The Government has decided to exempt fintech buy now pay later (BNPL) service providers from default fee provisions in the Credit Contracts and Consumer Finance Act (CCCFA).

This comes within Commerce and Consumer Affairs Minister Andrew Bayly's latest round of financial services reforms. The exemption has no conditions attached, according to a Cabinet Minute dated August 28 and released on Thursday.

Bayly told Cabinet he'd heard concerns from BNPL providers that complying with the CCCFA’s default fee provisions would constrain how they calculate and charge customers default fees to an extent that could put their businesses in jeopardy.

"The CCCFA’s default fee provisions limit default fees to reasonable amounts directly related to the costs incurred by the provider due to the default. These provisions were designed for traditional credit products that can recover other costs through interest charges," he said.

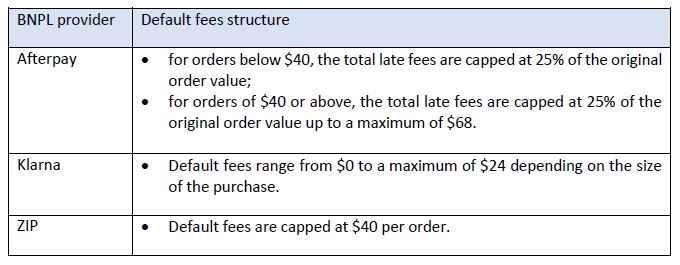

In a Regulatory Impact Statement the Ministry of Business, Innovation and Employment (MBIE) noted there are just three BNPL fintech companies left operating in New Zealand. They are Afterpay, Klarna and Zip.

No conditions

Bayly advocated the exemption be conditional on compliance with a "reasonable cross-subsidisation" of total credit losses through default fees, as recommended by MBIE. MBIE said such conditions would prevent BNPL providers from "over-recovering total credit costs and losses incurred by defaulting borrowers through default fees."

However, Cabinet decided for an exemption with no conditions, as advocated by Regulation Minister David Seymour.

"This approach would provide BNPL lenders with more flexibility in setting their default fees, but would not provide adequate protection for consumers. Furthermore, the regulator would be unable to take action if concerns about excessive fees arose without returning to Cabinet to seek necessary changes to the fee provisions, and any changes would not apply retrospectively," Bayly said in a Cabinet paper.

Placing conditions on the exemption had been aimed at putting in place "bespoke protections against excessive default fees and future-proofing against potential unreasonable fee increases by BNPL providers," Bayly said.

The previous Labour government moved to bring BNPL under the CCCFA last year with regulations taking effect from September 2, or Monday of this week. However, Labour's Commerce and Consumer Affairs Minister Duncan Webb decided to exempt BNPL loans from affordability and suitability assessments saying these would be "too onerous for these short term, low value, interest-free loans."

Instead, Webb decided BNPL lenders would be required to complete comprehensive credit reporting when customers sign up or increase their credit limit. Now, the Coalition Government is exempting them from the CCCFA default fee provisions.

A BNPL transaction typically involves three agents; a merchant, a customer, and a BNPL platform. BNPL payment schemes allow consumers to divide their spending into interest-free instalments, with the cost of the platform-based BNPL service primarily falling on merchants. That means consumers can manage their expenses while incurring only small or no fees. However, there are penalty fees for late payments. And imprudent spending or a poor understanding of BNPL terms can lead to significant indebtedness.

'They might all exit the market'

MBIE said to the extent BNPL providers charge borrowers for other costs through their default fees, the adjustment required would've been to increase the merchant service fees BNPL providers charge, to make up for the losses incurred by lower default fees. These merchant fees are already significantly higher than those charged by banks.

"As the BNPL business model is different from more traditional lenders, this Regulatory Impact Statement questions whether the CCCFA fee provisions should apply to this credit product in the same way they apply to consumer credit lenders, as these provisions were originally drafted for credit products charging interest, as well as fees," MBIE said.

"The unintended impacts of the application of the CCCFA default fees provisions could reduce access for consumers to BNPL."

"If BNPL business models are no longer viable under the CCCFA fee provisions, they might all exit the market. This would either restrict access to short-term and small-amount loans to New Zealanders or make these loans more expensive, where the borrower moves to an interest charging product, e.g. credit card, short-term personal loan."

MBIE noted its conditional recommendation to exempt BNPL from the CCCFA default fee provisions would've gone against the Supreme Court's 2016 Sportzone Motorcycles v Commerce Commission judgment stating; “there is no compelling reason why temporary defaulters should pay costs attributable to other debtors who default permanently. Temporary defaulters, who can be charged fees covering the cost of their own defaults, have no greater responsibility to pay for the costs involved with permanent defaulters than any other debtors."

That judgement, however, wasn't made in the context of BNPL products specifically, and the provisions were not in force for BNPL providers at that time.

"There are currently no prior or active cases looking at default fees charged by BNPL providers," MBIE said.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

5 Comments

The restrictions should put the BNPLs in jeopardy. The model is predatory on those who are desperate and unable to pay.

No surprises where the exemption came from.

Actually the whole setup is predatory on consumers with merchants upping the price for everyone to cover BNPL. You don't find advertising stating 5% off if not using BNPL do you.

Only three companies left in the market.

Zero would be a good number, they do absolutely nothing for the economy

Nothing says "our economy is a debt-ridden house of cards that could collapse at any moment should a credit restriction hit" like a government giving loan sharks an easy ride.

This is a disgrace. Is the Govt going to reduce compliance costs for all other “failing” businesses too? Either the rules/ fees have a genuine purpose or they don’t across all of the affected businesses. So Bayly, MBIE and Seymour are easily pressured. Sigh, running out of parties to vote for.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.