There are more carded home loan rate reductions over the past 24 hours, the latest being from ASB.

Recent cuts by Kiwibank, by ICBC, and by SBS Bank are also notable as well. Yes, it is a challenge to keep up.

The extension of the flurry of rate cuts are changing the relative positioning of all bank rate offers.

At each fixed term, these show who has the lowest offer, and how your current bank compares.

It also helps you assess the rate benefits you give up for going shorter.

ASB is back with dips to take them again lower than their main rivals.

Main-bank competition remains fierce with no-one prepared to give an inch.

Very oddly, this has left Heartland Bank in an uncomfortable position. For years their online offers were the market-leading benchmark. Now they are far from that, although in this vortex of rapid rate cuts, they may restore that with cuts of their own. We'll see - we don't have any inside information on what they are about to do, if anything.

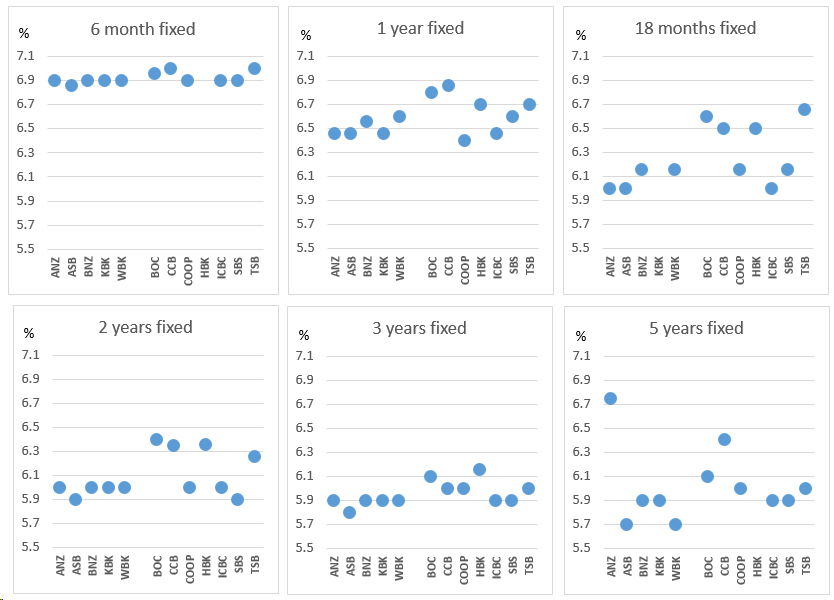

Now, the lowest carded rates for each fixed term are:

6 months = ASB at 6.85%

1 year = Cooperative Bank at 6.39%

18 months = ANZ, ASB, and ICBC at 5.99%

2 years = ASB and SBS Bank at 5.89%

3 years = ASB at 5.79%

4 years = ASB and Westpac at 5.79%

5 years = ASB and Westpac at 5.69%

It is probably worth noting that missing from this list is Kiwibank, the institution ComCom singled out to be the disrupter, and today their CEO said they were up for that role.

Almost all banks will have some flexibility in their rate offers. So the carded rates are just the start. Negotiate. How flexible they may be will depend on the strength of your financials. And don't forget, banks have savvy tools at hand to 'know' the likely valuation of your property, so if the loan-to-value ratio (LVR) is near 80% you may not find them very accommodating for a lower rate. With falling house prices, the point where low equity premiums start applying is shifting around as well. See this.

And the carded rates we report here can be different to the rates banks might offer in their banking app. We would like readers to reveal what their banking app shows as the potential offer rates. Please add that market intelligence in the comment section below.

A quick check of the wholesale swap rate chart below gives a clear understanding of where funding costs are heading.

One useful way to make sense of the changed home loan rates is to use our full-function mortgage calculator which is below. Term deposit rates can be assessed using this calculator.

And if you already have a fixed term mortgage that is not up for renewal at this time, our break fee calculator may help you assess your options. Break fees will be minimal in a rising market. But they become important in a falling market, like now. Don't forget, when you sign up for a fixed rate you are signing a contract. You have been given the right to break it in legislation but the bank has the right to reclaim its costs when you do so. This is NOT evidence of banks making it hard to switch (as some borrowers, and sadly some journalists seem to think).

Here is the updated snapshot of the lowest advertised fixed-term mortgage rates on offer from the key retail banks at the moment.

| Fixed, below 80% LVR | 6 mths | 1 yr | 18 mth | 2 yrs | 3 yrs | 4 yrs | 5 yrs |

| as at August 22, 2024 | % | % | % | % | % | % | % |

| ANZ | 6.89 | 6.45 | 5.99 | 5.99 | 5.89 | 6.74 | 6.74 |

| 6.85 -0.04 |

6.45 -0.14 |

5.99 -0.16 |

5.89 -0.10 |

5.79 -0.10 |

5.79 -0.10 |

5.69 -0.00 |

|

| 6.89 | 6.55 | 6.15 | 5.99 | 5.89 | 5.89 | 5.89 | |

| 6.89 -0.16 |

6.45 -0.30 |

5.99 -0.35 |

5.89 -0.20 |

5.89 -0.20 |

5.89 -0.20 |

||

| 6.89 | 6.59 | 6.15 | 5.99 | 5.89 | 5.79 | 5.69 | |

| Bank of China | 6.95 | 6.79 | 6.59 | 6.39 | 6.09 | 6.09 | 6.09 |

| China Construction Bank | 6.99 | 6.85 | 6.49 | 6.34 | 5.99 | 6.40 | 6.40 |

| Co-operative Bank | 6.89 | 6.39 | 6.19 | 5.99 | 5.99 | 5.99 | 5.99 |

| Heartland Bank | 6.69 | 6.49 | 6.35 | 6.15 | |||

| ICBC | 6.89 -0.16 |

6.45 -0.40 |

5.99 -0.66 |

5.99 -0.50 |

5.89 -0.50 |

5.89 -0.40 |

5.89 -0.40 |

| |

6.89 -0.10 |

6.59 -0.26 |

6.15 -0.34 |

5.89 -0.10 |

5.89 -0.10 |

5.89 -0.10 |

5.89 -0.10 |

| |

6.99 | 6.69 | 6.65 | 6.25 | 5.99 | 5.99 | 5.99 |

Fixed mortgage rates

Select chart tabs

Daily swap rates

Select chart tabs

Comprehensive Mortgage Calculator

41 Comments

Drops in anything beyond 1 year are kinda pointless now. The 6m and 1y still remain in mid to high 6s.

The question is how much further are banks willing to erode their margins to attract borrowers.

Drops in anything beyond 1 year are kinda pointless now. The 6m and 1y still remain in mid to high 6s.

I wonder how the maths works

If you take the cheaper longer term rates

And pay them back as if you were paying the highest short term rate.

I would probably take the 6 month rate, though the 18 month rate looks tempting.

Yeah but you can see what I'm getting at.

Instead of thinking you'll save a buck more on interest in another 12 months or so when your rates up - therefore paying a higher interest rate and overall repayment today.

Why not make the same higher payment, but at a lower, longer term fixed interest rate.

I'd have thought you'd then be paying principal back faster from day 1, lowering your exposure to interest over time.

But I'm no mathemagician

You don't need to be a mathematician. This calculator does all the heavy lifting for you.

https://www.interest.co.nz/calculators/full-function-mortgage-calculator

Have an excel spreadsheet to do just that. The 18 month fix looks best with the model. It all comes down to how you predict the future trajectory.

Risk ON, banks are willing to play

No article on BNZ getting rid of the low equity interest rate penalties?

maybe not a massive thing, but one little thing that might make it a little bit easier for FHBs to buy

I'd almost put money on LVR or DVI thresholds being modified in the coming year or two.

Right now they are almost pointless and can only prevent a 2021 type scenario

Right now they are almost pointless and can only prevent a 2021 type scenario

That's the only reason they were introduced

Disagree. The RBNZ wants to keep debt rolling, and that's deemed safer if they keep constraining lending.

LVRs

DVIs

Ensures your pool of marginal lenders decreases, limits the risk of defaults, makes your debt market look safer.

It will not automatically prevent house price inflation.

They were not introduced to limit house price inflation, as far as I'm aware.

only to reduce risky lending and prevent defaults?

Mostly. It wasn't because of 2021 anyway, they've had it on the cards for a while.

None of these measures actually addresses affordability though.

"None of these measures actually addresses affordability though."

Could you explain why you think that?

Because you're only really trimming the extremities of your lenders.

If we take LVRs for instance, they were introduced in what, 2013? It meant that for a low income/entry level buyer, you may have needed to quadruple your deposit amount. Yet houses also went up a lot in the 10 years following 2013. Did housing become more affordable for those lower income/entry level buyers?

Will a DVI help those same buyers compete for a limited pool of housing against people who earn 3-4x as much? Will that stop those higher earners making the low to middle end of the market more expensive?

All it really helps, is it reduces the amount of people falling over in a time like this. They just get to slowly bleed out instead.

(What is a DVI? I've assumed you meant DTI.)

So LVRs and DTIs do rein in what is lent? They do restrict credit growth?

They put an limit on the absolute bounds of lending of the entire lending/mortgage market. But within that, we have to know (and perhaps you do)

- what is the current average DTI on a mortgage?

- what is the current net asset position of the average (or even by quartile) property purchaser?

Because I have a feeling, there is still significant available overhead before either limit is reached.

They would be great tools if everyone earned and had the same amount of money.

Modified…or removed during the “holy f**k what have we done” stage of slashing 😂

BNZ is also reducing the cash back redemption rate on their credit card from $1.34 per '200 rewards points' to $1.28 per '200 rewards points'.

They are also getting rid of the automatic cash back option that converted 'rewards points' into cash back.

They really want to push their silly loyalty scheme.

Remember folks, banks will use an array of different rates and offers to steer the average yield on ALL mortgages towards the carded 1-year rate. Current average yield is 6.25%, so the average yield on mortgages will continue to go *up* for a good few months yet. That means that things will get more contractionary for a while yet.

How did you calculate the "Actual Yield" (dashed white line)?

RBNZ publish it - https://www.rbnz.govt.nz/statistics/series/exchange-and-interest-rates/…

Thanks.

(I was hoping you'd come up with a better way.)

If one accepts the view that 'recessions follow a long period of interest rate inversion' then fixing at any period beyond 12 months would seem to be unwise.

If the USA catches a cold, who knows how low rates could be in NZ after 12 months.

Take care, folks.

And from the US today, we get:

"Even the casual observer will note that the parabolic rise in credit has outstripped the real economy (GDP).... In the modern era, gargantuan increases in credit (a.k.a. debt) pumped up asset bubbles. Absent a vast expansion of credit, it's hard to inflate a massive speculative bubble....The consensus holds that housing is bubbling higher because there are enormous scarcities in housing: demand exceeds supply, and so prices skyrocket. While this is undoubtedly true in specific locales, the nation as a whole has more housing units per capita than ever before.... The winners and losers when the housing bubble pops are clear: the younger generations win, the older generations lose, and those who counted on the phantom wealth of bubbles lasting forever will lose while those who didn't enter the speculative bubble will win."

https://www.oftwominds.com/blogaug24/housing-bubble8-24.html

A quality source of information? Or a highly dubious one from the fringe? (I now understand where you get your economic 'wisdom' from.)

These rates still hurt and don't forget the average interest rates mortgage holders is still increasing and hasn't peaked yet as fixed rates from 2,3,4 years ago roll off to higher rates

It’s the ridiculous prices we are paying for a house that is hurting.

Would be helpful if Interest.co also included floating rate changes in updates. This affects the many people with revolving credit accounts.

They having budged as far as TSB is concerned..

As today just signed new mortgage with ANZ (can't believe they would touch me) for 413k for the new purchase plus some to get subdivision and new build going at 6.85 percent locked in for 6 months. Wether a better deal in the 12 or 18 mth is not that great a deal. But the thing that really floored me apart from the lending is they also released a property as well as loaned me more money. Don't panic still only 40ish debt to equity. So that is now 3 properties with no mortgage. Life is good

This should give the property market a nudge.

Most people are still scared for theor jobs or looking to sell. I doubt there will be much of a upswing in sales til 2027

Banks are fighting over the few peeps that are actually still gambling (sorry ... buying).

The longest post WW2 recession in NZ was 2 years, it'll be over before you know it.

And those that had the gonads to buy property will be the winners.

Maybe

Let's see.

Winners?

Break even, after expenses, inflation, etc. is the most likely scenario.

That said, not losing money in property development is a win.

Everyone's a winner, except maybe the developer

- council

- suppliers

- bank

- insurance

- some of the subbies

- real estate agent

I'm in the market to buy right now. My driver is a roof over my head and land basing me and the wife after a couple of years of boat living. Surprisingly not in it for the tax free cg. Winning is retaining your breathing habit in my world.

New Zealand property is still very cheap to buy!

Yes maybe Auckland is hard to buy and survive if you are a first home buyer but then again Auckland is not that nice to live in nowadays anyway.

Currently in Europe and I can assure you that if you believe that NZ is expensive then have a look at what the prices are in Europe.

In Madrid today and a 3 bedroom apartment will set you back only 1.4 million Euro so something like$3million NZD!

I know Germany is just as expensive so stop thinking that NZ property is expensive, and we are still cheaper than Ozzie unless you are in the smallest towns over there.

If you want to continue to moan and sit on the sidelines expecting prices to drop then things will not improve for you.

The Chch market is the most stable market in NZ and gives everyone the opportunity to own and improve your financial position.

Your problem is trying to compare Christchurch to Madrid..

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.