TSB has cut its one year fixed home loan rate to 5.99%, a -30 bps drop.

It is the lowest they have offered for that fixed term since December 2022.

And they are the first bank to offer a one year rate below 6% on their rate card.

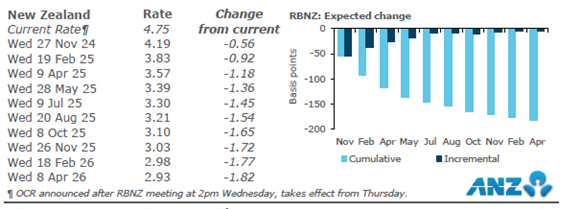

Following the Wednesday OCR rate cut, almost all the action has been on floating rate changes, and almost all of them have mirrored the -50 bps OCR cut.

But wholesale money markets wobbled briefly over the past few days, but have settled back into easing swap rates.

Those wholesale markets are now pricing in a full -50 bps cut again at the November 14 Monetary Policy Review by the RBNZ. So there remains pressure on the cost of money, and fixed home loan rates are likely to keep falling while that pressure is there.

In real estate markets, despite all the gung-ho commentary by hopeful participants, there is still no sign that sales volumes are picking up above their normal seasonal patterns. In fact, if anything, they are undershooting. Our auction monitoring suggests that while more properties are being offered, fewer are actually selling.

And that is a problem for real estate markets because they rely on momentum as part of their general market pitch.

And it is a problem for banks, because new transactions are needed to meet their lending targets. They can't achieve those on refinance activity alone.

So competition is pointed at present. And to avoid queering the pitch, a lot of that is going on 'off-card'.

Those off-card rate offers are now below 6% for a couple of banks other than TSB already (ANZ and Kiwibank). We know that because customers with a home loan can see updated offers from their bank in their bank app. And these often offer significant discounts from the rate cards published.

So we have been asking readers to help shine a light on this opaque practice. Please note actual bank-app offers in the comment stream below and we will add them to our table. This should give borrowers a stronger view of where the mortgage rate market really is.

Almost all banks will have some flexibility in their rate offers. So the carded rates are just the start. Negotiate. How flexible they may be will depend on the strength of your financials.

One useful way to make sense of the changed home loan rates is to use our full-function mortgage calculator which is below. Term deposit rates can be assessed using this calculator.

And if you already have a fixed term mortgage that is not up for renewal at this time, our break fee calculator may help you assess your options. Break fees will be minimal in a rising market. But they become important in a falling market, like now. Don't forget, when you sign up for a fixed rate you are signing a contract. You have been given the right to break it in legislation but the bank has the right to reclaim its costs when you do so. This is NOT evidence of banks making it hard to switch (as some borrowers, and sadly some journalists seem to think).

Here is the updated snapshot of the lowest advertised fixed-term mortgage rates on offer from the key retail banks at the moment. (Be aware that the reader-reported rates are unofficial and may be quite fuzzy themselves.)

| Fixed, below 80% LVR | 6 mths | 1 yr | 18 mth | 2 yrs | 3 yrs | 4 yrs | 5 yrs |

| as at October 14, 2024 | % | % | % | % | % | % | % |

| ANZ | 6.75 | 6.19 | 5.89 | 5.69 | 5.69 | 6.19 | 6.19 |

| current reader-reported rates | 6.69 | 5.59 | 5.69 | 5.59 | |||

| 6.75 | 6.19 | 5.89 | 5.69 | 5.69 | 5.69 | 5.69 | |

| current reader-reported rates | 6.59 | 5.99 | 5.75 | 5.59 | 5.59 | 5.59 | 5.59 |

| 6.75 | 6.19 | 5.89 | 5.79 | 5.79 | 5.69 | 5.69 | |

| current reader-reported rates | 6.69 | 6.09 | 5.75 | 5.69 | 5.65 | 5.59 | |

| 6.85 | 6.29 | 5.79 | 5.79 | 5.69 | 5.69 | ||

| current reader-reported rates | 5.94 | 5.44 | |||||

| 6.75 | 6.19 | 5.89 | 5.69 | 5.69 | 5.59 | 5.59 | |

| current reader-reported rates | 6.75 | 6.19 | 5.89 | 5.69 | |||

| Bank of China | 6.75 | 6.25 | 5.95 | 5.75 | 5.75 | 5.65 | 5.65 |

| China Construction Bank | 6.89 | 6.45 | 5.99 | 5.99 | 5.89 | 6.40 | 6.40 |

| Co-operative Bank | 6.75 | 6.19 | 5.99 | 5.75 | 5.69 | 5.69 | 5.69 |

| Heartland Bank | 6.19 | 5.89 | 5.69 | 5.69 | |||

| ICBC | 6.69 | 6.15 | 5.85 | 5.69 | 5.69 | 5.69 | 5.69 |

| |

6.75 | 6.35 | 5.89 | 5.69 | 5.69 | 5.69 | 5.69 |

| from October 14 |

6.75 -0.10 |

5.99 -0.30 |

5.99 -0.10 |

5.69 -0.10 |

5.69 -0.10 |

5.69 | 5.69 |

Fixed mortgage rates

Select chart tabs

Daily swap rates

Select chart tabs

Comprehensive Mortgage Calculator

36 Comments

I have the following in app offers

6.59 6 month asb

5.99 1 yr asb

5.59 2 yrs asb

5.59 1 yr anz

The 6 month rate is looking expensive given the discount you can get off floating.

UPDATE

6.45% 6 month

5.59 1-5 yrs

5.68 18 month

I can verify I'm also being offered the same on asb app

be interesting to see if ANZ retire their "limited special" if none of the others choose to match them directly at that level... it's obviously a struggle if banks have the gumption to announce 5.99 as something special after ANZ's move.

Hi David, appreciate you keeping the 'dark' rates reported by readers up. It goes to show how competitive the market for new lending is, as the housing market continues to tank.

BNZ

6.69 - 6mth

6.09 1yr

5.69 2yr

5.65 3yr

5.59 4yr

ASB this morning

6.59 - 6mth

5.99 - 12mth

5.75 - 18mth

5.59 - 2/3/4yr

Most of these are only 10bps below carded rates - so nothing too great. The ANZ 1 year which has been reported widely is the stand out, and we've got confirmation now that other banks are matching this rate under proof of being offered the ANZ rate. The $50 home loan check in, appears to be on it's way out, so make the most of this before it disappears.

Interesting to watch carded rates over next 1-2weeks as the daily swap rate normalizes the ocr cut.

Ha I wonder how much the banks appreciate this new service from Interest?

You'll find these rates posted as screenshots from various customers apps, all over Reddit and various Facebook groups. Opening the curtain to the 'dark' rates is not limited to Interest. Stuff & NZherald have also recently posted articles about these rates.

In an ideal world the banks would be up-front and honest with all customers from the get go, and not have these special rates (they can keep their 0.10bp cut for staff & family, but otherwise be more transperant). It would drive more competitive behaviour from the banks, something that is seriously lacking in current market.

I'm getting the same rates from the BNZ app.

Thanks for creating this community David. I've got a lot of lending floating right now and it's really helpful to know what banks are offering behind closed doors.

Keen to know Westpac’s offline rates.

On app still showing:

6.75 - 6mth

6.19 -1yr

5.89 - 18mth

5.69 - 2yr

They are advising that they are still making decisions on what discretion the team will have go to below advertised rates.

*Edit - Westpac has a different weekly schedule to ASB/ANZ who normally are Wed/Thurs. Suspect Westpac to move shortly.

US inflation getting sticky again. Oil inching up. US 10yr Bond yields back over 4%. RBNZ has to cut again in November. But maybe only 0.25?

With the chance to refix in December would it be best to take the 1 year offer at 5.??% assuming it is still available? Or go again for 6 months and hope for better mid 2025?

Depends on what 6month rate you can get. The 5.59 looks good. The 6 month rate would need to have a 5 in it to make me go that way.

SBS on holiday apparently. Haven't even touched their floating rate

Why aren't these challenger banks competing? If ANZ can do such a sharp 1 year rate, why can't TSB do the same (or better), but actually advertise it. They would probably bring in a lot of new customers.

Hey Jimbo, heres a couple of useful links.

https://www.rbnz.govt.nz/financial-stability/about-the-new-zealand-fina…

Some interesting data on where banks get their money from. Suspect TSB et al, don't have the funds to be super aggressive.

&

https://comcom.govt.nz/__data/assets/pdf_file/0026/347372/5BPUBLIC5D-Dr…

Page 4 of the comcom report is telling. Basically the challenger banks aren't challenging enough - suspect due to lack of means etc. I know it's socialist policy, but the government on either side in NZ needs to cash inject Kiwibank so that they can actually have the balance sheet to compete as the much needed disruptor. Until then, both KB and the other small fish can just tinker around the edges and not actually have a ~5.5% 1yr rate available for x00,000 number of customers..

It’s funny that inept, unqualified, inexperienced fools such as luxon & willis & brown are allowed to run for public office

First you need to have a CV that demonstrates you’ve had experience in that area

Ah yes, triggered keyboard warriors always know better.

It’s Friday, go out for a walk.

Um. No. ... Their point is a good one.

Compare Willis's credentials to most of those in OECD and you'll see what I mean.

But she has a BA?

Luxon was the CEO of NZs largest airline provider, a business man, & was also practically handed the election last year a Ardern, a dj turned socialist political dictator & Hipkins, who was the previous health minister who lied to the NZ public on national TV regarding mandates being a choice, did so badly.

The power got to their heads, Ardern went extreme calling free speech am act of terrorism, & hipkins couldn't even define what a woman is. Together they drove the entire country backwards by historical margins over their 6 years tyanny reign. Their list of failures is astronomical.

At this point, only 11 months in, any changes Luxon & Willis make would be am improvement on our last 6 years of Labour lead wokeness. Over 75% of the country who voted chose not to vote Labour back in again for a third term. That speaks volumes at the carnage they left behind and the no confidence vote of three quarters of all voters. Don't expect Labour to be anywhere near governing for at least another 2 terms, minimum. "Let's do this"?

Playing with your stats is a fun!

62% didn't back the Nats. 91% didn't back Act, 93% didn't back NZF. 46.5% didn't want any of those parties. Nobody at the polls chose for there to be a coalition, and those that don't mind NACT tended to be anti-NZF.

If you want to claim people not voting for parties means they support something else overwhelmingly, there is no party that a majority of people like. The only clear takeaway from 2023 was people didn't want Labour to go on. They did not wholeheartedly endorse any alternative however. They certainly didn't strongly swing to the Nats. The current government is operating on a very weak mandate, especially in any policy areas those parties took to the 2020 election and were resoundingly defeated on. At this point if Winston carks it it's going to be all over.

Nice attempt nnz - "If you want to claim people not voting for parties means they support something else overwhelmingly"

I didn't make this claim. Re read carefully. I said 75% of the country who voted chose not to vote for Labour. I didn't say they voted National or the Coalition. Considering it's only ever Labour or National governing, if those 75% who didn't vote Labour really thought that the country would be worse off still under National, they would have voted strategically and voted for Labour purely just to keep National out of office. This did not happen.

However I can agree though, voting every three years for the lesser of two perceived evils red or blue, blue or red, seems rather counterproductive, considering neither parties have shown over decades to have what it takes to effectively govern the country and improve things. I think your right, personally if we had a choice I think a majority of NZ would chose neither of the two. We then need a party governing that's from the people, for the people.

Dodgy claim, all the same. Some swung further left from Labour in outrage of them not bringing in a wealth tax, for instance. Labour were unpopular for reasons of being too modest and centrist as well as the accusations from the right. The set of voters who changed their mind between 2020 and 2023 was the typical slither of about 1 in 10 kiwis. That's all it takes to change a government. 65% of the country could still hate Labour in 2026 and they could still lead a coalition. Such is life.

Labour = naive socialists

CEO of air nz a taxpayer funded monopoly is exactly why NOT to have that as prime minister utterly inept experience & their first year in govt has proven as all economic & social indicators are failing

Relax IT84, National can't undo 6 years of Labours taxing, penalizing, restricting and deviding policies that has put us backwards in every industry possible in just their 11 months governing. They're good but not that good. Patience. They'll need at least another 5 years to be even remotely comparable to Labours failures - even then, at this stage any "damage" National could do, would likely be an improvement on Labours last 6 years.

Bet you had the exact opporsite opinion back in 2017 when Labour took over from National and people started pointing out the early signs of Labours failures, when appeared quickly, I bet you were first to come to Labours aid to say something like "well they've only been governing for a year, they can't undo 9 years of Nationals damage under JK" lol Short term memory???

Can't have it one way and not the other. Either we carry on making excuses for previous governments and refuse to hold current governments to account for their failings, choosing instead to blame previous governments for current governments failings, or suck up voter pride, admit maybe the party you elected plunged the country further backwards, own it, take accountability, learn from it, and find a more proactive solution.

There is plenty of evidence to suggest that the last Labour government has been the worst performing government in NZs history. No amount of scapegoating to "oh look over there Nationals 11 months..." It's a complete cop out. Own your governments failures. This government had not nearly had enough time governing to undo their 6 years of damage.

Westpac offered me 5.69 for one year !

I have refix due last week

Should I wait another week?

Thanks

I think there will be another cut around the time or next months announcement. You could fix a portion now and remaining at that time. Not advice.

The article says that the next round of OCR cuts will be on 14th November, though I thought it was 27th November. Can you or anyone clarify?

It’s the 27th at 2 pm

Funny. Sounded like advice.

Mine would have been different ... :-)

What will be yours

If you float till the end of November, it will cost you an extra $200-250 in mortgage payments per $100,000 loan. If the bank drops the interest rate by a further 0.5% at the end of November then you will save $500 in mortgage payments per $100,000 loan over a 12 month period (if you then fix your mortgage rate) If only we had a crystal ball.

I'm with TSB and have a fixed loan coming off next week. Told bank manager to lock in this new 1 yr rate less my normal discount of 0.1. Got told I should wait until Monday for more rate cuts...

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.