This Top 5 comes from interest.co.nz's Gareth Vaughan.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz. And if you're interested in contributing the occasional Top 5 yourself, contact gareth.vaughan@interest.co.nz.

As another Covid-19 Alert Level 4 groundhog day rolls around here in Auckland, I hope readers in the rest of the country are enjoying their new found Level 2 freedoms. At least today (Wednesday) I have an exciting outing ahead, albeit any outing is currently exciting. I am getting my second Covid jab. On top of now having had three Covid tests during this lockdown (for reasons explained here) and staying home, I certainly feel as if I'm doing my part!

Source: Twitter.

1) NFTs; A bizarre, speculative market or something more?

You might have seen the recent Newsroom story about ex-All Black Dan Carter getting involved with NFTs. No idea what NFTs are, or wanting to know more?

A report from Bernstein tells you all you need to know and more. Below is an explainer from Bernstein's Gautam Chhugani and Manas Agrawal.

NFTs stand for non-fungible tokens. NFTs are digital assets ('tokens') that represent ownership right over an underlying asset. An NFT can be used to represent any item that can be digitally consumed (image, music, etc.). NFTs have unique underlying assets that cannot be interchanged (thus non-fungible). Technology enthusiasts believe there will be a 'metaverse' (an online world) where each person will exist in the form of an avatar. Metaverse enthusiasts believe people will spend on digital goods that augment their metaverse avatar – in the form of digital skins for the avatar, or with NFTs for the mantlepiece.

While NFTs have been around for a while, the concept has become mainstream in the last few months. Like all collectibles and art, people derive social utility from owning something created/used/owned by other influential people. This has become a large reason for the increasing popularity of NFTs. Crypto-native users are bidding up NFTs as a way to show their involvement in the space, with participation from celebrities offering some validation (NBA player Stephen Curry bought an NFT for ~$0.2 Mn).

While people are buying NFTs today as a social-signaling mechanism, NFTs are a potentially useful innovation for empowering content creators. While social media platforms provide content creators with validation, they control all/most of the economic value created. NFTs for art/music/short-form videos can help artists take back control over their content and help monetize better (for e.g. Kings of Leon, a rock band launched their latest album as an NFT – the album NFT serves as memorabilia for rock enthusiasts and helps the artist go direct to their fans).

NFTs can represent multiple digital goods including art, music, domain names, trading cards, sports collectibles and events tickets, for example. Chhugani and Agrawal note popular NFTs include "generative" art being algorithmic art, profile pics such as Punks, Bored Apes and Pudgy Penguins, and in-game NFTs such as Axies and Horses on Zed Run.

So where to from here?

NFTs look like a bizarre, speculative market but could build a decentralized community movement that will onboard users to the crypto ecosystem. Before trying complex DeFi [decentralised finance] platforms, users could play around with the crypto infrastructure with some harmless and fun NFTs. NFTs also represent social digital identities which could see application in the field of gaming and social commerce – what is also being described as a decentralized metaverse. We see multiple private opportunities arising in the crypto ecosystem focused on gaming, social commerce, payments, and broader Web 3.0 applications.

2) How Covid-19 made supply chain management sexy.

Most readers will be familiar with the global supply chain woes caused by the Covid-19 pandemic. They're certainly being felt here in New Zealand, with economist Benje Patterson among those suggesting further Government action may be required,

There is an urgent need for government to consider the case for intervention to ensure our exporters’ access to shipping – which could even at one extreme involve chartering of vessels. This may seem crazy, but bear in mind that the government is already approaching $1 billion in cheques to airlines to keep airfreight moving. Airfreight on an annual basis accounts for less than $10 billion of total export receipts, while exports moved by seafreight account for closer to $55 billion of total exports across a typical year.

In a sign of the times Bloomberg's Matthew Boyle reports supply chain management has become the Covid era’s must-have MBA degree.

The tumult has forced companies to lavish more attention on their supply-chain professionals, who typically toil in obscurity until disaster strikes. It’s also prompted business schools to refresh their supply-chain curricula to make sure the next generation of logistics managers are prepared for future crises.

“For years, we had sort of taken logistics for granted,” says Skrikant Datar, the dean of Harvard Business School. “The pandemic caused us to rethink it.”

The problem, says Hitendra Chaturvedi, a supply-chain management professor at Arizona State University’s W.P. Carey School of Business, was that supply-chain education and theories had grown as rigid as some of the practices out in the real world. “After years of teaching without any tremors,” he says, “our courses had become less flexible.”

In response to those tremors, business schools are now emphasizing things such as risk mitigation, data analytics, and production reshoring—while also carving out room to explore more intangible topics like ethics, communication, and sustainability. Penn State’s Smeal College of Business is adding a master’s course in supply-chain risk management next year, with lessons taken straight from the pandemic experiences of corporate partners including Hershey Co. and Dell Technologies Inc. The course will count toward a new certificate program in risk management that’s also in the works. The W.P. Carey School of Business also plans to offer a certificate in supply-chain resilience.

The article features Jarrod Goentzel of MIT (the Massachusetts Institute of Technology) pointing out that logistics shouldn't be looked at as just an expense because it can create value when done well. And just-in-time supply chains are no longer flavour of the month.

Students who pursue supply-chain degrees this fall are certain to get an earful about the limitations of just-in-time inventory systems, which grew in popularity during the 1990s as companies aimed to mimic the success of auto makers like Toyota Motor Corp., the gold standard of lean manufacturing. For some companies, though, getting lean “became a religion,” says Penn State’s Linderman, and their orthodoxy became their undoing when the pandemic hit and there was no surplus stock to be found.

Covid-19 exposed the weaknesses of legacy inventory systems, which typically emphasize cost reduction above all else, says Hyun-Soo Ahn, a professor at University of Michigan’s Ross School of Business. The pendulum is now shifting the other way: At Walmart, whose bottom-line focus is legendary, U.S. inventory rose 20% last quarter as it doesn’t want product shortages come Christmastime. Still, shuttered factories, port congestion, and trucker shortages have brought more chaos to already overtaxed supply chains, raising prices on groceries and jeopardizing the delivery of millions of presents for the holidays.

Classroom discussions at Penn State and other supply-chain specialists will now delve into the downsides of sourcing too much from China or any single country, while they also explore the role that new technologies like machine learning and artificial intelligence can play in manufacturing and inventory decisions.

3) Do cloth masks offer enough protection against the Delta variant?

As the Government pushes for increased wearing of face masks in NZ, it's worth noting that some European governments and companies are banning cloth masks, arguing they're not as effective at stopping the spread of Covid-19 as medical masks. Elizabeth Segran details this in a Fast Company article.

Many airlines now ban fabric masks on flights. Last week, Finnair was the latest to adopt this policy, joining Air France, Lufthansa, Swissair, Croatia Airlines, and LATAM Airlines in announcing that passengers would not be allowed to wear cloth masks on flights. The reason? “Fabric masks are slightly less efficient at protecting people from infection than surgical masks,” according to Finnair’s statement. Now, all of these airlines are only allowing N95 masks, surgical masks, and respirators that do not have exhaust valves.

At the start of 2021, European countries began recommending the use of medical masks, as more transmissible strains of the coronavirus—like the alpha (or British) variant—began spreading. In France, the government made it mandatory to wear masks in public and recommended that citizens only use disposable surgical masks or N95 masks. In Germany and Austria, the governments mandated that citizens wear filtering facepieces (FFP)—a European standard that offers a similar filtration system to the N95—on public transportation, in workplaces, and in shops. In its announcement, the German government said that medical masks offer the wearer more protection than cloth masks, “which are not subject to any standards with regards to their effectiveness.”

The effectiveness of surgical masks was confirmed in a new study conducted by Yale and Stanford researchers that tracked more than 340,000 adults in Bangladesh. Among the subset of people who wore masks, there was a 9.3% reduction in symptomatic COVID; those who did get sick experienced a 11.9% reduction in COVID symptoms. The study’s authors believe symptomatic infections would have decreased even more dramatically if everybody in the sample group wore a mask.

4) Australia; State v state.

The evolving situation in Australia with Covid-19 is certainly something to watch. On Wednesday the premiers of Victoria and Western Australia were complaining that the Federal Government has favoured New South Wales with vaccine access. And with NSW, and now Victoria, having thrown in the towel in the fight against Covid-19 - the former seemingly due to a lack of political will and the latter seemingly through lockdown exhaustion - other states such as Queensland and WA remain proudly Covid free.

There will be disputes, arguing and finger pointing ahead in the Lucky Country as states, and their leaders, disagree on the path ahead and blame each other for problems and Covid spread.

In this explainer for The Conversation Anne Twomey, Professor of Constitutional Law at the University of Sydney, looks at whether states have to obey Australia's national Covid plan. It could certainly get interesting.

The national cabinet does not make laws. It has no legal powers at all. It is simply an intergovernmental body whose members discuss and agree on matters. As with any inter-governmental agreement, the national plan is not legally enforceable.

The members of the national cabinet – the prime minister, state premiers and chief ministers – are each responsible to their own parliament and, through it, their own people. The decisions of the national cabinet can only be implemented by each jurisdiction in accordance with its own laws. If a state government and parliament object to something agreed on by national cabinet, then it can choose not to implement it.

Twomey looks at whether the Commonwealth is the boss in the federation, meaning it can override state laws.

The Australian Constitution gives certain specific powers to the Commonwealth and general powers to the states. Where their laws conflict, Commonwealth laws override state laws.

For example, the Commonwealth parliament could rely on its external affairs power to enact a law that guarantees freedom of movement, which could override a state law. But this could be difficult while the Commonwealth is restricting movement in and out of Australia.

Alternatively, the Commonwealth parliament could enact a comprehensive quarantine law that covers the whole field of quarantine and associated restriction on movement, to the exclusion of any state law. But the Commonwealth has chosen not to do so. It has left the states to deal with quarantine and public health measures, as they have greater competence and public health facilities to manage the situation.

With their federal system, and Covid-19 now widespread in the most populous state of NSW, Australia's path ahead looks tricky. In contrast here in NZ, our political system is simpler. And despite lockdown challenges currently, we seem more united in where we go from here. Indeed the Government's risked-based approach for how NZ could gradually reopen to the world from the first quarter of 2022, unveiled on August 12, didn't cause much of a stir.

Our rocketing vaccination rates are, of course, helping now. In the meantime, fingers crossed that we can eliminate Covid-19 from Auckland again...

5) How Covid shook the world's economy.

Adam Tooze, professor of history at Columbia University, has a book coming out called; Shutdown: How Covid Shook the World's Economy. The Atlantic has an excerpt. Below is a flavour of what sounds like a good read.

At the start of 2020, almost $17 trillion in U.S. government IOUs were in public circulation. These are backed by the most powerful nation with the biggest tax base, and they trade in the deepest and most sophisticated debt market. You buy U.S. Treasury securities because the market is so big that, in an emergency, you can sell them without your sale affecting the price. There will always be someone who wants to buy your Treasuries. And there will always be important bills you can settle in dollars. When we say that the U.S. dollar is the reserve currency of the world, what we are talking about are not America’s nondescript green banknotes. What we are talking about is the wealth stored in interest‑bearing U.S. Treasuries.

A common chain of events in a recession is, therefore, for the price of equities to fall and the price of Treasuries to rise. When the price you pay for a Treasury rises, its yield—the annual interest coupon payment divided by the price you paid to own the bond—falls. And in response to the detection of the coronavirus in the U.S., in February 2020, that is what happened. Share prices fell. Bond prices rose and yields came down. Falling yields lower interest rates, make it easier for firms to borrow, and should in due course stimulate new investment. The financial markets were helping the economy to adjust. But then, gathering force from Monday, March 9, something more alarming began to happen. The run for safety turned into a panic‑stricken dash for cash. Investors sold everything—not just shares, but Treasuries too. That was very bad news for the economy, because it sent interest rates up—the opposite of what business needed. Even more disturbing than the perverse movement of bond prices and yields was the fact that the biggest financial market in the world was, in the words of one market participant, “just not functioning.” The trillion‑dollar Treasury market, which is the foundation of all other financial trades, was lurching up and down in stomach‑churning spasms. On the terminal screens, prices danced erratically. Or, even worse, there were no prices at all. In the one market where you could always be sure to find a buyer, there were suddenly none. On March 13, JP Morgan reported that rather than a normal market depth of hundreds of millions of dollars in U.S. Treasuries, it was possible to trade no more than $12 million without noticeably moving the price. That was less than one‑tenth of normal market liquidity. This was a state of financial panic, which, if it had been allowed to develop, would have been more destabilizing even than the failure of Lehman Brothers in September 2008.

The prospect of escalating dysfunction in the Treasury market collapse was horrifying. A “safe” asset that could no longer be easily sold, or could be sold only at a fluctuating discount, was no longer a safe asset. It ought to have been unthinkable to even ask whether U.S. Treasuries were safe. And if the implosion of the financial system was not bad enough, the Bank of America strategist Mark Cabana spelled out the wider implications. As he warned in mid‑March of last year, a nonfunctioning Treasury market was “a national security issue.” It would “limit the ability of the US government to respond to the coronavirus.” That was ominous, but for Cabana too the biggest risk was in the financial markets. “If the US Treasury market experiences large‑scale illiquidity it will be difficult for other markets to price effectively and could lead to large‑scale position liquidations elsewhere.” If you could not be sure of being able to convert your piggy bank of safe Treasuries into cash, it was not safe to hold the rest of your portfolio either, and if that was true for the United States, it was also true for the rest of the world. Beginning on March 12, the European Central Bank (ECB) registered outflows from all kinds of euro-area funds on a scale not seen since September 2008. Funds that had slimmed down their liquidity buffers to a bare minimum found themselves caught short and resorting to desperate measures like gating outflows. The fear of not being able to exit helped spread the panic.

18 Comments

Interesting that the ingenuity of humans devising the ‘clever’ Just-in-Time inventories and supply chains does not compare with the resiliency of the ancient wisdom of stockpiling during prosperous years for the lean years.

The financialisation of every sector and focus on short term balance sheets and cashflow only makes our systems more fragile.

That's capitalism for you. There's been a long period where just in time meant higher margins. If you didn't adopt it you were outcompeted and didn't survive. There are probably some companies with decent stockpiles left and they should be doing well in current conditions.

In the early 2000s I was the R&D manager for a local manufacturing company. We held a stock of some lines of products, that we were continually receiving small quantity orders for. This meant that we didn't have to tool up for them, could respond quickly and be competitive. Every time we got a big order for the products, we'd check the current inventory, and build more to maintain a stock level, off the end of the production run. An accountant bought half the company, saw this practice and demanded it stopped. In the first year after the last of the stock was used up, the lost direct business cost $tens of thousands. Indirectly at least one long term customer went to a European competitor because they maintained a stock and could respond quickly. Couldn't talk about it to or in front of the new owner though. His ego couldn't take it how much he had cost the company. Small markets often make JIT a flawed premise.

I thought JIT was a fad and not particularly good. It morphed into JTL. Just Too Late and was discarded when it didn't work as company's thought it should

I am just waiting for someone to NFT New Zealand property... all the prestige without the maintenance...

Let's just create tokens for all those that can't afford housing. Problem solved

Nah - it would be seen as a token gesture.....

I'm going to have to defend Just-in-Time (JIT) here. People who blame JIT, and many who profess to practice it, don't understand heijunka ("Lean method for reducing the unevenness in a production process and minimizing the chance of overburden") The problem with TPS is that people don't understand it at any depth, had they been following the principles single sourcing and global outsourcing would never have developed into these issues.

You can't blame the process if people aren't following the basic principles!

Just in Time was the reverse of Resilience; the difference was Capacity (to endure whatever shock - which was Russian-Roulette predictable to occur).

We had pared Capacity to the bone, essentially through short-term selfishness (the same way we ignore the planet when counting 'wealth'). If we had had more ICU beds.......

Of course we don’t have ‘lean years’ or famine anymore - we just print money, helicopter, and drop interest rates. That keeps the money flowing if not the physical provision.

I continue to be amazed at how credulous financial journalists are when reporting on the 'crypto space'.

What is the NFT 'craze'? It's a shell game where anonymous accounts owned by one individual will exchange a worthless digital receipt (not even *copyright*) at ever higher prices, until articles like this report breathlessly how much NFTs are 'worth', at which point the plebs start getting tempted by greed.

Or the amazing coincidence whereby all the major crypto exchanges suffered 'DDoS' attacks, or maintenance problems, last night as prices started cratering. Even though their hosting providers didn't see any problems. Hey, prices can't go down if you don't let people sell, right?

But financial journalists are too intimidated by the 'nerds' to question the obvious fraud and stupidity. And the con artists are very, very confident.

A good example of spending 1 minute research and then a brain dump comment. "The financial journalists are too intimidated by the 'nerds' to question the obvious fraud and stupidity."

...and a great example of how any criticism of crypto is met with personal attacks and misdirection rather than addressing the point with facts.

Why did all the exchanges go down at the same time, when people were trying to sell? and not at similar volumes when the price is rising?

Why do articles about NFTs not investigate whether the transactions are real or not?

The fraud in crypto is *too obvious and crude* for conventional financial journalists to even see it.

A few went down yes, funny on the day EL Salvador makes Bitcoin legal tender. A few want this to fail, but saying "all the exchanges went down" is again FUD. I am not an expert in NFT but can see a huge development to the upside for them, removing lots of middle men clippers.

OK, it's inaccurate to say they all went down, only some of them did. Fair point. Why did they go down together? Is it coincidental that it was during the middle of a massive price plunge?

What problem do NFTs solve? It's a digital hash attached to a file, that can be checked against a register; there is absolutely nothing new or interesting about the technology. It's a digital barcode. There are plenty of middlemen that are yet to be flushed by better online alternatives, but this has nothing to do with NFTs as speculative items.

and then there's Tether, who are singlehandedly propping up the Bitcoin price, with billion-dollar inflows every few days (inexplicable because the money flows in despite their being under criminal investigation, despite the uncertainty around their reserves, despite the existence of better alternatives). Tether, whose billions are backed by 'commercial paper' the identity of which they won't reveal, but no serious brokers of said paper ever having seen them in the market... anyone who owns Bitcoin is being *robbed* by Tether, but the nature of the cult is such that they'd rather be robbed than admit that the real price of Bitcoin should be lower.

Interesting article. I have been doing a lot of reading up on NFTs recently and see a great future. As they are basically a digital accounting of electronic goods, I see a real potential as a platform to sell shares direct from a company, ie do away with hedge funds and the like. With a lot of articles in the US about dark pools for shares, synthetic shares, etc, it seems a very logical move by some savy companies.

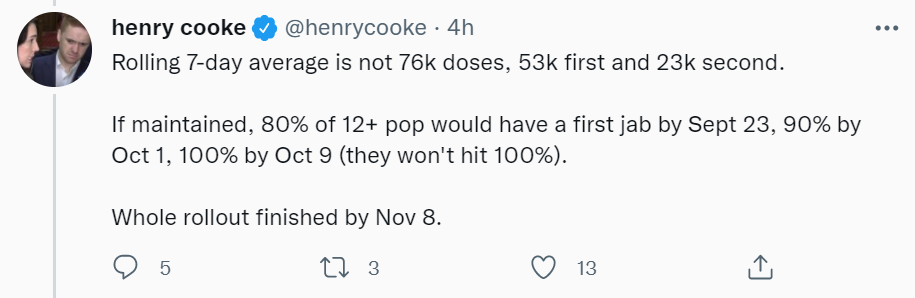

"Our rocketing vaccination rates are, of course, helping now. In the meantime, fingers crossed that we can eliminate Covid-19 from Auckland again"

The govt having been hanging on a wing and a prayer. There have been a number of instances where "fingers crossed" has got the govt thru with border and MIQ issues over the last year.

The govt will also be hoping for a high total dual vaccinations (at least 80%) within three months.

Any more lockdowns for Akl in level 4 or even 3 extending past end of this September I feel will result in lockdown blues and mass rule breaking. We shall see.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.