New Zealand's biggest mortgage lenders are now stress testing mortgage applicants at interest rates nearer 9% than 8%.

Banks use test rates to assess would-be borrowers’ capacity to meet repayment requirements if interest rates rise.

ANZ NZ's test rate, or what it calls its servicing sensitivity rate (SSR), is now 8.60%. ANZ is the country's biggest mortgage lender with lending exposure of $102.566 billion as of December 31.

"ANZ’s SSR is currently sitting at 8.60%. The SSR is regularly reviewed to ensure it remains responsible and reflects the current interest rate environment," an ANZ NZ spokeswoman told interest.co.nz.

ASB, the country's second biggest mortgage lender, has an even higher mortgage serviceability test rate.

"Our current servicing test rate is 8.75%," an ASB spokeswoman says.

"Test rates are set to ensure customers have room in their current budget to make larger repayments if interest rates rise. We consider a range of factors when setting a test rate, including current and forecast economic conditions, current home loan interest rates, and how interest rates may change across a longer time-period or economic cycle."

That ASB test rate is up 25 basis points since mid-February when the bank's CEO, Vittoria Shortt, said it was 8.50%.

Westpac adds 2.5%

As its mortgage serviceability test for new borrowers Westpac, NZ's third biggest mortgage lender, adds 2.5% to its interest rates at the time a loan is taken out.

“Like other banks we run a stress test and price in a buffer to our mortgage offers, so that if interest rates rise customers can continue to manage their finances. The main relevant test right now is that we’re adding 2.5% to retail rates and seeing if that can be serviced. For example, someone applying for a loan at our Choices fixed two-year special rate of 6.54% would have their servicing tested at 9.04%,” a Westpac spokesman says.

As of December 31, Westpac had home loan exposures of $64.902 billion.

A BNZ spokesman says BNZ's mortgage serviceability test rate is 8.50%.

"We regularly evaluate this rate to ensure all lending is appropriate and delivering the right outcomes for our customers. An OCR change may lead to a reassessment of the test rate," the BNZ spokesman says.

BNZ, the country's fourth biggest mortgage lender, had loan exposure of $55.629 billion as of December 31. Between them the big four banks held residential mortgages of $296.384 billion, or 88%, of the total $337.758 billion of outstanding loans, according to Reserve Bank data as of December 31 last year.

RBNZ wants current lending rates maintained

On Wednesday the Reserve Bank (RBNZ) increased the Official Cash Rate (OCR) by 50 basis points to 5.25%. With Consumers Price Index inflation above 7%, the highest it has been in more than 30 years, and the RBNZ targeting inflation of between 1% and 3%, it has now increased the OCR by 500 basis points since a low of 0.25% between March 2020 and October 2021.

The RBNZ says the OCR needs to be at a level that will reduce inflation and inflation expectations to within its target range over the medium term. Maintaining the current level of lending rates for households and businesses is necessary to achieve this, the RBNZ says.

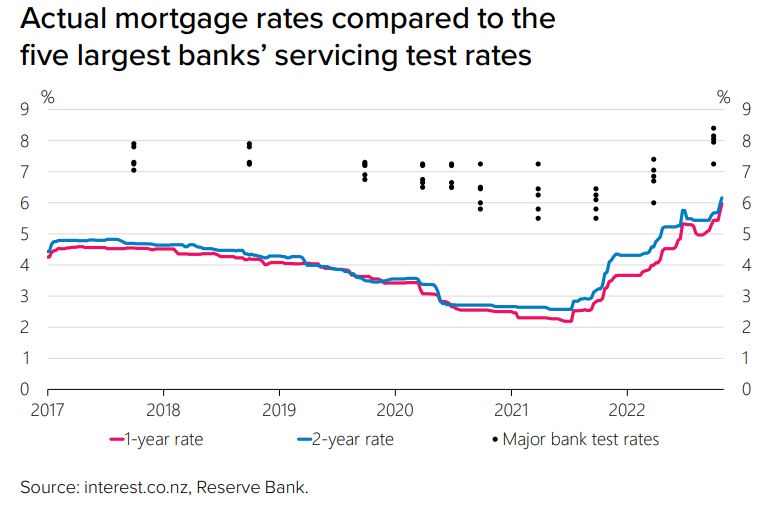

The average two-year bank mortgage rate is currently 6.443%, down slightly from 6.582% in late January. In mid-2021 it was as low as 2.524%.

Eyes on 2021 borrowers

Last May the RBNZ warned that, if home loan interest rates rose as it expected, a significant number of people who borrowed for the first time in 2021 could find it difficult to pay their mortgages and cover their other expenses. At that stage the RBNZ's OCR projection saw a peak of 3.9% in June this year, implying one-year and two-year fixed mortgage rates would hit about 6% over the following 12 months.

"If mortgage rates rise as forecast, there is a risk that a noticeable number of households that borrowed for the first time in 2021 will find it difficult to pay their mortgages and cover all their other usual expenses. This is because a 6% mortgage rate is close to the level at which borrowers were tested [by banks] during the COVID-19 period. There is a risk that these borrowers will need to cut back spending by more than currently assumed to meet their higher debt-servicing costs," the RBNZ said in May 2022.

"During 2021, major banks tested new borrowers’ ability to service mortgages at interest rates of 5.5% to 6.5%. These test rates are used to assess customers’ maximum borrowing capacity, and most will borrow less than the maximum. Therefore, mortgage rates up to these levels should result in relatively few borrowers having difficulty paying their mortgages."

According to the New Zealand Banking Association, about 56,000 new home loans were taken out between July and December 2021 at an average size of $407,000.

The RBNZ's next six-monthly Financial Stability Report is due out on May 3, when it may provide an update on where it sees current mortgage rates versus banks' serviceability test rates during the low interest rate, surging house price period of 2020-2021.

Last October ANZ CEO Antonia Watson told interest.co.nz the lowest her bank had tested borrowers at for servicing sensitivity was 5.8%.

"There are rates higher than that now which I acknowledge. But there are other buffers built into the equation, although we are looking at that cohort that was tested at that rate very carefully," Watson said in October.

Watson said the 5.8% test rate was in place for about six months in 2021, "when people were getting home loans at 2.4%."

And last November BNZ CEO Dan Huggins told interest.co.nz BNZ's mortgage serviceability test rate had been 6.25% when the OCR was at 0.25%. At that stage BNZ was not seeing borrowers who took out loans in 2021 paying interest rates at levels above what they were tested at.

Fixed mortgage rates

Select chart tabs

82 Comments

I don't understand why the stress test rates were ever under 10% in the first place.

Well, maybe the stress test should be 20%, surely that is safer than 10% ?

30%, better be safe.

Stop pulling random numbers

Lol, that's the point.

Thats silly statement Mr Yvil

Haha, so 10 is fine, but 20 is silly LOL. How about 15, 12, 7, 17, 8 25 ??? Where the limit?

Setting the stress test at whatever the high water mark was in the past seems like a logical place unless theres some reason we can guarantee that they won't reach that point again.

So 22% it is then. But Argentina has had mortgage rates at 49%, so maybe there, just in case we get there. Plus a margin for safety, call it 60%?

96% annual inflation. And those figures are suspect. Hope Kirchener gets bowel cancer. And f?ck the Hippo oath

Stress testing around 9% = taking even more buyers out of the pool, and almost all FHB's.

Easy fix, drop the asking price.

Exactly, how to get that through those thick skulls

If you are desperate you will have no choice

For a period of time that is true. It will however result in continued downward pressure on prices which is what is ultimately required to allow FHBs in particular access to the housing market.

With the 8.5% test, DTIs not needed now, but they need to be ready when the time comes (next year), especially if National attempts to throw petrol back on the housing market.

Wonder what they're looking at for pumping the market and their portfolios this time around. Last time it was raiding the country's retirement funds and increasing demand side welfare subsidies.

In addition to backing off liberalising zoning, obviously. Already seem to be making noises on that at the mo.

Never want to miss a chance to live off the wealth of following generations...

yes the usual conservative protectionism and backward looking continuence with a dash of religion.

Just when you thought 2022 was a "bad" year for RE...

Just over the last few days, another 10% of RE agents might have decided to quit

It amazes me that suburban agencies in Auckland can have 50 or so agents. Come on guys, get a real job.

It amazes me that suburban agencies in Auckland can have 50 or so agents. Come on guys, get a real job

I think it's possibly a good time to be a REA if you have money saved and understand how to live within your means. If you require a regular salary, look elsewhere.

1. Less competition as other agents get disillusioned and leave the industry

2. More punters looking to cash in their chips and get out before prices go lower - an important psychological fear that can be addressed by the agent.

I take it by addressed you mean exploited.

I take it by addressed you mean exploited.

No I don't. If you are spooked that your house will sell a price for 40% less than what you think it's worth, then the REA can play a role in helping you accept the reality and possibly meet your expectations in terms of closing a sale that keeps your emotional state in check.

Banks now stress testing speculators at 8-9% on rollover while factoring in declining equity, tax actually being paid from cashflow vs being rinsed via interest on debt, and inflation exceeding return on debt.

"Banks now stress testing speculators at 8-9%"

Not just speculators, everyone is being stress tested at 8-9%, read the article above.

Read past the word "rollover".

Sounding good, well better, to me.

OK, "while factoring in declining equity, tax actually being paid from cashflow, and inflation exceeding return on debt". This still all applies to everyone, not just speculators

No, all of that doesn’t apply to owner occupiers, does it?

Of course it does.

"declining equity" check

"tax actually being paid from cashflow" check (even worse for FHB as there is no income)

"inflation exceeding return" check (also even worse for FHB as there is no income)

Have you started contributing to Interest?

‘Tax being paid from cashflow’?

And stop being so juvenile.

That's a no then

What about Debt to Income? Sure we don't have a legislated DTI ratio, but a bank is going to look more favorably on a FHB couple with a household DTI of 5 than an investor with a couple of rental properties at a DTI of 10+ each.

Exactly, leave it to the banks to determine who they lend to and on what terms. Better for the RBNZ to determine how much capital the banks require to avoid bail out and price for risk.

So when you go to 'rollover,' and suddenly find you don't meet the new lending conditions, even if you are still meeting your payments, then what?

Winters coming - time for the banks to cull those they see might not make it through the economic winter.

Indeed. May the margin calls begin. Show me the equity....

Investors are still not paying any extra tax on cashflow. That doesnt kick in until 2024. Up until then higher interest rates offset the lower deductible.

I have no sympathy for the Banks or speculators testing at 8-9% they both entered into the transactions with their eyes open. Both are part of the Housing Market problem.

It just gets worser and worser for RE Agents.....

And 9/10 of them drank the cool-aid. When commissions dry up, and you have to try to unload your portfolio (commission free, of course!) to pay the bills at Countdown, that's when it will get interesting.

Don’t worry “independent economist” Tony Alexander will be along shortly with another “it’s a great time to buy” article

It is a great time to buy now, and if it goes lower then it'll be an even better time to buy, but anyone that thinks they are clever enough to pick the bottom may just be disappointed, so buy now.

Cheers, Tony.

Sadly he crossed that metaphorical line a while ago......

Tony "The Comb" Alexander - I wonder who is still reading his spruiker articles, and actually taking them seriously?

Interestingly they raised the stress test rates while easing the CCCFA. We all know the consequences of adding vinegar and baking soda at the same time...

Surely the test rate banks use for borrowers should also be the minimum rate regulators stress test banks at. Borrowers should fail before banks in a rising rate environment.

Maybe the test rates should be the interest rate ceiling for the duration of the loan. Banks might be less blasé on how they're set.

If the bank wants to entice lending of $800k @ 2.5% fixed for 1 year and test the borrower at 5% then that's on them. They have a max 5% loan on their books. Sure, might screw with loan portability but hey if someone is desperate to switch they can sign a new loan document with the next bank.

Since the test rate is higher than the actual rate, banks can use it to decline a rollover even if you can meet the new interest rate payments (which will be lower than the test rate.)

Yes, since they took people on board, then they should be automatically rolling them over at the new rate (not the test rate) if they can meet that rate.

People need to remember that these people are not their friends.

Banks only apply test rates for new lending to determine you can afford to repay. Why would they apply a test rate for a rollover? I've never heard of anyone doing that.

They may well not allow interest only loans to continue being interest only (and why should they? Debt does need to be repaid, it's irresponsible lending to allow someone to keep an interest only loan ad infinitum, as there is much higher chance of negative equity)

Duration of the Loan, or duration of the fix?

If you mean of the loan, eg. 25/30 years, then expect the banks to insulate themselves from the risk by adding another 3 or 4 percent (or more) to their NIM They'll make record profits in good times, and then you'll all bitch like mad. And they will probably get predatory about calling in loans if interest rates rise and you go into negative equity.

Duration of the loan (25/30 years). Cool, the banks insulate themselves from risk by adding 3 - 4 percent, house prices drop as a result, people are borrowing less etc. Smaller principal amounts.

Sure, the banks will likely make a killing on a dollar in vs dollar out basis, but their headline profit dollars shouldn't change much?

Bad for FHB who can’t get a loan, bad for sellers who can’t find a buyer especially if they are forced to dropping their prices below their buying price.

And then no change for many of us who will just hold longer.

The simple solution is for prices to come down to meet the market.

I find it funny that all the talk of "meeting the market" only seems to apply when prices are on the way up. \

No mention of meeting the market, by the usual suspects, on the long decent to the bottom.

Since the stress test is an indicator of risk in the economy, what it is doing is also showing that the economy is becoming risker to 'live' in.

I wonder what has been causing that?

Debt not supported by income, and banks operating assets books not marked at true market price.

My million dollar question is why did they drop the stress test rates when the RB bank dropped the rates to their emergency low rates? That was only a temporary measure, so I can't understand why banks dropped their stress test rates when that occurred. Apparently some were stress testing people in the 5's and lows 6's during that time, and it caused house prices to explode. It would be fine if people could take out 30 year terms at these low rates, but the max term people can lock in the ultra low rates for was 5 years. Maybe 7 years if they were with the one bank that still had 7 years rates until a few years ago.

The answer to the million dollar question is the the million dollar plus bonuses and golden parachutes that bank executives receive by achieving their short term profit objectives, hoping that the whole pass the parcel doesn't blow up in their face before they've moved on. Classic principal-agent problems.

And competition. A bank that is prudent loses market share during a bubble. God our Reserve Bank is stupid.

Few will be borrowing, the market is rooted now. Very foolish RBNZ not allowing time for results as other CBs are. There will be bigger fallout from delayed pentup buying

If more service providers competing for customers then cool

I won't be surprised if Adrian realises his blunder and reverses the daimler

I'll be surprised if we don't get at least 2 more rate hikes this year.

Agreed, don’t fight the fed.

very DGM

Yes its getting interesting now that the RBNZ decided to drop another Atom-bomb

On the other hand the Australian market has picked up two months running. I have mentioned this several times but the AI troll HM keeps pouncing on it to loudly rubbish the data.

This article goes a step further. Just when you think its all over and out, the market confounds the experts.

https://www.oneroof.co.nz/news/43362

That article makes no logical sense. To suggest a high OCR will eventually reduce sales stock to the point that demand outstrips supply and pushes up prices is absurd and ignores economic fundamentals.

Gosh they are getting desperate in their spruikerism.

There’s so many holes in their arguments I could spend all morning dissecting them if I had the time or desire.

And the talent

Once again, an unprovoked troll.

And the, not, or the. Yes that's clear I was meaning you have the vast talent to dissect the whole article piece by piece. And you should to prove you can.

Yes a few people are hijacking and ruining this site with their incessant and silly comments.

Oneroof. Troll posts from the Troll cave on behalf of the VESTED. But go-ahead and leverage up some more. Untill you can't as not enough income not enough equity. NEINEE.

Sure sucks for the speculative as the market moves back to fundamentals.

NZ really needs to legislate to ensure advertisements are marked as such and cannot be passed off as news or articles like this

Have you seen how Trump casts himself as a victim. His troll behaviours are old and boring, to me he always was.

Unfortunately there are 30% of americans with low IQ and blind religious beliefs that support him.

Instead of stress testing new applicants, it would be interesting to know how many of the existing loan customers would get the same loan if they were stress tested again at this rate ? Are the Banks doing such exercise ? Or waiting for the borrowers to come to them with request for help if they can't meet payments ?

Who knows.

I went to the companies office the other day and looked at Westpac.

Not many New Zealand names there.

if the board doesn’t live in New Zealand how do they have a clue what’s going on at the bank?they don’t know any customers. The execs have been trained to make the numbers look good,and good they will look until the iceberg

If the intention is to reduce disposable income, and rein in inflation, isn't it possible to allow people to increase their kiwisaver contributions instead? Seems like you'd get the desired effect, and it wouldn't go towards lining the pockets of banks who aren't passing on the higher OCR fairly for those with term deposits.

The OCR policy aint definitively working to stem inflation yet. High rates didn't help during the 70s and 80s either

They did in the end. At the moment of course it has not had a meaningful impact. Interest rates need to be at lease 2% higher that the inflation rate. A rate that is currently printed around 7%, but is more likely around 10%.

Doing gradual OCR hikes is just fueling the wage and price spiral to the detrement of all.

At the moment of course it has not had a meaningful impact. Interest rates need to be at lease 2% higher that the inflation rate.

Where did this pearl of wisdom come from? I've been researching it and can find nobody reputable that's made any such claim.

If you are going for 5 years fixed and with a shorter term, e.g. 20 years - make sure the b'stards stress test you at the end of the term and not the beginning. Why? Because you'll have paid back much more capital. (Although why you'd fix long now is beyond me.)

Use this and you'll see what I mean. https://www.interest.co.nz/calculators/full-function-mortgage-calculator

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.