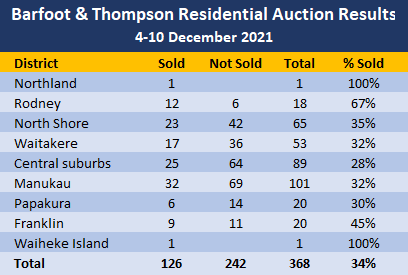

There was good and bad news at Barfoot & Thompson's residential property auctions last week, with a whopping 368 properties offered for sale, but the sales rate barely scraped past the one third mark.

Just 126 of the 368 properties on offer from Auckland's biggest real estate agency were sold under the hammer, giving an overall sales rate of 34%.

That means the sales rate has exactly halved over the last two months, falling from 68% in the week of 16-22 October.

That falling sales rate trend can be seen in the results below:

- 16-22 October 68%

- 23-29 October 67%

- 30 October - 5 November 62%

- 6-12 November 59%

- 13-19 November 54%

- 20-26 November 50%

- 27 November - 3 December 43%

- 4-10 December 34%

Around the main Auckland districts the auction sales rates ranged from 28% in central Auckland's leafy central suburbs, to 67% in Rodney.

The chart below gives the district-by-district sales rate breakdown.

The slow down in the sales rate follows a surge of new listings, which is giving buyers more choice.

This suggest that the buying frenzy which gripped the market over the last few months has now passed, and vendors with overly high price expectation may now struggle to sell their properties.

Details of all of the properties offered at the auctions monitored by interest.co.nz and the results achieved are available on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

176 Comments

Time to unleash some more monetary policy support or demand side subsidies then?

Agree, as Jacinda says "A house is most New Zealander's largest asset, so it not NICE to have that decline"

We must support our largest welfare scheme.

I'm no fan of Jacinda but she did also say just a couple of days ago "We need [the market] to stop heading in the direction it is," she said. "Even if you saw [prices] come away, in many cases it would be bringing [them] back to levels that we were at only a year or two ago."

Will she follow through, guess that all depends on the polling...

https://www.rnz.co.nz/news/political/457683/ardern-wants-runaway-increa…

Exactly, politics for someone without spine like our dear PM is purely a popularity contest - one week after the polls were out saying that 80 % of population would like to see house prices to fall, she changed her tone... And so this goes also for all those who believe that Govt and RBNZ are the plunge protection team, this may not be the case, once the public wants prices to fall and they express it clearly, our dear turncoat PM will not be there to save investors from themselves.

Poll driven politics, is a great way to not get anything done. Our current Govt have been exceptional at that.

Democracy in action, the tyranny of the majority upon the minority.

John Key 2.0

I wouldn’t be surprised if Adern walks away soon eh. She looks completely broken.

I’m not surprised, you couldn’t pay me enough to do that job.

I think that is part of the problem. There was a job to do, and she hasn't done it, any of it. Even her own working groups and committees are starting to point that out. Even child poverdy and welfare reform 42 items were highlighted needing improvement in 2018. Nothing done. This is her portfolio. She is a dodger, not a doer.

Wouldn't blame her at all. If she was a guy she would be bald by now lol.

The job of leading through a pandemic - especially in the age of social media nuttery - is absolutely not one to envy.

Yes fair point, very hard indeed.

She and her team haven't helped themselves at times, mind you.

She is loving the Covid environment, it’s a distraction from all of her failures. She link’s everything back to it being a difficult environment due to Covid. Covid won her the last election, she is trying to spin it out to the next election.

Yep, everything is Covids fault. If she had a clue, she could have solved that problem. But no, she is constantly backtracking, ignoring expert advice, not learning from overseas, and basically an all-round failure. It's actually beautiful to watch someone who promises everything, lies, changes tack and can deliver nothing, and now has to deal with the consequences. It's only just started too.

That's what I said: John Key 2.0

"I don't accept that our teachers, nurses, and police officers can't get into their first home... I do not accept that is the future of this country" - Jacinda Ardern 4/7/2017

Good riddance. Just another scumbag politician that says whatever it takes to get their grubby hands on power. Through her spineless inaction and incompetence she has destroyed life in this country for teachers, nurses and police officers.

Once she goes, of course, we get to see how much Grant will bugger the place up.

Come now, she is finalist for quote of the year with the "Neve fail". It's the one thing Jacinda is good at

Seemed like they started with genuine intent on housing, in their first term. However, the turn to "prices should keep going up but slower" was an absolutely clunker. The turning point into John Key 2.0

I agree, intent was there (unlike National) and in Auckland at least prices were flat until covid. Kiwibuild and that comment she made that you refer to will be the key failure.

Lip service to harvest votes.

She refused to implement the findings of her own tax working group, directly leading to the current disaster.

Anybody else that caused this much harm to society would be in prison.

Predicted she would walk away before the next election months ago. Think it will take her poll numbers to crash and they will come closer to the election. I will be very surprised if she is still there for the next election. The second she goes it will be National back in to try and clean up the mess.

Anyone would be dreaming if they thought National has any intent to make houses more affordable for younger New Zealanders though. That much was clear from Luxon's initial forays demonstrating NIMBYism and investor entitlement mentality. National will prefer to remove taxes from investors so working New Zealanders pay for the services all Kiwis use, then invite foreign buyers to buy NZ out from under young Kiwis because they can afford to pay more...while still wanting young Kiwis to pay their pensions, of course.

Jumping from frying pan to fire and back and forth won't help any of NZ's younger generations. It seems they will need to look beyond Natbour.

I don't reckon she will resign, not at least until they lose power.

Just think for a moment, it would be against her woke ideals to resign because it was 'all too much'. She won't want people saying 'Told you so, it IS impossible to juggle the PM's role and motherhood'.

Also, she clearly adores power and the limelight.

It would also be letting Labour down big time.

She will resign because an opportunity too good to miss came up in UN, WHO, EU, (delete those inapplicable), or some other initials I haven't thought of. However she is leaving NZ in good hands blah blah, etc, etc. Also, I heard the wedding is off. Correct me if I'm wrong.

But that is exactly what the Woke of this world do. Make a big song and dance of something that don't have a clue about, then try to implement whatever their solution is and then silently slink away after they fail. This is Jacinda's fate.

I didn't realise Donald J was woke?

But he didn't resign.

We are talking resignation here.

Using "woke" as a pejorative term is just Talkback Boomer virtue signaling, at this point. Time to move on.

I cant see Ardern walking. She loves a tussle and luxon is the new challenger

Stir is her last term so she might salvage her creditability - last chance.

"The measure of intelligence is the ability to change" (Einstein)

lets hope adrian orr has that ability,keeping a lid on interest rates when you have a weakening currency and rampant inflation isnt working for turkey and not likely to work for us.

That's a miserable result. The market has definitely well and truly turned.

Now's a good time to let the market cool off a bit.

It's quite possible the pace will quicken from later in January through to mid-April - as that's the usual seasonal trend with house sales.

But if prices taper off to a level I can afford, I'll be smiling...... 🤩 Renting is a curse. 🤬

TTP

The bottom has fallen out of this market, as expected. I can’t understand why more people aren’t forecasting price drops? The only explanation I can come up with is once bitten twice shy. You’d have to be living under a rock not to see what’s coming.

People are blinded by their experience historically. Rather than digest the information and the clues that are presenting themselves, it’s easier to huddle together and say ‘it’s different in NZ’ or ‘we’ll just get immigrants to prop it up’.

Its here folks. The pig troughs are empty.

It's a combination of both 'lazy' *thinking* and 'wishful thinking'.

I think past experience suggests that the Govt and/or RBNZ will do something to prop the market up...... I have given up predicting a fall - the ridicule for always being wrong is not much fun to deal with.

Yes. It's in the interests of the ruling elite to do whatever they can to stop the bubble burst.

But the RBNZ has much less ammo this time.

Remember when prices started dropping when the GFC hit they could cut the OCR deeply and repeatedly.

Less ammo and less desire. In fact, the Governor is on record as saying house prices should be lower, so it wouldn’t make sense for him to stand in the way of a correction except to the extent that financial system stability is threatened, which is not likely to be the case for a 20-30% drop (I'm picking 10-15% sans darkly-shaded waterfowl).

Much less ammo.

Imagine this current level of inflation for another 2 or 3 years.

Hi rjn1,

You say above, "the bottom has fallen out of the market".

That make about as much sense as saying, "the market has fallen out of my bottom".

With all due respect, it would be helpful if you were not so given to exaggeration.

TTP

So far all we are seeing is a drop in sales, not an actual drop in price. It may happen but all indications are that the economy is running hot and there isn't a lot of impetus to drive down prices.

There is an obvious potential driver for prices to fall. Mortgage rates fell from ~4% to ~2.5% leading to the +40% price rise feeding frenzy. Rates have now returned to ~4% so it is completely reasonable to expect price falls.

There are of course other factors, but many of them are also pointing in the direction of price falls (immigration is essentially zero, banks have stricter credit checks, DTIs on the way and perhaps already implemented by some banks, new building supply is very strong, planning restrictions are easing, and Government regulations on rentals becoming stricter esp. removing interest deductibility).

I see plenty of impetus to drive down prices. I own my home and wouldn't have any problem with a ~30% fall bringing us back to where we were a year ago, but if I were an investor I'd be seriously weighing my options. Many will be forced to trim their portfolios anyway if a reasonable DTI policy is implemented.

Have we seen a drop in sales though ? If 3 properties in the auction and all 3 sell that’s 100% clearance rate. If 338 properties in auction and 100 sell the 30% clearance rate is irrelevant if measuring sales volume.

Sorry, TTP, I was assuming a basic level of knowledge. To spell it out more helpfully for you, demand for residential real estate in the lower price ranges has diminished substantially, and vendors are now starting to chase the market down. Let me know if you need further clarification or an explanation as to how this feeds through to the rest of the market.

Very rich of you rjn. How many properties have you bought, owned and sold and over how many years to back up your sarcastic, condescending superior view?

Ah, did you see the post I was responding to? The guy was clearly TTP (my acronym, not his). And the answer to your question, however irrelevant, 5 properties over about 10 years, including 2 new builds. But more applicable to the current debate, my study of markets and human behaviour have not been limited to the NZ residential property market!

Even so, if any offence was taken, I humbly withdraw and apologise.

rjn1 The bottom has fallen out of this market, as expected. I can’t understand why more people aren’t forecasting price drops? You’d have to be living under a rock not to see what’s coming.

Or you have some experience coming across multiple previous situations where the RE market faced serious headwinds like the GFC, Covid and many more. Then you understand that a slowing market (which is definitely happening now) does not necessarily mean crashing prices

Just curious, does your experience extend to other countries where significant price falls have occurred? Just investing in NZ property could give quite a 1-sided view of what's possible unless you truly believe NZ is unique.

I have friends in the UK who spent years in negative equity after the GFC, and there were many more back in the early 90s. I don't have experience of other countries like Ireland or Spain which suffered far worse and would seem more comparable to NZ in many ways.

Great point MFD

Yes it does mfd, Spain is one of them

Must have been painful. Many in NZ seem to be unaware that corrections happen fairly regularly around the world, and perhaps we are overdue.

The problem is these things play out over cycles that last years / decades. And our immediate thought power is usually focused on the day to day or monthly.

This could well be a tipping point. Could just be a 1-2 year slight bump.

But agree that history shows we are at risk. Big time.

Yes fair call, but none of those situations involved such a fundamentally overvalued market with such a huge recent run up in prices. I think people are underestimating the effect of very high recent returns - I.e. only very recent buyers are underwater during a moderate retracement. This goes a long way to countering Kiwis’ extreme aversion to selling at a loss.

Rjn, The last 30% increase we have seen is the Euphoria stage that other markets also had in 2006

My uneducated take is that price rises will soon stop, the market will flatten, and there may be some small drops in certain areas (5 to 15%), but we will not see a price crash (greater than 20%). We will also not see a return to rapid price rises for at least 2-3 years, maybe more. The long-term bull run is well and truly over. There will, however, be people that lose the shirts off their backs. This won't be FHB or long-term buy and hold investors. It will likely be property developers, especially those new to the game, as well as some highly leveraged speculators.

It is easy to envisage a correction of 25% in areas that have had 30-40% capital gains in the last year. This would not be considered a crash as it doesn’t exceed the gains from of previous 12 months.

Currently there are a lot of potential downside risks such as further excessive government spending, a natural disaster, deterioration of health system this coming winter from another variant of Covid, unexpected global inflation, large numbers of kiwis departing NZ, etc, etc.

There will always be some probability house will decline more than 20%. The chances may not be high but unexpected events can still cause price crashes. eg Bank collapses etc etc. Hopefully investors have reserves if the worst scenario hits.

You're right, but I don't see a 25% correction happening. Many of the things you suggest will increase nominal values in my humble opinion. Let's see how it plays out.

So you are saying 1.3 million average house price is ok for Auckland. Are we LA or NY?

We are totally out of touch because of our own greed. I just hope lots is unsuspecting immigrants come to NZ and make us all millionaires. Who cares what happens to them later.

I am not saying that it's OK or that I agree with it or that I like it or that I benefit from it. I'm just saying that prices will stay there, possibly for a very long time.

But things are different now, right? Time never mirrors the past, events can follow the patterns of past events, but you have to be careful in extrapolating context forward. Events can also totally break from the past.

We had the huge luxury with the GFC to cut the OCR deeply and repeatedly, that was the only thing that prevented price drops being worse than 10%.

We don't have the same luxury now, right?

People understand that it is hard to fight against Prime Minister and Governor of Reserve Bank - who have made it clear that come what may will not allow the house price growth to stop. Personal guarantee so one has to be a fool to not speculate and make fast, easy and BIG Money.

Profit is ours and the pressure / risk is borne by RBNZ and government as they have more to lose than the person borrowing.

The monetary creation policies have been to keep the general economy moving, not to specifically inflate house prices.

Capital assets accross the globe have all been inflated. Though in nz our flavour of this debt glut just happens to be private debt/housing.

The only reason why in the past, that its been feasible to pursue the money printing response (lowering interest rates etc) is because inflation hasn't moved accordingly, or some cynically say hasn't been counted.

But we now have inflation. Big time. So in the event of a correction in house prices now, it would not be as easy to hit the print button (even if propping up the private property market is the goal, which its not)

People forget, for the vast majority of home owners, your actual daily lives would not be affected by a 40% reduction. You may feel less wealthy, but those were potential gains not realised.

Sure there will be job losses and lots of MSM noise, but life would go on. Lesson learned.

The actual number of houses exchanging presently for these crazy prices is comparatively low.

Oh, there is a place

A place in hell

Reserved

For auctioneers and their friends

You call yourself "charming"

Hi Yvil,

I'd wager that Charming has even fewer friends than auctioneers and real estate agents‼️ 👿

TTP

My bet is he's a Smiths fan, in which case I won't have a bad word said about him!!

A great band for DGMs if ever there was one. Morrissey must be the DGM God.

Although he had a wicked and wry sense of humour too. And lot of their songs were very playful and upbeat.

Johnny Marr is a musical genius, so that helped.

A hero of mine.

Little genius.

Great rhythm section too.

We had a painter do a quote to redo an old small cottage. He wondered how long we were intending to keep the house before totally replacing it with something new. 20 to 40 years was my response.... as I know how difficult and expensive new builds are. Anyway hopefully by then I would either have retired or otherwise expired so that I wont have to worry. I doubt this nz housing scene will be fixed by then and am sure Interest.co will still be raging over every property update

Do people still really think the OCR will rise above 1.5% if house prices are down at least 5-10% by mid 2022?

What is the inflation rate ... I am not sure the exact number let's say 6.5 and well outside the RB mandate

You don't think preventing a house price calamity comes above the 'RBNZ mandate'???

Remembering that mandate also includes employment and financial stability...

If the central bankers cared about financial stability they wouldn't have engineered an asset bubble in the first place.

The head of financial stability is slithering away now. Likewise the chief economist that was so enthusiastic about deliberately blowing this asset bubble.

Yes probably. The RB is somewhat snookered courtesy of robbo ... you would agree that a tight monetary policy also means higher exchange rate and that indirectly negatively affects employment. This govt has mashed everything

It all comes back to the Fed and what they do. Not everyone is going to be able to devalue their currencies at the same rate without triggering uncontrollable inflation/debt defaults.

Hi Indie, the US fed has already signalled an end to bond buying and QE. Hence the stronger USD. You could probably explain to the readers the implications of this....

Yep, I think they are snookered. Damned if they do, damned if they don't. Etc etc.

And it's at least partly the government's fault, by introducing employment into the RBNZ's legislative mandate.

The RBNZ is not in control the NZD is sinking inflation is up the US Fed have said rates will be raised soon and they have to do this or USD will tank.This is unfolding now not sure if the forecast for housing market could be any worse, this is why smart people are selling what they can at top prices.

Not that fast, our housing market has been booming for many years. OCR has been low for many years too. The situation won't change that fast unless there is a crash, which would be more than 10%. I highly doubt that 1.5 OCR would do too much for housing price. OCR is determined by inflation and unemployment rate, even if the house price are down for 5-10%, inflation rate wont come down that quickly. Give it two years, you might see OCR will stay around 2% for a while if we are lucky.

Bottom line is that the OCR was to low and held there for to long. Its STILL to low and is adding fuel to the fire. People are refixing their mortgages at low rates so its going to take YEARS to have a significant effect on the market. The result was huge house price increases with a soft landing.

Don't 70% (or something like that) of mortgages come up for renewal in 2022?

Also these higher interest rates will pull down demand for house buying, whether new or existing.

The big question is, in the face of dwindling demand, how much will sellers be able to hold firm with asking prices?

House owners just don't like to sell at a loss. If cashflow gets tight, the proverbial avocados and other discretionary spending will reduce (that's why you and I don't see interest rates rising for all that long). But owners will just stay in their houses, enjoy them and not sell. The only way house prices are going to crash is if there is another serious external shock.

PS, yes there may be a dip -10% in prices in 2022 which is different from a crash -30% or more

So if I bought a house in 2019 for 1 mil and sell in 2022 for 1.1, is that ‘selling at a loss’? Even if the market has recently fallen by 25%? It’s about volume at price, not just price.

No, if you sell a house $100'000 more than you bought it for, it's not a loss. I thought that would be fairly obvious

and how many other houses get sold i.e. volume does not affect your gain or loss.

PS, making things more complicated than what they are is not a gain either

I’m just trying to illustrate my point re the instability of very fast gains. Basic market dynamics - volume matters.

I’d have thought the same ;)

Ok but take the next step - if hundreds of thousands of households significantly reduce spending to ‘sit tight’ and not sell the house, what happens to businesses income across the economy. And if business income reduces, what happens to wages? And if if this happening while input costs (inflation) is rising both for households and businesses? It’s severe stagflation which will be maximum setting on the misery index.

Something would eventually give - either the household or the business that employs that homeowner defaults as costs are greater than income.

Enjoying their houses but not that delicious plump $1.20 avo on toast

Yeah but what about all the townhouses being built? The same luxury of holding does not usually exist.

At least in Auckland, new townhouse sales are a big part of the market.

I think some developers will get themselves in strife. Stories are growing of developers cancelling contracts because of rises in construction costs. Their behaviour assumes people will be will and able to buy the townhouses at the new higher prices at a time when lending is slowing and the cost of borrowing is jumping up.

2022 will be interesting and not in a good way.

Some of those just look like cynical ploys of using deposits to secure development finance then canceling to sell at a higher price later.

Probably a bit of a few things at play. Construction costs have certainly risen a lot in the past year, there will be genuine scenarios where a developer selling in 3 months time at the price agreed off the plans 12 months ago may no longer make a profit and could even make a loss.

External shock...so would that be something like Evergrande and Kaisa Group Holdings going into default, or, everyone waking up to the fact the US is a money printing naked emperor essentially abusing its position as the reserve currency, or, a US and Chinese warship or plane threatening each other in the Straights of Taiwan, or a global pandemic taking place, or, a global supply chain and transport breakdown, or perhaps all of these things happening at the same time...

Or do you mean something else...?

Yes, like the fed stopping QE and raising rates for example..

The reserve bank will.be caught if house prices fell dramatically yes they can cut interest rates back to negative, but can you imagine the effect on our dollar, it would plummet leading to much higher inflation much like the turkish economy their genius leader has followed that path and look at the outcome, perhaps Erdogan can advise orr on what to do .

Bankers know what is going on. I know people working in the main banks who have been modelling this exact situation. The clever money has already left the market.

I believe that just as Orr raised the middle finger to detractors on the way up, he will do the same on the way down.

Here's hoping.

Listing numbers are highly misleading unless you look at what is for sale. Rising proportion are not built or even started yet. These are not going to auction either. Owner occupied sales are falling rapidly and proportion of listings that are owner occupied is static or falling on Hibiscus Coast

re nz figures show listings of houses and townhouses are identical on Hibiscus Coast as were a month ago and NSC only 1% higher. The summer surge did not happen and the tide has turned. Time to wake up

.....back? hopefully more observation from you to come mike.

This finally looks like the first sign of 'the mania' dropping...

I like 'the buying frenzy' as mentioned above - a shark will snap at anything when in such a state

Hi Rastus

i have seen sales dropping for months and listings make up but been not bothered to comment as anyone questioning the meme of “all good and prices can ne’er go down” is not popular on here.

Stagnation is upon us all at once but inflation plus reversion to the 2019 mean were inevitable and seen by far wiser heads than mine

There is no reason to be happy for FHB, sales drop not asking price.

The asking price is still way strong and the seller seems to be ready to hold if the asking price is not met. A mass exodus is on the cards in the next few months but there is no indication of price reduction.

The 50 to 60% increase in last year will not go back, it's just wishful thinking. I know people will not like it but that's the truth.

50-60% increase?

..must be up to his eyeballs in speculative debt to comment like that.

Yeah I expect a mass exodus of young people. They are not wanted here as they want reasonable wages and the ability to put a roof over their head. Much better to let them go and replace them with immigrants who have lower expectations to become renters for life and keep the house price high for the property owning class.

I'm on a team of 10, we are down to 4 staff and have struggled to backfill vacancies. Most everyone that resigned was a young professional that was struggling with cost of living and left to find greener pastures. The spiraling costs of living are going to cause many problems and disruptions for NZ that will likely be ignored until it is too late

This is Auckland, not regional cities.

I guess if you want a market crash your always looking for reasons for a crash. IMO its not going to happen, its BAU into the New Year. It will take something epic to see a crash, not going to happen. Inflation is running hot, energy prices are increasing, wages will increase and the leading indicators are for price increases unless inflation can be controlled.

The key, as usual, is to buy in the best location you can afford.

Travel/transport issues in the main centres (certainly Wellington and Auckland) are not going to resolve anytime soon, so if you buy near the CBD (and/or near good schools and other public facilities) then you'll do well in the longer term (and possibly sooner).

Learn from my mistakes - get in as soon as you have a reasonable deposit.

TTP

This is the first year I haven't cursed Auckland for it's traffic.

https://www.economist.com/united-states/why-americans-are-rethinking-wh…

I agree Carlos. The only caveat is that there are a large number (35% quoted here) of properties in Auckland that are owned by investors. That is a large number when you consider that they react to very similar changes in the economy in a very similar way. That's in contrast to owner occupiers that sell for quite individual reasons (retirement, new job, kids, schools).

Diminishing yields because of the rising interest rates vs rent, tax breaks being removed, capital gain forecasts flattening, and healthy homes plus associated costs are all pinching them in the same way. The tipping point to pivot into another asset class may be provoked at about the same time. I have no idea when that will be, but if it is reached then it's possible that a run on properties may start which could become severe.

Firm predictions on house prices is a mug's game, better to look at scenarios and probabilities.

This is what I think for 2022:

Large price gains: 2.5% chance

Moderate price gains: 7.5% chance

Small price gains: 15% chance

Small price falls: 30% chance

Moderate price falls: 35% chance

Large price falls: 10%

Small being 0-7.5%, moderate being 7.5% - 15%, large being 15% plus.

Good work. However I tend to think the market is a little more unstable and volatile.

Large price gains: 20% chance

Moderate price gains: 20% chance

Small price gains: 10% chance

Small price falls: 10% chance

Moderate price falls: 20% chance

Large price falls: 20%

Nice.

Large price gains at 20% probability? What is the basis for that? Unexpected cuts to the OCR?

Its all a guess, you could have taken the same percentages pre-covid and the result was the total opposite with the numbers flipped upside down. The way things are shaping up you could still flip those numbers upside down for 2022.

This is what I think for 2022:

Large price gains: 10% chance

Moderate price gains: 30% chance

Small price gains: 15% chance

Small price falls: 35% chance

Moderate price falls: 7.5% chance

Large price falls: 2.5%

Fair call.

The important thing that is being borne out is that it's volatile and hard to predict, most people would probably say small price gains or small price falls are the most likely outcome, but others are also quite possible.

Interesting but I wouldn't call a 15% drop in price "Large" especially not after the gains we've had in the last 2 years

In the context of the NZ propety market, a 15% decrease would be huge...

Yes that is what I was going to type, we haven't in the last 30 years had a nominal fall of more than circa 10%, so by NZ standards 15% would be large. Also I don't want to get in to too many categories ie. Large, very large, huge...

My prediction is a reversion to mean - that parabola has to flatten surely?

Thames/coromandel median has increased 44.4 percent over last 12 months yeehaa. Just wait till auckland is released from its shackles and flooding the coromandel region over summer, some will have millions of dollars in their accounts looking for a place to put it.

When we transition from a building profit driven investors housing, to houses for people to live in do we go back to 2010 prices? does anyone know where the bottom is? do the massive cheap developments start dropping price of the properties when there is more choice? Will the economy collapse if the industry loses 30%- 50% when a lot of it is only on paper? Do we still need to build houses? it doesnt feel like it, but we were told it would take decades to correct the undersupply? Interest rates going up, immigration in negative territory, supply achieved, lending restrictions getting tighter, government that is making housing investment unattractive, The NZ Herald being run by One Roof? Barfoot sales rates decreasing every month, more properties being handed in at auction. Are prices still going to increase, not too sure now. The property market needs prices to continue increasing to be viable, but thats not practical. RE Agents making 2 billion in commission over the past 12months. Feels like a massive crash to me.

Once the market turns the 40% gains of last year or so will vanish very quickly this why people are selling what they can ASAP

The 40 percent gains will vanish? Never in a million years! "Million", See what I did there

The so called affordable projects are always the first to be dumped. People with money have money!

As for the government funded projects. Well we all know about government promises.

Hello, Does anyone have or know where to find the breakdown of the type of properties passed in? Is development property being affected? Or is is the well used middle to low priced properties that are being passed in at auction. A lot of media hype to create sensationalism by grabbing onto a balloons tail and being carried with the wind.

Slow down Sally. There are a lot of turns on this road. The first ones seem to be happening. But the journey is up & down, & no one is 100% sure on where it's heading. I like the % picks above. Kudos to those who have stuck their necks out. I've saved them for referencing this time next year. We're still not ''building'' the right houses for those that need them - the poor. Ms Woods is buying them, but not building them. No one wants to build them. No margin. Tough for FHB's. So, old stock in the wrong areas will turn into cheap stock unless maintained or upgraded. This is a slow process. Quality is King when buying today, especially location, as mentioned above. I would personally like to see the market settle & drift next year, & maybe into 2023. Risks ahead? There are many but I still think China property is the one to watch. If it goes, who knows.

I think you are right wrong john

You’re not wrong, John. I like to get stuck in to the permabulls, but you are of course quite right. We can (should) only speak in terms of probability weighting. What gets my goat is the propagation of this absurd myth that property prices can’t fall much in NZ. It’s clearly not true and it’s quite dangerous to some of the newer and/or more vulnerable market participants. I hope we don’t have an all out market crash, but we need to be able to honestly assess and discuss risk with our heads above sand-level.

My picks for 2022:

Large gains: 5%

Moderate gains: 10%

Flat (small gain/fall): 40%

Moderate falls: 30%

Large falls: 15%

'I like to get stuck in to the permabulls, but you are of course quite right. We can (should) only speak in terms of probability weighting. What gets my goat is the propagation of this absurd myth that property prices can’t fall much in NZ. '

Nailed it. It's the absurd (and self interested? or deluded?) notion that property prices can't fall, or at least by not much, that's especially infuriating.

Now they might not, or they might not for a while, but to argue it can't happen because it never has, is baloney.

I don't know anyone on this site who has stated that house prices can't drop

That's why I said (note bolded text):

'It's the absurd (and self interested? or deluded?) notion that property prices can't fall, or at least by not much'

Correct me if I'm wrong, but I thought you have acknowledged it could fall, but not by much.

I picked up my new house plans yesterday after waiting what seemed like a life time to get them. The architect commented that a number of builders are starting to enquire about jobs that might be in the pipeline. Apparently a number of projects that had been promised for them have been put on ice.

I am hearing the same. Projects that would have stacked up 12-18 months ago no longer do, a lot of developers won't get sufficient sales off the plans now for all those tiny two bedroom townhouses in less than average locations at 800-900k.

12 months ago they could have sold them for 650k with lower build costs. Also realisable demand was much higher then, with interest rates much lower and fewer barriers to lending.

Definitely early signs are emerging of the building sector collapse I have been talking about for quite a while.

It's going to get a bit ugly.

Watch out for much fewer Ford Rangers on the roads by late 2022.

If it happens, watch out for lots of this/last years Ford Rangers for sale for cheap on TradeMe. If it blows, our economy and currency go town the toilet, then oil and diesel costs shoot up, inflation explodes. Milk prices will go sky high though, so again, our food exports would save us, while prices at the supermarket will go crazy. We would likely lose a tonne of people to Aus (as long as they aren't in dire straights as well), feeding a house price drop. IMO we are teetering on this right now...

But at least we are at the end of the RBNZ and political populartiy ponzi.

Milk does little for the NZ economy, farmers were selling at break even for a long time a few years ago and it didn't make a dent. The NZ economy is totally dependant on Debt and Immigration.

Watch out for much fewer Ford Rangers on the roads by late 2022.

Don't know about that. They'll still be just as good a Fringe Benefit Tax avoidance scheme for city marketing managers as before.

https://thekaka.substack.com/p/pm-ties-herself-in-a-housing-affordabili…

Response should be that I Jacinda Arden the PM of NZ do not want to see the thouse fall annually but if it moves up from $100 to $150 annualy and if it falls by 5% or 10% or even 15% to $135 is fine as still up annually and good to kill FOMO being reason for stupidity and not just supply or interest rates BUT .......

It has been proved beyond reasonable doubt that only economy in NZ is housing And no politician can even think of not supporting the ponzi specially now after creating the monster.

Totally incoherent from Ardern.

“Cindy’s choice”, coming soon (not to be broadcast on NZ state TV).

Bernard Hickey is substantially right on all aspects of the NZ property 'market', in that article.

He, better than most, knows that hoping for orderly change is expecting the improbable, and what we face is a disorderly panic.

A long as our politicians say one thing, and do another, he's right - nothing will change for the better. But change will come. And it isn't going to be pretty.

Those disaffected property owners he writes of are going to be savaged by the change when it comes. And come it will.

Have a look at what is being built in Queenstown today, that wasn't a decade and more back - houses with Panic Rooms; rooms to keep the owners safe if/when the angry mob arrives looking for someone to blame for what is a problem of our own making.

It's still not too late for change to be orderly, but time is no longer on Hickey's; our politician's or our side's.

They won't let nominal house prices fall. Currency debasement is what they are going to do.

That laughable 1% - 3% CPI mandate is going to be ignored even more seriously.

91* at $5 per litre, you reckon? Could be.

I guess there's all sort of ways of 'fixing' the property market mess, and that might just be one of them.

That - 91 at $5, or even say $3.50 - would have interesting implications in terms of all the housing that is being on the outskirts of Auckland....

So we sit in million dollar houses but can’t afford a box of chocolates I don’t think so, if NZD is not protected as it’s will be need to be if US fed raise rates and we don’t inflation will destroy everything look at turkey right now

How is a "Panic Room" going to help you when things go south ? Are you planning to spend the rest of your life in there while the "Mob" lives in your house ? I think you need to think of alternatives, the Americans are experts at it its called "Self Defense".

Seems incredibly stupid to look to guns and panic rooms to hide from the impoverished and angry folk one's greed causes, rather than simply not creating those impoverished folk in the first place. But perhaps it's not surprising greed and narcissism don't consider the wider consequences of actions and policy.

Yes, guns and panic rooms would be stupid.

That's why robot warriors will be the ordre du jour for the elite.

There is always a solution.

Zachary was right. We truly are Elysium!

Upvoted!

yes Hickey and Jenee are onto it (the int.co effect) . Jacinta doing her best to avoid. How long before they get the press conference ban then?

Hickeys exactly right and saying exactly what many of us said should have been done at the start of all this, helicopter money to all was they right thing to do. Instead the gubbmint did the wrong thing, bailed in the already wealthy.

Remember the traitor Grant Robertson at the start of all of this who claimed "we cannot let inequality take hold", then went out and damn well made sure to entrench inequality through horrific policies.

Malice or incompetence?

My gut tells me incompetence, in the form of perfectly normal ivory tower syndrome. I am sure he is busy, but if he woke up and realised the damage the inequality is causing there are plenty of finance nerds he could tune into who know that more top down stimulus is freaking stupid.

Anyway, it's too late - massive offshore forces are currently shaping our future and our little govt has already fired almost all our ammo and future ammo.

I track the Lower Hutt housing market and the wellington market.

Lower hutt has as of today 416 listings (a 5 year high) and double this time last year. current sales are 40 listings a week - meaning there is 10.5 weeks SOH. Something listed today is likely to take until late Feb to sell - considering sales will be few over the last week of Dec and first week Jan.

Of the 425 listings - 189 have been on the market more than a month (45% of all listings).

Approx 50% - 204 of the listings have an advertised price. Some houses list with a price - most are adding a price when they fail to sell at auction or tender. Those with a price - approximately 30% have decreased that price since listing with a price - with the average price decrease been $47K. One house has dropped the price from $1.06M to 900K and is still yet to sell after 2 months on the market.

A buyers market is usually defined as

1. More houses than buyers- usually 2.75 months stock (11 weeks) is a definite buyers market - Lower hutt would be close on this.

2. Majority of houses list with a price and dont use auction or tender as there are not enough buyers to create competition.

3. The majority of houses listed have been on the market longer than 4 weeks

3. Sellers begin to increasingly decrease listing prices in order to sell their house quickly.

All of the above factors were used to categorise Sydney's housing market decline in 2018-19. The total decline in that market was 12% from the mid 2017 peak.

And we conveniently forget that, as detailed in your post, this has all happened before - right here.

In the mid 90s, Queenstown had 28 agents. In one particular month (May), between them all, they sold 4 properties. I asked one of them (Locations Reality, now First National?) "How long do you think it would take to sell my place if I wanted to?" The reply "Probably 18 months", and if I was lucky I might get $100k less than what it cost me to build. That's what competition does when it gets desperate.

The thing virtually economists miss regarding property busts, is the massive multiplier through the economy of the housing boom in net debtor nations.

Huge amounts of capital is borrowed offshore to purchase residential property, this cash is immediately injected into the economy as total mortgage debt increases. Some of this money is used to construct new houses, but a lot is used to purchase cars, jet-skis, swimming pools, boats etc. So during the boom years the economy lives beyond it's means via the spending of overseas capital. Like a household that has a net income of 100K per annum, borrowing 50K per annum for 3 years. For the 3 years they appear to be doing very well as they spend 150K per annum. But, after the 3 years the income reverts to 100K less interest payments (with or without capital payments) on 150K of debt.

This is the crux of the issue. It would be different if the overseas capital was used to facilitate production, such as robotics, automation etc. But, a lot of the money if spent on in installing new bathrooms and kitchens with granite benchtops, in rental properties in low socio-economic areas that have been reno-ed during flips.

So we have an economy that has a level of economic activity predicated on increasing mortgage debt levels provided from offshore sources. As soon as the level of mortgage debt growth slows the bust begins, even flat property prices is enough to trigger the start of the bust. Property related activities is 20% of NZ GDP, before the GFC it was about 10%. Of note the US figure before their GFC was 20%.

I think we need a correction now.

Imagine if they keep pumping qe, cram in another 3 - 4 years worth of immigrants etc. Making it worse.

We need to clear this mess and reset before to the cost of climate/energy starts to kick in.

The % sold for the same weeks as article, year on year

2019 2020 2021

57% 62% 68%

52% 54% 67%

48% 59% 62%

45% 59% 62%

46% 60% 59%

49% 57% 50%

56% 58% 43%

49% 53% 34%

47% 56%

For those suggesting that it is just a normal seasonal trend

Hello FONGO - its next year calling

Nice post, clearly shows the stark fall away this year.

Higher interest rates AND more restrictive lending are clearly having an impact.

How can they not. Tax avoidance debt junkies are facing inflation for their daily fix. What happens as the fix becomes further away just like watching home ownership dreams of our future taxpayer generation have been stolen in favour of debt speculation and bank profit.

Lets ask a junkie...how long do the Headhunters extend credit when you cant pay?

Greg, I’d like you to consider seasonality in your analysis. Maybe at this time of the year near Christmas the clearance rate drops from the spring flush results of October? I don’t know the answer, but we do need to consider this.

It will be interesting seeing what happens in the New Year, bearing in mind as well that the new national intensification rules are now passed by Parliament and whether this will push up prices for property in areas deemed highly desirable by developers.

See the post above yours.

I think prices in Auckland will go flat maybe-5% drop,prices will stay the same if not grow by5% around the rest of the country, major towns and city's like Nelson etc, rising interest rates are the key factor here,,

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.