By Sheryl Sutherland*

Assuming that you have read this and tackled your savings, here is a brief refresher on considering saving vs. investment.

1. Saving

Saving has many benefits such as providing a financial safety net for unexpected events, liquidity for purchases and other short-term goals, and being safe from loss. However, there are also some drawbacks to consider, such as missing out on potential higher returns from riskier investments. Savings can also lose purchasing power caused by periods of rising inflation.

While saving is a crucial part of any financial plan, it's essential to combine it with other forms of investing, such as retirement accounts or investing in the stock market, to achieve a balanced approach to financial planning.

Saving Pros:

• Builds up an emergency fund

• Funds short-term goals like buying groceries, a new phone, or going on a holiday.

• Minimal risk of loss, and something that may improve with the arrival of the Deposit Compensation Scheme in mod-2025

Saving Cons:

• Much lower yields

• May lose out to inflation

• Opportunity costs when not invested in riskier but higher yielding assets

Savings are an excellent vehicle to meet short-term goals and prepare for unexpected situations. They should be low risk, which means that your money is ‘safe’ but the returns are also low. Short term is generally up to five years.

2. Investing

Investing has the potential for higher returns than savings accounts, the ability to grow your wealth over time through compounding and reinvestment, and the opportunity to help you achieve long-term financial goals, such as saving for retirement or buying a house.

However, there are also some cons that should be considered. Investing always involves some level of risk, and there is no guarantee that you will make money or even get back what you've invested. Diversification across several holdings can help. It's important to do your research and understand the potential risks associated with different types of investments. Investing requires discipline and a long-term perspective, which can be difficult for some people to maintain in the face of market volatility or the temptation to follow the crowd in an attempt to make quick profits.

Investing Pros:

• Potential for higher returns than savings

• Can help achieve long-term financial goals

• Diversification can reduce risk

Investing Cons:

• Risk of loss, especially in the short term

• Requires discipline and commitment

• May require longer time horizons

Why do some people fail at investing?

There are several reasons why people may struggle with investing. One common reason is a lack of knowledge or experience, which can lead to poor investment decisions. Additionally, emotional biases, such as fear or greed, can cause investors to make impulsive or irrational decisions that may result in losses.

Successful investing requires a long-term perspective, discipline, and patience - and it can be difficult to stay the course during periods of market volatility.

The bottom line is that both saving and investing are important components of a healthy financial plan. Saving provides a safety net and a way to achieve short-term goals, while investing has the potential for higher long-term returns and can help achieve long-term financial goals. However, investing also comes with the risk of losing money. Each approach has its own pros and cons, and it's important to find the right balance that works for your financial situation and goals.

Ultimately, a well-rounded approach that includes both saving and investing can help build wealth, protect against financial shocks, and provide a solid foundation for a more secure financial future.

Becoming an investor

If you are considering investing, one of the first steps that people take is that of completing a personal risk profile.

This will ‘tell’ you where you invest, or necessarily, even address your attitude to risk. Knowledge on the balance between risk and reward is something that is usually acquired over a long term. A 15-minute exercise like the one below will however, give you some points for consideration.

Try to answer the following, giving yourself points from one to five according to the statement that best reflects you, then add these points together for a total that will tell you which group you belong to (Source: Select Wealth).

1. The value of your investment may move up and down regularly. Suppose you had $100,000. If after three months the markets had not performed well and your investment dropped in value, which of the following most closely aligns with how you would feel?

| I would not be comfortable with any loss | 1 |

| I would be comfortable with a loss of up to $5,000 (5%) on my $100,000 investment | 2 |

| I would be comfortable with a loss of up to $10,000 (10%) on my $100,000 investment | 3 |

| I would be comfortable with a loss of up to $15000 (15%) on my $100,000 investment | 4 |

| I would be comfortable with a loss of up to $20000 (20%) on my $100,000 investment | 5 |

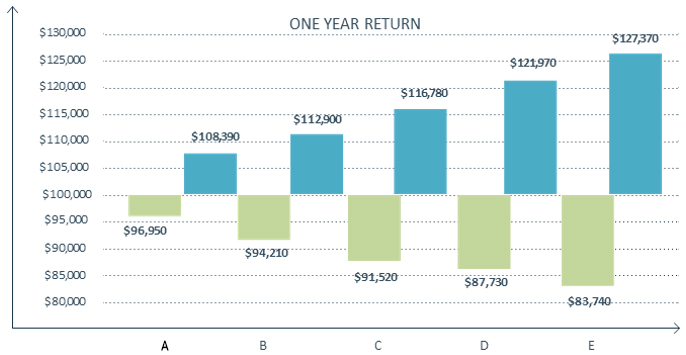

2. Suppose you had $100,000 invested. The following graph shows the returns of five hypothetical portfolios over a one-year period. The higher values show the potential maximum return, while the lower values show the potential minimum return each portfolio# could experience (note the portfolio with the best potential maximum return also has the largest potential minimum return).

Which of these portfolios would you feel most comfortable being invested in?

| Portfolio A | 1 |

| Portfolio B | 2 |

| Portfolio C | 3 |

| Portfolio D | 4 |

| Portfolio E | 5 |

3. Investing involves taking some risk. The level of risk will vary depending on the portfolio your funds are invested in. If you are seeking higher returns, you need to be willing to accept more risk (i.e. chance of loss). If you are seeking lower risk, you need to be willing to accept lower returns. How do you feel about taking risk over the long term?

| I am willing to accept lower returns to limit my chance of loss | 1 |

| I am willing to accept some risk and chance of loss to achieve higher returns, but prefer investments with low risk and return | 2 |

| I am willing to accept moderate risk to achieve higher returns. Minimising risk and maximising return are equally important | 3 |

| I am willing to accept high risk to achieve high returns | 4 |

| I want to maximise my returns. I am not concerned with risk or seeing my investment balance fall. I accept there will be significant fluctuations in my investment balance. | 5 |

4. Inflation is the term used to describe a rise of average prices through the economy. In NZ, the Reserve Bank’s target is to maintain an inflation rate between 1% to 3%, which means that on average, the value of goods and services increase between 1% and 3% each year. For example, $100,000 in 2006 is worth approximately $122,000 in today’s money when adjusted for inflation*. If your investment is not returning at least the same rate of inflation, the ‘real value’ of your money has reduced. What is your outlook towards your portfolio returns in relation to inflation?

| I do not want to see my portfolio returns fall at any time | 1 |

| I would be comfortable with my portfolio returns being about the same as the rate of inflation | 2 |

| I would be comfortable with my portfolio returns being marginally above the rate of inflation | 3 |

| I would be comfortable with my portfolio returns being well above the rate of inflation | 4 |

| I would be comfortable with my portfolio returns being significantly higher than the rate of inflation | 5 |

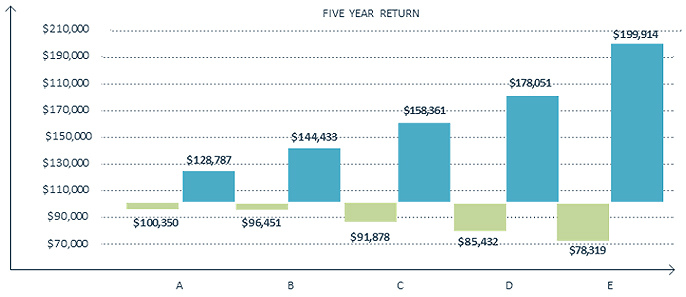

5. Suppose you had $100,000 invested. The following graph shows the returns of five hypothetical portfolios over a five-year period. The higher values show the potential maximum return, while the lower values show the potential minimum return each portfolio could experience (note the portfolio with the best potential maximum return also has the largest potential minimum return).

Which of these portfolios would you prefer to be invested in?

| Portfolio A | 1 |

| Portfolio B | 2 |

| Portfolio C | 3 |

| Portfolio D | 4 |

| Portfolio E | 5 |

RESULTS

Add up your score to see which group you fall into.

| 5 - 7 | Conservative Investor |

| 8 - 12 | Conservative balanced income |

| 13 - 18 | Balanced Investor |

| 18 - 21 | Growth Investor |

| 21 - 25 | High Growth Investor |

The next step is to figure out which proportion of assets you want to utilise; shares, bonds, cash and property.

*Sheryl Sutherland is director of The Financial Strategies Group, and author of Girls Just Want to Have Fund$ – Every Women’s Guide to Financial Independence, Money, Money, Money Ain’t it Funny – How to Wire your Brain for Wealth, and co-author of Smart Money – How to structure your New Zealand business or investments and pay less tax. You can contact her here.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.