The Commerce Commission says its draft decision on the interchange fees businesses pay to accept Mastercard and Visa payments would lead to a $260 million annual fee reduction, and see surcharges consumers are stung with drop to between 0.7% and 1% from an average of about 2%.

"We’re proposing a reduction of around $260 million a year to the largest component of the fees charged to New Zealand businesses to receive Visa and Mastercard payments. We’re also setting the clear expectation that payment providers and businesses should pass these savings on to customers,” says Commission Chairman, John Small.

"If our draft decision is implemented, we’d expect to see consumers benefit from lower surcharges of around 0.7% to 1.0%, or through prices of goods and services that reflect the lower fees. We’ll be doing more work next year to determine whether, and to what extent, regulation of surcharges is necessary," says Small.

"The average merchant service fee for small businesses is around 1.2% to 1.5% [of the transaction's dollar value]. This means costs for some businesses will be more, and for other businesses will be less. The Commission expects any surcharges to not exceed costs, and encourages businesses paying more than 1.5% to check if they can get a better deal from their existing or new payment provider. "

The Commission estimates consumers pay up to $150 million in surcharges annually with up to $65 million of this "excessive," and businesses pay $1 billion in merchant service fees each year to accept Mastercard and Visa card payments.

It wants "excessive" surcharging to stop, regardless of any changes to interchange fee caps.

"We consider that surcharging, whilst a point of annoyance for some consumers, is a valid part of the retail payment system as it reflects that some payment types are more costly to merchants than other payment types such as Eftpos and new account-to-account payment methods," the Commission says.

For in-person payments, consumers should be offered a surcharge-free option, it adds. And where a merchant is unable or unwilling to provide a surcharge-free option, such as Eftpos, the payment shouldn't include a surcharge.

Regulation of surcharging to be considered, with 'excessive' annual charges of up to $65m

Small says the Commission will be looking next year to ascertain whether, and to what extent, regulation of surcharges is necessary.

The Commission says New Zealanders spend about $45 million to $65 million annually in "excessive" surcharges. It says excessive surcharging rates need to fall, and with a further reduction in interchange fees its expectation is surcharge rates should follow.

"The average surcharge rate is almost double the average merchant service fee for those businesses. Some small businesses are paying less than 1.5% on average to accept Mastercard and Visa card payments, while others are paying over 2.5%," the Commission says.

"The variability and complexity of these merchant fees can hinder appropriate surcharging."

"It seems likely that some form of surcharging regulation will be needed, given the extent of excessive surcharging currently, even if this draft decision is implemented. We expect to consult on surcharging regulation in the new year. We are considering options such as a maximum surcharge rate, requirements to display average merchant service fees and/or requiring terminal providers to sight evidence of average merchant service fees prior to uploading a surcharge rate to a terminal," the Commission says.

The Commission considers excessive surcharges to be surcharge rates higher than the average merchant service fee paid by NZ businesses for in-person transactions. This estimate is based on data provided by what's described as a large NZ terminal provider and Commission analysis, taking into account transaction values from merchants likely to surcharge.

"We will continue to monitor and evaluate the magnitude of the issue. We note Mastercard estimated excessive surcharging to be more than $90 million annually," the Commission says.

Interchange put at 60% of merchant service fees

The Commission says interchange fees comprise about 60%, approximately $600 million, of the merchant service fees paid by New Zealand businesses for accepting Mastercard and Visa card payments.

"If our draft decision is implemented, it would significantly reduce the fees businesses pay to make and receive card payments. These fees are high in comparison to many other comparable countries. The fees are also overly complex, hindering a business’ ability to understand their merchant service fees and accurately surcharge," the Commission says.

Interchange fees are charged by the financial institution, typically a bank, on one side of a payment transaction to the financial institution on the other side of the transaction. A typical card transaction involves four parties the cardholder, the cardholder's financial institution (the issuer), the merchant and the merchant's financial institution (the acquirer). For most card transactions, the interchange fee is paid by the acquirer to the issuer.

Visa and Mastercard point out, unlike scheme fees, interchange doesn't generate revenue for them. However it underpins and grows their networks and is the biggest component of merchant service fees paid by merchants to their banks. Interchange can thus drive up costs for merchants and ultimately consumers too, being reflected in retail prices and surcharges, with some also rebated to card holders as rewards.

They're also complicated. Visa and Mastercard have hundreds of interchange fee categories, impacting the cost and transparency of the merchant service fees paid, merchant service fee pricing and the accuracy of merchant surcharging.

The Commission says interchange provides a revenue stream incentive for entrance and expansion in supplying Mastercard and Visa cards to consumers. It acknowledges this revenue can also contribute to covering the costs of issuing credentials, including producing physical cards and investing in anti-fraud services and technology.

"The interchange fee, a feature of the Mastercard and Visa networks, is set at levels that result in merchants paying higher merchant service fees for accepting Mastercard and Visa payments than they need to. This in turn means consumers are paying, directly and indirectly, more than they need to for goods and services," says the Commission.

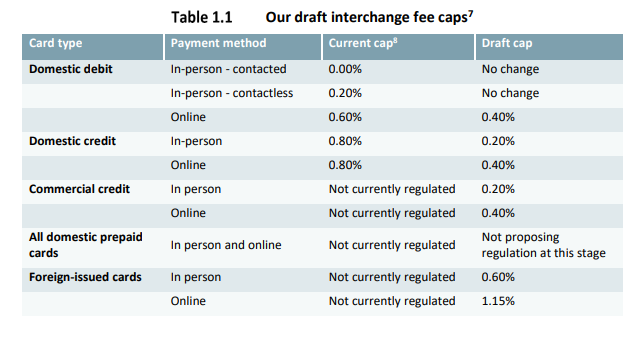

"If we were to implement these draft fee caps [see table 1.1 below], we would expect reductions in interchange fees to be passed through to businesses in the form of lower merchant services fees and we will be monitoring this closely. We are conscious that the benefits of reducing one component of the merchant service fee may be partially offset if there are increases to other components. We will continue to monitor the components that make up merchant service fees, especially the scheme fees charged by Mastercard and Visa to card issuers and acquirers," the Commission says.

The Commission says its draft decision will reduce and simplify the interchange fees in NZ to levels reflecting the cost and value of accepting card payments, promoting competition and efficiency in the retail payment system.

"Interchange fees play a role in the early stages of a retail payment product by fostering both demand and supply through network effects. As these payment systems become widely accepted and essential, as they are in Aotearoa New Zealand, the necessity for high interchange fees diminishes because the systems become more self-sustaining. Moreover, the two-sided market dynamics in the payment system results in competition between the Mastercard and Visa networks driving interchange fees above efficient levels, creating unnecessary frictions and cross-subsidies. For instance, non-cardholders end up paying higher retail prices to subsidise rewards for cardholders," the Commission says.

"We estimate a reduction of approximately $260 million in interchange fees paid to Mastercard and Visa card issuers annually. Domestic card issuers will see a $200 million reduction and foreign card issuers will see a $60 million reduction."

*Table 1.1 and notes 7 and 8 below come from the Commission's draft decisions and reasons paper.

7 We note that a flat fee (such as a fee in cents) may be charged so long as that fee complies with the relevant cap when converted to a percentage of the transaction value.

8 These are the specified maximum interchange fee rates from the initial pricing standard. The cap for a transaction is the lower of this specified maximum and the interchange fee as at 1 April 2021.

No regulation for prepaid payment products

The Commission says it's not proposing to regulate domestic prepaid payment products because they act as a gateway product for fintechs, new entrants and the underbanked.

"Therefore, the potential cost of erroneously deterring the issuing of domestic prepaid payment products, through a reduction in interchange, could be high, and competition and innovation may be detrimentally impacted," the Commission says, citing submissions from fintech and aspiring bank Dosh, plus Sharesies.

In terms of open banking, the Commission says payment products seem at least in part, to be competing based on the lower cost to merchants and the lower cost to consumers given there's no surcharge, whilst offering the convenience of contactless payments.

"We therefore need to be mindful of reducing interchange fees so low that the uptake of open banking is not hampered," the Commission says.

"There are still issues preventing open banking payments from being more competitive, including the prices some banks are charging for access. We are seeking to address these in our open banking work."

'Not able to rely on competition'

The Commission says it can't rely on competition alone to "drive interchange fees to efficient levels." That's because competition pushes Mastercard and Visa to set interchange fees above efficient levels to win market share by enabling card issuers to offer lower cardholder fees or other benefits.

"Moreover, merchants are susceptible to Mastercard and Visa networks exercising market power over them. Both the prospect of accessing more customers by accepting card payments and the ‘must-take’ nature of established card networks arising from the fear of missed sales imply Mastercard and Visa can set interchange fees higher than efficient levels," the Commission says.

"This can be done with minimal merchant resistance. Interchange fees set at efficient levels will balance the costs and benefits of using the network and lead to optimal usage and costs for both merchants and consumers."

"While we have limited ability to determine the precise efficient levels of interchange fees for New Zealand, we have considered how the current levels differ from other jurisdictions and relativity across fee categories to assess the trend. Compared to the EU, UK and Australia, interchange fees are generally set higher in New Zealand. Moreover, the rates for New Zealand vary more depending on card type and payment method," the Commission says.

Consultation on the Commission's draft decisions is open until February 18. It'll then make a final decision in the second quarter next year, with new interchange fee levels taking effect from November 2025.

The Commission's oversight of retail payments comes via the Retail Payment System Act, passed by the previous Labour government.

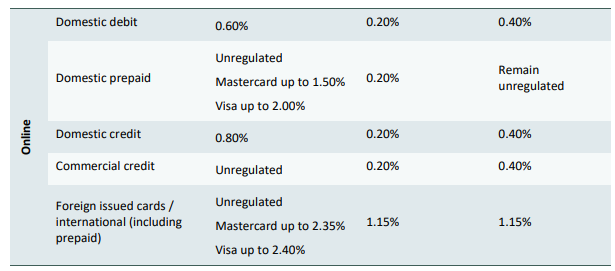

*Table 2.1 below and notes 22, 23, 24 also come from the draft decisions and reasons paper.

22 We note that a flat fee (such as a fee in cents) may be charged so long as that fee complies with the relevant cap when converted to a percentage of the transaction value.

23 These are the specified maximum interchange fee rates from the initial pricing standard. The cap for a transaction is the lower of this specified maximum and the interchange fee as at 1 April 2021. Unregulated rates taken from Mastercard and Visa interchange fee tables. Mastercard domestic rates available at https://www.mastercard.co.nz/en-nz/business/overview/support/interchange.html; Mastercard international rates available at https://www.mastercard.com.au/enau/business/overview/support/interchange.html; Visa domestic rates available at https://www.visa.co.nz/about-visa/interchange.html; Visa international rates available at https://www.visa.com.au/about-visa/ap-intra-regional-interchange.html.

24 Commerce Commission "Costs to businesses and consumers of card payments in Aotearoa, New Zealand: Consultation paper" (23 July 2024) available at https://comcom.govt.nz/regulated-industries/retailpayment-system.

6 Comments

'Setting expectations' is always a foolproof way to ensure compliance

Still seeing paywave fees at some tills of 3%. What in the actual?

Gareth, do you have any idea how providers like Stripe would be impacted by any proposed regulations? Their fees are 30c + 2.7% per transaction for domestic cards and 30c +3.7% for international cards - which is higher than any of the charges listed in the ComCom doc ... and are in addition to the MasterCard/Visa card charges?

I don't believe Stripe's network(s) is/are designated under the Retail Payment System Act. Therefore they're not overseen by the Commerce Commission.

https://comcom.govt.nz/regulated-industries/retail-payment-system

OK, thanks.

About friggin' time.

All the ticket clippers involved recouped their initial set-up costs at least 25 years ago and have been creaming it every since by hiding behind layers of obscene obfusication and secrecy.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.