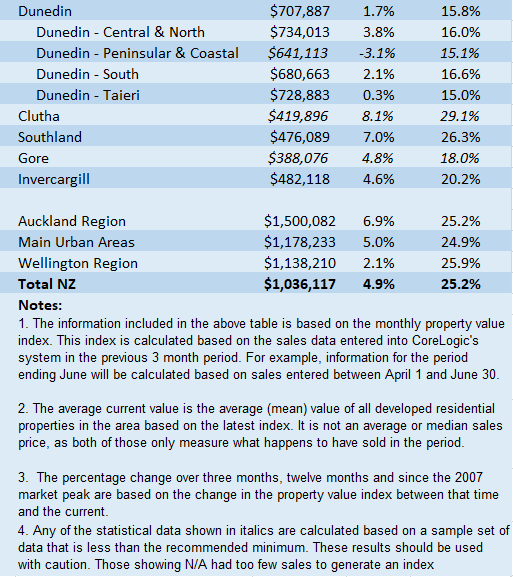

The average value of Auckland homes has pushed past $1.5 million for the first time.

According to the House Price Index (HPI) compiled by property data company CoreLogic, the average value of dwellings throughout the Auckland region was $1,500,082 at the end of February.

CoreLogic bases its valuations on sales data over the previous three months and updates its figures monthly. So the February figures are based on sales that occurred over the three months from December 2021 to February 2022.

Within the Auckland region there is now not a single district where the average dwelling value is below $1 million, with average values ranging from $1,054,716 in Franklin on Auckland's southern flank to $2,152,389 in central Auckland's eastern district which includes the affluent waterfront suburbs of Mission Bay and St Heliers.

Other districts around the country in the million dollar-plus club are Thames-Coromandel, Hamilton's north-east suburbs, Tauranga, Western Bay of Plenty, Porirua, all of Wellington City, Christchurch's hill suburbs, and Queenstown-Lakes.

The average value of all homes throughout the country is $1,036,117.

The table below gives the current average values for all major urban areas throughout New Zealand and shows how much they have changed over three and 12 months.

However CoreLogic warns that although average values are at record highs and still rising in many areas, the latest sales data suggests selling prices are declining and that will eventually flow through to lower average values.

"The national measure of housing prices was 0.8% higher in February, a sharp drop from the January growth reading of 2.1% and down from the cyclical peak rate of 3.1% growth in April 2021," CoreLogic said in its commentary on the latest figures.

"Given the Index incorporates sales data from the past three months, February's positive reading can be attributed to stronger sales evidence prior to Christmas.

"CoreLogic analysis of very recent sales, including unconfirmed sales, shows sentiment is changing rapidly, with vendors unable to achieve the prices of 2021," the company said.

CoreLogic's Head of Research for New Zealand, Nick Goodall, said he expected the HPI to start falling.

"Our expectation is the HPI will dip further over the coming months as continued [mortgage] rate hikes and tighter credit controls weigh on market conditions," he said.

"The significant drop in the monthly rate of growth from January to February indicates a clear change in trend."

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

108 Comments

Who's behind this corelogic article? Certainly someone who wants to keep the RE ponzi to keep going.

Seems like some in the industry are getting really scared now and putting all kinds of news in the. Media.

What's the real story?

From the article:

"The significant drop in the monthly rate of growth from January to February indicates a clear change in trend."

Doesn't sound like someone who is too desperate to "keep the RE ponzi... going" to me.

Facts don't matter anymore, what's important is that everyone is supposed to feel the same way about everything.

My view is that CoreLogic is no better or worse than the other housing market monitoring/forecasting agencies that rate a mention on www.interest.

CoreLogic's latest analysis is consistent with a soft-landing scenario for the housing market - following a buoyant period of activity.

TTP

hahaha - "soft landing". global pandemic, rising interest rates, highest inflation in 30yrs, war in Europe, record energy prices, supply constraint issues. "yep, soft landing - definitely" ;) hahahahah that made my day.

Hi there,

I trust the word "resilient" will also make your day.

TTP

it does. be quick! buy buy. property never goes down! the best time to buy is always now! ;)

The word "flaccid" makes the year as soft market conditions prevail.

Hi Brock Landers,

Kindly take your medical problems to your doctor.

They are not something that warrants discussion here.

TTP

Tim, you are so funny :) making us laugh since what......March 2017'ish?

Hi Amokk,

Property Brokers was deservedly fined for illegal conduct.

Price-fixing is a serious form of anti-competitive conduct in the marketplace. It worsens economic outcomes and leads to consumer detriment.

I have no respect for any business that engages in anti-competitive behaviour. The owners/managers responsible deserve to pay the price.

Sorry, Amokk, but it's no laughing matter.......

Find something else too amuse your petty mind.

TTP

NGK, you not liking the news doesn't make them fake!

NGK

Another conspiracy theory. You are really showing your ignorance.

CoreLogic is simply involved in collecting and reporting data and has no involvement in selling or marketing property; any movement in the market in either direction has no benefit to them.

Get well soon.

Just curious, are these two accounts the same person?

I only ever see them posting after each other.

Fake?? Jealous much?

this is a regular data release from CoreLogic, you don't like the data?

Isn’t this due to the kind of houses that are still selling. Watching the auctions it looks as though the top end of the market is still doing fairly well, with the lower value investor type properties being passed in. Therefore average prices could rise in a falling market.

Whoops

Hey Waikatohome, it's not because of that as it is a proper index which attempts (usually successfully) to remove those sorts of effects. The issue is that this data is based on settlements (not sales) in the three months to February relative to settlements in the three months to November. Being based on rolling three month comparisons means it is naturally lagged measure (e.g. some of the settlements will be from December and being compared to settlements that include settlements from September). Also, because it's based on settlements, it further lags current conditions (e.g. in my example those December settlements could have been sold (agreed, price determined) in November or October. The September settlements could have been sold in August or July. This is really outdated data.

Please use REINZ which will be based on sales in February and compared with sales in January (i.e. what we would expect) and uses proper index methodology to strip out compositional impacts.

Dig out the old school textbooks and brush up on variance, distribution, mean, and variance. One of the issues with any index, particularly if it relies on rolling averages or needs to be scaled to ensure depth of data, is that it's directional and not indicative of reality. Therefore, you need to be looking at the relationship between measures of dispersion and sales volumes. When sales vols are low, it turns into somewhat of a guessing game.

Perfectly put. The core logic dataset isn’t “wrong” or “bad”, it’s just slower to display recent trends and so shouldn’t be used over REINZ for looking at shifts in the market

Sales, as defined on settlement, are a very different measure as to sales as defined on the unconditional date. So we need to know which one they are using.

Also, there can be a huge time lag difference between the two.

Sales off the plan (unconditional) can be sold over a number of months leading up to a settlement date that could be up to 12 or 18months in the future from the first signed agreement, down to a couple of weeks prior to settlement for the last agreement, and yet they will all settle within the same month (or two) time frame.

Perhaps the CCCFA legislation has impacted the bottom end of the market?

I know it’s really difficult for FHBs to get finance now.

Just like the price of petrol is about 1.80 a litre in Australia and over 3 dollars in NZ, our house prices are crazy.

If there wasn't tax on petrol the price would be $1.50

Nah, don't think so. Most kiwis are loaded here because of recent years housing price increases. The fuel companies here know that most kiwis can afford higher petrol price. So even if the government is taken out tax, I bet petrol price wouldn't go below $2.5. That's one of the reasons RBNZ need to stop making excuses and hike OCR until inflation come back to normal as their mandate stated.

This isn't a thinking exercise. You can look up all of the taxes on petrol. 52% of what you pay is tax.

I never said it isn't 52%. But you need to understand how pricing works in a uptrend market, it's not as simple as when 52% tax being taken out, you get 48% of original price. There are factors like how competitive the market is, risk of cost increase...

If I have $3 and I give someone $1.56 I am left with $2.50.

You wot, mate?

read.

Did not compute.

Do I need to draw you a picture?

Or do you want to read the previous comments and then use your brain?

Please draw me a picture. Is it like Jesus turning water into wine?

This is a modern art masterpiece.

Kjeldcasso?

Haha, good drawing mate, you are funny!

If there wasn't tax on petrol there would be no roads to drive on so no need for petrol. Horses anyone?

Tax for roads can come from other places like capital gains tax that exists in every other OECD country. But no we need to squeeze our poorest with consumption taxes so that we can give asset owners a free ride.

On the basis of taxing what you want to discourage, I think high petrol taxes are a good thing as they act to encourage active and public transport, and living closer to work. I appreciate there is collateral damage, and would certainly prefer to see more capital gains and wealth taxes in place in income tax (on the basis that income taxes discourage work).

That really depends on if you think public transport is a good idea. And living close to work is a luxury that only the better off can afford. Ask your average office block cleaner living in Manurewa if they'd like to live in Parnell - I reckon we all know what the answer would be. They'd probably also really like to own a Tesla and pay zero road tax and minimal fuel costs, too. Plus lugging all their cleaning products and equipment in on a bike isn't really an option. Same goes for your shift-working nurses and orderlies. Public transport isn't 24/7 or reliable. So yeah, it's the working class that get hammered, and effectively subsidise the rest of us.

I do have sympathy for your point of view. However, given that oil is not a renewable resource I think it's crazy how flippantly we burn it at present, and would prefer us to move away from widespread individual car ownership.

I don't think that making petrol cheaper is the right answer to making society more equal - better to bring in a tax free allowance and increase tax on the wealthy to pay for it.

Better also to allow much more freedom to intensify closer in so public transport is more viable for far more people, rather than preventing it at a massive infrastructural and environmental cost to society. Makes no sense at all for us to actively cause people to live in a more costly manner and to require their own personal cars ...yet often we do this while pretending it's about giving people choice.

The tax has nothing to do with the use of petrol per se. As more people switch from ICE to electric, they will need to tax electric, which they can't do by charging a tax on electric use as most charging is at home. I presume they will charge via mileage, with maybe a minimum charge regardless.

As usage shifts there will absolutely be an electric RUC charge.

Yep just like Diesel that used to be way cheaper, they just end up taxing you so its the same.

Better to base it on an LVT on the unimproved value of land so that we have lesser need for paying for sprawling roads anyway.

Want to guess how much of the 52% tax at the pump goes towards roads?

If there wasn't tax on petrol there would be no roads to drive on so no need for petrol. Flying cars anyone?

Want to clarify your point, or it simply a whinge that you have to pay tax?

My reply was to a comment that stated the gas prices are $1.80 in Aus and $3.00 in NZ.

I stated that half of what we pay is tax. The obvious implication being that those prices are similar once you remove tax.

Since you didn't get the obvious implication here are the numbers:

Aus Petrol $1.80 - tax = $1.35

Nz Petrol $3.00 - tax = $1.48

If our taxes on petrol were the same then we would be paying pretty much the same for petrol (once you factor in exchange rates).

Complaining that we are paying taxes on petrol, no. Pointing out that we are paying more than triple the taxes on petrol than our dear neighbor, yes.

what about GST and incoming tax? oh right that is reserved for govt salaries and beneficiaries.

One of our more special commenters whinged yesterday that people were leaving New Zealand because they "hate their country" and "good riddance, won't be missed".

One glance at the basket case numbers above and it's clear the real problem is that their country hates them.

It feels like dejavu - another year starting with commentary and predictions about house price falls yet prices continue to go up? Nothing can stop kiwis by the looks of it...

Auckland - Manukau $1.3million...LOL

It is important to know that the data from Corelogic is lagged and smoothed - so it makes sense that it still shows rising prices as it reflects conditions a few months back when prices were rising (see explanation in a reply further up). Prices are definitely falling now though across many regions (not all), and nationally. I await the legit data - the REINZ HPI (not the median) - to see whether this has continued in feb.

While I value interest.co.nz, I am always a bit disappointed when they report this data as 'news' as they understand the limitations.

Yes! I feel exactly the same re the reporting of this data. It needs a Facebook-style disclaimer so people don’t go hanging their hats on it without context. For those who don’t understand the nuances of the data and its representation, it’s just plain confusing to have a news article one day talking about two months of declines and a likely market peak, only to have this metric a couple of weeks later suggesting the market is still going up.

The reason so many measures and indexes exist is so that the real estate industry can cherry pick whatever suits their agenda and feed it to their bought and paid for media.

oh something is going stop them alright. its called interest rates - i understand they are coming back.

More evidence of the uselessness of Core Logic's lagging data for any sort of timely analysis.

Agree

CoreLogic's data is useful because it gives an indication of what to expect from REINZ's data when it comes out... Which at that point will also be lagging.

At that point we will be looking at data relating to the annual cyclical dip months but we will be moving into the annual cyclical peak months.

None of the data ever reflects the current moment in time which is why people like to kid themselves with Auckland's daily auction figures, looking and hoping to find their prefered direction of change.

The number of property price analysts saying that 'property will peak soon' just relentlessly increases every year.

And rightly so. The market can remain irrational longer than you can remain solvent, but when it wakes up to the (not so) freshly brewed coffee, it happens all of a sudden.

*irrational

Whoops, fixed, ta.

It's quite strange to say something will peak soon when it is declining :)

Surprising that Corelogic's values are still rising over the 3 months of December, January and February when REINZ's data is down for December and January (February to be released mid March).

Not surprising at all. If you put a 3 month lag on the REINZ index, hey presto, you have the Core Logic index. Quite comical they expect the index to peak and start dropping soon. I can also state with a fair degree of certainty what's already happened.

rjn

There is the time when a property goes unconditional (basis for REINZ data) and the sale is completed (basis for CoreLogic data) which can typically be four to eight weeks.

Indeed. Add to that a bit of data smoothing and you get a roughly 3 month lag.

P8, I think your explanation is on point, rjn's doesn't make sense to me

That’s funny, because they are essentially the same explanation. I took for granted that people here know the difference between unconditional contract and settlement data, and the timing lag between the two. If you just looked at raw figures, you’d get a roughly six week lag as suggested (average settlement timeframe), but the additional lag is most likely explained by data smoothing, either that or they must be looking at different markets.

There was also the recent phenomena of much longer settlements due to sellers needing time to find the next place to live

rjn, only P8 commented abut the difference between the time when a property goes unconditional and the sale is completed, you did not, so no, not the same

Because everyone here knows that already, it’s been done to death. I was commenting on the derived effect of this, sheesh.

Interesting to see Queenstown down -4.7% over 3 months. Annualised, this is starting to get up there.

Looks like the egg is firmly TIG welded onto the mouse for it's lifetime, the Mexican math examiner failed his own test and Dr. M's noise theory fell apart like extraterrestrial sighting claims.

And I told you so!

There's still room for upward valuation.

🚀 Be quick! 🚀

Congrats...?

Thanks, but I'm not into flattery.

... This makes even less sense than usual. Literally just ad hom and a self-referential trope?

I made the list, how exciting. You may also remember the entirety of your claims in that bizarre thread were based on B&T auction sales prices in the first week of February, which bares very little relation to the data Corelogic are presenting today. Certainly today's release doesn't provide any support for your claims, as I expect (hope?) you would understand.

We will see whether this data series in two-three months reflects your expected double figure monthly increases in Auckland prices, or we can just wait for REINZ in a couple of weeks.

https://www.interest.co.nz/property/114277/buyers-are-being-more-cautio…

Go easy on the guy. Dementia is a terrible disease.

Terrible comment, my dad had dementia, I can assure you it's no fun at all, some days he didn't even recognise me : (

Sorry to hear that. As I said it's absolutely terrible.

Good grief are you genuinely this stupid, or just really dishonest? Corelogic data uses settlement figures which lags sales data by several weeks. It’s also an aggregate of 3 months rolling data.

The figures in this article won’t contain the sales figures for barfoot auction results in February. Jog on

Reading the headline I gasped and almost choked on my coffee...

Bahahahaha

Oh no, this doesn't fit the story line that we are in decline.... Wait for all the tears.

Tell us you don't understand this index without telling us you don't understand this index.

I’m ready to give up expecting a bit of critical thought from the permabulls.

I understand just fine Mr Landers, I'm saying there is a group of doom merchants that will be activated by this heading, now jog on.

An appreciation of reality doesn’t make one a DGM. The reality is, property prices are in the process of correcting from a peak that anyone with a pulse knew was unsupported by fundamentals. Yes, some of us are ‘activated’ by misleading data that has the potential to drive poor decision-making.

I mean you are right. I was activated by this heading. (Although I'm not a doom merchant, I'm just aware of the recent better-quality REINZ data).

"CoreLogic analysis of very recent sales, including unconfirmed sales, shows sentiment is changing rapidly, with vendors unable to achieve the prices of 2021,"

I love the smell of financial stability in the morning!

Perhaps everyone should wait for the March - May figures before jumping to any conclusions. If the way they "Measure" these things doesn't change its all you have to rely on so if it doesn't fit your narrative don't go looking for reasons why. It looks pretty clear there will be a decline in the average house price by May, how much remains to be seen.

No real need to wait, better to be forearmed and run with the smart money. Just look at up to date data and leading indicators like Tony Alexander’s surveys (particularly the one coming out tomorrow in which the majority of agents say prices are dropping) and the picture is very clear.

Indeed

The problem with waiting until May is that the actual achievable sale price of your house could have easily fallen by 10-15% by then.

Waiting for r.e. data is like driving while looking in the rear view mirror. Makes it difficult to avoid a crash.

Be quick!

I monitor the Hutt Valley Market and can confirm that the decrease in house prices is in line with what I'm seeing. Core logic is showing a decrease of 1.1% in values over the last 3 months - the highest decrease across any market. Lower Hutt has the highest number of houses on the market since 2009/ 2010 (when 700 were for sale) and a high number of new builds/ off the plan coming to market (approximately 100 listings). Interestingly it also has 155 houses for rent the highest seen in the last 5 years.

As of today 570 houses on the market - (average is 40 sold a week - currently seeing around 30 been sold a week) so roughly 14 weeks SOH at 40 - 19 weeks SOH if 30 is the true number (will get a better sense when the REINZ report is released)

341 of the houses have been on the market for more than a month = 57.6%

190 of the houses have been on the market for more than 2 months = 33.3%

230 houses are now listed with a price - of which around 60% have reduced their prices since listing. Average price reduction has jumped from 70K last week now to 72.4K. I am aware of 3 houses that have reduced their prices by > 300 K - one was listed at 1.5M, another 1.9M and another at 2.5M and are all now listed 300K below this.

Approximately 75% houses with a price are now listed at a price below their QV valuation and QV valuations fell in the area by 30K from Jan to Feb.

4 houses with a price greater than 950K have been removed from the market- unsold and rented in the past week.

Interesting. I thought there were heaps of rentals too but in practise when I was trying to find a rental in the hutt late december many of the rentals listed already had applications and no viewings. In effect you were joining the backup queue. Out of 12 or so on my list I could only view two, and of those chose the cheaper one which I was accepted for-Probably due to having history with the same rental company. Otherwise Id be in a tent.

Interesting but the picture is not the same for everywhere in NZ. Tauranga is still WAY down on listings compared to 18 months ago. Yes its slowly climbing but its 880 vs a peak of nearly 1100 when I was looking. This tend to suggest that price shifts will be highly regional.

So much negative doom and gloom rhetoric.

Can we not all just take a moment to celebrate this new milestone in how much wealth we are managing to extract out from younger generations of Kiwis by saddling them with ever greater debt?

Geez...next someone will start to suggest something like that we should focus on making housing more affordable, not getting young people to pay more. Ridiculous carry-on.

@ RickStrauss ....alot of the young ones are looking at UK/Eur, Aussie, North America etc and have either left or are making plans now,

If I was in their shoes with these house prices vs. salaries, I would be doing the same.

The property bulls hate it, as they can see the "fodder" for their "ponzi scheme" leaving the country - but the Labour gummint will come to their rescue and open up the immigration floodgates ....and it continues......just "crazy" says the Crazy Horse !!!

It is shameful that a so-called socialist govt refuses to admit a correction is necessary. As a valuer, I am deeply disappointed that govt interference has manipulated this market since prior to 2008 really, probably longer.

We are massively overpriced, in the order of 40%, and I wouldnt touch the NZ market with a barge pole, especially if Putin gets away with this latest move. China will be watching and if the West doesnt show some strength, it will be Taiwan then onwards across the South pacific.

I watch the market daily and I can tell you it is definately on the way down. At the rate it is moving I think the Banks estimates of a fall of 3-7% this year is too light. 10% would be a good start , but with inflation running at circa 6% it needs to be a lot more.

This generation is unaware that in the 1970s the NZ market fell by over 30% over 7 years so it can, and should happen.

The picture above couldn't be more prophetic. Down the creek without a paddle - that's all of us by the way, not just the housing market profiteers, but our whole way of life. Why? Because not enough people have broken free of the mainstream hypnosis that will be their downfall.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.