bad investments!

The sound like the embodiment of Entitlement Mentality.

I am sure National will rubber stamp this plan...it reminds me of a little kid in a candy store told to "help yourself"!!

Haha true. Why stop at 10.5% tax. Just make it zero, cause they're such good guys providing accomodation to the plebs. Why not chuck in knighthoods all round too.

They did!

Only thing I agree with on that list of proposals is making Insualtion and energy efficient heating tax deductible (should add solar power installations to that). Everything else mentioned would eliminate the impetuous behind the property market finally cooling down.

But those aren't running expenses they are capital costs, and what's more they are pretty basic conditions that should be there anyway if they are charging rent.

IMO the Govt handing out rent subsidies and working for families tax credits contributes in a major way to rents and housing costs being out of control.

Rent subsidies 100%. WFF not so much.

For example, take a couple earning the same combined low income before and after having children. In both cases this family receives accommodation supplement regardless of children, which raises the floor of the rental market. It is provided when rent is not affordable. It's a market support.

WFFTC provides tax relief for the family once they have had children. The tax credit does not go as far as to cover the basic needs of raising a child.

MFTC on the other hand is a credit to ensure families have a minimum income to afford food and shelter. This is ~$30,000. This model is closer to providing a "support".

Please explain how a family of three earning $30,000 could push housing costs to a median of ~$1m, and median rent over $26,000 per year.

Has the ball started rolling - price fall (If actually has fallen to last year price is real bad as it is just the beginning Has the ball started rolling - price fall (If actually has fallen to last year price is real bad as it is just the beginning :

https://www.stuff.co.nz/business/128481870/a-year-of-capital-gains-wipe…

Defaulting :

https://www.stuff.co.nz/business/128479669/about-400000-borrowers-behin…

Three weeks back prediction in Australia turning to be true :

https://www.dailymail.co.uk/news/article-10705987/Reserve-Bank-Australi…

Latest update :

https://www.macrobusiness.com.au/2022/04/anz-westpac-interest-rate-shoc…

https://www.news.com.au/finance/economy/interest-rates/cba-anz-nab-west…

Fed has not even begun raising OCR in true sense and fear has taken over and not to forget USA has bigger and diversify economy unlike NZ - where everything is riding on housing.

Finally asking prices has fallen by more than 10% for the first time.......and is just the beginning:

https://www.stuff.co.nz/business/property/128505952/its-a-house-buyers-…

In the mainstream media to boot. If the stress levels in Aussie start to bite, the Aussie banks will ensure their South pacific whipping boy pays more than it's fair share. Oh that's right, they already are... to the tune of Billions extracted per year.

https://www.interest.co.nz/property/113184/new-homes-are-getting-smalle…

A comment from that article

We build about 20 new houses per annum. Our 195m2, 4 bed, 2 bath, internal garage, all floor covering & 7.2kw heat pump tops out at $2442.00inc gst per m2. Excludes land; fencing; landscape

https://www.odt.co.nz/star-news/star-districts/star-selwyn/it%E2%80%99s…

A comment from that article

Examples included the 32-section Hanks Run at Rolleston. Sections in stage one, with an average size of 750 sq m, sold for an average price of $361,000 about two months ago. Sections in stage two, with an average size of 695 sq m, sold for an average of $385,000 per section about four weeks ago.

So acquisition price of a new 4 bed in Rolleston in the South Island - $476,190 + $385,000 = $861,190. In Rolleston.

Prices will lower but won't crash until building costs and land costs also reduce.

Think that's fairly well acknowledged, that building costs might not fall as much but land certainly can. If there are no buyers for the total package cost then how can one sell the land for that price?

I think prices will go down but I am just calling out that this is a brake on the speed of the fall.

If we start to see a large increase in Mortgagee sales then we will know that brake has been removed as well.

It is not a brake at all, simply the market solving the equation that house price = land + building, and therefore a section costs the price of a finished property minus the build cost. The equation will continue to be solved, with land cost dropping disproportionally as house prices drop (assuming prices continue to fall as they are currently).

Market forces will bear down on build costs. It’s very bizarre the way Kiwi’s talk about build costs as if they have to remain inordinately expensive. Necessity is the mother if invention and if a crash is painful enough, Kiwi’s still need work, labour costs will come down. The monopoly that keep building materials high, who rake in massive profits year upon year, may find they have to make a loss or less profit.

So input prices go up with inflation but the cost to the builder goes down? OK.

Prime example - do you think somoene is willing to pay 1m for this.. FHB are calling your bluff.

https://homes.co.nz/address/auckland/birkdale/1-8-abbeygate-street/WlenW

Vendors and buyers to some extent have been completely delusional. Everyone thinks their squalor is worth 1mil. I don't see it.

Holy fk moly - that right there is the embodiment of how unhinged this bubble has become and why many talented Kiwis will be leaving our shores.

Or maybe the argument needs to change to - yes, it will cost $1M, but what does that say about the value of our money? Looks like Grant and Adrian et al have planted us firmly in the footsteps of Venezuela or Zimbabwe. And remember how they always blame foreigners for their woes? I see us very soon as having $100 coins as minimum physical denominations.

In last two year the house prices have moved up so fast and high that slight fall is meaningless.

From $850000, average price in Auckland to 1.3 million PLUS .....wow..... and now,even if it falls to 1.2 million, does it make any difference....will just be hiccup.

20% fall is minimum to make a difference.

it makes quite a difference if you bought at $1.3Mil

i think we are close to those levels if you try and sell now... the question is how much is the drawdown from those levels if you don't take the offers around now.

Isn't there a graph showing a recession occurring within two years after a global event? Seem to recall its been tracked since WWI.

Might be over 24months now only because we kicked the can down the road.

Inverted yield curves and the Fed raising rates to slow overheated economies have been pretty accurate indictors.

TTS the bed

Anyone else see a soft landing?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.