The rush for ever-shorter fixed rate mortgage terms has continued in earnest.

Latest monthly figures - these for April - show that some 73.6% of the new mortgage money taken out by owner-occupiers (including on floating rates) was fixed for a year or a shorter term.

This continues the stampede to shorter fixed rate terms that started at the beginning of the year and has only picked up pace since. People are picking that interest rates will go down sooner rather than later. Are they going to be disappointed? (Spoiler alert: The Reserve Bank's suggesting that they might be.)

The Reserve Bank (RBNZ) introduced the C71 data series, which details mortgages as they are actually drawn down and for what terms they are fixed for last year. It only goes back as far as 2021, but offers interesting insight into what the borrowers are thinking - and also shows to some extent what offers the banks have been pushing at various times.

In April 2024 owner-occupiers took out $4.683 billion worth of mortgages.

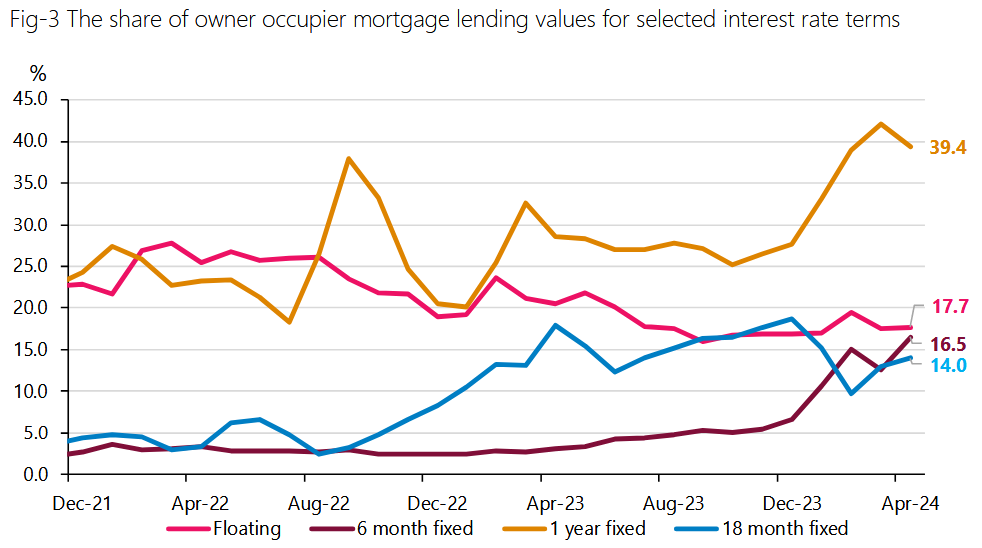

A stand out in those April figures is the fact that the amount of mortgage money fixed by owner-occupiers for just a six month term has hit a new high (albeit in a short-run data series, just three years) of 16.5%. Till this year the six-month terms have hardly featured as something the owner-occupiers have considered.

One-year fixed terms are still much the most popular term of owner occupier lending, accounting for 39.4% of the owner-occupier total, down from 42.1% in March.

But if short is hot long is not. It is getting colder and colder. As the RBNZ says in its summary of the highlights, the share of owner occupier lending on fixed terms above 18-month fixed terms decreased or held steady – with some at or close to historical lows.

"For example, the share of two-year fixed decreased to 8.6% from 10.2%, and the share of three-year fixed terms decreased to 2.8% from 3.3% - both are at historical lows. The four-year fixed terms held steady and are at a historical low at 0.3%.

There's an interesting point to make at this stage:

The fact that the latest figures highlight mortgages that were drawn down in April of this year means that the decisions on what term to take were all made well before the latest Reserve Bank Official Cash Rate decision and Monetary Policy Statement release on May 22.

That's important to bear in mind because prior to the RBNZ's latest OCR decision the wholesale interest rate markets had been fairly aggressively betting on rate cuts sooner rather than later, with the market pricing in a first OCR cut by October of this year and a fair chance of two cuts by November. Such a scenario would of course see likely significant falls in mortgage interest rates well before Christmas.

But the RBNZ's statements on May 22 were much more 'hawkish' than had been expected, with the central bank pushing back the expected time of a first cut to the OCR (currently on 5.5%) to the second half of next year.

If everything turns out as the RBNZ is currently forecasting then the hoped for mortgage cuts might not happen within the next year - certainly not in a meaningful way, so, maybe the 'go short' strategy might not pay off.

The wholesale interest rate markets ARE still pricing in an OCR cut in November, so the RBNZ's words don't necessarily take away the chance of earlier mortgage cuts. It will though be interesting to see if in the wake of the RBNZ's latest statements there is any change in the mortgage rate fixing strategies of the home buyers.

Separate figures earlier released by the RBNZ that lay out the county's entire mortgage stock and times to the next repricing show that as of April 2024 some 71% of the $262.4 billion of owner-occupier mortgages were either on floating rates or on fixed terms of a year or less. That's up from a comparative figure of just 59.4% as of April 2023 - demonstrating the extent to which homeowners have been 'going short' with their mortgages.

In means that homeowners will be very responsive to cuts in mortgage rates when they come (well, or for that matter, RISES if something untoward happened), with basically nearly three quarters of the owner-occupier mortgages due to be repriced in a year or less.

As said above, however, the RBNZ's dogged determination to get inflation under control, coupled with a desire to not see interest rates come down till it's good and ready, could yet frustrate homeowners.

Some quick details on the borrowing of investors:

The RBNZ says new residential investor mortgage lending rose to $1.48 billion in April 2024 from $1.336 billion in March.

For the investors, one-year fixed terms also continue to be the most popular, making up 45.0% of new lending, down from 45.7% in March-24.

The share of new residential investor lending on six-month fixed terms increased from 16.9% to 18.7% in April.

The share of three-year and four-year fixed terms decreased from 2.2% to 1.6% and from 0.3% to 0.1%, respectively. These figures at are historical lows.

28 Comments

The BEFU is picking end of 2024 for rates dropping, RBNZ picking end of 2025. Who do you believe?

I'd rather trust current market consensus, which is clearly expecting a first 25 bps cut in November.

The market has been pricing in a rate cut soon for a long time now. We were meant to have had 2 already this year.

And history will show we should have.

Inflation is sticky. Rates no doubt stable for 2024 unless a huge stock market crash / war occurs.. A lot of pain is out there with 71%+ at 1yr rates or more. Further pain to come. Plenty of opportunities on their way.. It's a shame that Grant Robertson and Adrian Orr lead so many people down this track.

I wonder how many people topped up their mortgage when interest rates were very low to buy a car, boat or overseas trip.

Now us and the rest of the world have realised low interest rates are not the norm.

All the recent stories about electric car sales plummeting are less to do with subsidies ending and far more to do with consumer inability to finance via mortgage top-up.

Hmm seems a big reason is the novelty has worn off. People have realized how much of a pain in the arse an EV is to have - charging etc. A reason Hybrids are doing well.

There aren't many second hand EVs so if you're looking to buy a car but can't afford new, your EV options are limited.

One way of addressing this is to put incentives in to encourage big corporates to electrify their fleet, which then has downstream effects a few years later when they hit the second hand market.

Can't say charging was ever an issue for the couple of years we had an EV. You plug it in at night when you get home, unplug it in the morning and drive away. No more complicated than charging your phone.

I can only guess the "etc" refers to range limitation, which is much less of a concern these days, and towing capacity, which is something that is less of an issue for most people than they think unless they're pulling a properly heavy trailer.

I note your implication that you got rid of your EV and no longer have one.

Yes Finance has dried up.. Or the test rates increasing have lowered peoples max limits. EV wise that was inevitable once the rebate disappeared, RUC's added, life expectancy unknown, diminishing value resale wise and the cherry on the top is the realisation that the carbon footprint for the life of an EV is close to an increasingly efficient ICE vehicle anyhow... Even more so when EV's are charged with Coal or Diesel generators.

…..and plus they are junk. Went away for a long weekend with some people that have them. Extension cords everywhere….ridiculous….and to stop for charging on a 200km trip before there were hills (range busters). Comical. People are finding this out now…which is why there is no secondary market for them.

Most households have multiple cars. Electric is a great option for the day to day car, with a petrol for the long distance trips.

I agree with on that. It is their niche. Inner city shopping trolly.

The 'niche' of nipping around towns and cities is likely the majority of vehicle journeys.

We just hire a car/van when we have long trips to do. Works out cheaper than a second car/van.

I'm not going to say EV's are the best option for all but they are a valid option for a large portion of households. Particularly to replace one of a 2 car household.

We changed our 2008 corolla into a 2018 leaf ~20k. Grid lock driving in auckland has never been so good for my commute. i have a 40km commute. We drive up to Orewa and back etc. Perfect.

We have an SUV that we use for longer trips and camping etc. But in an around auckland driving its a fight of who drives the leaf.

The issues seem to be around resale value, maintenance and the lack of any climate benefits.

Now that the govt added to the initial purchase cost and added RUC the value proposition makes no sense.

Plenty of low-use, 2 or 3 year-old boat/jetski/motorcycle/caravans on TradeMe at the moment

Most people have no idea about the event horizon and just go for the cheapest rate at the time it rolls over. If Kiwis were that smart they would still be on the 5 year at 3 point something percent and about only 2% of mortgage holders if that went this way.

The cheapest rates are currently long term not short term...

Yep. Im On 3% out to end of 2026. Right now with everyone on the high short term rates the banks have them right where they want them. If they push rates a little higher after some adverse inflation news or whatever people will panic and dive into a 3-5 year rate to get some certainty…..and that is exactly what the banks want. They will then begin to drop them after conditions allow and when they have a suitably large number of people locked in on high rates for long terms.

Interesting, I'm on 4.95% out to the end of 2026. How did you manage to get 3% for five years at the end of 2021?

Sorry. 3 range. Not actual 3, but still very low. I have also offset a few chunks now as well which I put on shorter terms, so my overall rate currently is 2 something which the larger fixed sum set to 3.x out to 2026.

Ah true, I do recall rates rising fairly quickly in 2021 while we were house hunting. Just checked the Int.co rate chart, and it was by about September that 5 year fixes hit the 4% mark, they had started climbing steadily from April.

We fixed 5 years for 3.05% in about March on a very small mortgage (our first home), the bank insisted we discharge that mortgage rather than carry it over, by the time we bought in December our rate landed at 4.95%.

hyperbole

June 20th (GDP) ... and we'll get a steer.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.