They process $95 billion of card payments in New Zealand annually and NZ businesses spend about $1 billion a year to accept their card payments.

Who am I talking about? Global payments behemoths Mastercard and Visa.

Chances are if you have a credit or debit card in NZ it's a Visa or Mastercard one given their cards are promoted and issued by NZ's key retail banks.

Visa has the bigger presence with ANZ, ASB, BNZ and Kiwibank issuing Visa cards. Mastercard cards are issued by Westpac, TSB and the Co-operative Bank. SBS Bank issues Visa credit cards and Mastercard debit cards.

According to the Commerce Commission, which regulates the Visa and Mastercard credit and debit networks under the Retail Payment System Act 2022, $95 billion of card payments are processed annually by Mastercard and Visa. It estimates NZ businesses spend about $1 billion a year to accept their card payments.

Given that, you might expect the two to have sizeable NZ operations, booking significant revenue and profit in NZ, and paying chunky sums in tax here. But that's not the case. Instead Mastercard and Visa's NZ operations are run through regional hubs in Singapore.

Whilst NZ may be a small but presumably lucrative market for them from a global perspective, any tax on payments revenue generated in NZ is paid in Singapore. The latest annual financial statements from the two show Mastercard's Singapore unit paid a 1.1% effective income tax rate and Visa received an income tax credit.

Are New Zealanders paying too much?

In November 2021, 20 years after Australia embarked down the same path, Visa and Mastercard's interchange fees were capped in NZ ahead of the Retail Payment System Act taking effect a year later. This followed a 2020 Labour Party election pledge.

Now, in a new consultation paper, the Commission is questioning whether New Zealanders are still paying too much to make and receive payments using Mastercard and Visa cards.

It thinks we might be and is thus consulting on potentially reducing these costs.

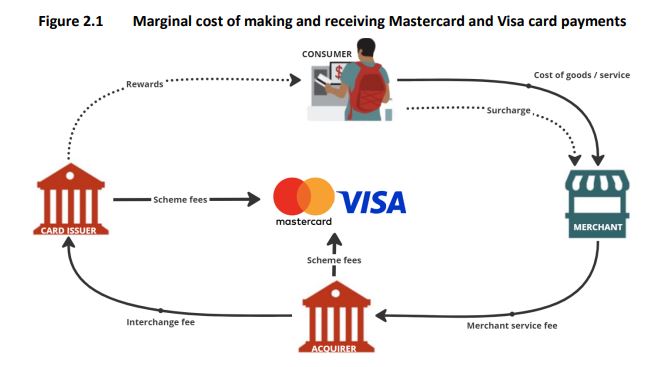

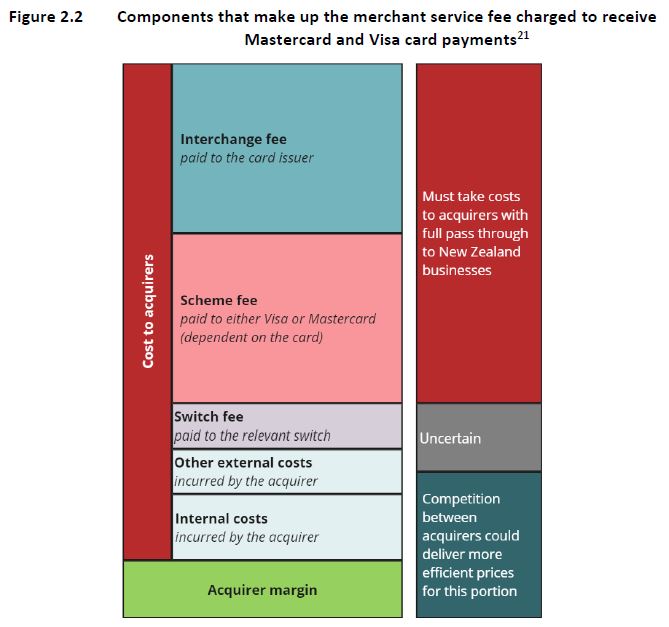

As the Commission puts it, when a customer uses a Mastercard or Visa debit card online or contactlessly, or a Mastercard or Visa credit card to purchase a good or service from a business, the business is charged a merchant service fee by its bank. Mastercard and Visa interchange fees comprise about $600 million, or 59%, of these merchant service fees paid by NZ businesses to banks for accepting Mastercard and Visa card payments.

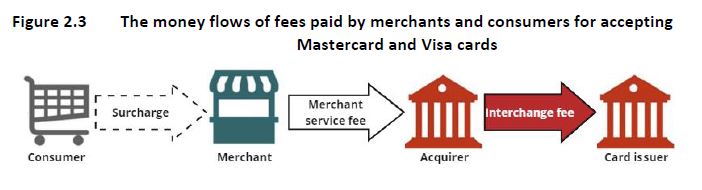

Mastercard and Visa interchange fees are charged by the bank/financial institution on one side of a payment transaction to the bank/financial institution on the other side of the transaction. A typical card transaction involves four parties - the cardholder, the cardholder's financial institution (the issuer), the merchant and the merchant's financial institution (the acquirer). For most card transactions, the interchange fee is paid by the acquirer to the issuer.

The Commission says further interchange fee regulation could reduce fees substantially. Assuming 90% of potential savings are passed through to merchants, merchant service fees could fall by more than $250 million annually, it says. This estimate is based on 0.20% domestic and 1.15% international interchange fee rates, which currently range from 0.20% where they're regulated to as much as 2.40% where they're not.

Carolyn Young, CEO of retailers' lobby group Retail NZ, says retailers would welcome lower fees. Young says of around 37,000 retailers about 35,000 have no ability to negotiate the rates they pay. And, if they can't accept payments they can't do business.

"A medium sized retailer told me yesterday by the time they look at their profit margin of 4% to 4.5% and take off fees of 2%, they end up with a very tight margin of about 2%, and that's for a business in surplus," Young says.

Mastercard and Visa are strategic partners of Retail NZ.

Ticket clipping

The Commission points out whenever someone buys something, gets paid, transfers money, or uses an ATM, they're using the retail payments system making it the most used financial service in NZ.

The consummate ticket clippers, Mastercard and Visa are all over retail payments. They look to position themselves at the centre of the payments system and are adept at embracing new threats to their businesses, enabling them to clip the ticket when new payments technologies and services emerge. Visa calls this its "open partnership model."

Speaking in 2020 Visa Inc's then-chairman and CEO Alfred F. Kelly, Jr, noted the company's goal to be in the middle of any transaction in the movement of money, both on the Visa network and beyond.

And in his latest annual CEO letter Mastercard Inc's President and CEO Michael Miebach notes; "People have a choice in how they pay – card, account-to-account, buy now, pay later and more. Our focus is on giving them a reason to choose Mastercard across all these areas. And they are."

In Visa Inc's latest annual report, CEO Ryan McInerney details Visa's scale. Its network spans more than 200 countries and territories, about 14,500 financial institutions, more than 130 million merchant locations and 4.3 billion payment credentials, he says.

"All told, during our full-year 2023, the Visa network enabled US$15 trillion in total volume and 276 billion transactions," McInerney says.

The two US companies, and their shareholders, enjoy an incredibly profitable business model.

For the year to September 2023, Visa Inc reported net revenue of US$32.7 billion, net income of US$17.3 billion, and share buybacks and dividends of US$16.1 billion.

For the 2023 calendar year, Mastercard Inc recorded net revenue of US$25.1 billion, net income of US$11.2 billion, and dished out US$11.2 billion to shareholders via share buybacks and dividends.

How Mastercard & Visa operate in NZ

Against the backdrop of the Commission's consultation, it's interesting to look at how Visa and Mastercard operate.

Visa's NZ company, Visa Worldwide (New Zealand) Limited's shareholder is Visa Worldwide Pte Ltd of Singapore, with its ultimate parent Visa Inc. of the US.

Visa Worldwide Pte lists the NZ company as a 100% owned subsidiary alongside companies from Australia, Hong Kong, Singapore and Indonesia. It says Visa Worldwide NZ's activities are marketing support, client support, and relationship and liaison services to its related company.

Whilst Mastercard New Zealand Ltd is registered in NZ, as the company told the Commission in a 2022 submission; "The entity which carries on Mastercard's cards business so far as it relates to New Zealand, including licensing the Mastercard name and marks, is Mastercard Asia/Pacific Pte Ltd."

Mastercard Asia/Pacific Pte is also a Singapore company, with Mastercard Inc of the US its ultimate parent company.

The 100% owned Mastercard New Zealand Ltd is listed as one of 20 subsidiaries of Mastercard Asia/Pacific Pte in the latter's most recent financial statements. It's described as "providing services to its related companies." Other subsidiaries include Mastercard companies across a range of Asian, African and Middle Eastern countries.

Singapore sling

One of the things the Singapore link, or Asia-Pacific operating hub as Visa puts it, means is Visa and Mastercard's NZ revenue flows through the city state. That in turn means income tax on payments revenue generated here is paid there, rather than in NZ.

At 17%, Singapore's standard corporate income tax rate is already significantly lower than NZ's 28%. However, Mastercard and Visa's Singapore operations pay much lower effective tax rates than that.

Combined, Mastercard and Visa's Singapore arms recorded annual pre-tax profit of more than US$6.8 billion in 2023, with Mastercard's share of that US$3.7 billion, and Visa's US$3.1 billion. Mastercard paid income tax of US$40.325 million, which Interest.co.nz's calculations suggest is an effective 2023 tax rate of a mere 1.1%. Visa booked an income tax credit of US$49.470 million.

So how does this work?

Mastercard Inc's annual report notes Mastercard Asia Pacific Pte "received an incentive grant from the Singapore Ministry of Finance." This provided it with "a reduced income tax rate...on taxable income in excess of a base amount."

"Without the incentive grant, Mastercard Asia Pacific Pte would have been subject to the statutory income tax rate on its earnings. For 2023, 2022 and 2021, the impact of the incentive grant received from the Ministry of Finance resulted in a reduction of Mastercard Asia Pacific Pte’s income tax liability of US$571 million, or $0.60 per diluted share, US$454 million, or $0.47 per diluted share, and US$300 million, or $0.30 per diluted share, respectively," Mastercard Inc says.

Visa Inc discloses a similar deal, saying its Asia-Pacific operating hub has benefited from a tax incentive, conditional on meeting certain business operations and employment thresholds in Singapore.

"In fiscal 2023, 2022 and 2021, the tax incentive decreased Singapore tax by US$468 million, US$362 million and US$273 million, and the gross benefit of the tax incentive on diluted earnings per share was $0.22, $0.17 and $0.12, respectively," says Visa Inc.

Visa Worldwide Pte was also helped in 2023 by a US$105.105 million tax credit arising from a re-evaluation of its tax position in an unspecified foreign country.

Revenue sources the Mastercard and Visa Singapore units cite are a smorgasbord of fees; Domestic assessment fees, cross-border volume fees/international transaction fees, transaction processing fees, service fees, data processing fees, and royalty fees.

In contrast to the tight retailer margin cited by Young above, Mastercard Asia/Pacific Pte had an operating profit margin of 65.63% last year and Visa Worldwide Pte's weighed in at 77.71%.

Some hints at their NZ scale

We don't know exactly how much revenue or profit Visa and Mastercard make in NZ. It would be a small chunk of their respective reported Singapore earnings. However, in a NZ context these would probably be significant sums.

Visa Worldwide Pte's financial statements provide some detail on NZ. For example, they note the company had US$36.618 million of exposure to NZ credit risk for trade and other receivables, including tax receivables, as of September 30 last year. And its foreign currency risk exposure included a net position of US$167.187 million against the NZ dollar.

Additionally Visa Worldwide Pte says a 10% strengthening of the US dollar against the NZ dollar would've increased its 2023 profit by US$6.607 million.

As for Mastercard Asia/Pacific Pte, it discloses NZ dollar financial assets, almost entirely comprising cash and cash equivalents of NZ$41.217 million at the end of 2023. It also had NZ$105.816 million of financial liabilities, almost all of which was attributed to trade payables.

Complying with tax laws

It's important to note we're not suggesting Mastercard or Visa are breaching any NZ tax laws. It appears to be more a case of utilising global networks, scale and a friendly tax jurisdiction, for an arbitrage play.

"Mastercard New Zealand complies with all tax laws," Mastercard says in a statement attributed to Ruth Riviere, its Country Manager for NZ and the Pacific Islands, and a Mastercard New Zealand Ltd director.

"Our contribution to the payments landscape, the wider business community, and Kiwi customers provides significant benefit to New Zealand every day," Riviere says.

Asked to provide examples of the benefit cited, a spokesman says Mastercard; "Will certainly be outlining their vital role in the NZ payments landscape in their submission [to the Commerce Commission]."

A Visa spokesman says; "Visa treats its tax obligations seriously and complies with all applicable New Zealand tax laws and reporting obligations."

"As a global digital payments network, Visa contributes to the economic growth, development and financial inclusion of New Zealand’s consumers and merchants."

"We work with the broader payments ecosystem to ensure security is at the forefront of our technology and capabilities, including tokenisation, AI-powered fraud prevention, and biometrics. Visa’s artificial intelligence (AI) based real-time payment fraud monitoring solution has helped New Zealand financial institutions prevent $273 million in fraud from disrupting New Zealand businesses in a year," the Visa spokesman says.

Inland Revenue itself has a long standing policy of not commenting on the affairs of individual taxpayers due to tax secrecy laws.

'Regulatory intervention in interchange fees can lead to unintended consequences'

The Visa spokesman says the company has met its obligations under the Retail Payment Systems Act and reduced interchange fees to be in line with the regulatory caps introduced in November 2022.

"It’s important to note that Visa is a payments network, not a bank, and does not set fees for merchants or consumers. Interchange fees do not generate any revenue for Visa in New Zealand," he says.

"Visa is committed to encouraging a fair and level playing field for all participants in the New Zealand payments ecosystem, and we believe the best path forward for payments policy is to strike the right balance for all in terms of cost, value, security and innovation."

"Interchange is just one component of the merchant service fee that a business pays their acquiring bank, but it plays a critical role in supporting the resilience of New Zealand’s payments ecosystem and balancing the interests of all participants, including merchants and consumers. It supports issuer investment in providing best-in-class digital payments and fosters the adoption of innovative technologies that support security, while compensating participants in the payments ecosystem for the risk they undertake," the Visa spokesman adds.

He goes on to say regulatory intervention in interchange fees can lead to unintended consequences including reduced investments in secure technology and infrastructure by issuers and acquirers, less innovation, and uncertainty over whether perceived cost reductions for merchants actually benefit consumers.

"It may also undermine the entrance of new entities, such as payment facilitators and fintechs, that can bring more innovation and value-added services to the payments ecosystem," the Visa spokesman says.

"Visa transactions deliver specific benefits and additional value to both consumers and merchants, such as enhanced fraud protection, dispute resolution mechanisms, and international and ecommerce transactions that help merchants grow their businesses. Visa is one of multiple ways of paying in New Zealand, alongside the domestic network and other international payment networks."

Riviere's statement says Mastercard is currently drafting a submission to the Commission.

"The Retail Payment System Act was passed two years ago, and its objectives are to promote competition and efficiency in the retail payment system for the long-term benefit of merchants and consumers in New Zealand. Mastercard’s interchange rates for retail credit and debit transactions made within the Mastercard network are in line with the current regulatory caps in place in the initial pricing standard issued pursuant to the Act," she says.

"The broader payments industry has never been more competitive than it is today, and it is important for Government policy to get the economic parameters right to continue to incentivise new innovation and even more investment in safety and security. We compete every day across the robust set of payments options available to consumers, from cash to several global and regional networks, and increasingly, buy now pay later providers, person-to-person and account-to-account services, real-time payments platforms, digital currencies, wallet providers, and other forms of payment."

Of interchange & must take payments

Visa says it sets interchange "reimbursement" fees as transfer fees between issuers and acquirers to balance and grow the payment system for the benefit of all participants. Mastercard says interchange is a small fee paid by a merchant's bank (acquirer) to a cardholder's bank (issuer) to compensate the issuer for the value and benefits that merchants receive when they accept electronic payments.

An example Mastercard provided to the Commission in a 2022 submission notes on a $100 transaction the switch, Mastercard, would calculate the issuer is allowed to keep 0.30% as interchange and would thus require the issuer to pay $99.70 to the acquirer so the acquirer can, in turn, pay the merchant.

Interchange, however, has its critics. A 2018 report on competition in the Australian financial system by the Australian Productivity Commission recommended a ban on card payment interchange fees. It argued this would result in merchant service fees falling, reduce the costs of the payments system overall if cardholders move some of their card payments to other, lower-cost payment methods, such as cash or bank transfers, and reduce cross subsidisation from the prices all consumers pay to the rewards received by some cardholders.

The Reserve Bank of Australia has said interchange fees may be appropriate in the establishment of new systems where they may be necessary to rebalance costs between the sides of the market, and ensure both sides of a market have an incentive to participate.

"However, the major card schemes [Mastercard and Visa] are mature systems, and regulators in many countries have reached the judgement that their cards are ‘must take’ methods of payments – that is, that merchants have little choice but to accept their cards. In practice, with interchange fees being used to incentivise issuers to issue cards from a particular scheme and cardholders to use that card, the tendency has been for competition between mature card schemes to drive up interchange fees and costs to merchants, with adverse effects on the efficiency of the payments system," the RBA said.

What about Eftpos?

NZ businesses can, of course, receive in-person card payments with no fee per transaction when they are processed by the Eftpos network. The Commission notes no other country has a domestic debit network like Eftpos where there is no per transaction fee. Eftpos is available via Worldline, formerly Paymark, and Verifone NZ networks.

Eftpos currently only services in-person card payments and charges businesses a monthly terminal fee for the connection to the Eftpos network for unlimited payments. Eftpos use has been in decline and the Commission expects this to continue.

"In 2023, 30% of the in-person transactions on contactless-enabled debit cards were contacted and processed through the Eftpos network. Whilst uncertain, we provisionally estimate this to reduce to around 20%. This would lead to an approximate increase of $5 million in merchant costs... In 2023, 57% of all in person card payments in New Zealand were contactless [primarily Visa and Mastercard], an increase of 28% from 2019," it says.

And surcharging?

The Commission says some interchange fees in NZ remain materially higher than those observed in other countries, and there's potential to reduce "a significant component and the complexity of the fees" paid by NZ merchants to accept payment from Mastercard and Visa payment products.

This, the consumer watchdog says, should also reduce the surcharges NZ consumers face, and/or reduce retail prices or lessen inflationary pressure on businesses to increase prices. It says interchange fees can lead to high and overly complex costs for businesses given the hundreds of interchange fee categories.

A surcharge is a fee a business adds to a consumer's transaction when they use a particular form of payment such as a credit card, which may be expensive for the business to provide. The Commission, which can issue merchant surcharging standards under the Retail Payment System Act, says appropriate surcharges should be no more than a businesses additional cost for accepting a particular payment method type.

"In most cases, this will be your merchant service fee for that payment method."

The consumer watchdog says the average surcharge imposed by merchants is about 2%.

"Currently we have a payment system where surcharging is not a consistent practice and where surcharging does occur, often this is a blanket rate that does not change dependent on the different cost of each payment method. This means consumers that use Mastercard and Visa do not directly face the costs (surcharges) or necessarily receive the benefits (rewards) of card use."

"Interchange fees are widely used to fund card rewards. In the absence of surcharging, the cost of a consumer’s choice of payment is, in part or in full, borne by New Zealand businesses and in turn all consumers, while the rewards benefit only some consumers...surcharges can be used to counter this distortional impact but only when they accurately reflect the underlying cost," the Commission says.

"If merchants did not respond to a reduction in merchant service fees by reducing surcharges, we could seek to address this by setting caps on maximum surcharges that can be applied and publicising this cap."

"Maximum merchant service fees and surcharges for domestic transactions could be reduced to approximately 0.70%. We expect this would result in fewer merchants surcharging and if they did, surcharges could drop to no more than 0.70%," says the Commission.

Young says for some small retailers who have no control over other costs such as supplies, rent and wages, surcharging enables them to recoup card acceptance costs. She suggests 20% to 30% of retailers are surcharging.

For its part Visa says it has a global policy of opposing merchant surcharging, which it says can "discourage growth of the digital payments ecosystem and cardholder usage."

The Commission's deadline for submissions on its consultation paper is September 2.

*Figure 2.1 below comes from the Commerce Commission's Retail Payment System Costs to businesses and consumers of card payments in Aotearoa New Zealand: Consultation Paper.

*Figure 2.2 also comes from the Commerce Commission.

*And figure 2.3 below comes from the Commerce Commission too.

*This article was first published in our email for paying subscribers early on Wednesday morning. See here for more details and how to subscribe.

23 Comments

Online EFTPOS? ASB supports with certain vendors…..

It's not widespread enough to warrant it being a viable alternative. Credit cards are easy and simple and you can use them almost everywhere. Even if it were popular in NZ, it wouldn't be available for overseas vendors.

From a storefront perspective, tap and go / apple pay etc are just far simpler, and since you don't need to touch a disgusting eftpos machine to make the transaction it helps prevent spread of viruses and germs etc.

NZ needs to legislate on preventing additional taxes at checkout like paywave, similar to how the european union does it. Businesses may up their costs to compensate but at the end of the day you can make an educated decision on whether or not you want to purchase something based on the price you see on the item.

I'd like to go the other way and require the actual cost of all transactions to be additional to the purchase. Consumers would then be aware and pay accordingly. I'm sure eftpos could be made to work contactlessly. Eftpos is being undermined by the vested interests of the credit cards and the banks that issue them.

This.

I cannot for the life of me understand why 20 years late, eftpos still does not have contactless. Why would you pay 1% surcharge to use your visa debit, if you eftpos card could do contactless for free?

Either worldline are in bed with visa/mastercard - i guess that they get greater commission on visa/mastercard transactions. Or perhaps there is some stupid patent on using NFC for bank transactions that visa/mastercard have. It surely can't be that worldline are just happy to see eftpos slowly die?

Ireland plays the same game. They offer much lower corporate taxes and then bag the windfall gains. Countries have tried to team up on them but it's hard to change.

I don't think Singapore will change (they are also the bankers for all the weird and wonderful regimes in Asia).

NZ govt needs to play hardball with the corporates. Or failing that, do something radical and be like Singapore and Ireland. Although I don't think Australia would accept that.

Be like Singapore. With those types of companies setting up shop, we attract HQ personnel from overseas to live here and retain our HQ citizens. Just one of many positive examples.

Then you will also need to offer low personal income tax rates like Singapore (and no capital gains tax). Top tax rate in Singapore is 24% and it kicks in at NZ$1.26 million a year.

And you'll also need the government to offer cheap housing for citizens like it does in Singapore. They don't need to worry about capital gains tax because it's the government that owns most of the housing.

These are the topics that need to make the news as non tax paying corporates are contributing to the erosion of our standard of living.

someone has to pay form 0.8% cashback rewards

Put gst on financial services.

Mastercard and Visa interchange fees comprise about $600 million, or 59%, of these merchant service fees paid by NZ businesses to banks for accepting Mastercard and Visa card payments.

Are these fees part of our national GDP calculation similar to the US or considered overhead and deducted as a cost of production?

You will be bleed dry and you will be happy to have them do it. People hate the idea of paying and extra percentage of tax on anything but quite happily allow these companies to intercede and get paid handsomely for it while paying no tax themselves here .

Almost none of the regulated "interchange" fee, which is the biggest component of the merchant fee, goes to Visa and Mastercard. The Singapore based schemes make very little profit out of card fees. This is because the Visa/MC networks just act like a switch to collect fees for the benefit of the issuer of the card used for any transaction. And almost all cards in NZ are issued by the big banks. That's where the fees are going (and profits).

if a retailer accepts a card issued to a customer by, say, Westpac, then Westpac is getting almost all of the fee paid by the merchant. All the issuers in NZ set these fees at the maximum allowed by regulation.

It's a fair point, but the cut for Visa/Mastercard/etc. is not insignificant

If you look at Visa's financials, they had a total payments volume of $12 T in 2023, and total revenue of $32 B, which comes out to a crude rate of 0.2% of payments volume worldwide. Though instead of looking at total revenue, you could argue that the data processing revenue of $16 B is a better fit, bringing it down to 0.1%

However those numbers are worldwide, in the EU card interchange fees are capped at 0.2% for debit cards and 0.3% for credit cards. So it would be interesting to see what the numbers break down to in a NZ context, but I don't think it will ever be clear due to the accounting used.

While the banks do take a lot of the cut, I believe that they are the ones that carry the risk with things like the fraud guarantees, and a certain amount is passed back to the consumer with rewards cards.

One should remember it was the Commerce Commission that said the Visa and MC COULD NOT prevent retailers from charging a fee for using the card. Prior to that in NZ Visa and MC prohibited retailers from imposing a charge for card use.

Pretty sure the UK outlawed this a couple of years back

Same with Afterpay. Currently its a condition of their contract with merchants that retailers cant surcharge for Afterpay payments. Various regulatory entities in NZ/Australia are trying to prevent that, so consumers will be forced to pay surcharges for BNPL choices.

Visa and MC always charged the mercant the fee, what changed is that the CC said merchants are allowed to pass on the fee. So people paying with eftpos aren't subsidising those with high rewards platnim credit cards.

Hoping open banking will improve this. Certified bank to bank payments with a QR code or similar.

As a former retailer , i never use contactless , aware of the extra charges on the retailer. its a few seconds more to enter your details.

Claiming consumers have choice is technically correct only.

Banks have been cunningly trying to get rid of EFTPOS for years. Step by step.

Yesterday I came across a parking machine which accepted paywave only. Which I did not have. Aaaagh.

It's time we put on our trousers (or big girl pants) and taxed every revenue in New Zealand. Singapore is laughing at us.

It is crazy they can earn income in NZ and not pay a cent of tax on it. Needs to stop. Something simple like 1-2% of revenue, or normal company tax rate, whichever is higher. Will mean we get at least some tax on those companies that transfer the profit to other jurisdictions

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.