There's one thing better than a bold decision. And that's a bold decision that appears vindicated.

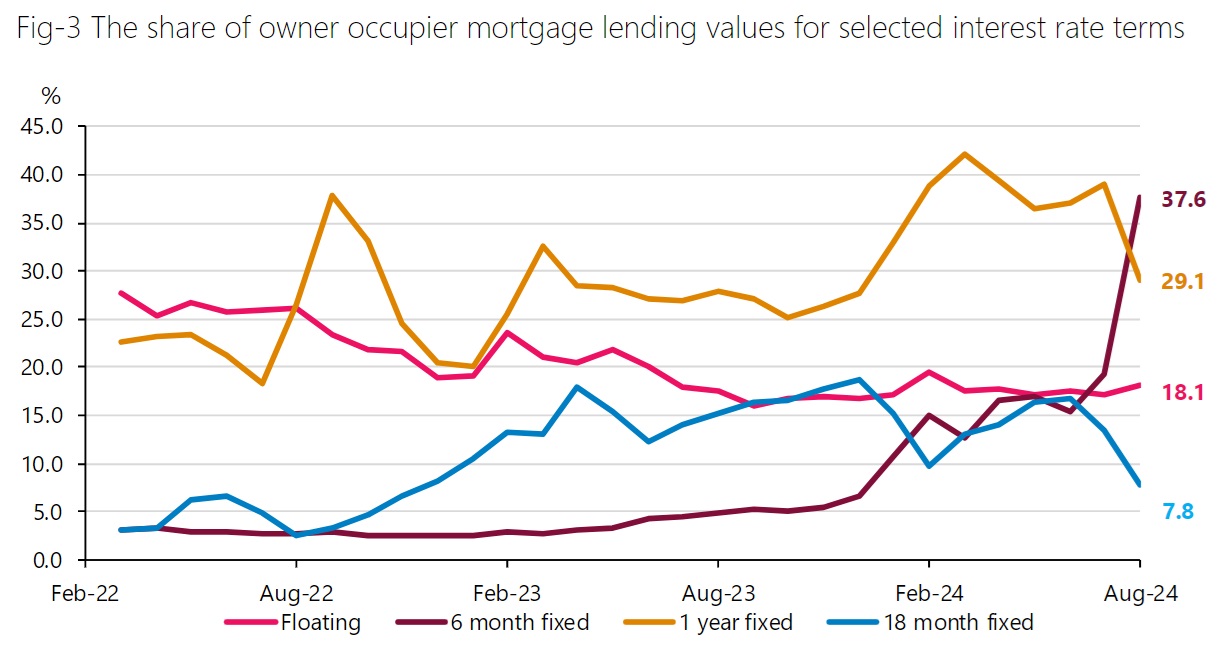

Contrary to my expectations when reviewing July mortgage figures, the move to ever shorter fixed terms for mortgages not only continued in August but soared, explosively, to new heights - to the point where the perennially popular one-year fixed mortgages were overtaken with six month fixed mortgages becoming most popular for the first time.

The Reserve Bank, in its latest monthly figures says that 37.6% of new mortgages taken up by owner occupiers during August were for a six month term.

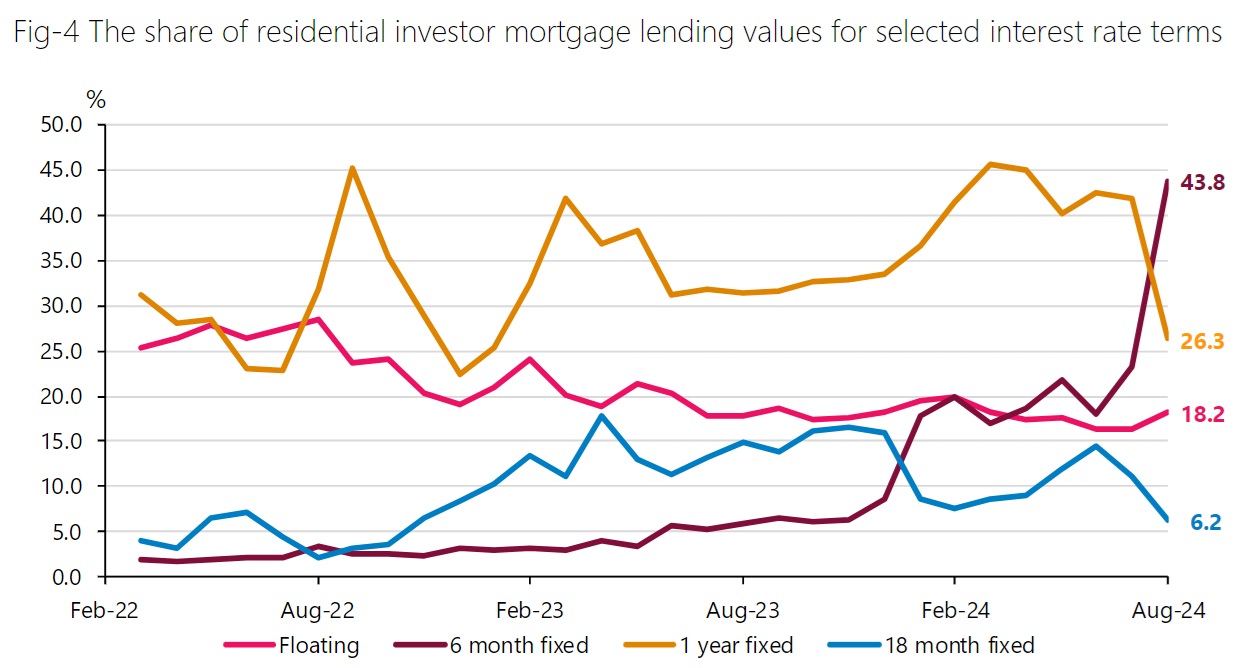

The investors have been even bolder than that. Some 43.8% of investor new mortgage money during August was for six months.

And yes, these figures are very much records for this data series - notwithstanding that the series dates back only to 2021. But clearly, it would be a very long time since people went this 'short' with their mortgages - and I would be reasonably happy to say they probably never have gone quite this short in terms of actual fixed rates. There was, however, a period in 2011-13 when far more money was actually on floating rates rather than fixed.

The significant thing about this data series is that unlike other monthly RBNZ series capturing mortgage information, this one records mortgage details as per when the mortgage is physically drawn down as opposed to when it is committed to.

So, for people to be drawing down mortgages in August on a six month term, there has to have been some good anticipation on the part of at least some on what the Reserve Bank was going to do. On August 14 the RBNZ dropped the Official Cash Rate from the 5.5% it had been on since May 2023 to 5.25%.

Mind you, people would have been helped in their anticipation by the fact that mortgage rates themselves were already heading down before that first OCR cut. But anyway, with at least 25 basis points more of cuts to the OCR expected this week, and more to come before the end of the year, anybody who took the six month option in August and who will therefore now be looking at refixing their mortgage in around February, is probably feeling justified.

In terms of the total sum of money that was drawn down in mortgages during August, it was $6.841 billion. Of that, $1.27 billion was on floating rates, while the investors and the owner-occupiers together took out $2.639 billion worth of six-month fixed rate mortgages. Add the floating and six month totals together and it means that some 57% of the new mortgage money drawn down can be reset by February. That's a big percentage.

To put some historical perspective on these figures, just a year ago in August 2023 the owner occupiers took out only $208 million of six month mortgages, which made up a mere 4.8% of the $4.347 billion of owner-occupier mortgage money.

The $75 million of six-month mortgages taken up by investors in August 2023 made up just 5.9% of the investor total of $1.266 billion then.

And yes, a swing to popularity for one thing, means a swing away from others. In August 2023 owner occupiers and investors together took out $1.206 billion of mortgages fixed for two years, which was over a fifth of the $5.699 total in that month.

A year on, in August 2024, a paltry $230 million worth of mortgage money was taken up for two-year terms. That's just 3.4% of the $6.841 billion total. And yes, that's a record low.

But as we've seen these things are obviously cyclical. I say again that I've been impressed by the keen way the country's mortgage customers have keenly tracked what's likely to happen with official interest rates. And they've got themselves, it seems, ahead of the game.

I reckon that refixing decision in February might be a bit harder though.

38 Comments

people can smell lower rates

The OCR I'd now a national sport. It has been politicized so heavily, it is literally everywhere with the media.

It is clear as day now with Federal Reserve going first that we will follow, so it's hardly a risky 'bet'.

Lo and behold Orr & Co will probably throw in a big surprise just for the hell of it.

The OCR I'd now a national sport. It has been politicized so heavily, it is literally everywhere with the media.

Everyone's now a student of central banking and money supply. Credit to the Ponzi for this.

Competition for entry-level jobs under Grand Wizard Orr will be fierce.

On a macro scale, this is a positive. The more people are attuned to how monetary policy works, are able to think more critically than "OCR dropping = magical paper wealth", and understands the various factors involved in the national, and global economy, then the more educated the voter.

If the system really wants to educate voters, the ballot boxes could have the policies stated under each political party of what they stand for, and what they intend on accomplishing. This means voters can align with the best political party that best suits their ideals, viewpoints and outlook. Unfortunately this is not the case, as the system is designed to take advantage of people by turning voting into a popularity contest - best publicity and media pay off wins. We need to change how we vote so that it becomes more widely known the effectiveness & ideals of each political party, rather than voting for who seems popular. Popularity is no guarantee of effectiveness at all. We don't need nice politicians with cheesy slogans and false promises, we need action, if that takes someone unpopular to do so, then so be it.

How has the OCR “been politicized so heavily”? Maybe you are confusing “popularized by the media” with “political”? they aren't the same thing.

The all blacks haven’t been politicized, but everyone has an opinion on them for example. Ditto Interest rates / the OCR.

Regardless of how good a job one thinks the Reserve Bank has been doing, the reserve bank has by all appearances been politically neutral in its inflation fight.

How has the OCR “been politicized so heavily”?

One example of 'poltitcized' actions of central banks in the Aotearoa context is the appropriation of Maori deities into a completely artificial construct that is alien to traditional Maori culture and spirituality. You could argue that at its core is another form of colonialization.

I think it's blindingly obvious to go short at the moment. The trick now will be knowing when to move back into the longer fixes. Doesn't everyone wish they had locked in for 5 years at 3%?

Pretty much nobody went for a 5 year fixed because the RBNZ was shouting about rates going negative at the time. Would have been more than 3% as well, got my partner on the 3 year at 3.29% from memory, the 5 year would have been more. She is now on a 6 month fix, comes out in Feb next year.

If i ever see even a 3.99 fixed for 5 years i am taking it - I still admire the people who 2.99 it for 5 years very very good forward vision

I vividly recall an argument with a colleague over taking the 2.99 5 year. He was of the opinion he wanted it as a new FHB with plans for a kid. I was talking him out of it. At the time we'd heard that some other ANZ customers who could haggle well were getting 2.19% for the 1 year, us mere mortals were getting 2.35 and complaining about it.

Paying a 0.7% premium for the long term just didn't make sense to me. But at least it got me thinking about the hypothetical of increasing rates. That prepared me well for when they did, and I grabbed every 2-3 year fix in the 3s I could get my hands on.

My 5 year fix at 2.99% ends in November of 2025. I remember listening at the time to the Saturday pm real estate shows and being absolutely baffled that the Mortgage industry "talking heads"--Ashley Church being one where not shouting from the hilltops at what an exceptional gift the banks were offering. My thinking was Interest rates couldn't go any lower as banks needs at least two hundred basis points above their costs, and to bank that rate for a long term you just couldn't go wrong But no professional was out there pitching that 5 year fix of 2.99%. I even broke a 4.39% and paid a few hundred in break fees to jump on it.

I broke loans at 2.69% and 2.49% to put everything on 3.19% in May 2021, cost me nothing but $100 in admin fees all up. I would have everything at 2.99% but ASB moved first and I was too slow with the emails by a matter of hours because I wasn't paying attention that day. I'd already decided that it was a once in a many-year opportunity and even if I was wrong then it was still a cracker deal.

Being on that rate has enabled us to invest a significant amount in our fledgling business over the past 3 years.

We started our house hunt in about May 2021. By the time we found the perfect place, sold our first home and had our offer accepted it was November/December and the 5 year rate was 4.95%. Was crazy how quickly rates rose over those 6 months, was a little annoying but thankful our rate doesn't start with a 6.

"Pretty much nobody went for a 5 year fixed because the RBNZ was shouting about rates going negative at the time"

That is kind of my point. Every man and his dog expects rates to drop and keep dropping at the moment. At some point the 6 month term won't be the best deal though. Hindsight is 20/20

I fix at end of this month.

Assuming Oct change works in lockstep and 1 year rate is still 50 basis points lower than 6 months then I'd need at least 100 basis points from November and Feb decisions to make 2x6 months come out even.

If they go 50 now then I am definitely going 1 year.

Pleased some are doing the maths. It's not as cut and dried as it looks, ay!

Financial sense is the best way to ensure you always are achieving your goals, and planning longer into the future than many. Keep it up!

Remember interest rates don’t follow interest rate cuts on a 1:1 basis. Big chunk is driven by wholesale funding rates which are based on global interest rates and future expectations, as well as local funding rates (more influenced by OCR) but also future expectations priced in of local funding rates

If J.C. and other pundits are correct we won't be seeing anything like as much of Japan's mum & dad's savings banked into the global pool.

Assuming Oct change works in lockstep and 1 year rate is still 50 basis points lower than 6 months then I'd need at least 100 basis points from November and Feb decisions to make 2x6 months come out even.

Nov24 - 50

Feb24 - 50

Now you're even.

Apr25 - ?

May25 - ?

July25 - ?

August25 - ?

October25 - ?

6 months looks like a good bet to me.

So glad I fixed for 5 years at 2.99%.

Several M all rolling off Mar 2026.

Was pure greed that stopped people from fixing at the lowest rates ever....

For every winner like this, there's a tale of someone who fixed 5 years in 2018 and never benefited from sub-5% rates at all, then was dumped into having no choices sub-6 at refix.

Not nesasarily. If you require to break that fixed term, ie to re finance to make things work then break fees would be in the 10s of thousands. If one had more than 1 property, and went to sell one, depending on how the loans are structured, most cross collaterize their properties and this could trigger a refinance occuring break fees. Equally so those requiring to use their existing equity position to purchase another property will also go through some sort of re finance, which again will cause break fees.

The longer terms work out better for those who are happy with their financial position, but certainly isn't for everyone.

Break fees on a 2.99% mortgage would be the $100 admin fee, and they'd probably waive it and say "thanks so much".

"most cross collaterize their properties and this could trigger a refinance occuring break fees" ... Not "most". Only those signed by absolute fools.

"Only those signed by absolute fools."

Why do you say that?

That only applies when rates have dropped below the rate you are trying to break

Most of us would go shorter still, if there wasn't such a premium on floating rates.

Do you think we could make a public market for 10yr rates?

Banks have offered longer terms in the past, but kiwis didn’t take the up. Our rules are quite different and punitive compared to the US or Europe (or so I’ve been told) when it comes to changing/breaking longer terms

"I say again that I've been impressed by the keen way the country's mortgage customers have keenly tracked what's likely to happen with official interest rates. And they've got themselves, it seems, ahead of the game."

Or the consistent message from the consulted mortgage brokers

Interesting UK comparison of how much interest the different generations had to pay.

Noticed some of the comments too. As usual, statistics are met with trauma competition from some of the older commentators.

Comments like "What rubbish, we had 15% none of the younger generations had to pay that!!" and "Our wages were a lot lower back then, they must've gone up 15x since the 80's" or "The data is cherry picked!!".

And people wonder why certain generations are so despised.

Bought our house 2 years ago. Mortgage is coming up for refixing this month. 3yr is 5.59%. If OCR gets cut by 100 bps between now and Feb that goes down to 4.59% (maybe, or maybe the OCR cuts are already priced in?). The difference comes out to ~13 hours work after taxes per year. Honestly that's not a make-or-brake sum for us. I'm not sure it's worth it to get worked up about and try to time the market and try to be all clever about it.

That people pay such attention to this tells me people have taken on wayyy to much debt and it would be healthy to de-leverage.

EDIT: clarified hours per year

I got offered 5.59 for 1yr today.

If a 1% change in interest rate is 13 hours work, you are very well paid or have a small mortgage. 1% of 500k is 5k about $385 for each of the 13 hours.

Small mortgage. As I wrote, a lot of people appear to be way too in debt.

5.59 for 1 year today. Anyone taking that?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.