Here's my Top 10 links from around the Internet at 4 pm in association with NZ Mint.

I welcome your additions in the comments below or via email tobernard.hickey@interest.co.nz.

I'll pop the extras into the comment stream. See all previous Top 10s here.

Various cartoons are very disrepectful to Mr Silvio Berlusconi today...

1. 'Watch out below' - As the European financial system staggers on under the weight of enormous and unsustainable sovereign debt, banks are doing everything they can to offload the dreck, hopefully (for them) onto an unsuspecting (or just plain stupid or conflicted) central bank.

This is why Germany is so opposed to the European Central Bank buying these bonds.

The ECB is the crucial player here.

The only reason Italy is not already bankrupt is the the ECB has been buying bonds over the last five months.

The mere threat of the ECB stopping buying these bonds (on Sunday night) was enough to cause a revolt inside Silvio Berlusconi's government.

All this is going pear-shaped at a rapid rate.

Here's an idea of what's happening now under the covers of the bond markets via Bloomberg.

BNP Paribas SA and Commerzbank AG (CBK) are unloading sovereign bonds at a loss, leading European lenders in a government-debt flight that threatens to exacerbate the region’s crisis.

Banks are selling debt of southern European nations as investors punish companies with large holdings and regulators demand higher reserves to shoulder possible losses. The European Banking Authority is requiring lenders to boost capital by 106 billion euros after marking their government debt to market values. The trend may undermine European leaders’ efforts to lower borrowing costs for countries such as Greece and Italy, while generating larger writedowns and capital shortfalls.

“European regulators and leaders are shooting themselves in the foot because a big investor group for sovereign bonds has been taken out of the market,” said Otto Dichtl, a London-based credit analyst for financial companies at Knight Capital Europe Ltd. “The downward spiral will continue until policy makers find a back-up solution for the sovereigns.”

2. 'Eliminate the bonuses' - Nassim 'Black Swan' Taleb has written in the New York Times that bonuses for bankers should be eliminated.

Fair enough.

More than three years since the global financial crisis started, financial institutions are still blowing themselves up. The latest, MF Global, filed for bankruptcy protection last week after its chief executive, Jon S. Corzine, made risky investments in European bonds. So far, lenders and shareholders have been paying the price, not taxpayers. But it is only a matter of time before private risk-taking leads to another giant bailout like the ones the United States was forced to provide in 2008.

it’s time for a fundamental reform: Any person who works for a company that, regardless of its current financial health, would require a taxpayer-financed bailout if it failed, should not get a bonus, ever. In fact, all pay at systemically important financial institutions — big banks, but also some insurance companies and even huge hedge funds — should be strictly regulated.

Critics like the Occupy Wall Street demonstrators decry the bonus system for its lack of fairness and its contribution to widening inequality. But the greater problem is that it provides an incentive to take risks. The asymmetric nature of the bonus (an incentive for success without a corresponding disincentive for failure) causes hidden risks to accumulate in the financial system and become a catalyst for disaster. This violates the fundamental rules of capitalism; Adam Smith himself was wary of the effect of limiting liability, a bedrock principle of the modern corporation.

3. 'Let's not do that again' - Bryce Wilkinson writes at CapitalEconomics about the problems with New Zealand's Deposit Guarantee scheme. HT Eric Crampton.

Under-priced government guarantees for financial instruments potentially undermine the stability of the financial system by inducing excessive risk taking. The precedent created by the adopted scheme is very troubling in this respect.

The report considers the "necessary in the public interest" test and concludes that the scheme was justified because no run on the banks occurred, the economy was stabilised and some finance companies survived.

None of these reasons stacks up. First, the scheme cannot be given any credit for preventing the feared flight of deposits to Australia because under our freely-floating exchange rate regime the fear could never be realised. (Anyone wanting to exchange a New Zealand dollar asset for an Australian dollar asset must find a buyer for the New Zealand asset. As a result there can be no net outflow of funds from the banking system.)Second, credit for boosting confidence in the banks can be more readily attributed to the separate wholesale guarantee scheme since this scheme dealt directly to the real threat that the banks faced – the freezing up of the global wholesale market. Third, sound finance companies would plausibly have survived in the complete absence of a retail deposit scheme.

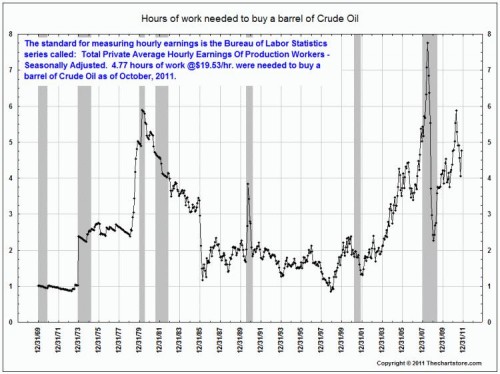

4. What inflation really looks like - Creditwritedowns points to an excellent chart showing the number of hours needed to buy a barrel of oil over the years going back to 1969.

The chart does illustrate how real wages whip around with the price of crude oil. As a rule of thumb one barrel of crude (42 gallons) produces around 20 gallons or about one tank of gasoline. So what took 2 hours of work to fill the tank 10 years ago now takes about 5 hours. Of course this is a simplification as other byproducts are produced from a barrel of crude, but it is does illustrate the point.

5. The problem with hot money - It goes cold very fast and destroys banks and brokers that rely on it even faster.

Investment banker and author William Cohan writes at Businessweek about the collapse of MF Global and how it should warrant the end of the hot overnight money that has kept investment banks afloat.

Oh and by the way New Zealand's banks rely on foreign hot money (matures in less than 90 days) for about NZ$63 billion (in NZ$ and non US$ terms from non-residents) or about 20% of fund.

Here's Cohan.

No self-respecting Wall Street banker would ever advise a client to personally take such short-term financing risks. And yet the industry itself was doing this very thing.That’s what makes the MF Global debacle so shocking. Jon Corzine, the firm’s former chairman and chief executive officer, had previously been CEO and CFO of Goldman Sachs. He understood exactly the fragile short-term funding dynamic of a securities firm.

His principal financial sponsor, the billionaire J. Christopher Flowers -- one of MF Global’s largest shareholders who installed Corzine as CEO in 2010 -- was a former financial institutions banker at Goldman Sachs.

Flowers made his fortune by buying and turning around a distressed Japanese bank. He also had a seat at the table during the collapses of Bear Stearns, Merrill and the rescue of American International Group Inc. Flowers knew exactly how fragile short-term funding could be. And yet both he and Corzine allowed MF Global to take the risk of financing a long-term bet -- its $6.3 billion gamble on European sovereign debt -- in the short-term markets.

6. And you guessed it - The Telegraph reports staff at MF Global were paid bonuses just hours before it went bankrupt...

Sigh. See #2 above and number #5.

7. Want a free BMW? - The FT reports one Chinese property developer has taken to spruiking his unsellable new apartments by offering a 'free' BMW to the 'lucky' first buyer of an apartment in his block.

My favourite line is the last quote:

The deal is a sign of the desperation felt by developers in China’s once-booming property market, which has been pounded by government measures aimed at heading off a bubble. The slowdown is a matter of international concern, with Chinese house construction driving demand for commodities and propping up growth in the sputtering global economy.

Chinese developers have been reluctant to cut prices as transactions have slowed this year, but some are finally capitulating after dreadful sales in October. Others, afraid of the stigma of slashing prices, are offering giveaways such as extra garden plots, Louis Vuitton handbags, cruise vacations and now cars.

“Whoever signs a contract and makes the downpayment will be able to drive away in a BMW,” said the sales assistant at Central Mansions, a cluster of brown towers with 868 apartments that have just come on to the Wenzhou market.

“No, it doesn’t mean that sales are bad. It’s just that we’re trying to attract customers,” she said.

8. Bankruptcy or hyper-inflation - Gold fan Eric Sprott talks at a German precious metals conference about precious metals and the outlook for gold and silver.

He worries a lot about banks. It lasts 30 minutes, but a bracing alternative view to the usual smiling, waving, muddling and reassuring we get publicly from the powers-that-be.

Other discussion topics include the choices between austerity and increasing stimulus and how both will bring on a meltdown, whether bankruptcy or hyperinflation brought on by money printing. They talk about the huge leverage in the banking system and the risk inherent in the system. People are only now starting to understand counterparty risk. They explain that 20-to-1 and even higher leverage is common in the banking system. They talk about the disparities between the physical market and the paper silver markets.

Eric talks about supply and demand and how the upward pressures on silver price from demand growing much faster than supply are not being accurately reflected. A 900 million ounce silver supply simply cannot cope with a 380 million ounce increase in demand and maintain current prices. Eric also explains that investment sales of silver are 50 to 1 in volume compared to gold and that this means a decreasing gold/silver ratio.

Also under discussion is Sprott's analysis which shows that the US government, with a GDP of 15 trillion, has liabilities of almost 80 trillion and that these promises will be broken just as the Greek government is breaking its commitments.

9. Spain is next - Sean Egan from credit rater Egan Jones talks in a CNBC interview below about the problems with Spain's economy and its debts, and how Greece and Italy are just part of a bigger picture, including Spain. The good stuff starts about 4:30 HT Credit Writedowns.

Egan sees 90% haircuts in Greece, eventually. And he says that 6% is the point of no return. If you look at the debt crises in Greece, Ireland, and Portugal, once you hit 6%, the interest rate death spiral kicked in as insolvency was self-fulfilling.

That’s how it works when no lender of last resort steps in. It works the same way for financial institutions too. You wanna know why MF Global went under? There it is.

10. Totally irrelevant Jon Stewart interview with Clint Eastwood about J Edgar Hoover below...

But first here's lots of jokes about Herman Cain's ... ahem... love life:

And Clint Eastwood:

34 Comments

most alarming post ive read all week...........http://www.juancole.com/2011/11/godzilla-carbon-emissions-in-2010-unprecedented.html

FYI from CNN Money. Something for us to chew on here.

Older Americans are 47 times richer than young

According to analysis by the Pew Research Center released Monday, younger Americans have been left behind as the oldest generation has seen wealth surge since the mid-1980s.

While it's typical for older generations to hold more wealth than younger ones who've had less time to save, the gap between the two age groups has widened rapidly.

In 1984, households headed by people age 65 and older were worth just 10 times the median net worth of households headed by people 35 and younger.

But now that gap has widened to 47-to-one, marking the largest wealth gap ever recorded between the two age groups.

http://money.cnn.com/2011/11/07/news/economy/wealth_gap_age/index.htm

cheers

Bernard

Yet who is left to pick up the tab, and ponzi fund their retirement?

Bernard, you may find the original article worth looking at:

http://www.pewsocialtrends.org/2011/11/07/the-rising-age-gap-in-economi…

And perhaps then more accurately targetting your baby boomer bashing.

Good one Colin .. that's the trouble with the twitterati .. alert .. scan .. copy .. paste .. bang .. it must be true .. wonder if the BH will do a comment (fair and balanced) on this http://finance.yahoo.com/focus-retirement/article/113751/retirement-crisis-closes-baby-boomers-reuters?mod=fidelity-readytoretire&cat=fidelity_2010_getting_ready_to_retire

Thanks Inconoclast. A good suggestion, and an interesting link that covers ideas some of which could have been useful if Bernard had replied to my comment.

Before taking up your sggestion I would hope Bernard would first use the link below to establish that the first wave of catabolism had started in the US, the UK and likely NZ, by 1974 - a point at which half the baby boomers were still at school.

That being the case, the question is simply when to place the first wave of catabolism in America – the point at which crises bring a temporary end to business as usual, access to real wealth becomes a much more challenging thing for a large fraction of the population, and significant amounts of the national infrastructure are abandoned or stripped for salvage. It’s not a difficult question to answer, either.

The date in question is 1974.

http://www.energybulletin.net/stories/2011-01-20/onset-catabolic-collap…

I am not sure though that Bernard will want to put it all together. The conclusions may not go down well at TSY's next conference of journalists and economists.

Not many ppl have read stuff like this.....its viewpoint changing if you take it on.....lots of good pieces on youtube as well....

Who needs nightmare on elm street when you can read/watch pieces like that!

regards

Banks are offloading Italian bonds, what are they doing with the money? Parking it the ECB? Smart money would be selling now while it still has value, since the Euro Summit rendered void any form of insurance. I used to hear that 6% was unsustainable for italy, now its 7%, thats right up there with small business loans. Way more risky then housing.

Hence Gold at 1300 Euro / oz....

7.246% now.....6.5% 2 days ago? and 7.5% at one stage earlier (7amNZ) I assume someone ECB? stepped in and bought....cant sustain that, next is bank runs.....the graph is now looking vertical...

The f word comes to mind.....

http://www.bloomberg.com/apps/quote?ticker=GBTPGR10:IND

regards

Great piece here from Douglas Rushkoff here on the origin of the corporation (just the same as people says Mitt Romney) HT Vanderlei

http://hilobrow.com/2011/11/04/douglas-rushkoff/

Douglas Rushkoff: The corporation is the result of two innovations: the creation of centralized currency, and the creation of the chartered monopoly. In the late 1300s the upper classes — the aristocrats, the people who had been feudal lords — were becoming less wealthy relative to real people. As the merchant class and people in towns were producing and doing, the relative wealth of the aristocracy was going down, and this was a problem; the aristocrats wanted to continue the system that had been working for them for the last 500 years wherein they didn’t have to “do” anything to be rich. So they hit upon the idea of passively investing in other people’s industries.

Suppose I am the monarch. I want to make money through your shipping company; how do I get you to let me invest? Well, I use what power I have as a monarch to write up a charter, which means I give you a monopoly in a certain area, and you give me 30% of the shares in the company. The chosen merchant avoids competition and gains protection from bankruptcy, while the king receives loyalty, because the merchants’ monopolies are based on keeping him in power. He doesn’t mind if a few of the merchant class are as rich as he is, as long as he is able to get still richer as a result.

But this was not the promotion of free-market capitalism. It was the promotion of monopoly, non-market capitalism. It was locking into place a set of players and a set of systems that had nothing to do with the free market. And it changed the bias of these merchants away from innovation; in other words, from “how do I innovate and maintain my competitive edge” to “how do I extract wealth from the realm that I now control?”

China's gold demand is insatiable courtesy of Xinhua

The output in the first nine months of the year hit 259 tons, up 4.32 percent from a year ago, said Sun Zhaoxue, also the president of China National Gold Group Corp, at the China Mining Congress and Expo 2011 that concluded Tuesday in the northern coastal city of Tianjin.

The consumption, however, is estimated to hit 400 tons this year, a surge from 270 tons in 2010, Sun said. The purchase of gold bars is expected to nearly double to 270 tons amid safe-haven buying, he added.

http://www.chinadaily.com.cn/bizchina/2011-11/09/content_14063394.htm

ECB stymied on debt crisis without fiscal union Germany's top banker has vehemently rejected demands from David Cameron and other world leaders for drastic action by the European Central Bank to stop the eurozone crisis spiralling out of control. http://www.telegraph.co.uk/finance/financialcrisis/8877818/ECB-stymied-… When all this blew up in the US in 2007/08 and then edged its way into the eurozone, there was a time when I thought (naively) that Europe's political elites would come up with workable options for handling a deterioration of the euro crisis.

Some of us always knew that the trajectory of this crisis would be downwards (read my and many others' comments on these DT blogs for the past 3 years and more); the trajectory will continue downwards for a further decade.

Indeed, some astute observers reckon that we face unprecedented socio-economic change over the next 20 years, characterised by a trend of economic contraction, rather than economic growth. There is plenty of evidence to suggest that the overall trend over the next 20 years or so will indeed be one of economic contraction. The politicians, of course, will never admit this. No sizzle in election campaigns with the theme "Things Can Only Get Worse".

Needless to say, no signs whatsoever of Europe's political elites coming up with workable options for handling a deterioration of the euro crisis. In fact, the opposite is true. These guys are digging a black hole all the way though to the centre of our galaxy at the moment.

My money is now on the situation going dysfunctional and disorderly overnight. I don't have a date in the diary, but like all of these things, there'll be an "unforeseen" event, the timing of which will take everybody "by surprise".

The macro-economic problem will suddenly and shockingly transform into 500 million micro-economic problems - whence the likes of you and I will have started taking decisions to do things over which the politico-bureaucratic mafia in Brussels will have no control; no control whatsoever.

I reckon there must now be a real chance of a tidal wave of bank runs right across Europe as citizens' uncertainty and fear about where all this is heading in relation to their own assets becomes widespread panic. Already, the euro itself has been undermined by the very politicians who purport that the euro is forever, by hinting that a member of the Club could be cast adrift. When that happens - for happen it must if Greek society is not to turn in on itself violently - then it could be the "unforeseen" event that I mentioned.

This situation becomes more Alice in Wonderland by the day. It's now "them" and "us" - and it's all beginning to look very ugly.

Summary from Barclays Capital inst sales:

1) At this point, it seems Italy is now mathematically beyond point of no return

2) While reforms are necessary, in and of itself not be enough to prevent crisis

3) Reason? Simple math--growth and austerity not enough to offset cost of debt

4) On our ests, yields above 5.5% is inflection point where game is over

5) The danger:high rates reinforce stability concerns, leading to higher rates

6) and deeper conviction of a self sustaining credit event and eventual default

7) We think decisions at eurozone summit is step forward but EFSF not adequate

8) Time has run out--policy reforms not sufficient to break neg mkt dynamics

9) Investors do not have the patience to wait for austerity, growth to work

10) And rate of change in negatives not enuff to offset slow drip of positives

11) Conclusion: We think ECB needs to step up to the plate, print and buy bonds

12) At the moment ECB remains unwilling to be lender last resort on scale needed

13) But frankly will have hand forced by market given massive systemic risk

Hint:Not Good.Sell EUR, Buy Gold

http://www.zerohedge.com/news/barclays-says-italy-finished-mathematically-beyond-point-no-return

AndrewJ

Even with all of the new developments in Europe there is still not much sign that you will be able to buy a cheap farm. Even with inflation here officially at 3% the ECB just cut rates.

We now have an Italian as head of the ECB and Germany and France obviously want the ECB to support the banking system. The ECB recently announced more covered bond purchases - ie more mortgage support.

Weidmann talks with a forked tongue. He does not want countries to be bailed out but the banks are getting unlimited liquidity - ie the banking system as a whole can convert assets to cash in an unlimited manner at the ECB. There will be nationalisations but nationalised banks just act to create more loans as the governments bad banks which then support the other banks. Ultimately they are going to monetize. The show will probably be still running by the time we are very old men.....going nowhere fast with rising prices.

Nations come and governments go - but what always remains is the bank.

Moraymint is a respected and highly recommended poster on Telegraph blogs. His comments are on the money and so are many others.

Moraymint

You are right there will come that " Archduke Franz Ferdinand" moment. More than likely it will something so small and seemingly insignificant but it will be enough to set the whole thing going.

You would have to be extremely naive to think that this whole crisis won't end in large scale social unrest.

George Osborne's priority now is to examine ways by which he can safeguard as much as possible the UK'S finances. Not an easy job but damage limitation is now the name of the game

re #6

Andrew Abraham

The below is a letter that was sent to Senators & Congressmen..

Dear

Congressman

I am writing to you to ask for your immediate help and

intervention to ensure the integrity of the US Financial markets in lieu of the

MF Global debacle. The integrity of the markets are at stake as well as the

integrity of the USA in the eyes of the financial world.

Segregated

client accounts of MF Global are missing upwards of $600 million USD. This

money just does not disappear or then according to news reports show up at JP

Morgan and then to disappear once again. JP

Morgan was a custodial bank for MF Global. JP Morgan had repurchase agreements

with MF Global. Were funds sequestered from MF Global Clients by JP

Morgan to make up in short falls? Does the US Financial system allow stealing

of segregated funds at one institution by another?

These segregated accounts are no different than personal or

corporate bank accounts or even stock market accounts. These accounts were

(possibly) violated and a large amount of assets are missing.

What

is worse is the violation of the

Commodity Exchange Act, which states that in the event of a FCM bankruptcy

client funds are to be handled separately from the firm assets and given priority. It is questionable what transpired,

however 50,000 customer accounts have been frozen and hundreds of millions of

dollars are unaccounted for. The analogy is very simple. It is as if a bank

makes bad loans and then pillages their customer’s accounts to remedy the

situation or if a Stock brokerage company makes bad investments and then

withdraws monies from their client’s accounts. If this is allowed to continue

there will be NO Trust in the markets. Nothing will be safe!

The implications are severe to farmers to hedgers of

virtually aspect of our human existence. This is not just a group of commodity

trading speculators. This is the basis of the US economy.

The fact is that the regulators were not regulating nor are

they acting now in order to protect the integrity of the financial markets. I

implore you to take a stand to protect the financial markets. I implore you to

1.Demand that the trustees of the MF Global release at least

partial of the frozen cash

2.Open immediately investigations of JP Morgan and how

segregated accounts & money supposedly appear and disappear.

3. Open immediately an investigation of the regulators who

failed their task in regulating the markets.

This can spin out of control very quickly. Myself and countless

others are counting on you to protect the integrity of the US Financial markets.

Andrew Abraham

Abraham Investment Management

#8

Great posting Bernard. I'd love to see Bill English and James Turk go head to head!

The key for me is not having all my eggs in one basket, INCLUDING gold/silver

MF Global — 2011′s version of 1929

Posted: 09 Nov 2011 04:43 AM PST

There are beginning to be some serious concerns that the futures market segregated account holders at MF Global may not be made whole.

If this becomes the case, then MF Global will be 2011′s version of 1929.

I have been in the futures business since the mid 1970s. The industry always spoke about how client money was protected by the independent clearing corporations of the exchanges and by the segregated account banking arrangements.

This apparently false assumption of protection was reaffirmed in 2005 with the collapse of Refco due to reputed fraudulent activity by its CEO. While general creditors of Refco recovered slightly more than 30 cents on the dollar with the dust settled, Refco’s segregated account holders had full recovery – after some time delay.

Fast forward to today. There is a strong hint that segregated account holders at MF Global will be left holding the bag. See Reuters article from yesterday.

Futures markets and futures commission merchants (FCMs) are supposed to be highly regulated by the Commodity Futures Trading Commission (CFTC). If MF Global’s seg customers are not fully protected, it would be the equivelant of, let’s say, depositors of Chase bank or customers of Fidelity not being protected.

The failure of MF Global”s segregated account to be made whole would be the biggest financial disaster since 1929 and would spell the end of the futures industry as we know it. Folks in the financial industry should take this matter seriously — very seriously. Do not underestimate the importance of this matter.

I am not into conspiracy theory. Never have been. But if the current administration in D.C. does not step up on this one, my only conclusion is that this administration would be taking a direct shot at market speculation. Just saying!

Let me get this straight. The current administration made good on AIG, Deutsche Bank, Fannie, Freddie and many other financial biggies (only to have their executives grant themselves millions in bonuses), but is unwilling to make account holders of federally regulated FCMs stand out in the cold.

This will be a telling story to follow — and could result in the end of futures trading in the U.S. And if so, members of the futures industry and all futures’ market segregated account holders need to become card carrying members of “Occupy Pennsylvania Avenue.”

If there is a shortfall for MF Global’s seg accounts, then at last we will have the BOGI gap (Bernanke, Obama, Geithner Incompetence). And, the fat lady will finally get her chance to sing — at the funeral of the CFTC.

For updates, follow the web site of MF Global’s trustee, James W. Giddens.

http://blogs.telegraph.co.uk/finance/ambroseevans-pritchard/100013198/a…

The EU Project has become both dangerous and insane.lava...or blood?

On the one hand I will do a Libertarian and say let them fail they deserve it and will clap.....however not being able to buy food as the banks shutdown, lose 50% of my house value and see un-employment double if not treble inside 6 years isnt in the slightest way funny.

regards

"the third task has become dominant"

http://www.marketoracle.co.uk/Article31455.html

be afraid....be very afraid.....

"At some point, the nations will default. A Great Default is coming. This may be all at once. It may be piecemeal. But the big banks will get stiffed. So will the voters who have become dependent on income promised by politicians, who will finally have to go cold turkey."

How soon before our great and mighty leaders in the Beehive issue the ultimate BS..."we are all in this together"....harrrrrrrrrrhahahaaaaha

".

Some Things You Should Know About China

And most importantly: Top of Chinese wealthy's wish list? To leave China

"Among the 20,000 Chinese with at least 100 million yuan ($15 million) in individual investment assets, 27 percent have already emigrated and 47 percent are considering it, according to a report by China Merchants Bank and U.S. consultants Bain & Co. published in April."

The Western resident of Beijing (married to a Chinese woman, with two children) who posted this on his blog added, "Everyone with money has a escape plan."

Here's a simple question for China bulls and all those writing about how infrastructure projects, an omniscient central government and rampant consumerism are going to keep China's growth engine humming for years to come:if the future's so bright, then why does everyone with money have a bug-out plan, two passports and a house in Vancouver, New York or Los Angeles?

If you can't answer that, then you need better sources.

The edge of the financial banking cliff of debt is giving way....it's underway folks...are you standing too near the edge?

http://www.telegraph.co.uk/finance/financialcrisis/8846201/Debt-crisis-live.html

Yurk...the only good news is that meat prices are holding firmish...maybe these fat lambs will bring a fat return....!

Don't bet the farm on it, I talked to my stock agent last night, all my sheep are going next week, he thinks its all down hill from here, he's more optimistic than me.

Is he working for you...or working for the works!...the price of quality food may well receive a Bernanke QE3 promise any day now...another round of bubble prices from Ben!

Na, he's independent. At $8 a kg I think sheep prices are unsustainable. QE is really default by the back door and now production is rocketing into falling demand. AS you have said in the past, interest rates will climb. There has been 7.6 trillion of losses in the US housing market if rates rise it will be our turn. Soon some bright spark in the bond market will notice us and say," wait a minute that little place way down the bottom of the south pacific is bugged, pull up, damm it pull up"

7.6 trillion losses is 7.6 trillion less wealth (aka money).

That's a lot of deflation pressure and without inflation interest rates won't go up.

If it follows 2008 eg Fonterra's prices dropped....so it makes sense (as much as anything in this loony world does) that commodity prices will drop.....so clearing the decks makes sense to me at least.

Re: Fonterra's payout.....just how low can it go before we see dairy farms going under I wonder........its going to be worse this time and for way longer.....I cant see it cant be so.

regards

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.