The fast-moving interest rate landscape is changing who has the best offer (carded) rates.

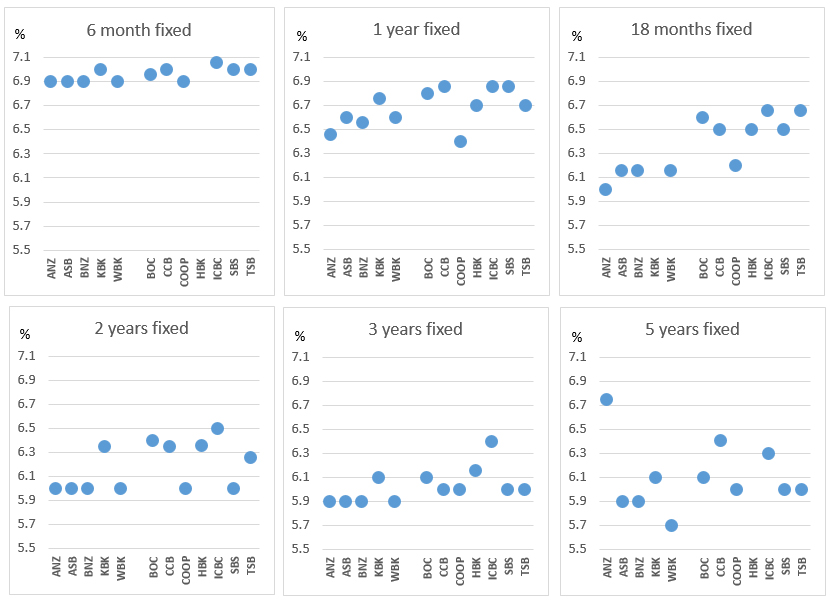

Seeing the rates in our full tables is one thing, or even in the table at the foot of this article, but it doesn't give you an easy way to get a sense of the differences between bank offers.

But a dot-plot does.

At each fixed term, these show who has the lowest offer, and how your current bank compares.

It also helps you assess the rate benefits you give up for going shorter.

Today, Monday, the largest home loan lender, ANZ, cut its fixed rates (again), just the latest in a string of reductions, led by the major banks.

ANZ's biggest cuts were to their 12 and 18 month rates, taking them down -40 basis points (bps) and -50 bps to market-leading levels.

In fact going sub-6% for 18 months makes this their lowest since October 2022.

ANZ also cut their term deposit offers, taking -40 bps off their 12 and 18 month TD rates.

As we post this, ANZ has not released all the detail of this latest change - only that they will effective August 20, (along with the rates they want to skite about.) Update: They have now. And the Cooperative Bank has also cut its rates. In fact their one year rate at 6.39% is now the market low for that term. Further update: BNZ has matched their main rivals.

With spring now just weeks away, and a central bank that has cut interest rates (and financial markets suggesting more are coming), banks will be very active and very competitive in pushing through multiple rate cuts to their advertised home loan rate cards.

First to break from the pack was ASB. Then it was Westpac. Responses from BNZ and Kiwibank will almost certainly come in the next day or two.

Main-bank competition is fierce at present.

Almost all banks will have some flexibility in their rate offers. So the carded rates are just the start. Negotiate. How flexible they may be will depend on the strength of your financials. And don't forget, banks have savvy tools at hand to 'know' the likely valuation of your property, so if the loan-to-value ratio (LVR) is near 80% you may not find them very accommodating for a lower rate. With falling house prices, the point where low equity premiums start applying is shifting around as well. See this.

And the carded rates we report here can be different to the rates banks might offer in their banking app. We would like readers to reveal what their banking app shows as the potential offer rates. Please add that market intelligence in the comment section below.

A quick check of the wholesale swap rate chart below gives a clear understanding of where funding costs are heading.

One useful way to make sense of the changed home loan rates is to use our full-function mortgage calculator which is below. Term deposit rates can be assessed using this calculator.

And if you already have a fixed term mortgage that is not up for renewal at this time, our break fee calculator may help you assess your options. Break fees will be minimal in a rising market. But they become important in a falling market.

Here is the updated snapshot of the lowest advertised fixed-term mortgage rates on offer from the key retail banks at the moment.

| Fixed, below 80% LVR | 6 mths | 1 yr | 18 mth | 2 yrs | 3 yrs | 4 yrs | 5 yrs |

| as at August 20, 2024 | % | % | % | % | % | % | % |

| ANZ | 6.89 -0.10 |

6.45 -0.40 |

5.99 -0.50 |

5.99 -0.35 |

5.89 -0.10 |

6.74 -0.10 |

6.74 -0.10 |

| 6.89 | 6.59 | 6.15 | 5.99 | 5.89 | 5.89 | 5.89 | |

| 6.89 -0.10 |

6.55 -0.30 |

6.15 -0.34 |

5.99 -0.35 |

5.89 -0.10 |

5.89 -0.10 |

5.89 -0.10 |

|

| 6.99 | 6.75 | 6.34 | 6.09 | 6.09 | 6.09 | ||

| 6.89 | 6.59 | 6.15 | 5.99 | 5.89 | 5.79 | 5.69 | |

| Bank of China | 6.95 | 6.79 | 6.59 | 6.39 | 6.09 | 6.09 | 6.09 |

| China Construction Bank | 6.99 | 6.85 | 6.49 | 6.34 | 5.99 | 6.40 | 6.40 |

| Co-operative Bank | 6.89 -0.10 |

6.39 -0.40 |

6.19 -0.30 |

5.99 -0.30 |

5.99 | 5.99 -0.10 |

5.99 -0.10 |

| Heartland Bank | 6.69 | 6.49 | 6.35 | 6.15 | |||

| ICBC | 7.05 | 6.85 | 6.65 | 6.49 | 6.39 | 6.29 | 6.29 |

| |

6.99 | 6.85 | 6.49 | 5.99 | 5.99 | 5.99 | 5.99 |

| |

6.99 | 6.69 | 6.65 | 6.25 | 5.99 | 5.99 | 5.99 |

Fixed mortgage rates

Select chart tabs

Daily swap rates

Select chart tabs

Comprehensive Mortgage Calculator

94 Comments

"In fact going sub-6% for eighteen months makes this their lowest since October 2022" - the table above shows 6.49%

Unfortunately, the 6 months term, the only one anyone should be interested in, is still 6.85% from ANZ.

6 months is still the go if you had to refix at the beginning of August, a month has already gone. The difference even now in total dollars over such a short term in negligible on a small mortgage. Rates could well be down in the low to mid 5's come February and it will be time to fix for a year or two. Reality is this is all good news for those paying off their home and it should bring in some stability for house prices.

its great news will be paying 6.85% for the next 6 months.... yay

if we all start buying houses again, and borrowing in general to buy stuff because interest rates have come down, then inflation will leap right back up again, and Mr Orr will have to put them back up to where they should have been for quite some time yet.

If that were true, then why wasn't there high inflation for the ~20 years before Covid?

Globalisation had us importing deflation. Magic money flowing into the economy just to try keep the inflation boat afloat, all of that money shifting to offshore settlement accounts through a growing trade deficit and luxury travel. Growing debt, low wages, even lower interest rates to support the debt. The question is, in a non-existential crisis way, where is cheaper from here? Where do we go that frees up more of our income to service debt? We already hit 50-60% of incomes to service debts, where does the additional money come from? This will end somewhere, and it's not going to be pretty.

The expectation there is that there will be a longer term rate <5.5% come Feb, but that rate could be for 18mo - 2yr and the OCR will be mid fall, looking lower again this time next year and towards the end of the year.

Fixing 6mo now is setting yourself up to fix long through what will likely be some significant falls through this cycle. In 6mo time, the 6mo rate needs to be 90bps lower to make that strategy a better bet than current 1yr. Either way you're coming round to refix this time next year and I think that the second half of next year we will see some very competitive rates. 18mo rate actually could be not bad here, again you're looking for current 6mo plus <5.5% 1yr in Feb to beat it.

Basically if you think we'll see >90bps falls in rates by Feb, go short. If not, then 1yr - 18mo are better options.

Or fix just long enough to get out of your cash-back obligation with your current bank so you're in a good position to negotiate for the next rollover.

I wonder if people will start moving away from the 6 month now. If you fix at 6.89 for 6 months, you then need to get 6% in 6 months time to end up better off than taking 6.45 for one year. Will the RBNZ drop 0.9% in the next 6 months?

Uncertainty, everywhere. From the AFR:

"The biggest market panic since the pandemic seems to have come and gone. But don’t believe the calm – this is a fragile market."

A2Milk down 16% this morning, for instance.

A2 and Synlait have both made announcements on the NZX hence one up and one down.

It's a good point, BW.

We're a long way from 'out of the woods'. Any euphoria about tiny rate cuts needs to be tempered by what is still to come. The OCR is still significantly contractionary and all indicators are NZ Inc. continues to contract.

That’s what Yvil doesn’t understand above. In 6 months he’d probably want to fix 1-2 years again which may not be the lowest rates then.

I doubt much will change in 6 months; RBNZ will still be on an easing cycle, so if you keep playing that strategy you would fix another 6 months. But I feel like there is more chance you end up worse off over a year.

"But I feel like there is more chance you end up worse off over a year."

"you feel"? wtf. Here you go:

https://calculate.co.nz/advanced-mortgage-calculator.php

Do the maths.

Oh but Yvil understands the interest rate market very well. In one year's time, rates will have dropped by much more than 1%, much more. Yvil will re-fix for another 6 months in February 2025. Ignore his wise advice and pay the financial price.

Yes but if you fix for 6 months you need to fix again in 6 months time. Are you sure rates will be more than 0.9% lower then? How many RBNZ meetings are there until then?

There will be 3 more OCR announcements in six months time, October and November 2024 and February 2025. Here is November 2024's OCR announcement.

"Given the deterioration of the various indicators, the panel has concluded that the OCR of 5.0% (after the October drop of 0.25%) is too restrictive and a substantially lower OCR is warranted. Therefore the panel has agreed to lower the OCR by 0.5% to 4.50%, and we forecast a similar easing for our next meeting in February 2025 (to 4.0%)"

Yes and because the trend is down, many people will fix short in Feb hoping to secure a good rate in August 2025. For this reason, Banks will hold the 6mo high, they do not need to attract customers when all the customers think they know best.

You called the big one right with the first cut...now with this comment you've got me overthinking it...I roll off in Dec damnit 🧐

LOL Yvil, it doesn’t take anyone smart to know if you keep fixing for 6 months you’re going to almost always end up losing.

Jesus. Why did I need to spell that out. Some “advice” and comments are here are just insanely crazy.

"Yvil, it doesn’t take anyone smart to know if you keep fixing for 6 months you’re going to almost always end up losing."

Why would that be, in times of steeply falling interest rates ? Please explain in detail ?

Interest did an article on this a few months ago , and 6 months came out on top, but not by much. The big advantage is it allows you the chance to repay, or change your monthly repayment rate to suit your income, if variable.presuming you want to reduce your debt, rather than just reducing your interest cost.

"Will the RBNZ drop 1.1% in the next 6 months?"

It's a possibility. It also depends on what you're being offered with your lending guy, e.g I was offered 6.75 for 6 months, and 6.45 for 1 year. Either way I don't think you can go wrong with either the 6 month or 1 year rate at the moment.

Yes in that case I would take 6 months...

LOL.

So you're saying the wholesale money market is going to do nothing for 6-months too? Seriously?

6 months from today is the third scheduled OCR meeting. a 25bps cut at each of those would be about break even with a 1 year fix by some back of the envelope numbers I just ran for the $160k I'll be fixing at the end of the week.

You can make your own guesses whether any of those meetings will be a no-cut meeting, or a double cut meeting. Or a surprise cut from an unscheduled meeting.

So you're saying just one cut above 0.25% and you'd be better off taking the 6 month rate?

I just checked back and I did ok with fixing for 6 months the last 2 times. 7.05 and then 6.99. 12 months was 7.05 and 18m was 6.95. That was with potentially rising interest rates but I didn’t see them going much higher. This time there is more scope for them to drop quite fast. 12 mount rates below 6 are not out of the question this year.

We are all still getting fleeced, but perhaps by a little less now.

Short-term rates are horrendous given where the economy is at.

"We are all still getting fleeced, but perhaps by a little less now."

The retail banks appear to preserving their margins and not giving anything away. Seem to me they're fleecing us the same as always.

So who's fleecing us less?

Will be interesting to see if the other banks match or go lower still.

They can all go lower still and keep their juicy margins if predictions of where the OCR is going are correct.

They can, but why would they? As noted above, everybody has been certain rates will be lower in 6mo for about a year now, and further into Feb. The short term rates will surely be slow to come down because they know people will opt for the short term cost thinking things will be lower again and again. So, Feb. OCR 4.5? 4?? Will the 6mo rate follow each of those cuts one for one? Who knows..

I think the banks know it’s not so easy to change in reality. Who can be bothered with all the tedious paperwork to save another 0.25 or 0.5%.

Will this change with open banking?

"Who can be bothered with all the tedious paperwork to save another 0.25 or 0.5%."

Sure. But don't complain that banks are making too much money, or they're ripping us off, if no one does the simple maths to check whether they're really engaging in any sort of competition.

Come to think of it ... David, that's a calculator you don't have. And it'd be quite useful to improve competition.

There is costs associated with changing banks and the cash backs lock you in for several years. There are other factors to consider also. Other than breaking and refixing there is very seldom much difference in rates between main banks.

Probably looking to improve the picture... Others will likely follow ...looks like a Peter/Paul scenario for savers but they wont want too many folk walking elsewhere looking for better TD rates. My opinion.

"For the six months to March 2024, ANZ has reached out to over 200,000 homeowners to offer extra support and 8,500 customers have completed a home loan check in," ANZ NZ says.Watson says only about 17% of ANZ NZ's home loan customers are still on interest rates below 5%." "The ANZ Group says ANZ NZ has 82 cents in deposits for every $1 in loans.... (Interest.co.nz 07.05.2024)

This is fantastic news. I mistakenly clicked on the link to the Ferraris for sale at Conties. It is obviously karma. With these low interest rates I have decided to get one and chuck it on the mortgage. It’s going to be epic.

You may as well buy a personal brewery too

No I’ll have to cut back there. Don’t want to risk a DIC in the Ferrari and have it impounded.

Less than a handful of years ago, a 5 years mortgage rate was ~3.99% and the prevailing wisdom of the times was "Fix short - they are going lower" (something about don't touch them with a bargepole). And where did the OCR go? From 0.25% to 5.5% - totally unexpected back then.

Why that happened is not as important as the fact that it did. No one saw it - no one. And there's no guarantee that the same thing will not happen again today - or worse.

An OCR of 5.5% isn't high, yet we think our economy is threatened unless we lower interest rates? (That should tell us all what we choose not to know about Risk)

Fix short by all means, but know that by doing so you have increased your Risk Profile - Duration being part of the calculation. As with anything, you get what you pay for.

Or indeed it could drop from 5.5% to 0.25%. I think that's unlikely, but more likely than an increase to 10%.

You could be right. But what would our economy look like if we have to revert to 2.5%, let alone 0.25%? Arguably, it would look far better if the OCR was 10% because that tells us that borrowers can borrow; make money and profit, and still make the Risk of taking on Debt at that level, worthwhile.

Ultimately we cannot go there until significant policy change.

"But what would our economy look like if we have to revert to 2.5%, let alone 0.25%?"

That depends on what the RBNZ does with DTIs.

Ratchet them down hard and banks would need to lend to others, like, I don't know, maybe to productive businesses?

Yes. This should be the centre of the analysis. To be honest, I think most commentators don't even understand this basic principle.

"No one saw it - no one"

A few did, and fixed long for 2.89%. I would listen to these few people.

I missed the boat and only got 2.99% expiring next year..If Im lucky we will be back to that rate by then? Gotta keep the Ponzi going..

Well done Baywatch.

I'll offer my serious thoughts in May 2026 when my 5 year fix expires.

/humblebrag

My 5 year expires December 2026. I hopped on the elevator part way up, at 4.95%. Beats paying 6% for the last 3 years.

I don't get why the banks don't offer really competitive 5yr rates, get punters locked in. 6.74% for 5 years from ANZ is a joke! It really needs to start with a 4 or maybe a 3.

Considering that the 5 year swap rate is at 3.58% and 1 month ago it was over 4%, there's not enough margin for a bank to offer 5 year rates below 4% at the moment.

Lock a punter in for $500k at 3.99% for 5 years, make about (0.0399 - 0.0358) * $500000 * 5 = $10,250.

Maybe that is small change to the big banks, but surely a challenger could do it?

4.99% maybe. Don’t see a rate starting with a 3 appearing this year.

Somewhere in Riverhead right now, Wingman just had an orgasm.

I don't live in Riverhead, but I have bought some land and building a house there, because I've done loads of homework and come to the conclusion I'm going to make a bundle.

https://www.aucklandcouncil.govt.nz/UnitaryPlanDocuments/06-pc100-app-4…

I disagree Wingman, you're going to print money, not just make money. Great forward thinking buying out there with reference to Unitary Plan. I'd do the same if I had extra capital.

How long before the 6’s fall off?

The Fed may give up some hints re rate cuts at Jackson Hole this week. But, if they do in fact cut in Sept.....I wouldn't be surprised if NZ follows suit for a second cut in Sept. I would say at least another cut in NZ between now and Nov, so 6% rates should be mostly wiped out before the end of the year in my opinion.

You are predicting an out of cycle cut by the RBNZ in Sept if the Fed cuts in sept?

"Main-bank competition is fierce at present."

Were that correct, the 6-month rates would reflect it. They don't.

All the movements at longer periods is the banks pretending they don't know the what effect successive OCR cuts will have. Rest assured, the banks will still be coining it in at one-year and above.

Question:

For a Lender, is the Risk Higher or Lower to lend at 7% and then see rates halve to 3.5%, or to lend at 3.5% and see them double to 7%? Answer: The risk is Lower at Higher interest rates. Because if they lend at 7.5% and rates fall, their borrower will be just fine as their repayments will be more affordable. But the reverse applies if they lend at low rates - it's Riskier. Interest Rates are Dynamic.

Yet, we are trying to go back to exactly where we have just come from - Lending low and risking a future of higher repayments! And just look at all the squealing from the Lenders at having miscalculated their past Risk Profile. I know! "It will be different this time"

"Insanity is doing the same thing over and over again and expecting different results."

"And just look at all the squealing from the Lenders at having miscalculated their past Risk Profile"

Are you sure about that? It seems to me that the banks (the lenders) are doing just fine.

Here's a paraphrase; When you owe the bank $1m, that's your problem. When you owe the bank $100m, that's their problem.

So whose problem is the commercial banks risk profile? The banks seem to be doing just fine... so is it theirs?

That paraphrase is a bit simple. If the bank has security over something they can quickly sell for more than you owe them, it's still your problem. It's only when the security (at sell it TODAY prices) is worth less than the loan that the bank really has a problem.

And where are the risks if they lend at high rates and the rates go higher?

You could almost say the initial rate is irrelevant, only the direction of the change matters.

Anyone got the App rates. I'm falling due $250k and just been offered 6.85 for 6mnths (I'm LVR 50%+).

Same here. ASB. 70% equity. Time to switch banks I would think? Their public rate is 6.89 so 6.85 via app is a joke, surely?

Kiwibank via the broker today

6mth 6.85%

12mth 6.59%

2-5yrs 5.99%

I assume this was before ANZ moved so I'm going to sit on my hands for another few days and see what happens.

I just told the broker to let KB know that their offering is same/worse than Westpacs carded rates and we are not amused.

Kiwibank… leading from behind. Making banking more competitive as usual.

I was getting a RCF limit boosted to it's maximum by KB the middle of last week and was told "wait till Monday" for a better result. I got the impression their internal processes when the market changes rapidly may struggle to keep up. Given market movements in the last few day, KB's answer may be better once they've had an extra few days. Let us know what transpires.

Time to take home lending off commercial banks and into building socities witl longer terms available ie 5-10-20-30 years of to reduce the volatility out of the home loan market

It cant be right that you buy a house and you sit comfortable, then less than 12 months later you are at foodbanks trying to survive on the same income as you been on all the time...

With longer terms you would have time to make an exit plan , if circumstances changed.....

Excellent idea. USA does it so why not here.

Anyone attempting that would probably get shot due to the amount of money involved. But this would be the most significant piece of beneficial legislation passed, maybe ever in NZ. As it is we send a major chunk of our GDP off shore.

The commercial banks have clearly demonstrated they're reckless in setting the test rates. Some banks were operating at 5.5% test rate in 2021, before ratcheting it up to over 9% less than 12 months later. Some borrowers came out of 12 month fix terms onto interest rates higher than they were benchmarked for.

People claim borrower responsibility etc, but the banks are supposed to be the subject matter experts and they derive a healthy profit for doing so.

Yawn

Wake me up in June ‘25 when I am ready to fix again and retail rates are at least 1.5% lower

Wasn't the NZD predicted to plunge by the 'experts' here after the recent reduction in interest rates? It's done the opposite.

https://www.investing.com/currencies/nzd-usd-chart

Yep, here and on Reddit. I suspect in many cases they are the same x-spurts posting on both.

The rate cut was priced in by markets plus many more but the RBNZ had to have the narrative of a slow and controlled reduction now shows a better than expected result hence NZD hasn't dropped. Probably they're whole point in the May narrative - currency wars, nothing to do with internal economics...

"Probably they're whole point in the May narrative - currency wars, nothing to do with internal economics... "

More fodder for the conspiracy theorists?

We have 70% equity, and been offered 6.85% for 6 months by ASB, online via Internet Banking. Time to switch? Their public rate is 6.89 so it's hardly competitive.

They will discount different terms differently. I fixed for 6 months in May and got 0.86% off the carded rate of 7.85 (6.99). With the same discount I’d get 6.63 now. Looking back at what I’ve been offered it ranges from 0.8-0.94% off standard. The specials advertised are 0.6% off standard at present ANZ. I roll over in Nov so it will be interesting to see what sort of discounts are available.

So 6.29% for 6 months at ANZ as a special rate? (0.6 off the carded).

Absolutely not. I have just renewed with ANZ for 6 months, I have good financials, 6.85% was (disappointingly) the best we could get.

How hard did you push? I'm going for 6 months and 6.85% is offered via app. Plenty of equity.

Did you call? Ask for any cash back?

Went through my broker, yes I got a cash back.

Spill the details Yvil - what %?

You're helping to increase competition between the banks !

Can anyone share a big bank with a better rate than 6.85% for 6 months or 6.45% for 12 months.

And if any cash back.

Can't seem to get anything better despite giving it a decent nudge

@averageman I would like your view ? You missing here I was hoping for 5.5 by March you mentioned it’s not possible due to rates being close to 7%…… I need your view it usually levels out my spruiker view

Clearly, they are trying to get renewals go for the longer terms. That tells us where the banks think rates are heading.

According to my Premium Banking manager the rates shown as current on your mortgage interest rate chart are incorrect. They tell me the floating rate is not available until 29th August.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.