Barfoot & Thompson's auction rooms continued to get busier last week with more properties being offered at auction but unfortunately the sales rate continued to decline.

Barfoot's auctioneers offered 135 residential properties for sale in the week from 29 January to 4 February, up from 90 the previous week and 60 the week before that. Barfoot & Thompson is Auckland's biggest real estate agency.

However buyers appear to be remaining cautious at the start of the year and auction sales were achieved on just 36 properties, giving an overall sales rate of 27%.

That was down from sales rates of 38% the previous week and 42% the week before that.

We are now approaching the busiest time of year for the residential real estate market and these latest auction results support a recent statement by economist Tony Alexander that we are in a buyer's market.

Vendors can no longer rely on readily available cheap credit and a lack of listings to drive prices higher and will now need to pay more attention to getting their price expectations aligned with the current market, and focus on choosing an agent with good post-auction negotiating skills to get the best result.

Around the Auckland districts, three of them, Rodney, Papakura and Franklin, had no properties sold under the hammer although the number of properties offered in each district was low, while the sales rates in the other districts ranged from 21% in Central Auckland's leafy suburbs to 36% in Waitakere.

You can the see the results of all of the auctions monitored by interest.co.nz on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

176 Comments

Vendors should have been quicker?

Be quick! ;)

CWBW been noticeably absent in these articles..

As we've learned from past cycles, a fall in sales volumes does not mean that prices must also fall.

Currently, the signs for a soft-landing are evident and that's what's likely to eventuate...... But you already knew that.

TTP

Yes, you can't guarantee that a fall in sales volumes will lead to falling prices. You have to look at the data that prices are falling for that:

https://reinz.co.nz/Media/Default/Statistic%20Documents/2021/Residentia…

We have also learnt that constantly falling interest rates over a decade, to unprecedented lows, pushes prices higher.

We are about to learn what happens when rates start rising again.

Interesting that the RBNZ sets the interest rates but has no remit for stable house prices, which it could control very effectively using interest rates. It does however have a strong remit to control the price of things like petrol and anything containing a computer chip, which interest rates have next to zero ability to control. Crazy world huh.

This is really underrated as a factor. It’s a massive blind spot for some.

Over 3-4 decades, actually.

Yes - one of the major factors in the 'house prices double every X years' narrative - another being previous bouts of inflation meaning the doubling is not always in real terms. All the data that goes into these NZ rules of thumb are based on times of steadily decreasing interest rates, and longer datasets from other countries show real estate performing far worse. NZ may be looking forward to some reversion to the mean.

Agree if you look back before 1990, in real terms, house prices were flat for the previous 100 years. 1990 to now is the anomaly, not the norm.

You can fool yourself with recency bias in the short run.

It's very easy to double something every 10 years if you halve the cost every 10 years. I.e. the debt.

There's recency bias, something that afflicts many probably well meaning but limited economists and commentators, and then there's 'spruiker bias'.

So what if it's flat in real terms? Your debt gets inflated away.

That’s the point, in real terms housing returns has been massively above inflation for the last 20-30 years…an anomaly, not the norm. A bubble - could be…If we have flat nominal prices now for the next 5-10 years with inflation at 5-10% to ‘inflate away the debt’…we have a bubble that is bursting in real terms.

It’s the opposite of what we’ve just experienced where prices have been rising say on average 10% per annum the last 10 years with inflation near zero. Real returns have been exceptionally frothy - like crazy frothy…never seen before frothy.

Why? Because central banks kept lowering rates to allow more debt to be created against the housing market and to avoid deflation. Eventually in that process there is too much debt and central banks can’t raise rates even if they want to to control inflation - that is where we find ourselves. Also known by Dalio at the end of the long debt cycle…which typically last 75 years…and it’s been 75 years now from Bretton Woods.

Why? Because central banks kept lowering rates to allow more debt to be created against the housing market and to avoid deflation.

...as in CPI deflation. We've actually not come close to actual deflation, just as measured by CPI. The whole system needs an overhaul - and we shouldn't be scared of the price of consumer goods going down over time. That is the product of technological advancement!

Allowing the central bank over the last 30 years to pump house prices far above inflation annually. No dramas…

Agree system needs massive overhaul

Im glad someone gets it.... CBWZ or whatever his/her name is should take notes.

We are about to learn what happens when the following things converge:

- Rising interest rates

- more barriers to lending care of CCCFA etc

- close to zero net migration

- large amounts of new housing supply being completed

- soaring construction costs.

- household budgets being squeezed by high inflation

Anything I have missed?

Anything I have missed?

FONGO

Well googling fongo for meaning produces some seriously weird/dodgy results. I'm assuming you were meaning fear if not getting out...

Removing interest deductibility for investors and potentially DTIs crippling their ability to borrow more (may be covered by your 'more barrier to lending').

Omicron and any future plot twists...Natural disaster?

I think you missed question marks around :

- Rising interest rates

- close to zero net migration

- Almost everyone thinks they will continue to rise. I am less bullish than the vast majority but I still think they will rise circa 1%

- net migration has been very low for the past two years, and is likely to remain so for the rest of this year. Even if immigration increases, emmigration will too. I agree with Tony Alexander that many young kiwis will move to Aus

Inequality will rise as OCR rises. The RBNZ says the opposite about OCR cuts...

https://www.mpamag.com/nz/news/general/rbnz-directly-links-cash-rate-cu…

We already know what happens. When interest rates go up, home prices stabilize and correct mildly. However what has happened is that when interest rates goes up, economy stalls, and then the government lowers them again. This is time and time again the fact.

The days of double-digit interest rates are gone.

Agree. Normally it is buy the dip but if this trend continues for sometime, could be different as this are not normal times and asset class, be it stock or housing has actually been pumped up like never before only because of generosity by central banks and government unlike earlier.

Also first time when central bank have run out of ideas and no longer able to manipulate or kick the tin that they have been doing since over year by coining the word 'Transitory Inflation' to deflect despite all data and infirmation was pointing towards ponzi.

Now the only excuse to defend themselves is SUPPLY ISSUE (though an issue) which too will prove to be a farce - another Transitory Inflation.

Supply is an excyse but not the sole reason for the situation which has been created by least regret approach of centeral bank.

The clever people have left the RBNZ.

Don't you love how people are so cynical hoping and praying for a housing crash - when history always has shown the housing market stays resilient even after a correction (small or large). In the long run, unless you can convince citizens of this Earth a better tangible investment, they will always continue to buy homes/land as a storage of wealth.

A housing "crash" will not happen, especially when lending continues to be tightened and borrowing gets more difficult. No other investments offer a big enough return (stocks, bank term deposits, rolex watches, precious gems, gold, etc.). With so much money out in the market after the pandemic, the cash has to go somewhere.

The best part about the inevitable correction is that it's going to blindside so many people that refuse to believe it's possible for prices to fall.

I'm going long on popcorn.

‘A housing "crash" will not happen, especially when lending continues to be tightened and borrowing gets more difficult.’

Oddly, these are the exact conditions that occur during a crash/cause/result in a crash.

Yeah I couldn’t understand the point he was trying to make here. When credit contracts, prices are more likely to fall.

You lose credibility when you define an event that has repeatedly occurred as being impossible. You cannot claim that a crash will not happen; it's just your apparent desire for one not to occur that you're reflecting. We're in unprecedented territory and any credible prophecies should incorporate the many future uncertainties of how this plays out.

His desire comes from having bought his first home last year, at what was probably the peak. Which kills his little plan on leveraging equity into an investment property.

by 7jai | 4th Aug 21, 12:17pm

Hope prices continue to rise. As part of a big cohort of FHB who were able to buy these last few months, I would like to see my only asset appreciate in value.

https://www.interest.co.nz/property/111618/barfoot-thompsons-july-sales…

by 7jai | 24th Mar 21, 5:59pm

Not hurting myself. Not a property investor, but after this news, I do hope prices fall, because I have been looking at ways of buying a 2nd investment property but the prices were too expensive. Super excited about what's to come!

https://www.interest.co.nz/property/109663/prospect-home-ownership-has-…

Makes sense. Good sleuthing Nzdan!

Not accurate.

Accross the developed world thier have been dozens of property bubbles burst over the past 50 years.

Don't confuse can't and won't with not observed in your local market yet.

Also don't expect a sudden move. The adjustmemt will like play out over 1 or 2 years.

I'm personally waiting with a vulture fund ready.

Totally incoherent, and wrong.

At least he has stopped using -7 at the end of every post. I thought he’d realised it was dumb… but then I read the content of the post. He lost me at Earth I’m afraid.

I don't disagree that property is a strongly emotional asset class for many cultures that means that it can stay overvalued for many years. But your second paragraph view is highly debatable. "A housing "crash" will not happen, especially when lending continues to be tightened and borrowing gets more difficult." Those conditions will almost certainly cause a housing crash.

Just buyers remorse and wishful thinking from a FHB who bought last year.

by 7jai | 4th Aug 21, 12:17pm

Hope prices continue to rise. As part of a big cohort of FHB who were able to buy these last few months, I would like to see my only asset appreciate in value.

https://www.interest.co.nz/property/111618/barfoot-thompsons-july-sales…

Ouch

Should have sold in November - December but greedy vendors waited for the busiest time of the year to get more money.

Greed can never be controlled. Do they have plans to spend the millions they are going to profit from the deals?

Anyway in the end, everyone is in the casket empty handed.

But yes keeping aside the philosophy of life, i would like to see some normality coming to the market. The assests should appreciate but they should appreciate based on well being of everyone around them. A balanced society is a happy society. And don't we all just like to be happy and raise our families in a safe and happy environment?

Let's try to not be greedy.

Totally agree the smart investors would have left the market a few months ago but a number of naive pundits on here who give people bad advice pushing FOMO and trying to get other users to over extend themselves look quite foolish when interest rates are raising inflation is high and NZD is tumbling the only way this housing market is going for next few years is down. I understand these naive pundits have never seen a downturn so will be a green,the best thing to do is just have a laugh at their comments and move on.

Blood is in the water - no doubt. On the backdrop of the busiest time of the year it's hard not to agree that the market is in decline. ]

However I'm sure our regulars will do just that though....

20% decrease is about to arrive.

Still 27% is high, either the buyers cannot wait and in some kind of urgency or the expectation/selling price is compromised by vendors.

Prices rising or falling makes little difference to an owner occupier (assuming decent equity). If you are buying and selling in the same market it makes little difference. So there will always be people transacting in the market

Actually, if you’re selling into a falling market, you could pick up more value for the same cash.

That's why everyone should have at least 2 to make a difference.

If everyone owns 2 houses, who rents from you, or just leave half the housing stock empty as a pure capital/speculative asset.

That's the part you don't get.

Not everyone can make it to have 2 and some will have more than 2.

2 is an ideal target to aspire and there will always be a drop out rate.

Too complicated for you?

So just to be clear…. you say ‘everyone’ should have 2, but then say this is also impossible because everyone can’t have 2.

I think this logic would be too complicated for even Einstein himself.

If everyone owned 2 properties we would have zero supply issues (massive over supply) and there would be no demand and prices would plummet.

Sure you’ve thought this through?

The qualifier is "should", it doesn't mean everyone is able to.

It's not my message that's an issue, it's your comprehension.

But everyone shouldn’t own two houses because if it were true, your investment theory is dead. There are no renters and there is no lack of supply, Which you said yesterday was half of your portfolio and was crucial to the investment strategy.

So your ‘should’ is really a fallacy to distract from yet another misleading comment. Should everyone own two homes, homes wouldn’t be worth much as there are two for everyone!

Nothing wrong with the comprehension - thanks 🙏

I have a home owner friend who wants to trade up to a bigger place. He is struggling to sell his place because the auction rates have dropped, and the places he wants to buy are an even bigger step up in price than before the price explosion, so he is needing to arrange more borrowing than he would have a few years ago. So the changed market is not neutral to him.

Sorry I didn’t make my point very clear, when I meant in the same market I was also referring to not doing sizeable upgrade/downgrade.

Definitely aware of rising prices increasing debt burden on people upgrading houses. It is why the idea of rising prices are good for people “climbing the property ladder” is such a pernicious idea

We successfully traded up in November/December just been. If we had done so 12 months prior, we would have had double digit attendees at each open home, however we only had 3 viewers across 2 weekends and 1 offer which was at the lower end of our range. Thankfully we still walked away with a good chunk of change.

Other properties that came onto the market in our old area not long after we listed are still sitting unsold, it feels like we scooted through the door just as it was slamming shut.

27% is really low. When we were watching the last lull in Auckland this was the bottom.

Of the 43 sold since the beginning of February, the median selling price is $1,341,000 compared to month of January's which is $1,180,000. That's a growth of 13.64% in terms of value exchange even for a traditionally slow week of the year.

For a comparison, in the same week of 2019, the auction clearance rate was 32% and that was pre-pandemic without the current hurdles of DTI and CCCFA.

Hoping sellers would budge is naive as fellow ✊ Kiwis are know to have diamond hands ✊.

The market is currently doing exceptionally well given policy makers' attempt to break the market to appease the sub-segment of envious voters.

This chart demonstrates the current market momentum.

Just a side note to credit my finance and computer boys, they had managed to come up with a forecast a while ago that's on the money. To appreciate how impressive the feat is, the forecast was 8 months out and they hit 7 correctly- and here's their homework.

Houses in NZ indeed doubles every 10 years and here's the proof- the sinusoidal wave is a beauty and I almost assigned a function to it and carved my name on the new theorem of NZ house prices.

Make no mistake, your next credit approval is uncertain and waiting will cost you very dearly.

Buy everything and anything before you aren't able to.

🚀🚀🚀 Be quick! 🚀🚀🚀

Wow, just wow.

How convenient that the graph only commences at the start of the 90's...

Nice try but you need to go back to school.

The further in history you go, the less relevant is the data to its present.

We could have only have a 15 years range which is even more relevant but people like your kind would again claim it's too short.

Sometimes it's better to ask nicely than to confirm your own ignorance- it's never too late to learn if you know how to be polite.

"The further in history you go, the less relevant is the data to its present"...........at the risk of being fooled by recency bias.

You are misapplying psychological concepts again- do note that in the commentary sections there are real professional psychologists and psychiatrists and I bet they're having a good laugh at you constantly going around diagnosing other people with psychological diseases.

Market structures do not change overnight.

Oddly that is exactly what a psychopath would say when exposed as telling lies to the people around him or her (attempt to get the group to laugh at the person who has caught them in order to silence them).

Here's a good book if you want to better understand yourself and others.

https://www.goodreads.com/en/book/show/49127387-surrounded-by-psychopat…

Recency bias is a not a “psychological diesease”

But it is a concept in psychology.

haha, you're shameless mate. By that logic house prices actually increase 30% per annum as really we should only analyze the past 12 months data as 30 years is irrelevant...

That's why I say you need to go back to school.

They will teach you how far to go back in time- according to my boys, there are actual formal tests for it.

Ignorance is the seed of tribal hostility.

Nice ad hominem attack there mate, no counter argument at all.

That chart only goes back to 1992?

Why bother with the boys in the basement if property just doubles every 10 years? Hardly needs analysis right.

Property investors tell me its 7 years, not 10...so guessing we will be getting close to $3million median in Auckland by the end of the decade if true.

Hi IO,

Note that a median price of $3.0million + has been reached in some Auckland suburbs already.

TTP

Thanks for the enlightening comment TTP.. so those houses will be worth $6 million in 7 years according to this bullet proof theory.

I think currency wars will have started by then if we (and the Fed) have managed to devalue the NZD (and USD) by that much in those 7 years…

Certainly not impossible but we will be paying $10 a litre for fuel by then and the RBNZ still won’t have raised rates!

Hi Utah, the ability to interpret information is crucial in decision making. It also debunks conspiracy theorists and the ignorant.

We want to know if a trend holds and how well it holds throughout the time periods and its cyclical behaviours. With analysis, we can test it.

Therefore, your assertion that no analysis is required is incorrect.

For your first question see previous comment.

Like your analysis of an accounting reporting change being the trigger for a bearish stock market?

Pull the other one.

What does the NZ50 composite consist of?

The more you dig the deeper you find yourself.

The more you dig the deeper you find yourself.

Quite!

That chart only goes back to 1992?

1992 is Year Zero. Ashley Church had a revelation when scouring quotes from a Bible and remembering meeting a Jewish person for the first time.

Clearly a troll comment with such biased selection of data - house prices prior to 1990 were flat in real terms for the previous 100 years. So lets ignore that (at our peril).

I'd being called worse things than a troll for 30 years.

Just to share a secret with you, nothing brings me more joy than to see name callers get it wrong.

It takes a troll to assume others are.

I'd being called worse things than a troll for 30 years.

I know what happened in 1992. You're not that clever.

Inflation targets?

Financial deregulation

Migration policy and immigration numbers changed around then too.

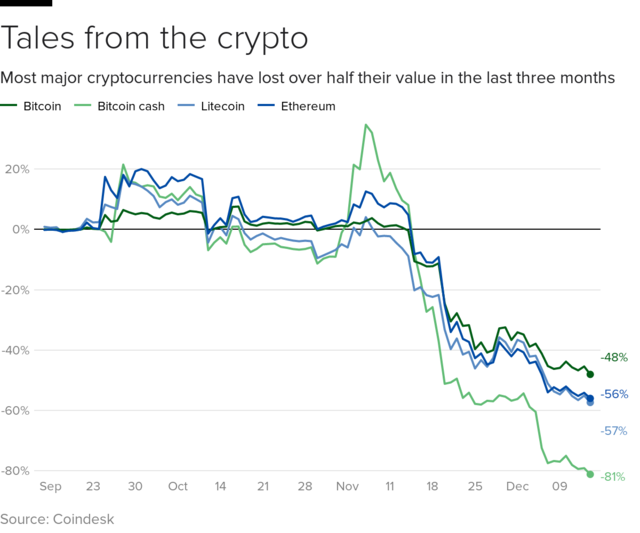

"Houses in NZ indeed doubles every 10 years" shrewd observation. Here's another - cypto loses over half its value every 3 months here's the proof!

{kind=link}

🤡🤡🤡 Be silly! 🤡🤡🤡

Aucklanders are coming to Otorohanga- you may need to pull out the red carpet.

Sold the red carpet so we could afford to buy cheese.

LOL what is this crap? A bunch of numbers made up to suit a narrative is what.

You have some real issues CWBW.

I must admit some of these things are hard to comprehend.

Perhaps it's was the right decision on your part to adamantly stick with Bitcoins.

So you are claiming "Houses in NZ indeed doubles every 10 years", based on your data, if I bought my house in 2007, was the price of my house doubled by 2017?

Be quick! ;)

If you bought at the median at 105K at the beginning of 1992, by the end of 2002 the median is 191.5K.

That's +82.4%.

Almost doubled. If you want to whine about the 17% then go ahead and time the market if you think that good.

(Note: Nice try on ghost editing from previous 1992- 2002. Even if you bought in the beginning of 2007, at the end of 2017 it's still up 67.2% despite you choosing the worst year in NZ recorded NZ housing on this web.)

Okay, I did put 1992 and 2002 before, but how about from 2007 to 2017? On 30th Nov 2007, the median price was 355k. By 31st of Nov 2017, it was 540K. Was this doubled then?

Is average very hard to understand?

Even if you bought in the beginning of 2007, at the end of 2017 it's still up 67.2% despite you choosing the worst year in NZ recorded NZ housing on this web.

I am glad you recognised that. And that's my point. Because of that your statement of "Houses in NZ indeed doubles every 10 years" is not true and biased. It's the same that if I am claiming house price increases 60% every 10 years, which is not true and biased. And there are reasons why 2007 is the worst year in NZ recorded NZ housing. I think you know why.

You're going off tangent again.

The keyword is average.

If you don't get it even after this, you won't.

Lol, try to use an "average" growth on "Median" house prices of "whole" New Zealand based on just a selected period of time to approve your "housing price doubles every 10 years" claim? Sorry mate, it's biased...

“Of the 43 sold since the beginning of February, the median selling price is $1,341,000 compared to month of January's which is $1,180,000. That's a growth of 13.64% in terms of value exchange even for a traditionally slow week of the year.”

can you point to the data that you got this information from?

Latest Auction Results: Barfoot & Thomson 1 - 8 Feb.

Date Auction sold price

1-Feb $1,240,000

1-Feb $1,100,000

1-Feb $1,155,000

1-Feb $1,450,000

1-Feb $1,060,000

1-Feb $1,556,000

1-Feb $1,360,000

1-Feb $975,000

1-Feb $900,000

2-Feb $1,350,000

2-Feb $781,000

2-Feb $1,250,000

2-Feb $1,312,000

2-Feb $1,390,000

2-Feb $895,000

2-Feb $1,185,000

2-Feb $1,341,000

2-Feb $1,838,000

2-Feb $940,000

2-Feb $4,004,000

3-Feb $1,425,000

3-Feb $1,530,000

3-Feb $1,558,000

3-Feb $1,393,000

3-Feb $859,000

3-Feb $962,000

3-Feb $1,850,000

3-Feb $1,040,000

3-Feb $1,868,000

3-Feb $635,000

3-Feb $1,615,000

4-Feb $1,250,000

4-Feb $1,925,000

4-Feb $1,985,000

8-Feb $816,000

8-Feb $1,150,000

8-Feb $1,435,000

8-Feb $938,000

8-Feb $1,859,000

8-Feb $730,000

8-Feb $2,650,000

8-Feb $1,391,000

8-Feb $1,435,000

Median to date (February): $1,341,000

Median (January): $1,180,000

Growth: 13.64%

As you know, median measures have limitations.

In 2022, I will assess things by looking at the HPI.

The median may not fall much if at all if there is a dropaway in lower priced new build townhouses being sold because of a slump in the development sector.

That could totally distort things.

People don't buy and sell houses based on an index, they buy in real prices in real dollars.

Lame answer.

We are talking about indexes as a measure (albeit imperfect) of the market.

I dare you to say I am right, for once. I have praised / liked your comments on some occasions, I am mature enough. How about you?

Let me ask you a question.

Do you go to the supermarket with the CPI numbers in hand to determine the cost of inflation that accurately reflects the impact on you and your expenditure?

I won't fail to give credit when it's due.

You are willfully discarding useful compiled data and claiming that anecdotes are more powerful. As someone once said, "the ability to interpret information is crucial in decision making".

Not discarding data, instead decomposing it.

The HPI index can neither accurately capture nor predict what's happening in Barfoot and Thompson's auction results.

That is why when you want to know what exactly is transpiring, you need to go to BT results rather than using the HPI to infer what's going on with BT.

The Corelogic's HPI is an old school real estate indexation and there're more out there (even Wheeler came up with one).

If you understand how HPI is calculated in detail, you'll find that its power to infer is limited and sometimes misleading.

He's just proven what a piece of work he is.

Quotes the numbers and indexes when it suits him, obfuscates (a polite way of putting it) and puts forward disingenuous arguments when it doesn't.

He's just a troll, although he's smart enough to pull some decent tricks out of the hat unlike many trolls.

Just don't bother responding.

Exactly. I erred and got lured in by the troll.

From REINZ:

"Data on median and average house prices is open to being skewed by market composition changes. This means observed changes in these values could be almost entirely due to the changed nature in the underlying sample (e.g. an unusually large representation of high end housing sales) rather than changes in the true market value. The REINZ HPI takes many aspects of market composition into account resulting in greater accuracy"

Median may be most robust than mean, but why not use a well developed index instead?

Because market participants do not buy sell based on an algorithm of indexes to determine the final value that they are willing to pay.

In a free market, participants are free to determine the price of goods and services and manage their own price discovery.

Artificial and generic indexes cannot provide precise valuation for goods and services at individual levels or determine the user's final utility.

Of course they don't - that's not the purpose of an index. But you are trying to compare date from one month to another, and choosing 'median price', when this is precisely the purpose of the index - analysing trends.

The only think your data has going for it is it's more timely as the HPI only runs to December so far, but you must acknowledge its limitations.

I think you will need more clarity on how Corelogic actually calculate their HPI.

They'd have to be doing a hell of a job to produce a worse series than 'median of the auction successes by a single agent in a single city'.

You can compare the HPI vs REINZ median on this website (a more robust median than yours), and clearly see how noisy the median data is in comparison. The idea that you'd pick a worse version of that for a month-on-month comparison is crazy.

Of course the two datasets are roughly equivalent over the long run, but the median is far noisier. As expected.

https://www.interest.co.nz/charts/real-estate/qv-house-price-index

https://www.interest.co.nz/charts/real-estate/median-price-reinz

That's precisely my point.

In an attempt to come up with an index, data is dropped and assumption of equals are made and therefore it resulted in a smoother looking chart.

To give you an example, I have a pool and so do my neighbour. Does our pool valued the same? Mine has a jacuzzi, his doesn't. However HPI considers a pool is a pool and all pools are the same.

I don't think Corelogic's HPI is any better than actual median price when it comes to market analysis.

My point remains. Take a look at the more robust REINZ median data (whole of country, all sales vs your Auckland, single agent, single sales method) and tell me you can infer absolutely anything from a month-to-month trend. It's up and down like a yo-yo.

You are pointing our small flaws in the HPI methodology and ignoring the crater in your own measure.

https://www.interest.co.nz/charts/real-estate/median-price-reinz

"Of the 43 sold since the beginning of February, the median selling price is $1,341,000 compared to month of January's which is $1,180,000. That's a growth of 13.64% in terms of value exchange even for a traditionally slow week of the year." - this is statistically meaningless.

It's meaningless to you because you aren't a participant in the market.

If you were, the fact that people are paying 13.64% more than what was last month on average should concern you.

HPI's are not exclusive to Corelogic, they only tweaked it a little. The general framework for HPI came from academia.

BT is the largest RE in Auckland by transaction and volume; if there's an entity we can use to infer Auckland general, it is them.

My boys in the office just proved you wrong, how do you think they are able to come up with a forecast if not for inferences being part of their specification?

HPI is not the most robust measure when it comes to lower level analysis.

Seems like you don't understand nor attempt to do so.

Enjoy your day, we're getting busy so don't expect further replies.

I have a couple of houses and am selling one right now, if that somehow gives me a better appreciation of statistics. We do not know for a fact that people are paying 13.64% more than last month, because this is based on a small sample so it has huge error bars - maybe 10% for 1 SD? Certainly large enough that any Scientist would shy away from drawing a conclusion. Even the all-Auckland sales REINZ data looks to have an SD of perhaps 4-5% - imagine how large it is for 8 days of data from one agent and one sales method? At best you have ~10% of their data so your SD will be perhaps 3 times larger.

Perhaps the boys in the office are the brains and you're the mouthpiece? Stats can be tricky - don't feel bad. It's just worth knowing their limitations.

All Auckland sales in December is 2,313 and Barfoot and Thompson (BT) did 941. Assuming consistency, BT's share of the market is 40%.

We are in the first week of February and the number of sales is 43 at BT. With reference to the 40%, total Auckland sales for the same week is estimated to be 108.

Given N = 108, n = 43,

A sample size of 42 or more are needed to have a confidence level of 95% that the real value is within ±12% of the measured value.

Indeed Statistics always seemed tricky, especially when detractors play strawman.

Wait, wait wait. You are trying to show me you are just about confident that the BT data is representative of the whole Auckland market? This isn't what's in question. Even if I had the whole market median data for 8 days it's still essentially noise.

Sorry if I wasn't clear - you have a more fundamental problem than the one you are addressing here.

What a load of waffle. Throwing around jargon is a typical technique of bullshitters!

Exactly.

And yes - the HPI is far from perfect, CWBW.

House prices double every 10 years*

*When looking 20 years back only

Hey, guess what the auction clearance rate was this time last year? 71%. https://www.interest.co.nz/property/108967/activity-barfoot-thompsons-a…

6 price drops in my email today and the day is young.

Its quite obvious that you have a lot of money in housing and you are kaking yourself behind the scenes.

In my wife's RE office, the weekly sales meeting this week was all about asking vendors to lower expectations.

Listings are no good if they don't turn into sales etc.

"vendor conditioning" was the euphemism when I was in the game

From my 'on the ground' observations it appears that tidy houses or better in good locations are selling. Houses that are 'dungas' or in pedestrian or bad locations are not selling at the price point their owners are expecting. People that are buying have the money which they will expend to pay top price for a better house and/or a better location. It's as simple as that.

Agree that : Houses in NZ indeed doubles every 10 years.............so an old house in 2019 on appox 600 sqmt section in Pakuranga was for $800000 is now priced in between 1.3mil to 1.4 million so you are correct that in next seven years from here on will move another 10% to 15% from current level (In between may see up or down but most likely will see down but in 2029 will be double from 2019 price, it could either happen uniformly over 10 year or does not happen for few years and suddenly shoots up or happen in initial year and is than dead) - Think we are in category where it has happened in initially, if we take 2019 as base and now will be dead.

Good luck to all those who bought in 2019 and have already sold as their yield will be big and will also, now have cash waiting to be deployed when it crash and here also stock market will give bigger return than housing in near future.

The median and average house prices tend to rise at the start of a downturn, as investors and first home buyers exit the market. Whereas, turnover in higher value segments of market continue, as owner occupiers continue to transact.

The low auction clearance rate early 2019, likely was due to the fact that it appeared the world economy was heading for recession This led to the Powell pivot in Jan 2019, when the US tightening cycle was dialed back. The slide into recession was evidenced by the Sept 2019 explosion in libor to over 10%, as credit markets started to freeze up. Sept 2019 was when the US re-started QE, in an attempt to prevent a likely recession. Obviously this downturn in the business cycle, was prevented by massive worldwide QE as covid hit.

I'm not a perma bear, during the 2020 lockdown I purchased a property for each of my sons. As it was obvious that with slashed interest rates and a recent share-market crash, NZers funds would not head to the share-market, or term deposits. I did not predict the extent of the rises, but I knew prices would likely rise, and that buying during lockdown when no one was purchasing was a great opportunity. I genuinely believe that NZ property prices in general will be at similar levels in the 2030 to 2035 period. With risk of severe declines during inevitable recessions.

The key is that NZ does not control our own mortgage rates. Why, did NZ mortgage rates in crease 1.5 to 2% with minimal change in the Reserve Bank cash rate? NZ mortgages rates are principally determined by prevailing US market rates. The US economy can tolerate higher rates, and they need them with rising inflation. US corporations have a net 2.4 trillion of cash on their balance sheets, and very low debt to EDITBA levels for this point in the cycle. Most US mortgage holders are fixed for 15 or 30 years, given their GFC experience with short term low teaser rates. So the US economy can tolerate higher rates.

If you have a marked property shortage, you do not have the NZ experience of rent increases of 5% per annum (less than the rate of inflation). You have the US experience of rental increase of 13 to 17% per annum. You have property prices outstripping changes in rental levels, during a speculative boom.

It’s the boom time boys!

1 week of data and sample size of 42 sales says the property market is alive and well!

The only thing that managed to be sold in the central auction rooms yesterday was this:

https://widget.auctionslive.com/widget/auctions/view/70600/19Y

It sold for around 20% below it's supposed internet valuation of a million dollars.

It was truly heartwarming to see Jacinda go on television yesterday to reassure us that her government is going to do whatever it can to ensure prices don't go down much. Soon to be added to their long list of failures.

Meanwhile, New Zealand is going to be increasingly saying goodbye to its working-age taxpayers as aspirational kiwis depart for the West Island to enjoy spacious modern 4/5 bedroom houses with pools for less than a lousy two bedroom unit in New Lynn.

My sister (25) bought an apartment in Fitzroy (Melbourne) for 350k at a 2% rate.

My wife and I laughed when we saw a similar unit in our two horse home town for 360k.

Consider I earn about 80-90k more here than the equivalent job in NZ, we’re having very serious discussions about staying here for good!

why do only some have prices?

The ones without prices attracted zero bids.

A sign of the times.

Staggering.

BL ......or for the same money as NZD816k (in AUD759k) - https://www.domain.com.au/205-5-waterloo-street-east-brisbane-qld-4169-…

While you are comparing New Lynn with East Brisbane ?

I have had my fair share of buyers remorse over the years, but wow ... 800k for that dog box... Pass.

Sucess rate from 42% to 38% to now 27% does not seem positive for housing market. If next two weeks also reflect sale rate near around 30% can confirm that party is over.

Even today though unable to sale at auction, vendors expectation / asking is still high near the premium as was the trend earlier and may take a while and only saviour if this downtrend stops and market start moving upward, which seems doubtfull as everything going forward in 2022 seems to suggest that worst is yet to come, be it stock or housing market.

Stock market reacts fast unlike housing market.

Another article by Bernard Hickey...... exposing Jacinda Arden :

"PM restates housing hope without defining success

PM denies giving up on housing affordability and says she's pulling all the levers, but continues to refuse to define what success or failure looks like, or actually pull all the levers

PM Jacinda Ardern has rejected the suggestion her Government has given up on meaningfully improving housing affordability for buyers and renters. Yesterday in her opening Parliamentary statement of the Government’s ambitions for the year she again said the Government wanted to improve affordability and was ‘pulling all the levers’ to do that.

But again the PM would not indicate what success would look like, or when the Government could be judged on its progress (or lack of it). I take a deeper look below the paywall fold at the PM’s statements yesterday on housing and which levers aren’t being pulled."

In many respects she's been very lucky to have COVID that is distracting the media from reporting any other real, pressing issues facing society - and that would expose how badly fiscal and monetary policy has further increased inequality and poverty.

The government, has saved lives with its COVID response, but ruined many in doing so - at least in terms of financial security and future prosperity.

I agree, Covid appears to be taking up 95% of this governments "Valuable Time". They appear to be unable to sort anything else out and are very busy keeping everyone focused on Covid when it should have been taking up 5% of their time. Come next election in 2023 will see even the stupid people in NZ finally realise they have been taken for a ride.

Ministers are asking officials to make sure they are focusing on Covid and not spending time on other things (that might be considered BAU).

27% sales rate, that's abysmal! Watch stock rise quickly are sales languish and listing rise... which is not going to help further clearance rates...

No idea what the average is for this time of year but tradme listings in (all of) Wellington have gone up from about 1808 listings to 2318 over the last three weeks.

AKL stock levels have been rising are now back to roughly pre-covid levels. Still a long way (~30%) below 2018/early 2019 levels though.

Well done Sherlock nice to see you are working it out.Housing stock going up 5-6% each week interest rates raising inflation high and NZD tumbling only way housing market is down Yvil like I have said before the smart investors have left the market and sold at top price. The decline is speeding up without doubt.

Also, I can see shoeboxes all around the place rising from the earth in Auckland, so the listing will definitely go up more in the next 5 months.

And now winter is coming which will not be the ideal time for open homes and people want to stay home rather looking for properties, considering omicron is around and winter flu will leave its impact.

And every one that did not sell is now being told by the agent to drop 200k off the price.

Nice to see Interest give credit to T Alexander

Indeed, there are plenty of properties for sale in South Auckland but few are selling, or not selling as quickly and easily as last year. Don't fret through, BANK executives and major shareholders are still doing OK.

Flatten or slow decline is solid healthy way for the next take off in the next decade. The foundation is well set.

Yep the broken clock brigade are about to be right for once but the same long term trend continues unabated.

With all the current dynamics is anyone really surprised. Several sectors in NZ are in an inflation furnace at the moment, especially medical, construction, transport and technology. All driving hyper inflation. I'm picking the RBNZ 23 Feb MPS (live-stream) will be hugely watched next week. Even my banker is telling me an increase in OCR is locked in.

Will Orr continue to fiddle while NZ burns...?

Its going to be a cracker, yet another Oscar winning performance from "The Arsonist", coming to you live on the 23rd.

Orr is a bureaucrat. He only listens to the government, his pay masters.

And the government doesn't listen to its pay masters (the public). The current government listens to their sponsors, the ones who pay high fees to join gala dinners and attend seminars.

So don't expect much if you are a poor worker trying to make a life on the street, working hard and paying taxes. You will be a loser under the current government policies.

Well put. The independence of the RBNZ is exaggerated. In a statutory and structural sense it is independent, but as in many things in our capital city there's all sorts of smoke and mirrors, and workarounds

I wish the RBNZ and the government were less independent, frankly. As things stand it's a farce.

RBNZ: "We want LVRs."

Govt: "Well, you can't have them."

...

Govt: "Oh all right then, take some LVRs."

RBNZ: "Nah, don't want them anymore."

Govt: "Aren't you gonna use those LVRs we gave you?"

RBNZ: "They're not cool anymore, you don't get it."

its 2 weeks from now and a 25bps increase is baked in. hardly worth tuning in for. If they do 50bps or 75bps, i'll pay attention - but they wont. watching paint dry.

I see T Alexander is picking 50 BPs.

Me too.

That will be almost enough to scuttle the economy / housing market.

I imagine you read his study on future spending plans? It looks very bad for NZ

Yes I did, and I think he's right.

Yep me to, should have done it last review but didn't and things have got progressively worse, its going to go 50 points with talk of more rises to come to try and scare the shit out of the market to get it to behave

Yes he'll try and scare the shit out of the market, then proceed to lift the OCR only once or twice more this year.

i sometimes feel the comments section on these articles are more informative that the article itself. basically you get an idea of the mindset of the readers.

I've been reading the comments for a for years now and it always seems like the property crash is around the corner, and even TTP capitulates, but it never turns up and a few months later prices are higher still.

Its like Alice in wonderland, jam yesterday, jam tomorrow - never jam today.

Is this crash ever going to happen?

Don't take it as a mindset of the general public though - very different outside of interest...

I guess you can never say never.

Maybe the government will start acting as a bank for FHBs, gifting them 20k, and providing super low mortgage rates.

Unlikely, but certainly not impossible.

Didn't stop them from doing so in the past, 3% housing corp loans and capitalising future benefit payments into a deposit.

3% FHB mortgages fixed for 30 years and capitalising forward WFF payments into a deposit.

I don't think interest rates are going to raise as much as everyone thinks.

The banks have more than factored in any hint of inflation & rate increases but when the volume of lending slows and the economic activity slows down this year mortgage rates could decrease slightly

Yes, that's what I have been saying for months. A contrarian position.

I guess time will tell whether or not I am right and the vast majority are wrong. Or the other way round.

It really depends on what happens in US, Europe and Japan (G3). If rates are rising there, regardless of the local situation, they're going to rise here too. Arguably the rate cuts we've had since the GFC are more to do with keeping in line with the G3 and avoiding a massive currency appreciation (but fuelling a massive housing bubble). Same thing kind of happened to Ireland with currency union.

9 Months ago I fixed for 5 years at 3.05%. 2 months ago I traded up, and fixed for 5 years on 4 x the borrowed amount at 4.95% (same bank). All specials off the carded rates.

You could be right about the limits to rate increases due to economic slowdown, but is that not a negative self feeding loop? If economic activity slows, then surely the job market suffers. Easing back on mortgage rates does not give someone their job back or stimulate wage growth resulting in a sudden increase in lending demand.

However I'd rather you be right and be locked long, than you be wrong and locked short.

Is there any information on how many sold on the day in post auction negotiations?

That would be interesting reading...

Those are usually counted as auction sales.

Realterms - thank you. That's really helpful to know.

No one can force people to borrow and buy.

You cannot push on a string......

Once price falls start they may continue for some time , just as interest rate rises, will continue for some time.

RBNZ has a clear inflation mandate, its the most important mandate besides growth in the economy.

Unlike vax mandates its been around and will stay around for a LONG TIME.

House prices are going a lot lower and everyone with financial knowlegde knows time in the market will not beat timing the market this time.

Trade accordingly

RBNZ has a clear inflation mandate, its the most important mandate besides growth in the economy.

Doesn't seem to be that important, they've been ignoring it for quite a while now...

Agree with Nifty. Is their mandate to mandate inflation or is it protecting the house bubble/bank profits (see ASB half year profit) because based on the last 24 months its looks like the latter.

Basically people out there looking for a bargain but vendors not wanting to sell below top dollar

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.