Two years ago, the average bank two year fixed rate was 2.51%.

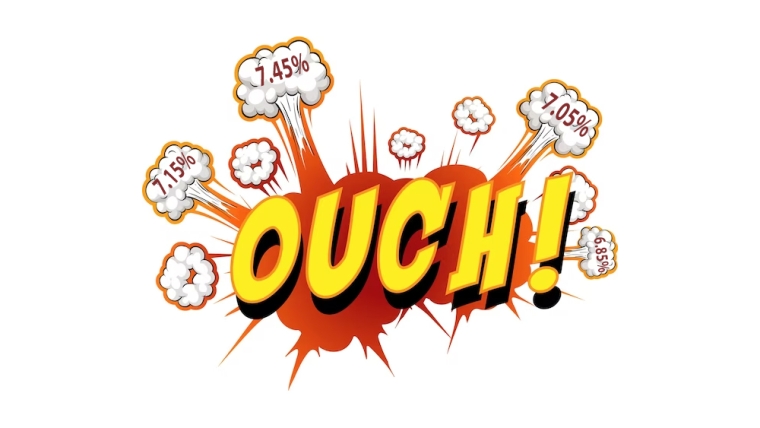

Today, Kiwibank raised its two year fixed rate by +10 bps to 6.99%.

This rise isn't a surprise, and may lead rises from other banks soon.

Update: BNZ has also raised rates for 18 month and 2 year fixed terms.

For a household with a $500,000 mortgage, that translates to a +$310 bite into the family budget, taking a $456/week repayment suddenly up to $766/week. For any borrower, that would sting.

Cafes, restaurants, concerts and even holidays are going to feel the downstream effects. It will probably mean the car upgrade will get put off too.

It isn't as though Kiwibank's rate rise is leading the market. Far from it. The new rates they announced today just catch up generally what their big-bank rivals are currently offering.

It is not the 'new higher rates' this week that are biting. It is the new higher rates over the past year that are now coming into effect for many.

For a household that took out a one year fixed rate a year ago, that rate was likely about 5.11% and for a $500,000 mortgage that translates to a +$152 bite into the family budget if you stay with Kiwibank. It will be a bigger bite from any other main bank because their current one year carded rates are higher. And may go higher from here.

Perhaps much longer rates could give some immediate relief because they could be as much as 100 bps lower. (Westpac has a 7.25% one year rate but a 6.25% five year rate, for example.) Yes, you may have a view that in five years home loan rates will be lower than they are now. But in the meantime, you will have avoided some family budget sticker shock and locked in a rate that you know you can live with. Just don't second-guess yourself.

Obviously you should negotiate and shop around. Most banks will discount their carded rates if you have strong financials. You shouldn't need them but if you are uncomfortable negotiating, a broker can often be helpful. But be aware some brokers won't offer you the best over the whole market, only the banks they have approved connections to in their "lending panel." And clearly bank mobile managers are there to pitch their company's own product.

One useful way to make sense of the changed home loan rates is to use our full-function mortgage calculator which is below. (Term deposit rates can be assessed using this calculator).

And if you already have a fixed term mortgage that is not up for renewal at this time, our break fee calculator may help you assess your options. But break fees should be minimal in a rising market.

Here is the updated snapshot of the lowest advertised fixed-term mortgage rates on offer from the key retail banks at the moment.

| Fixed, below 80% LVR | 6 mths | 1 yr | 18 mth | 2 yrs | 3 yrs | 4 yrs | 5 yrs |

| as at September 25, 2023 | % | % | % | % | % | % | % |

| ANZ | 7.09 | 7.25 | 7.04 | 6.99 | 6.69 | 7.09 | 7.09 |

| 7.45 | 7.45 | 7.15 | 7.05 | 6.85 | 6.75 | 6.69 | |

| 7.39 | 7.19 | 7.09 +0.14 |

6.99 +0.14 |

6.69 | 6.59 | 6.49 | |

| 7.25 +0.10 |

7.15 +0.16 |

6.99 +0.10 |

6.69 | 6.49 | 6.49 | ||

| 7.19 | 7.25 | 6.95 | 6.89 | 6.69 | 6.49 | 6.25 | |

| Bank of China | 6.99 | 6.89 | 6.79 | 6.59 | 6.39 | 6.29 | |

| China Construction Bank | 7.19 | 7.09 | 6.89 | 6.75 | 6.45 | 6.40 | 6.40 |

| Co-operative Bank | 7.19 +0.10 |

7.19 +0.10 |

6.95 | 6.79 | 6.49 | 6.49 | 6.49 |

| Heartland Bank | 6.69 | 6.69 | 6.59 | 6.45 | |||

| ICBC | 7.19 | 6.95 | 6.85 | 6.65 | 6.49 | 6.49 | 6.49 |

| |

7.39 | 7.25 | 7.04 | 6.89 | 6.69 | 6.59 | 6.69 |

| |

7.19 | 7.19 | 7.04 | 6.89 | 6.69 | 6.59 | 6.49 |

Fixed mortgage rates

Select chart tabs

Daily swap rates

Select chart tabs

Comprehensive Mortgage Calculator

139 Comments

And yet the commentators have the audacity to say the house market has bottomed.

The rates may have bottomed, the effects are only just beginning.

I guess some draw a distinction between the "housing market" and the "entire economy". They're inter-related, but what's facing us is more than a property market hiring the skids, it's the average persons' ability to afford anything, including houses.

I would argue that the vast sums of money to service a mortgage (or rent) has a significant part to play in the reason why the average person struggles to afford anything in this country.

Uh, sure. Over and above that though, if all anyone wants to see is housing, they might miss wider economic matters. Food and fuel's getting more expensive, while house values are flatlining (or slightly declining or improving based on what you read on the day). The mechanism being used to tame that, whilst likely impacting asset values, is going to have very serious negative financial ramifications for many people's lives. Disproportionately ones that don't own houses.

I guess maybe you have to break a few eggs, to make a schadenfreude omelette.

House values have been falling for 2 years but prior to this have been increasing almost exponentially for the best part of 4 decades, far outstripping wage growth, hence the worsening of the house price to income ratio. With the exception of some wildly volatile periods of oil shocks both fuel and food have been very stable compared to housing inflation.

They need to be held accountable for false propaganda

That's hilarious coming from Dgm

Feel better after laughing..?

Yep. Mind you, none of what the vested mouthpieces say can be construed as financial advise. They all quote that line daily.

TA 'ALWAYS' references his facts and figures to what his surveys say....covering his butt.

Get in quick, while you can afford to buy..... 😁

TTP

Geez, things getting desperate over there Tim?

When looking at any bubble chart there is always the small rebound of hope before the next leg lower...

Retail rates across the board will rise over the next few weeks. Read the tea leaves (swaps).

Higher for longer is starting to play out

Wait until Higher Forever starts to sink in

That would be a holocaust for the housing market

Just the return to a more balanced housing market. The stupid bit was the speculative bubble.

The stupid bit was pretending that living beyond means by consuming the wealth of following generations was a viable economic policy in the first place, rather than rewarding the value creators in society.

The interest rate is a tool from the US to rip off wealth all over the world. It has been using the tool for several rounds.

It obviously fails to rip wealth from emerging market this round then it will do it to developed markets/its allies.

It only works because the USD is the reserve currency.

the USD is reserve currency because companies globally create and settle their debts using it.

they do that because there is no better alternative.

there is no better alternative because the other major economies (China, India etc) do not have governments that can be trusted. If China had the reserve currency, I believe they would misuse that power more than the USA does... this is why the BRICS currency will never happen. The likes of Xi, Putin and Modi don't trust each other, and with good reason.

The Townhouse construction slump will continue to build. A stress test at 9% means a 500k mortgage over 30 years is circa 1k per week. And many potential FHBs would need a mortgage significantly higher than 500k for a townhouse, more like 600k.

9% is too low. Its should be a minimum of 2.5% above the mortgage lending rate, which means it should be 9.5%-9.75% now. Its 3% in Australia which would make it 10%-10.25% in NZ if the banks were doing their job properly.

Yep. So even worse

It won't just be a forward construction slump. So many of them currently on the market, it will be a sector-wide collapse of builder/investor capital.

I wouldn't be surprised to see overseas vulture capitalists move into NZ residential asset purchasing in a big way.

I'd far rather see high inflation as opposed to high mortgagee sales. Funny how we have a 1-3% inflation target band but no cost-of-borrowing target band. Those in the US are far more buffered from this shock as mortgage rates are for the life of the loan there.

I suspect, our populace don't fully comprehend how many households will suffer.

"I'd far rather see high inflation as opposed to high mortgagee sales"

High inflation results in reduced purchasing power for those on fixed income the most.

Those in retirement or nearing retirement would likely be impacted.

Those nearing retirement might choose to remain working due to cost of living increases.

If you want to learn about the impact of really high inflation - read about the extreme situations going on currently - Argentina, Zimbabwe, Venezuela, Lebanon, Turkey. Currently, Argentina has annual inflation of 125% p.a. See what high inflation does to the local residents.

Also look at those economies where inflation is in the 8-10% range such as the UK. Look at the lower socio-economic groups in NZ, and how they're being impacted with higher inflation.

The historical record is clear with the impact of higher inflation and its effect on the local residents.

How did the nation get itself into its current situation?

One single decision back in 2016 led to continue GDP growth and now we're facing the consequences of that policy decision.

If the then Finance Minister had allowed the RBNZ to implement debt to income ratios on bank lending back in 2016, then house prices would not have reached such extreme levels in 2021. As a result of that single decision, the nation is now in the current situation where a sufficient number of households took on debt levels that are now causing financial and mental stress. Unfortunately some will resort to self harm. The pain that is being felt among highly indebted borrowers is the unintended consequence of that single decision back in 2016.

As they say, the bigger the party, the larger the hangover.

Greed. The biggest winner is the banks owners.

"The biggest winner is the banks owners"

Avoid assessing bank profitability solely on the boom part of the cycle. Need to assess the banks over the entire economic cycle.

It's quite early on in the down cycle. Let's see how the bank loan losses play out over the down leg of the cycle. We'll get to see how their loan underwriting standards are.

Remember the commercial banks looked extremely profitable in the US, Europe up to early 2007. Then there was the downturn and many bank owners lost a large amount of their investment and in some cases they lost their entire investment - e.g Northern Rock (UK), Royal Bank of Scotland (UK), Washington Mutual (US), Citibank (US), Wachovia (US), UBS (Switzerland), Landsbanki (Iceland), Glitnir Bank (Iceland), Kaupthing (Iceland), Bank of Ireland (Ireland), Allied Irish Bank (Ireland), Anglo Irish Bank (Ireland), banks in Denmark, banks in Greece, banks in Cyprus, etc

Remember that in 1989 and 1990, the bank shareholders lost a large part of their investment in BNZ, and the BNZ needed recapitalisation twice.

Well put, and a solid reminder of why inflation should remain the key focus now irrespective of the pain. The sooner we drop it off, the sooner we can regroup, assess the damage and push forwards. The penny still hasn't dropped

What a load of dribble. Why do you consider the price of fuel and food increasing to be inflation, but the astronomical increase in house prices isnt?

Wonder if that finance minister had a conflict of interest in the form of a property portfolio?

The policy decision may have been politically motivated.

I.e - what did the then government need to do to keep the economy going in order to increse their chances of getting re-elected?

Debt to income limits may have an adverse unintended consequence on the economy and on house prices and decreased their chances of getting re-elected.

Hate the game, not the players.

Agreed. Inflation punished everyone especially the fixed income retired and low wage. It bails out the risk take speculator and their masters....the banks, at the expense of everyone else.

That type of really high inflation in failed states has more to do with currency collapse/no willing lenders. I don't see that happening in NZ. We are more in the UK type situation, only we never got quite as high as 8%, I don't think.

Those on fixed incomes in NZ - such as the retiree with no assets that you refer to - will suffer the cost of rent going through the roof with higher interest rates. That retiree can always get food from a food bank, clothes and shoes from a charity, but can't get shelter from the state with the SH waitlist in the mess it is. Rent is the biggest expense by far.

And the immigration tap is flowing thick and fast, putting further pressure on rents. I thought Q3 2023 would be the worst of it initially last year, It is looking more like 2024 to be the start of the real pain.

Whether inflation is the lesser of two evils depends on what else is happening.

If incomes are rising steadily, and asset prices (property, equities) are falling relative to inflation, then it could improve the long-term wealth of the young & working demographic.

But if wages are falling in real terms, and asset prices aren't falling enough to allow those workers (who are getting raises) to buy in, then inflation is a bail-out of asset holders at everyone's expense.

The UK inflation rate is currently 6.7%. Its been coming down faster than the NZ inflation rate.

Good points. I imagine National’s $2 million+ scheme would allow purchase of a whole development?

Kainga Ora is providing a Govt bailout for stressed developers, by agreeing to buy whole developments once built, and underwriting the build of new developments. This is why the new build market hasn't collapsed like it has in Australia.

Oh, well good on them. Are KO actually acquiring the assets - or simply picking up the rent?

Buying them. Which has the added benefit of bypassing all the pesky notification processes and presenting large social housing complexes as fait accompli to neighbours.

Isn’t there a fairly small cap on the total expenditure (maximum of $50 million total rings a bell). I might have that wrong. And regional areas prioritised?

.

No… they’re spending large. Contracts thoroughly scoped and open book…purchase price guaranteed… biggest risk is for developer to keep to schedule and manage costs as margins are slim.

That sounds good TBH. Building more state housing, and keeping the construction industry afloat, without offering excessive margins.

What's to stop overseas vulture capitalists purchasing 2 Million dollar and over properties and subdividing them an selling them off or renting them back to NZers?

The fact interest rates are still this high is a huge surprise to me. I really didn’t realise the NZ economy was this strong, I thought we’d be like the US during the GFC right now. Yet we still have very few forced sales and almost 3% growth, remarkable really.

Yes it is remarkable. With so much debt in the system, who would have thought the economy would be this resilient when mortgage rates go from 2.5% to 7% within 2 years.

It’s probably the product of two key things:

- All the covid stimulus

- Increases in interest rates taking time to work through the system

In terms of the latter - let’s see in 6 months when a large number of mortgages have finally rolled over to higher rates.

Don't forget savings rates. Some people went crazy spending over covid, others likely started tightening their belts.

Yeah

and I would also add wage rises. While they typically haven’t quite kept up with inflation, they haven’t been far off.

And of course there’s a large chunk of people who don’t have mortgages.

But let’s see 2024, lots of headwinds building (including likely significant bureaucracy lay offs)

Boomers paying large chucks of their millennial children's mortgages off perhaps? I've seen anecdotal evidence of this, would be interesting to know how much of this is going on....

If the boomers co-signed the mortgage and put up their own property as security then they might not have much choice.

I did exactly that. The offsprings pays me off interest free. It was a small mortgage, but not doing this would still have been disaster.

Best to keep the money in the family and not wasting it on the bank. No concerns re repayment in this case.

Add to that way less people being over-leveraged than spruikers claim (but those who are, oh boy!). And overleveraging to service speculative rental mortgages really doesn't have that much of an effect on the economy (unlike builds or business securities - though I'd be surprised if many businesses were over-leveraged).

And a cohort's retirement paving the way for younger workers to achieve higher pay (we're at the low point now before the late boomers head off - the next 8 years are going to be interesting).

"Two years ago, the average bank two year fixed rate was 2.51%."

Says it all really

We don’t have a choice. The RBNZ don’t set the rate really - it all comes from the federal reserve and the US treasuries which influence our market considerably.

Don't fight the fed.

That's a view that holds no water.

There are many countries that have far lower interest rates. And some that haven't needed to raise rates at all. And they have just as much exposure (or more) to the federal reserve and the US treasuries that we do.

If you were talking about "Americanized" countries you'd be closer to the mark.

Such views will ensure Kiwis just roll over and take up the .... We should be wiser than that.

All the countries with lower interest rates you are referring to (including Japan) have current account surplusses so are capable, as seen by the bond market, that they will pay off their debt. Check: Switzerland, Sweden, Ireland, Taiwan, Netherlands, Germany and so on......New Zealand with their one commodity, one customer approach is not seen as capable to pay of their debt.

Haha if we were wiser than that we wouldn't have created the mess in the first place or we would've learned from it 20 years ago.

Agreed. Perhaps the banks are suppressing action on people failing mortgage payments to avoid 1987. The longer it takes the bigger the mess will be.

They can't do that when the crap really hits the fan.

Remember economics is about human behaviour. Banks are doing all they can to prevent panic, as panic brings unpredictable and irrational behaviour that undermines the system.

People know if they get knocked out that's it for the rest of their life, and will do anything to avoid that. Mental health indicators will be on the rise. Please, focus on keeping your relationship healthy - failure to do so is a guaranteed worse life.

I really didn’t realise the NZ economy was this strong, I thought we’d be like the US during the GFC right now.

Interest rates are not rising because of 'economic strength'. They're rising because of inflation.

Yep I get that. But did you think interest rates could rise this much without the economy falling over? I didn't.

I didn’t either. But again, let’s reserve judgement and see how things look this time next year.

Will be interesting to see what the interest.co.nz predictions are like for next year! I think mine was one of the rosier ones last year and even I was way too pessimistic, I certainly didn't predict 3.2% GDP growth (I am sure that will be lower by the end of this year but still very positive). Maybe the DGMs will be right next year, haha

The economy won't fall over - it's people that will.

The people that took a mortgage without any interest rate buffer. Not that I blame them, we were told we had gone Japanese, interest rates would be low forever, etc.

Even the retail banks did not know. They were testing mortgages at 5.5% during 2021. Either they didn't know, or they were lending with malice.

Therefore as you say, it's not unreasonable to expect young first home buyers to be lead to believe they were making the right decision. Those who slate them for it are experts in hindsight.

Oh come on.

Lets not start with the "even the banks didn't know" crap. Of course they did! It's their damn job to look forward 10-20 years!

ASB’s CEO, Vittoria Shortt:

"We've been preparing for higher interest rates ever since we had record low interest rates."

In February 2021, ASB were testing at 6.45%. Six months later it was above 7.5%.

See figure 2.2. I stand slightly corrected, 2 out of 5 major banks were around 5 - 5.5%.

https://www.rbnz.govt.nz/-/media/project/sites/rbnz/files/publications/…

But yes, I am well aware the banks knew I was being facetious.

Figure 2.2 also shows that since late 2019, the bank stress tests were 7.0 - 7.5%.

Current 1 year mortgage rates are now above the lower end of that level (refer above table embedded). Some borrowers may have locked in for longer periods. However those that have only locked in for 1 year periods might be facing cashflow stress.

If you look at 2021, 2 of the banks had their test rates below the 6% mark. I'd had to do some Googling, but I recall at least one of the major banks was testing around the 5.5% mark according to some article.

Hard to foresee the need to buffer against a trebling. But that was more the banks job, than the borrowers - and, surprise surprise, the banks failed them.

"But that was more the banks job"

The banks / lenders are protecting their own financial interests (ie. reduce the risk of loan losses which impacts their capital, capital adequacy ratios, ability to stay in business) - the lenders assessment of the ability to borrowers to continue meeting debt service payments with higher stress test mortgage interest rates and a limit on loan to value ratios is a part of this process.

It is the borrower's personal responsibility to ensure that they could continue payments under ALL situations that they could face - such as increases in interest rates, reduced household income, loss of job, etc. Failure to do so, could result in cashflow stress and mental stress.

Most owner occupier buyers were so pre-occupied and focused on the successful purchase of their residential accommodation that they ignored / dismissed / overlooked some of the potential risks. Here was one such very public warning in February 2021: - https://www.stuff.co.nz/national/politics/300238808/reserve-bank-govern…

In light of rapidly rising house prices in Feb 2021, borrowers may have chosen to dismiss / ignore / downplay these warnings.

Many owner occupiers were borrowing as much as the bank / lenders would lend to them or as much as mortgage brokers could get banks to lend to them (there is a huge self serving financial interest here).

The borrowers chose to borrow as much as the lenders offered to lend, however they could have chosen to borrow less than the maximum offered by lenders. I heard some borrowers chose to borrow much less than the maximum amount offered by a lender or maximum amount suggested by a mortgage broker. There were reports of mortgage brokers suggesting to borrowers to include non existent borders in their mortgage applications in order to boost the household income, and hence to increase their borrowing power, and pay a higher price for their house purchase. Mortgage brokers were gaming the lender's loan assessment criteria to earn their commission. These cases could come to light in future.

It is the borrower's personal responsibility to assess how much debt they can handle. People are free to choose, however they are not free to choose the consequences of their choice.

Desperate FHBs also had to look at what the Reserve Bank had done to pump property over COVID, and to the welfarism for property successive governments had run, and worry that if they didn't get in the same types of leaders would find some new way to further inflate property. I feel sorry for young FHB facing that type of narcissistic entitlement mentality from those in charge over the years and having to worry about getting locked out forever.

So you're saying the banks have no responsibility to assist their customers in prudent lending and that all responsibility falls on the borrower? That environment would really open the door to severe predatory lending practices.

I'll throw a hypothetical out there. Bank lends $600k @ 3% to household earning $200k. 2 years later household is earning $250k, but for whatever reason the banks are now charging 15% p.a. "because they can". Would that scenario be "borrower irresponsibility" in your eyes? If not, then where's the cut off point?

Perhaps we need nonrecourse mortgages.

I wouldn't go so far to say non-recourse, but maybe cap a loan's maximum interest rate to the test rate. Then you'll find the banks might take their test rate settings a little more seriously.

Limit the amount of debt a borrower can take via a debt to income ratio limit.

This prevents borrowers taking on too much debt.

Agreed. Banks should take responsibility for their predictions. At present it seems like the average punter is expected to gamble on interest rates years out in the future, as if they're better equipped to do so than the bank.

Likewise, American-style fixed rate mortgages would help with that.

It does perplex me this whole tough love "personal responsibility" line that is rolled out to young borrowers. I mean, I get where people are coming from as the current set of rules lends itself to average punters needing to be responsible for the outcomes of their borrowing. But it doesn't have to be that way, unless everyone defaults to being defeatist and pointing the finger at the average punter instead of the banks.

Interesting there's all this talk about bringing in protections for gullible people from scams, mainly older people of course. Doesn't personal responsibility apply to older people?

Personal responsibility applies to the younger and poorer. The older and wealthier must generally be bailed out.

See: South Canterbury Finance investors, property owners in a flood, farmers facing flood or drought or disease outbreaks, businesses needing new equipment, businesses flooded and needing cleanup, property sector when a pandemic hits.

Do you know who invented the term “personal responsibility”?

The tobacco companies. Need I say more…

If people choose to reduce the chances of financial stress then they should do their own risk assessment.

Those who choose to outsource that risk assessment to their lenders are unknowingly increasing the chance of financial stress and can become potential collateral damage. Look at the lessons from the GFC of highly leveraged borrowers in the US, Spain, etc, as well as Japan in the 1990's and other instances in history. Those who choose to ignore the lessons of history are doomed to repeat them.

Financial literacy is poor in most developed countries. Those that are financially illiterate are at higher risk of facing financial challenges due to use of a decision making framework that may lead to outcomes that are undesirable.

People are free to choose, however they are not free to choose the consequences of their choice.

We outsource a lot of risk, why should financial lenders be any different? What do we need the Consumer Guarantees Act for? Are people too stupid to know a cheap fridge might not last more than 12 months?

Imagine if the insurance companies decided to push risk back on to you? "Sorry to hear about the house fire. Yup, we can see the electrician was registered and qualified, but your claim is denied. Electrical illiteracy is not an excuse, you should have known a 10 amp cable can't be used to power an electric oven".

"We outsource a lot of risk, why should financial lenders be any different?"

Feel free to change the current rule of law, current terms and conditions of contracts and other current conditions.

In the meantime, people should choose to operate under current conditions, and if conditions change, then adapt accordingly.

Not only do young people need to study macroeconomics outside of their full time work, family life and other hobbies, but now they must study law? All to buy their first home, because those actually making money from the whole racket are making potentially malicious calls on their approvals?

I agree with what you're saying though, but I don't agree with this whole "defeatest" stance of blaming David rather than Goliath. Maybe these changes could be introduced alongside the changes to protect victims of scams.....

Sure, privatise the gains socialise the losses. You know how sick it is that home owners gladly accept the 40 years of capital gains as their own, despite it coming directly from the economy?

How is expecting the banks to apply their servicing test rates to the entire loan, and apply some prudent assessments around loan applications for their clients "socializing the losses"? Provide an example of where the taxpayer would pick up the tab if someone couldn't stretch themselves to borrow 10 x their income at record low interest rates?

Maybe 40 years of excessive capital gains wouldn't exist if our mortgage lending segment wasn't built off pushing the envelope further and further as cash rates fall?

If we were financially literate we wouldn't have turned homes into capital gains investments, we wouldn't have overblown debt markets and stupid crazy money creation.

The numbers didn't compute a long time ago. If the experts are too illiterate to understand this, what hope is there for the average citizen?

"I'll throw a hypothetical out there. Bank lends $600k @ 3% to household earning $200k. 2 years later household is earning $250k, but for whatever reason the banks are now charging 15% p.a. "because they can". Would that scenario be "borrower irresponsibility" in your eyes? If not, then where's the cut off point? "

Close relatives got themselves into an over indebted situation in the late 1980's / early 1990's and got caught out with rising interest rates. They lost their owner occupied house and other income generating agricultural property - they lost the lot. They were fortunate to live in a country with a social housing program and received social housing and social welfare payments. The parents had a lot of mental stress, whilst the father never really recovered psychologically. They were unable to rebuild financially. The parents died a few years later, and when they were buried, the children had to pay for their funeral costs (i.e their estate value was negative). That is the result of financial illiteracy. Now the follow up to that is one of the children is now aged 48, is financially conservative, manages personal finances responsibly - that person continues to rent in Auckland as they did not have access to the bank of mum and dad, or other siblings to jointly buy their owner occupied residence - they have insufficient borrowing power and will continue to rent.

CN - we do not have non-recourse loans. A person subjected to a mortgagee sale does not have their debt extinguished if the price achieved in the sale fails to match the borrowing. The borrowing/balance of debt remains with them.

A banks risk relates only to time to recover the outstanding debt.

"A banks risk relates only to time to recover the outstanding debt."

A bank would have unrecoverable amounts in the following situations where the borrower may have an unsecured debt outstanding to their lender (after sale of a house to repay the mortgage as the house is in negative equity):

1) Personal borrowers can file for personal bankruptcy

2) If a company borrower has insufficient assets to repay loans (and the shareholders choose to not inject any money into the company), the company can be liquidated. That is the purpose of a limited liability company for a company's shareholders. This assumes that shareholders have not given personal guarantees for the corporate loans.

3) Loan guarantors can file for personal bankruptcy

Here is one example from 2011 - https://www.stuff.co.nz/business/money/6051241/Property-Guru-declares-h…

Here is a guy who have been bankrupt 3 times - https://www.stuff.co.nz/business/128478872/how-thricebankrupt-property-…

A couple of other high profile loan losses for lenders

- Andrew Krukziener - https://www.odt.co.nz/business/property-developer-offers-350000-settle-…

- David Henderson - https://www.odt.co.nz/business/auckland-property-developer-declared-ban…

https://www.nzherald.co.nz/business/first-rise-in-bankruptcies-since-20…

"Hard to foresee the need to buffer against a trebling"

This assumption on mortgage interest rates is where many highly leveraged borrowers are going to get caught out.

As a result of this assumption, many house buyers of 2020- 2021 took on high levels of debt relative to their incomes, leaving insufficient buffers if mortgage interest rate levels rose significantly.

Here is the 20 year history of mortgage interest rates. In the 2008 period, mortgage interest rates rose to 9-10% levels.

https://www.rbnz.govt.nz/statistics/series/exchange-and-interest-rates/…

Its this resilience that is driving the theoretical neutral central bank interest rate higher globally. Which is driving the "higher for longer" narrative. If economies don't go into recession in the next year or two then the neutral rate will be permanently higher. Which is a good thing, as it gives central banks room to move when the next crisis hits, instead of being forced into ZIRP or NIRP.

I'm surprised too.

A possible answer is that households built up a good buffer through covid (when they couldn't spend) and while rates were low (thanks for nothing RBNZ).

That buffer will run out soon.

We've seen this in past recessions where many people were able to ride out the beginning but ultimately the buffer gets exhausted and things start breaking. (Listings with mortgagee in the text have started rising in the last few months.)

Another part of the answer is that covid cleaned out quite a few fragile businesses so they're no longer here to show up the impending raft of failures. Just look around many high street at the empty shops that have been empty since covid and you'll get a feel for this.

I expect this collapse is just delayed rather than not-going-to-happen.

The outright lying by the media to drive 'sentiment' is discrediting any 'positive' notions in the market.

Many (including myself) more likely to spit on a real estate spruiker than ask them a question.

House prices are not dropping fast simply because we are importing so many labourers and fruit pickers and stacking them into rentals - keeping demand just high enough.

If we slow the immigration rate, or if national fails to win, or if a national led coalition cannot agree on policies needed to keep deman high? then we may see the house of cards start to collapse. Most other sectors of the economy are wobbling.

And banks have offered stressed households extended loan terms, or interest only to make it through this tough period.. or push out the day of reckoning...

For those borrowers who are seeking financial hardship assistance from their lender and these banks are allowing these borrowers to go on interest only payments - how long do the banks allow the borrower to remain on interest only before the borrower has to revert back to P&I payments?

The banks don't really care that much.

They are really only interested in the interest portion of a P&I loan in the first place.

And going interest-only increases the total amount of interest paid to the bank so they're actually quite happy about that. That's what their stress testing is all about, i.e. can this borrower continue to pay interest-only if they can't extend the loan term. Note they're quite happy to extend loan terms as, once again, the total interest is higher.

But the RBNZ does care. They don't want banks carrying lots of interest only loans as things can get risky - both financially and politically. An interest-only loan is akin to charging 'rent'. Whereas a P&I loan pretends to be helping the person buy something.

Those ifs seem unlikely. National will win, NZF may be a handbrake but didn’t do much to limit immigration last time. Public toilets might be in for a shake up.

The Aussie cartel ASB,BNZ,Westpac,ANZ are just getting greedier and greedier.

Very sad for kiwis that this cartel is allowed to control the NZ property market.

Let me fix that for you ...

"Very sad for kiwis that this cartel is allowed to control the lives of so many kiwis."

It is simple! GDP is driven by government spending (both import as well as export revenue decreased strongly compared with August last year so the private sector economy is in the doldrums). The increase in government spending is driven by taking on more debt leading to higher yields at the Treasury bond auctions. So an increase in GDP can lead to higher rates for longer!

Petrol prices aren't helping either!

https://www.nzherald.co.nz/business/petrol-prices-oil-price-surge-makin…

“I’m sort of nervous that it continues to climb, and it climbs back over that US$100 mark,” Z Energy general manager of retail Andy Baird told Markets with Madison.

Higher fuel prices were hurting demand “quite substantially” across its 289 stations, Baird said.

Seems crazy that oil prices are going up though: https://www.drivencarguide.co.nz/news/study-evs-could-capture-up-to-86-…

Petrol prices are for sure nasty at the moment (and it seems more upside to come). Seems to be around Chch over the past few days the price for 91 at 'normal' stations - i.e. manned ones with the shop, as opposed to self-service discount stations - is sitting over $3 per liter. Was up in the lower North Island late last week and saw a few $3.10-3.15 per liter for 91.

Personally I hope they keep going up, but I can't understand why they would when demand is going to fall dramatically in the next few years. Maybe OPEC are trying to make as much as possible while they can, and less supply at a higher prices is the way to achieve that.

1. Russia needs to fund its war

2. The US needs to refill the SPR and OPEC are taking advantage of it

3. The northern hemisphere is going into winter with increased energy demand

So OPEC have cut supply to increase the price.

Don't expect petrol prices to fall below $3 ever again. Demand is still rising and production falling. You would do well to engineer your life to minimise petrol use.

Outside of whatever the impact is on things like the transport component of product pricing, $3+ P/L petrol isn't really affecting me that badly if I'm honest.

I have a enormously thirsty old 4x4 but that is only used very occasionally; one tank can last upwards of 4 months at this point. My normal car is a super frugal little hatch; I'm spending about $20 per week on petrol, as I bike mostly or even walk to some meetings now as I live centrally.

My wife's car/family wagon is a bit thirstier, but I'm hoping to replace that with an EV soon. However, even at current prices it's about $50 per week tops in petrol.

My primary concern is not the price of petrol per se but the concern that if it climbs too much further will it result in a recessionary scenario that flows through to wrecking my business. If 91 was $4 per litre it wouldn't massively affect my household budget, but I know many would not be able to tolerate that plus all the flow-on increases in other costs.

Oil prices fell from a high of $133.88 in June 2008 to a low of $39.09 in February 2009. Over the same time period, natural gas prices fell from $12.69 to $4.52. Link

OPEC or Saudi Arabia anticipates demand falling and cuts production. It has a decent record of being right. We will go back to normal pricing once the economic crash is over and and the US makes peace with BRICS and OPEC+.

$4/l 91 next year. Mark my words

Is that like the 10% interest rates we got this year?

Still 3 months to go.. no I don’t think we will get to 10%. That would be absolutely crippling to the nation.

Overheard at a bus stop ... "Petrol prices? Yeah! It a greenie conspiracy to save the planet. The elites are all over it."

While rising fuel prices are inflationary to consumers (suppliers just hike their prices) they are hugely anti-inflationary to people who must use their vehicles to get to their salary & wage jobs. Even more money sucked from pockets. The RBNZ will be forced to act early next year.

(I can hear NZ Inc creaking in the storm. When will branches breaks? And what branches will be first Retailers? Christmas will be awful for them.)

Lol is this why oil prices increasing? Saudi Arabia diversifying in the name of GDP growth?

https://www.telegraph.co.uk/football/2023/09/21/mohammed-bin-salman-mbs…

Z energy - weren't they all about a NZ brand, creating a competitive market blah blah... Instead they sold out to Ampol?

There are a lot of people who have fixed for one year in the belief that interest rates will be soon be lower. It will be a rude shock for them to find out they will be refixing at even higher rates next year.

Read the tea leaves ... NZ Inc will be broken soon and RBNZ will need to act.

What will they do? Pretty simple solution really ...

1. Introduce the Debt to Income Ratios they've been prevaricating about and then ...

2. Drop the OCR - possibly quite hard.

"Drop the OCR - possibly quite hard" will crash our exchange rate. They might find themselves in a can't win scenario.

Perhaps why the RBNZ has increased it's FX war chest?

And I'd also suggest the relationship between NZ's OCR and the FX rate is overstated.

Golly. Who'd want to be the next government!

Also, that war chest will have next to no long term effect. The FX market is just too large for lil' ol' RBNZ to be able to influence in that manner (what's $4B on a daily turnover of $70B - NZD being roughly 1% of the $7.5T traded daily).

For a household with a $500,000 mortgage, that translates to a +$310 bite into the family budget, taking a $456/week repayment suddenly up to $766/week. For any borrower, that would sting.

For those who are unaware, imagine an expense which might be say 30-40% of your household expense, increasing in one year by 67%. What would that do to your weekly / monthly cashflow? What would that do to your mental health?

plenty of tenants already in that boat.

I’ve got a good friend who purchased a house way beyond his means in 2021. It’s such a domino effect of a story.

A) His partners family retail business goes under. Losing $300 net per week for the household

B) The bank of mum and dad dries up and the weekly top up payments cease

C) He’s in a sales role in construction. Things are tight in this sector no pay rises for over a year

D) The cost of living

E) and the final dagger. Rolling off a 3% interest rate early next year

Ouch.

no pay rise and probably no bonus?

Tell them to pack up his shit, rent the house out and shift to Aus. Get a FIFO job that pays well and then you also have no living expenses while your on swing.

On your off week just stay in a hostel or go find somewhere short term to stay for cheap.

Working well for me and there is no reason to be on less than $40 an hour over here.

I am picking $4 98 by the end of the year and oil over $100USD. Oil goes into everything and inflation will continue to rise. Interest rates will continue to rise to fight the oil price induced inflation. OCR over 6% by Jan 2024. I’m so glad I locked 3 years 6m ago at 5.99%

Why are we still doing this to ourselves?

What a shambles

Wait for Chippy’s final statement as he walks out the door defeated come election result:

“Joke’s on you Luxon, no backsies!”

Reminder that this is what the Dec 2021 Property Focus by ANZ stated at the time:

1) peak inflation of 5.8%

2) peak OCR of 2.0%

3) peak 1 year mortgage interest rate of 4.0%

https://www.anz.co.nz/about-us/economic-markets-research/property-focus/

Highly leveraged house buyers of 2020-2021 may have assumed a worst case 1 year mortgage interest rate of 4.0% (or 5.5% mortgage stress test rates used by lenders in their loan applications).

As we now know, economic conditions changed dramatically and the peak 1 year mortgage interest rate rose well above 4.0%. Currently for the big 5 banks in NZ, standard 1 year mortgage interest rates are above 7.0% as can be seen in the table above.

We sold our last house project about 3 months ago and are kicking ourselves for not getting that done 6 months earlier. Currently have that money in the bank and are renting which is making economic sense but not loving not having a permanent home and also not loving the dearth of interesting properties on the market.

Trying to be patient. Lots of talk in the media that the market has bottomed yet common sense suggests to me that it will start falling again due to ever rising interest rates and ever slowing economy. Property prices are not rising but they don't really seem to be falling either. Is every potential seller trying to ride it out? When will there be more property on the market and when will be the right time to buy?

I guess if I could answer this I would be seriously wealthy by now.

Not a single person in this comment thread has asked the most relevant question, which is “why exactly do the banks have to charge 7% on loans?

The current OCR is 5.5%, so I guess the lazy option would be for the banks to store all of their cash as Settlement Cash at the RBNZ to get a similar return.

Net interest margins seems to be about 2% getting us to around the 7% figure.

But it seems to me that the OCR is completely arbitrary and has nothing to do with inflation.

People don’t borrow money to pay for their fuel or groceries.

Charging businesses more on their loans will just flow through to the cost of those same goods, INCREASING inflation.

People are already massively suffering having had to pay stupid prices just to get a house, and to add to this with more interest cost just seems cruel when those interest rates make stuff all difference to inflation rates in the real economy as far as I can tell.

The whole system just seems moronic, but if someone has a better understanding of how its meant to work I am all ears.

https://www.rbnz.govt.nz/hub/publications/bulletin/2023/-/media/project…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.