By Sheryl Sutherland*

I recently read a feature article based around the financial life of a 72-year-old. The retiree had a freehold home and little else, relying on the Super of $606.67 per week (before tax) for a single person living alone. Not surprisingly, the lifestyle the retiree enjoyed was financially restricted.

Takeaways were a sandwich and a slice from the bakery, with the biggest edible indulgence being cheap chocolate bars. Nothing was spent on alcohol, but a small amount on petrol. In winter it’s to bed in the evenings to save money.

Not surprisingly, the retiree described themselves as constantly concerned about their financial situation.

Many adults in this age group suffered through very low wages most of their life, allowing only the ability to pay off a mortgage, but have little or no savings. Women, of course, are harder hit than men; due to shorter and interrupted paid working lives, lower pay and often acting as primary caregivers for parents. There is no doubt that retirees need to have significant savings or additional income later in life so that they can live comfortably.

There is an option that those over 40 can utilise – fortunately, like the retiree I mentioned, most retirees are likely to own their own home. This can provide a solution. Currently in New Zealand there are two offerings which could assist in this instance - the Southland Building Society and Heartland bank. If you choose to go down this path, I suggest that you examine and compare both offerings. You should, of course, also discuss them with your lawyer and your family. A note of warning here though: I have seen instances where family have been quite resistant to any borrowing as it will erode their likely inheritance. Heartland bank advise that they have assisted more than 23,000 kiwis release equity through the means of a reverse mortgage.

A reverse mortgage is a loan against your home. Unlike a standard mortgage, you don’t make regular repayments, although you can at any time. The loan balance will grow over time due to compounding interest. The loan is payable when you move out. It is important to remember that you still retain ownership of your home and just like a standard home loan, the mortgage will be registered against the property. Typically, funds are used for debt consolidation, family support, day to day expenses, medical and health care, home improvements, travel and holidays – almost anything to make life easier and more comfortable. The following table outlines the differences between and standard mortgage and a reverse mortgage:

| Standard Mortgage | Reverse Mortgage |

|

|

How much could you borrow? That depends on your age and the value of your home – summarised in the table below (although this may vary slightly for different lenders):

| Age of youngest borrower |

Maximum % of home's value available |

| 60 | 20% |

| 65 | 25% |

| 70 | 30% |

| 75 | 35% |

| 80 | 40% |

| 85 | 45% |

| 90+ | 50% |

A common question is how a reverse mortgage adds up over time, and how much equity will remain in the property when the loan is due to be repaid. This depends on a number of factors including the interest rate, term of the loan and any increase in property value. The following is an example put together by Heartland bank for illustrative purposes.

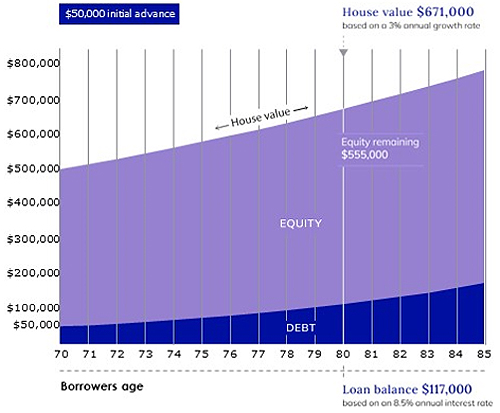

Jo and John are both are 70 years old and they own a home valued at $500,000. The maximum amount to them available is $150,000. Initially, they choose to draw dawn $50,000 for home improvements, and set $100,000 aside in a cash reserve facility in case they need it in the future. The cash reserve is never drawn, meaning interest is never charged on that amount.

The following graph shows what happens to Jo and John's equity over time. While the loan debt increases, so does the value of their property. The amount of equity increases as a result. In dollar terms, Jo and John will have more 'net equity’ after 10 years than what they did before the loan, about $571,000 of the home value. After 15 years, when they are both 85 years old, there would still be $636,000 remaining.

Remember, this graph is simply an example. A reverse mortgage is designed to last as long as required, or until you move permanently from your home. Your provider should be able to give you a personalised loan projection.

Reverse mortgage providers should offer guarantees to protect you. You should always ask your provider about the guarantees they offer. If you do decide to proceed with o reverse mortgage, look for the following safeguards.

Lifetime occupancy

You can own and live in your home for as long as you choose.

Loan repayments

You should not have to make any loan repayments until the end of the loan.

30-day cooling off period

It's important you feel comfortable with your decision. You should be given the opportunity to change your mind within 30 days of taking out your loan.

No negative equity

The amount required to repay the loan should not exceed the net sale proceeds of the property.

Equity protection option

You should be able to choose to protect a percentage of the eventual net sale proceeds of your home and the chosen percentage should be guaranteed.

Independent legal advice

It is important that you are completely happy with all aspects of your reverse mortgage. To ensure this, you should seek independent legal advice from a solicitor of your choice, who will represent your interests and work with you to explain and discuss your loan.

This may not apply to you at this stage in your financial life but tuck this knowledge away, it may be a useful weapon in the future.

Current reverse mortgage interest rates are listed on this page. Most banks do not offer them, but see Heartland Bank, and SBS Bank, as examples of ones that do. And remember, reverse mortgage rates are floating rates.

*Sheryl Sutherland is director of The Financial Strategies Group, and author of Girls Just Want to Have Fund$ – Every Women’s Guide to Financial Independence, Money, Money, Money Ain’t it Funny – How to Wire your Brain for Wealth, and co-author of Smart Money – How to structure your New Zealand business or investments and pay less tax. You can contact her here.

2 Comments

This is an important article if we start introducing wealth indexed superannuation for rich retirees.

Cut The Pension CTP 🎬

Raise the pension !

How many folk actually perceive that having worked hard and paid off the mortgage, life may not be the bed of roses many expect. Lack of liquidity can make day to day life a trudge and being older limits options . Having all your equity tied up in an asset such as your home is something many overlook. Plenty of folk choose to downsize to release capital and often reverse mortgages are frowned upon. The general model is that the value of your asset (house) will increase over time. But it is also TRUE that RE cycles tend to inflate then decline somewhat before trending again. My guess is that if you can clear debt at or near peak and jump back in at the bottom of a cycle in the right locale it might very well be possible to make either a downsize or reverse mortgage work significantly better for you. So timing is critically vital because risk is ever present but lets face it that hard earned pension just doesn't cut it these days so alternatives are always worth exploring. Do your homework , dont just jump in the deep end , know fully what you are getting into ...Ask yourself is this the right time . You are looking for a favorable outcome... not more headaches...choose wisely and remember timing is critical...sell high/buy low... RAISE THE PENSION !

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.