If we needed confirmation that the June quarter 2024 was a rough one - it's provided in a big way by Statistics NZ's latest household assets data.

The data shows that during the quarter household savings decreased, the net worth of households dropped and - for the first time since this series started in 2016 - total household income decreased for the first time.

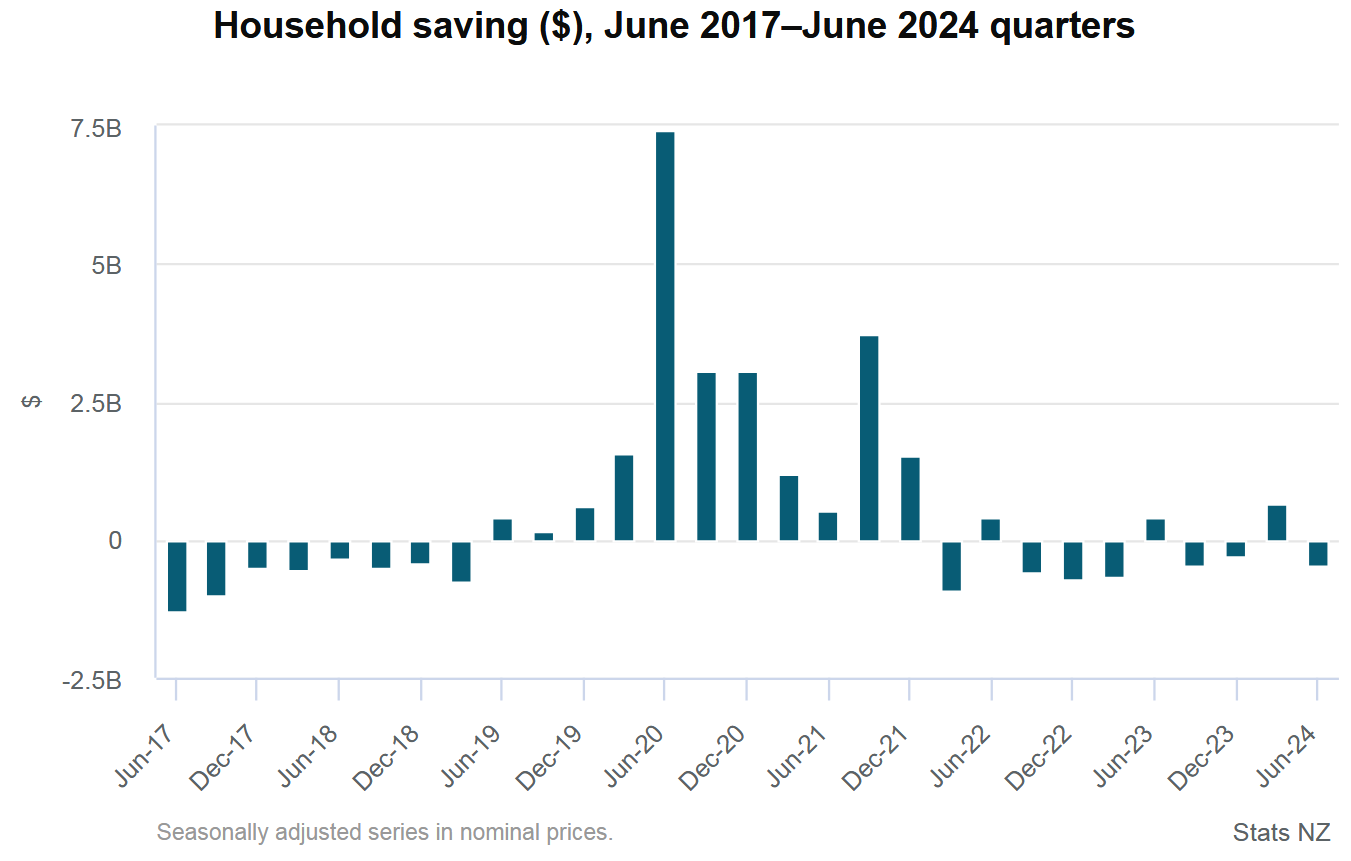

According to Stats NZ, household saving was a negative $479 million in the June 2024 quarter (a -$1.1 billion turnaround from the previous quarter's figure) as household spending increased while net disposable income fell.

Seasonally adjusted household spending increased 1% to $59.7 billion in the June 2024 quarter. The increase in household expenditure was driven by spending on services and non-durable goods like groceries, partly offset by a decrease in spending on durable goods like motor vehicles.

Meanwhile household net disposable income decreased 0.9% to $59.2 billion.

Total household income decreased 0.2%, which as mentioned above was the first fall since the start of this data series.

Stats NZ says household net disposable income is the amount of money a household has once all income such as wages, interest, and child support, and income payable such as taxes have been accounted for. It represents the money available for a household to save, spend, or invest.

"With net disposable income falling in the June quarter, the household sector is funding the increase in spending through borrowing and drawing on existing funds," Stats NZ's national accounts industry and production senior manager Ruvani Ratnayake said.

Westpac senior economist Satish Ranchhod said Stats NZ's update on households’ finances highlighted the continued pressures in the household sector.

He said adjusting for population changes, he estimates that disposable incomes for individual households rose by 2.8% in the year to June. That’s below the 3.3% rise in consumer prices over the same period.

"Looking at the past three months, the pressure on incomes has been particularly stark. In fact, a number of households have seen their earnings going backwards as small business profits have fallen."

Ranchhod said the combination of slowing income growth, high interest rates and large increases in living costs over the past few years "has been a significant squeeze on households purchasing power".

Ranchhod noted that some of the "powerful financial headwinds" that have buffeted households over the past few years are now easing off. Consumer price inflation is dropping back, and next week’s figures are set to show inflation back below 3% for the first time since 2021. At the same time, the RBNZ has been cutting the OCR, with a large 50bp cut on Wednesday and more expected over the next few months.

"It will take some time for those changes to flow through to households back pockets. And at the same time, the labour market is weakening, with unemployment set to rise above 5% before the end of this year. As a result, we don’t expect a big rise in spending through the back part of the year.

"However, there is a growing sense in the economy that the worst is behind us, with business and consumer confidence turning higher in recent weeks. Combined with reductions in borrowing costs, we expect to see spending and economic growth gradually pushing higher over the year ahead," Ranchhod said.

Stats NZ said growth in wages and salaries was 0.8% in the June quarter, lower than the average quarterly growth of 2.1% from December 2021 to March 2024.

"Slower growth in household wages and salaries reflects fewer working hours in the June quarter," Stat NZ's Ratnayake said.

Dividends received and the income of self-employed business owners and partnerships both decreased in the June quarter as well.

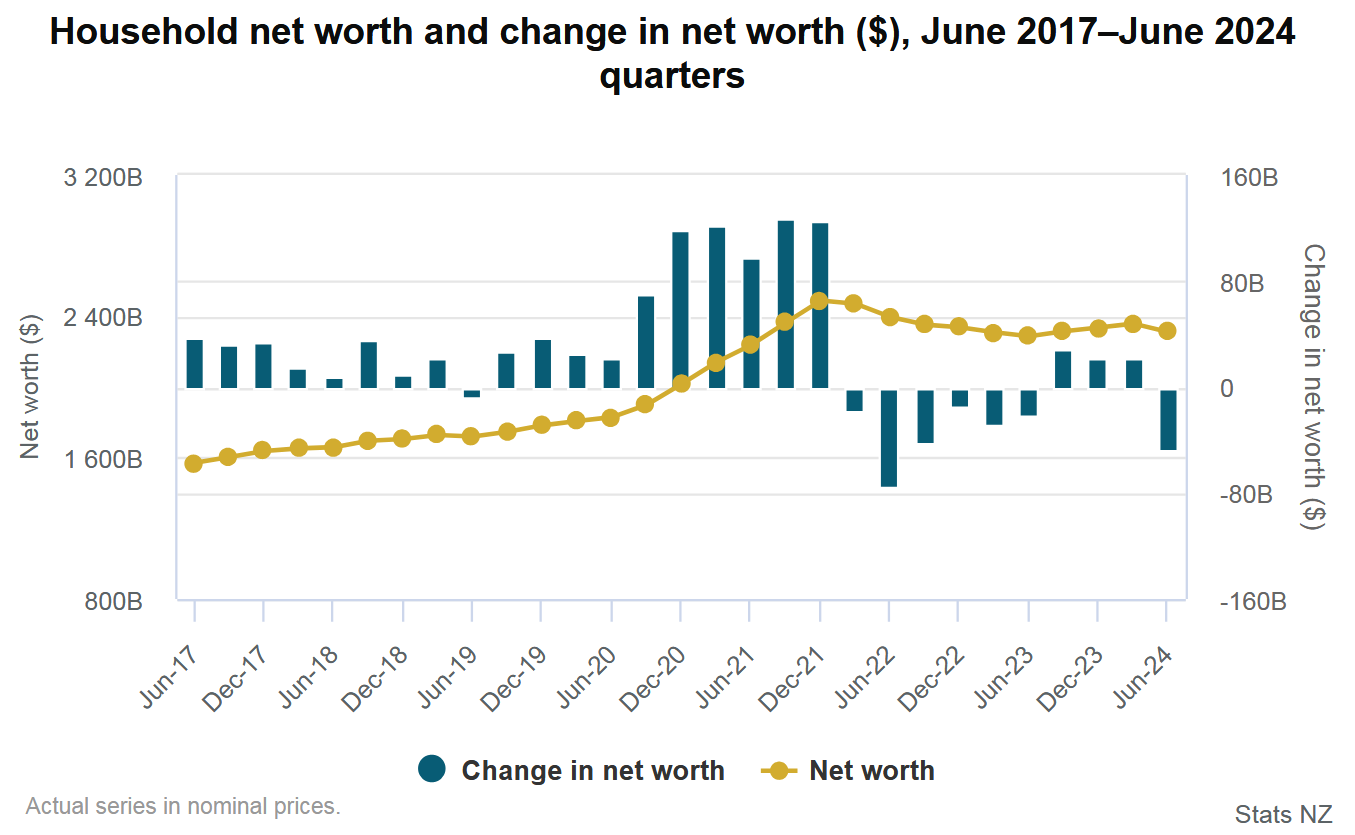

Household net worth decreased 2% ($47.1 billion) to $2,311 billion in the June 2024 quarter following increases in the previous three quarters.

Net worth is the value of all assets owned by households less the value of all their liabilities.

"Despite a fall this quarter; household net worth increased 1%, or $24 billion, over the year to June 2024," Ratnayake said.

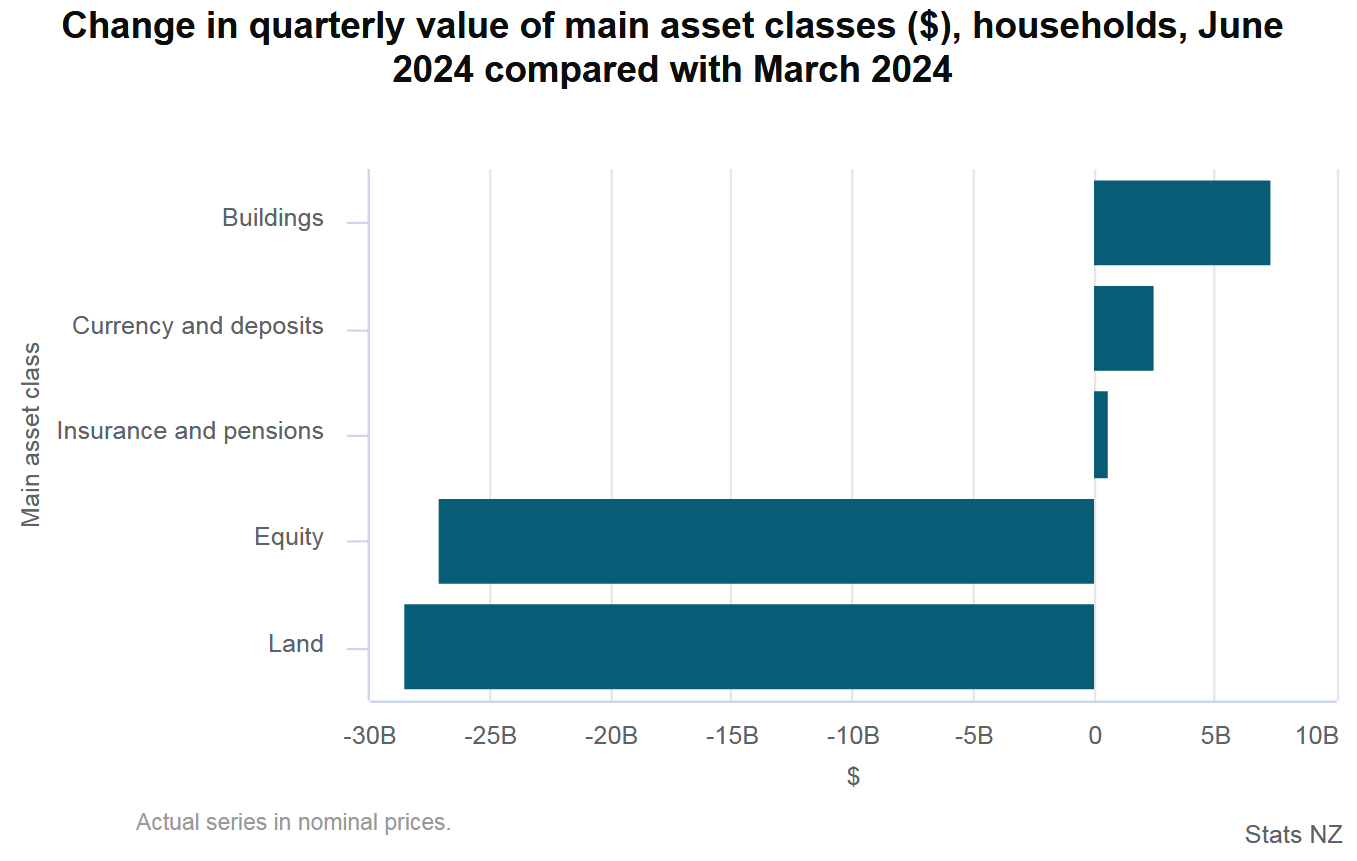

Among household assets, the value of owner-occupied property decreased $21 billion or 1.8% this quarter, and equity and investment fund shares decreased $27 billion or 2.6%.

Ratnayake said household equity assets include the value of rental properties less the mortgages held against them.

"The June 2024 quarter decrease in household assets reflects a fall in property values for both homeowners and landlords."

Household financial liabilities grew 0.7%, continuing a relatively steady increase in recent quarters. This was driven by a 0.9% increase in housing loans, and partly offset by decreases in consumer loans (1.2%) and student loans (0.7%).

41 Comments

"Slower growth in household wages and salaries" probably reflects the replacement of local labour with immigrant labour, as we export our professional/trades class to Australia and replace them with unskilled third world migrants.

Stats NZ's monthly employment releases show significant drops in filled jobs among the 15-to-29-yearl-old age bracket for several consecutive months in a row (May, June, July and August 2024) from the same months a year ago.

I reckon the mass exodus of young Kiwis has at least a major role to play, but the numbers still look rather concerning.

The government is asleep at the wheel, waiting for the central bank to also fix all structural issues facing the economy with its blunt instruments.

More likely the result of the equity bubble running it's course. This is exactly what happens when a country prints billions of dollars and funnels it directly into non-value add assets like residential real estate. Once the money is spent the party winds down but there is nothing to show for it, because houses don't have a continuing benefit to the economy like other forms of investment (eg. Infrastructure, R&D, business dev, etc.) Tradies and labourers aren't getting as many projects, fewer agents and brokers get a cut, and businesses have to retract. This is a NZ/economic ignorance problem not an immigrant/foreigner problem. Racism and xenophobia will only distract from the real issue.

Once upon a time, we were blissfully selling ever more overpriced real estate to one and other. The resulting wealth effect was treated like some newly created permanent phenomena and on the surface, it all looked really impressive.

Now that's all changed. It acts like a thief when in reverse.

A money go round and not exactly a merry go round whilst at it. Worth of NZ housing stock is meaningless. It earns nothing. It cannot be packed up and exported. Oh wait. Let’s just import the market, the buyers, instead and call it immigration.

... whilst we focus on our house prices , there's a world of A.I. tech creating astonishing wealth offshore ... and we're oblivious to it ... regardless that one of the greatest A.I. experts in the field is ex Rotorua High grad Shane Legg ... a co-founder of Deep Mind , now owned by Google ... the world is leaving us bricks&mortar boreds in its wake ... Legg came within a whisker of winning a Nobel Prize recently ... a fine Kiwi export ...

Robert is that you?

He is a legend , I'm a fan of his no BS logical positivism ...

We’ve got a lot of exceptional Kiwi tech talent, most leave when they figure out that those huge salaries people talk about online are in fact real. Some of us found remote opportunities to pull big tech salaries while living in NZ.

We need more incentives to foster this industry at home and we should be able to use our greatest asset, our societal capital. New Zealand is one of the most attractive countries in the world to live in with a family if you like the outdoors, and a shit load of tech people love the outdoors (because they’re trapped inside most days, we always want balance).

CGT would incentivise continuing to run a startup out of NZ rather than selling it to Americans to milk it dry and offshore jobs.

Tackling housing would make it easier to retain talent. Bring back LVTs, CGT helps here too.

Push for more tax incentives, RDTI is great but could be simplified rather than forcing everyone to learn how to say the same thing with the right magic words to qualify. Callaghan has been all but neutered as a source of funding.

Reduce the amount of low skill immigration to help ease the housing demand while making high skill immigration easier.

Continue the apprenticeship scheme and extend it to include kiwis entering into tech in NZ.

These are to my mind the highest value policies we could do to foster tech growth in NZ. Our issue is the we are losing our only existing edge right now, and that is quality of life. Housing costs and degrading public services are the cause of this.

SKF

Ernest Rutherford (who actually DID win a Nobel prize, just over 100 years ago) was also a fine Kiwi Export. The young&smart always knew that they will have a lot more opportunities to realise themselves in countries such as UK or US, so they leave. It's not a new phenomenon.

NZ has never been known for its 'opportunities', it's been known for its amazing nature, clean air, etc. instead.

500 million of disposable income dropped out of circulation in the June quarter. At the same time Households collectively got 47 billion poorer (due mostly to property price declines?). That's the wealth effect in reverse. No wonder we are in recession.

A 1% across the board reduction in interest rates on the total residential mortgage book will inject 900 million per quarter of additional disposable income into households. Will it be enough?

No.

They'll pay down Debt given the experiences we've all just witnessed (i.e. interest rates can and do rise against expectations, causing grief to the unaware). And is that 900m a Net or Gross injection? Because if it's Gross it misses the withdrawal of interest paid to the many who have savings providing liquidity.

No they won't. They had years of low rates to pay down the debt and instead they borrowed even more. Some people will go bust over the next 6 months because they could not ride out the storm but more will have increased disposable income.

And that's the point. They didn't pay down Debt last time - and not that long ago, and look what happened. This time, they will. "Experience is the best teacher"

900 million is based on 1% of the residential loan book of 363 Billion.

I suppose it depends who is paying their interest from after tax net income and who is paying from gross income and deducting the interest expense

from their taxable income. 92 billion of the total loan book is to investors.

Yes.

Yes ! ... unless I'm wrong , in which case : No !

Hmmm, sounds like conditions are just right for the property market to take off. To infinity and beyond.🚀

Even with the best cant-lose, previous results, some things don't go according to plan.

"Lightyear CRASHES and burns, Disney set to LOSE over $100m!"

You remind me of my mum, constantly looking for the problems and the bad everywhere, and unable and unwilling to see anything good in life.

I'll settle for my money back (property investments in Wellington, bought well before the madness), and a realistic chance my children can have a job that keeps our grandkids close to us.

Under this government... fat chance!

This shouldn't come as surprise to anyone. It certainly comes as no surprise to me.

This is exactly what happens when central banks hold interest rates too high, for too long.

Will it get better?

I'd suggest people ask the RBNZ that question and why the OCR remains restrictive and contractionary.

In 1985, following the Plaza Accord, the Bank of Japan (BOJ) began cutting interest rates aggressively. The OCR was reduced from 5% in January 1986 to as low as 1% by 1989 to stimulate economic growth and managing the appreciation of the yen, which had surged against USD. The drastic reduction in interest rates led to an environment ripe for speculation. Investors, buoyed by low borrowing costs, engaged in rampant purchasing of real estate and stocks. By 1991, commercial land prices had soared by over 300% compared to 1985 levels.

But the Japanese h'hold wasn't as stoopid. Historically, Japan has always maintained a high savings rate, peaking at 23.4% in late 1994. The average personal savings rate has been comparatively healthy. From 1994 to 2024 has been approximately 3.88%. Now, with Aotearoa, while positive savings levels suggest some resilience among households, our declining savings ratio raises concerns about long-term financial stability and economic sustainability.

It is what it is.

In the light of so many people on here saying that New Zealanders should invest more in shares and less in Real Estate, it's interesting to read a stat like this:

"the value of owner-occupied property decreased $21 billion or 1.8% this quarter, and equity and investment fund shares decreased $27 billion or 2.6%."

It's no mystery : Shares are part ownership in businesses , the engine rooms that drive our economy , the places of progress and innovation ...

...whereas real estate , houses , are those places where we drink Tui , cook beans , scratch our armpits , take a dump , and sleep off the Tui ...

Next time I have to make a speech to the grey-rinsed conservatives ... I'm going to get you to write my speech !!!

It is both more insightful, and more caustic, that I could ever be. Friggin' awesome.

Whatever the base number for those stats is, the problem is it is too high. We should never have allowed ourselves to mortgage our economy to residential property speculation the way we have. Perhaps a further revaluation of existing property assets down by another $50 billion might start to sober us up. And perhaps one of the reasons we got here is:

" NZ major banks have a risk weighting of 28% for mortgages and a capital ratio of 10% which means they hold $2.80 of capital for every $100 of mortgage exposure"

https://www.nzba.org.nz/wp-content/uploads/2019/05/Appendix-Two-Interna…

Tony Alexander says people have more money.

A net 39% of mortgage brokers say they are seeing more first-home buyers in the market and a net 47% are seeing more investors.

Get ready for the turn-around in property prices.

Nice one Wingman, however Tony also said this;

"It is also worth noting that although more people are looking to buy, 48% of agents still say that these buyers are concerned about their employment. At the start of this year only 14% of agents said buyers had income worries"

It helps greatly to have surety of income before having the confidence to sign on the dotted line. The employment situation is still deteriorating.

Nice one Wingman, however Tony also said this;

LOL. His "panel" is effectively a database of REAs. Anyone who understands representative research will take the findings with a grain of salt.

I am surprised you think like this. If house prices stabilised for a while and interest rates dropped more maybe your daughter could afford to buy a property in Auckland.

wingman: "Get ready for the turn-around in property prices. "

Maybe, get ready for the RBNZ to ratchet up LVRs and DTIs !!!

No. ... Wait ....

Anyone quoting terrible Tones the Comb........well, really, might as well interview your keyboard.

The Comb has had to go into a safehouse, such was the rotten eggs sent his way, by his once thronging adherents..........now destitute land agents and landlords.

The guy is a walking disaster!

- Those quoting him, look like silly wombles.

'Kiwi households income drops and spending increases' = House prices to the Moon?

Meanwhile household net disposable income decreased 0.9% to $59.2 billion.

Total household income decreased 0.2%, which as mentioned above was the first fall since the start of this data series.

Everyone just think about that for a second. Government deficit spending needs to be increased to get us through the tough times, instead National/Act are slashing and burning. Except on roads we don't really need...

I can't bear it. Look, it's really simple...

Banks lent out (created) about $14bn more in the year to June 2024 than they received in repayments.

Govt deficit spent about $13bn into the economy.

Our current account deficit was about $28bn.

So, $27bn into the economy and $28bn out = a reduction in incomes / savings. Whatever.

What's especially frustrating here is that Govt think they can actually reduce that $13bn deficit spend this year. They are about to find out that they are not in charge. The rules of accounting are like physics. The economic rules they are using are like voodoo.

Great analysis & comment. As always.

... Now for my caustic spin (which makes me uncivil, apparently)

"What's especially frustrating here is that Govt think they can actually reduce that $13bn deficit spend this year."

Could it be the fault of voters that fell for this Govt's spin? I mean, we were all told it was a smoke and mirrors job, i.e. the to-be Govt's numbers didn't stack up, nor could they ever. But all they heard was "tax cuts".

YES....

It seems NZ inc has lost a lot of IP lately

Was obvious one these clowns were voted in what the outcome would be...however I am surprised at the speed they have manged to get to these numbers.

I regret to inform you that the people advising govt and the ministers in govt all believe in wreckonomics. They genuinely believe that shock therapy, sharing the state, blah will lead to the private sector thriving and floating all boats. They are stark raving mad.

PM selling his third property in as many months (and they are all mortgage free) ... hmmmm surely he catches the wind before most others ..

https://www.stuff.co.nz/politics/350448224/christopher-luxon-puts-anoth…

Maybe he's got another project in mind. He's a smart guy, used to be my boss.

He'll be well aware that selling properties right now will be drawing the attention of the doom merchants.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.