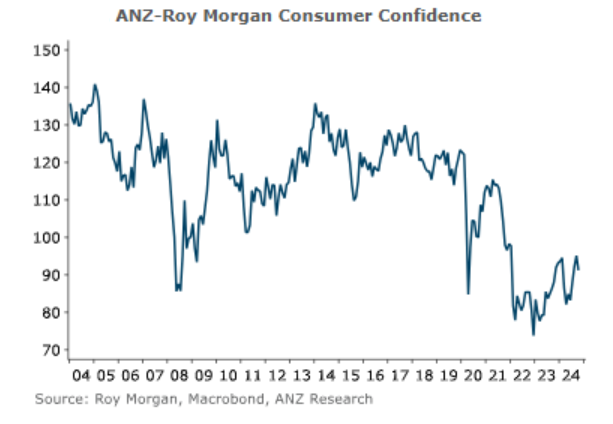

Consumer confidence fell in October after three straight months of increases, with job security fears taking a toll, according to the latest ANZ-Roy Morgan Consumer Confidence Survey.

The survey shows consumer confidence fell four points in October to 91.2, with both the current and future conditions indexes declining. Two-year ahead inflation expectations were unchanged at 3.8%. Expected house price inflation year-on-year rose to 3.4% from 3.2%

"Falling interest rates had spurred a cautious recovery in consumer confidence from July, but October marked a sombre return to reality. Interest rate relief won’t be immediate for many households, and there are still plenty of challenges to navigate in the near-term as job security fears add to uncertainty. Given the labour market lags the broader economic cycle by around six months, deteriorating employment conditions are likely to be a headwind well into 2025," ANZ NZ economists Sharon Zollner and Henry Russell say.

"The good news for households is the Reserve Bank has accelerated the pace of [interest rate] easing and is likely to deliver another 50 basis point cut by year end, bringing relief a little closer. Meanwhile, with CPI [consumer price index] inflation back in the [1% to 3%] band and within touching distance of the 2% target midpoint, the inflation challenges of the past few years that have battered consumer confidence are drawing to a close. That adjustment certainly hasn’t been without cost, and those costs will continue to be felt into next year, but brighter times do lie ahead."

Zollner and Russell note interest rate cuts will take time to flow through to mortgage borrowers, with about 65% of mortgage holders set to refix over the next 12 months.

"The wait certainly isn’t without its challenges as labour market conditions continue to deteriorate. The impacts of deteriorating job security are particularly evident in the regional cut of the data. Wellingtonians remain the most pessimistic across the country, with ongoing public sector job losses and the wider fallout from that likely weighing."

The latest Statistics NZ figures showed an unemployment rate of 4.6%, or 143,000, in June, up from 4.4%, or 135,000, in March.

The survey's future conditions index, comprising forward-looking questions, fell to 100.3 from 105.6. The current conditions index also dropped, down two points to 77.6.

Perceptions of current personal financial situations fell six points to -22%. A net 14% expect to be better off this time next year, down 11 points. A net 23% think it’s a bad time to buy a major household item, up two points. Perceptions regarding the economic outlook in 12 months’ time fell two points to -19%, with the five-year-ahead measure down three points to +6%.

A total of 1,002 people were survey. The full survey release is here.

Consumer confidence

Select chart tabs

48 Comments

If I read that chart correctly, consumer confidence is lower now than in the GFC, and has stayed down for longer.

Indeed. In 2008 confidence dipped below 100 for 5 months, today confidence has been under 100 for exactly 2 years and counting.

Back on track.

Steady hands in the wheelhouse, avoiding all the losers out there slowing us down.

Our GDP growth is one of the lowest of all the countries in the world. The only ones below us are countries such as Haiti, Sudan, and some other war torn places. Though surprisingly, Finland is also down the bottom with NZ.

It will pick up quickly IMO. GDP went down when interest rates went up, now that interest rates are going down I expect GDP to go up.

Please elaborate on ‘quickly’.

I completely disagree. I think things will be grim for the first half of ‘25. Things might pick up a little Spring ‘25

Depends on whether you mean GDP stats coming through (which can be almost 5 months delayed) or other signs such as card spending.

A large number of mortgages will be refixed in the next few months, and if they all fix for 1.5% less (or even better), that is a lot of extra cash that will probably be spent.

But few over the next 6 months will be 1.5% less. Some will be 1% less. Many will be similar, or just a little less, to 2 years ago if they took out a two year mortgage.

You talk about things tanking as interest rates went up. But it took a good year or more to start tanking after the hikes commenced. Similar timeframes will play out as rates are cut

Anyone that fixed within the last year or so is on ~7%, and now you can get ~5.5%, and soon it will be even lower.

I think the delay when rates went up was because many were fixed for 2 -> 5 years, now almost everyone sensible is <1 year.

But yes I agree it could take until next spring. Particularly if businesses can't wait it out and cut more staff or go under. But my gut feeling is early next year we will see card spending etc increase fairly significantly.

sorry last time I looked no one rated your opinion on Bloomberg

This is entirely as expected. Job insecurity is now front and centre. On the back of FOMO, some here STILL predict house prices are about to take off back to where they were and beyond - WOW.

Still lumbered with high costs of living, it's more like a fear of missing out on an income now.

Not sure what you are going to do when house prices start going up over the next few months, I suspect you will pop a vein while sitting on the toilet.

I don’t think they will fall anymore (several months ago I called the bottom in Spring), yet I doubt they will increase by more than 1-2% over the next 6 months.

Zwifter, I suspect you'll be gone after 01 March 2025 when you have to pay to post your usual bile ✅

Jeez, wee bit of venom in that one RP…it’s Friday…chill a bit eh 🍻🥩👌

Just curious, why are you offended? I was responding to Zwifter. I'm sure he took it well.

It's interesting how you didn't have anything to say on this article RP...

https://www.interest.co.nz/personal-finance/130398/latest-mortgage-figu…

If consumers confidence is so low, how could mortgage lending be rising so fast?

There’s a fairly weak relationship between the two. Consumer confidence is a societal wide issue, an uptick in mortgage lending is from a small % of the population

It's interesting how you didn't have anything to say on this article RP...

Nifty1, you're one of the first to complain that I comment on too many articles then suggest it's "interesting" when I don't.

I'd suggest you've become overly consumed with my posts. This is not healthy.

Answer the question poppy...

If consumers confidence is so low, how could mortgage lending be rising so fast?

by HouseMouse | 25th Oct 24, 12:08pm

There’s a fairly weak relationship between the two. Consumer confidence is a societal wide issue, an uptick in mortgage lending is from a small % of the population

I didn't need to....

I see you now feel the need to start name calling. That speaks volumes.....

Yeah you do given your comment linking the two..

by Retired-Poppy | 25th Oct 24, 11:27am

This is entirely as expected. Job insecurity is now front and centre. On the back of FOMO, some here STILL predict house prices are about to take off back to where they were and beyond - WOW.

Still lumbered with high costs of living, it's more like a fear of missing out on an income now.

Quick Nifty refresh - refresh -refresh that screen for my next response.....LOL!

Are we looking at the same graph? Describing mortgage lending as "rising fast" seems a stretch.

Lol, we're still paying off mortgages quicker than we are taking them out - that's highly contractionary.

As this collides with the considerable amounts parked in TD's, rates are falling off a cliff. It might not be so bad if such people weren't so convinced assets such as houses will underperform as an asset class for the foreseeable future.....

yep its turtles all the way down

Not offended, just felt it unnecessary…but hey, there’s no need for me to comment on it either

When life is unaffordable becoming slightly less unaffordable dosnt make much difference....we have a distribution (inequality) problem that will likely undo us even before the impacts of climate change/overshoot.

Everyone in that 1000 person survey sample is now a maximum of 2 degrees of separation from someone who has lost their job. Orr must know by now his MPS in May was dumb as F.

Let’s get real, the economy is screwed. The occasional , slightly more positive indicator does not negate that

Makes me scared how stupid/aggressive the response might be…what is the conversation going to be about in two(ish) years 😬

You mean OCR will be cut aggressively and house prices will shoot up again?

This is why he needed to cut earlier, he needed to be ahead of the game. Most of us predicted this would happen, the lever is being yanked in every direction.

Nah, you repeatedly said it was going to be a soft landing

I repeatedly said it looked like it was going to be a soft landing based on the stats at that time (and by the way we still haven't met our agreed criteria of a non-soft landing which was unemployment > 5% although we almost certainly will). My original non-prediction was soft landing 30% chance medium landing 40% hard landing 30%.

I expected Orr to keep the brakes on too long, but he went quite a bit further than I expected. I would have cut in January, I thought he would ~April, instead he suggested he was going to make another increase just to completely kill the economy. Earlier this year a soft landing was on the cards.

You are being creative with the truth. Have a lovely day

HM…yep, I hope I’m wrong & just being negative but the deeper this goes & the worse the number look surely the higher the odds of the printer being turned on, rates getting slashed & the restrictions (that we will desperately need) being eased or removed…property is the only thing that will give the economy a quick fix (well, fix isn’t the word but you get my drift). As much as people comment it can’t work this time, the capacity is there for the can to be kicked again.

It’s hard to know. If you believe Orr, rates won’t come down that far or that quickly. If retail rates bottom out around 5% I don’t think we will see the housing market take off. However, Given how screwed the economy is, and how little the government is trying to stimulate it, I suspect monetary policy will need to work harder than Orr suggests (is he playing mind games?). I think the OCR could easily be 2% this time next year, in which case retail rates will be circa 4% Strong chance that would stimulate the housing market quite strongly.

Hopefully My Orr is playing mind games and being clever. If he actually wants to wring out the last bit of inflation and ends up killing off the economy altogether that would be unfortunate.

Rents seem to have stabilised, perhaps because house owners can now write the tax off again. Interest rate cost push should be reducing, insurance payments have made their price increase adjustments. The only outlier now are the councils and any further rate rises from them. So local inflation is driven only by firms trying to recover their margins, mostly professionals.

Oil is up and down but major factors for overseas driven inflation have fallen away.

I myself see the balance as tilted towards disinflation. I think Orr needs to end his part of the current contractionary bias of credit and interest rates and move much more quickly to returning monetary policy towards support of the economy rather than adding to the contraction.

Definitely, if the govt don’t come to the party soon then he’ll have to take it well below the NIR, chalkboard rates at 4% & then all bets are off with regards to continuing downwards spiral for the HPI…the longer/deeper we go the more I can’t help but think it’s likely 😣

What were you responding to Jfoe?

House mouse comment on house prices taking off.

Only very very gently was my pick JFoe!

But will it continue?

Don't forget that a drop in mortgage rates is matched by drops in deposit rates. So any increase on the mortgage holders side of the income equation will be matched by drops in income / spending on the deposit holders side. Sure not a one to one relationship but the idea is that the drop in interest rates will still have an effect on confidence and willingness to spend in a different part of society.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.