Population growth from migration continues to decline, with a net gain of 2322 in May, the lowest it has been for the month of May since 2014.

On an annual basis there was a net gain, (the surplus of long term arrivals minus long term departures), of 66,243 in the 12 months to May, the lowest it has been since the 12 months to May 2015, according to the latest Statistics NZ figures.

The net migration gain in the 12 months to May was down 7.9% compared to the previous 12 months, while the net gain for the month of May was down 25.5% compared to May last year, suggesting the trend is continuing to decline.

The slowdown in the net gain is mainly due to increasing numbers of people leaving the country, while arrivals are more stable.

In the month of May there were 8140 long term arrivals, down 2.9% compared to May last year, and 5818 long term departures, up 10.4% compared to May last year.

China and Hong Kong continue to be the main source of new migrants, with a net gain of 8968 in the 12 months to May, down 18.7% compared to the previous 12 months.

India remains the second biggest source of migrants, although there has been a huge decline in net migration from that country over the last two years.

In the 12 months to May there was a net gain of 6767 from India, down 10.9% compared to the previous 12 months, and down 44.9% compared to the 12 months to May 2016.

The next biggest source countries were the UK with a net gain of 5513 in the 12 months to May, down 15.6% compared to the previous 12 months, South Africa with a net gain of 5048 which was up 6.7% compared to the previous 12 months, while the net gain from the Philippines was almost unchanged at 4550.

More New Zealanders are continuing to leave the country permanently or long term than are arriving back after extended stays overseas, with a net loss of 1386 New Zealand citizens the 12 months to May.

However that figure is almost unchanged form the previous 12 months but has fallen hugely from where it was six years ago, when there was a net loss of 39,413 New Zealand citizens in the 12 months to May 2012.

There was net gain of 67,629 citizens of other countries in the 12 months to May, down 7.7% compared to the previous 12 months.

That decline was almost entirely due to a 21.9% drop in the number of overseas citizens returning home, while arrivals of overseas citizens were largely static.

In a newsletter on the figures, Westpac Senior Economist Anne Boniface said the net gain from migration was expected to continue tracking down.

"We expect this trend to continue ... as many of the people who arrived in New Zealand on temporary work and student visas in recent years return home after completing their course or contract," she said.

"We forecast annual net migration to fall to a low of around 20,000 in around five years time."

Net long term migration

Select chart tabs

161 Comments

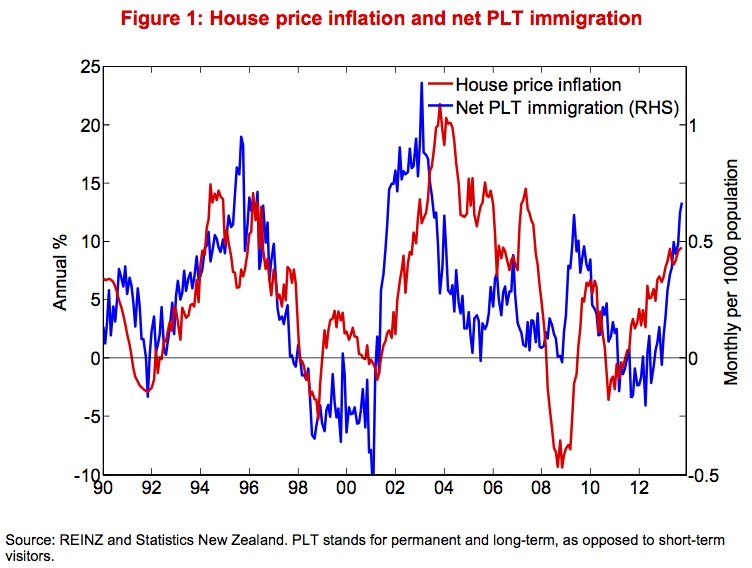

Still a lot of people. 830 houses needed to accommodate this month’s increase at 2.7 ppl per house. This is one of the statistics that actually does have an impact on house prices. The correlation is undeniable -

http://www.greaterauckland.org.nz/wp-content/uploads/2015/04/RBNZ-net-m…

{kind=link}

Not sure why May the lowest month every year...

So what you're saying is, with Auckland house prices currently flat-to-falling and annual migration into Auckland of say 35-40k, that if that Auckland migration number drops to say 10-15k per annum that Auckland house prices would fall materially?

That's an interesting interpretation of my comment. What I am saying is that, based on past trends, I expect house price inflation to roughly correlate with net migration. Net migration at this level is still putting upward pressure on prices. Less pressure than previously for sure.

Do you appreciate the huge resources and time it takes to build 830 houses? All that cancelled out to accommodate this month's population gain.

I'll take that as a "yes". Auckland migration falling to 10-15k isn't a certain outcome in any case.

In the past a house price / migration slow down would be accompanied by a commensurate fall in construction. The difference this time is whether the Government can/will try to stick to 10,000 homes per year in this circumstance. Sure, they might not hit their target but if they are pushing ahead with construction despite migration/prices that could be interesting (not to mention many other head winds for property which is a separate discussion). It would be tempting as a means of keeping the economy running with jobs and fiscal stimulus (all those huge resources you mention).

I'd say "probably no". At 10K-15K annual net gain in Auckland, I'd expect prices to be flat. Seems like we're around that level in May.

The Kiwibuild underwriting scheme will probably keep construction more buoyant than it otherwise would have been if there is a downturn, but I don't think the impact will be huge. I think most Kiwibuild houses would have been built anyway - they would have just been bigger more expensive houses.

"the correlation is undeniable" and yet a 50%+ fall in migration would not change house prices from the current level? Your argument doesn't make sense to me.

"the correlation is undeniable" and yet a 50%+ fall in migration would not change house prices from the current level? Your argument doesn't make sense to me.

Correlation is not causation. The existence of a correlation doesn't necessarily mean anything.

Agreed. Not suggesting that particular correlation = causation, simply looking at BuyLowSellHigh's argument. I would also subscribe to credit availability/price being the most dominant factor.

and it’s a win to Zombie Ponzi

A 50% fall in net migration could cause a noticeable drop in house price growth. You said a drop in immigration to 10K-15K in Auckland would result in house prices falling. The data shows that while net migration remains in the positive, house price growth is likely to do the same.

Yes but growth is already zero/negative......

As I said above, at 10K-15K annual net gain in Auckland (which it looks like we're at for May), I'd expect prices to be flat, which they are. Still price growth nationally though.

Wrong. 66,000 arrivals in the past 12 months, so ~30k+ would be to Auckland, not 10-15k.

Unless you're suggesting all migrants buy a house the month they arrive in New Zealand? In which case you'd still be wrong.

No, 10-15k for May, not on average year to date. I'm not suggesting all migrants buy a house the month they arrive in New Zealand.

I'm saying there is a very close correlation between net migration and house price growth. This has been the case for a very long time, it it the case now, and it will likely continue to be going forward.

Migration is also not the only demand driver, and whilst demand is still present, and banks are still lending, and home loans are still serviceable, prices won't go through the roof (pun intended) but nor will they plummet.

No, I think that analysis is completely wrong. Demand for housing as accomodation is a contributing factor but not the main factor in current prices. The main factor is the cost and availability of credit. If demand for accomodation was the principal factor you would see similar movements in rents. You don’t, rents are quite disconnected from prices, current yields are miserable. The house price bubble reflects the credit bubble. If available mortgage credit shrinks prices will fall, regardless of what net migration is doing. You can’t buy a house with mortgage credit you don’t have.

Well said Bobster!

Boobster & Retired-Poopy,

I think it is naive to say that demand for housing as accommodation is not a very significant driver of property value. There was a very good interest.co.nz article a few weeks ago (Rodney Dickens I think) showing that rent rises are determined largely by income rises. I.e. rent is determined by what tenants can afford to pay. The article did a good job (inadvertently) of explaining the disconnect between rent and property values. And remember, many immigrants are wealthy. They are selling up in London, Sydney, Brisbane to buy in NZ, not rent.

My key question to both of you - what do you have to say about the very clear correlation in the graph I linked to above, and why do you think now is different?

^^LOLdgz^^

Hey, you haven’t posted much property porn lately!? Don’t make me beg......grrrrrrrr

#sadpropertypornaddict

No he just makes silly comments, then giggles at the end. Bizarre!

Bobster, DGZ had a particularly exhausting "apogee" for the 11 million dollar house last week, I don't think you're giving him time to recover. I know you are used to his #doublegrammartumescence coming in quick succession but after the really climatic sale last week, you are going to have to be more patient.

Harrumph.....why’s it always about HIS needs?!

Lodge? makes sense

Some migrants are wealthy, but most are not, they are pretty average or below average. These are the people putting pressure on rentals. To rent a property is materially cheaper than buying it. It makes no sense to me to suggest that rents are capped due to low migrant incomes, but yet those lower incomes are not a barrier to taking on ever larger amounts of debt service? Both those things can’t be right. Migration is part of the cause of current high prices, but it’s not the biggest. The biggest cause is cheap and loose credit. Migration is really part of the narrative used to justify current prices and explain why “this time it’s different”, but the real cause is expanding credit and an investment bubble. IMHO.

1. "Some migrants are wealthy, but most are not". Evidence please?

2. You say that most migrants are not wealthy and are putting pressure on rentals. If this were true, why have rent rises been so modest over the last 8 years while net migration has skyrocketed. Doesn't make a lick sense.

3. "To rent a property is materially cheaper than buying it". Yes, but not in the long run. Your mortgage payments stay at about 6% over the life of the loan on average, and reduce as the debt is repaid. But rents go up with inflation year on year. Regardless, many immigrants earn excellent incomes and are buying, not renting.

4. "It makes no sense to me to suggest that rents are capped due to low migrant incomes". I didn't say this. I said that rent rises correlate extraordinarily closely with income rises. See data here - https://www.interest.co.nz/property/93555/rodney-dickens-doubts-landlor… . Rich immigrants buy houses and push up prices, simple.

5. Again, and most importantly - I linked to a graph in my first comment showing a very clear correlation between net migration and house prices. What do you have to say about this and why is now different?

"3. "To rent a property is materially cheaper than buying it". Yes, but not in the long run. Your mortgage payments stay at about 6% over the life of the loan on average, and reduce as the debt is repaid. But rents go up with inflation year on year."

This is way too simplistic. You also have to pay rates (which also increase over time) and for maintenance and insurance when you own a house. There is no guarantee that owning will make you better off than renting and investing the excess money elsewhere.

Use any online compound interest rate calculator to do the maths. You'll find that with all of the costs of ownership included, you are better off in the long run to buy. Rents increase 3% - 5% per year on a compounding basis. Over 30 years, this is significant and offsets insurance, rates etc. Meanwhile, your mortgage repayments are reducing year on year as the debt is repaid, plus you own a house in the end.

Buylowsellhigh... what about your moniker?

It's not just a case of should I buy or should I rent? But when should I buy and when should I rent? Why do you keep mentioning a 30 year mortgage vs a lifetime of renting when that is not the scenario most are considering. Most will be thinking... shall I buy now... or wait 6 months, 12 months, 18 months.

If you are currently renting and based home ownership purely on economic measures... why would anyone buy now?

Migration is dropping, the economy is slowing, house prices in Oz are crashing, foreign buyers soon banned, house prices ALREADY flat and falling in places (the chill has spread and spreading,) business confidence low, global headwinds, global interest rates hikes.

By my calculations, my capital is currently more or less neutral. My cash is earning more in investments than it would currently be in property, because capital gains are disappearing.....and when all the numbers are crunched, for the time being, renting vs mortgage interest payments for the next few years + insurance, rates, buying costs etc... renting looks like the better choice.... not FOREVER, but just in the short to medium term.

And as more and more data comes in, there is the opportunity cost of house prices actually dropping.

There are many factors putting upward and downward pressure on property values. I think you've overestimated the magnitude of the downward pressures and underestimated the magnitude of the upward pressures.

As for my moniker - it's just a moniker. When it comes to property, you'll find its very difficult to predict when the market is at it's peak or bottomed out. Best not to try be too smart in this regard - look at the trends for rents and property values over the last 30 years. These trends, on average, will continue, with peaks roughly every decade. As for your “when to buy question” - buy a house as soon as you can afford to, then keep it.

Seems like you want to wait until prices fall to get into the market. Also seems like you’re the type that would then say you don’t want to catch a falling knife.

You'll find whatever the assumptions you put into the calculator give you. Any reasonable comparison would account for renters putting the principle payments they aren't putting into a house into an alternative investment which may perform better than housing. Any reasonable comparison would account for the flexibility of renting, the low relocation costs, the huge gain in free time from not having to maintain or improve the property.

My perspective it to buy a house not for financial reasons but for psychological benefits when you believe you will be stable for a while and want the commitment. I've done both and there are benefits to each. The main reason so many think buying a house is so good financially is that it forces people to save money who would otherwise be psychologically incapable of doing so.

Some rather extravagant assumptions there.

I consider a decade long enough to be "in the long run" I rented from 2006 to 2016. I was far better off renting for that decade than owning, as the places where I lived had zero or negative capital gains. For most of my rental decade, I paid my rent with a portion of the proceeds of the rental house value that was invested in term deposits. My landlord had to pay the rates, a property manager, and also occasional maintenance costs. By my calculations, I ended up about $150k richer by renting over a decade than if I had bought. And over that decade, I had a single $10/week increase in my rent. That works out to be a bit under 0.2% rent increase per year, not 3-5% increase per year.

For reference, I was a homeowner for the two decades prior to this decade of renting, and have since returned to home ownership. It is a myth that one is always better to own than to rent.

Wankiwi,

Which region/suburb had no or negative growth from 2006 to 2016?

So you purchased in 2016? Many doom and gloomers on this site would no doubt say that you’re a sucker that purchased right at the peak of the market when prices started to slow.

I recommend looking at Hawkes Bay home values. I actually sold in US in mid 2006, the rented there for another year, then rented near Christchurch until winter 2009 then moved to Hawkes Bay. In every one of these locations it was significantly more fiscally prudent to rent than to buy during these time periods. My biggest coup was renting a house in 2007 to 2009 at$ 345 per week, with the house value above $800k. The term deposits during this time had yields around 9%. You do the maths... there were no capital gains during this period, there were significant capital losses at this price strata for this time frame

After moving to Hawkes Bay, I rented a ~$550k house for $525/week. Seven years later the house sold for less than $600k after we gave notice. The landlord sold immediately after we moved, she had owned six homes in the area for investment when we started renting, she sold every one of them excepting ours due to bad tenants during the years until we moved and she then immediately sold our rental as she didn't want any further bad tenant issues

BLSH,

Your gratuitous and egregious spelling error suggests a mentality nearer the schoolyard bully than a rational investor. Would you care to compare investment returns over to past few dacades? I am rather happy avoiding the lackluster property returns of the past couple of decades myself, even if one bought into the best of the AKL market locations... one could have done so much better elsewhere.

Wankiwi,

Hawkes Bay - so you’re right out in the regions then. I posted a related comment yesterday. I’m a big fan of Professor Paul Spoonley on this topic - I believe him when he says that two thirds of the regions are going to experience continued stagnation or decline for the foreseeable future. Avoid these like the plague (Hawkes Bay, Northland, Southland etc.), but invest in the rest (Dunedin, Tauranga, Palmy).

But still, if you had purchased that $550,000 house in Napier in 2006, it would’ve been worth $680,000 by 2016. This is based on the official median statistics, not your anectotal claim. So you’ve managed to lose out on $130,000 there. Probably not the best place to have your capital invested though. I’d be looking to the likes of Dunedin, Palmy, Tauranga.

B**LSH**

Any link to your officious statistics? When I google median house prices to confirm the data that I am familiar with, I find that the capital gains for the timeframe I reference are on the order of 5% or less. Your assessment of a capital gain of ~25% is a bit amusing and not related to any data I've seen. Have a look at https://www.addedvaluation.co.nz/napier/ for annual prices in Napier for a realistic evaluation, or for this to match my local circumstances ( https://www.addedvaluation.co.nz/hastings/havelock-north/ ). I am quite comfortable with my evaluation of reality. A sidenote, we actually finalized our purchase price in late 2015, and took possession in the beginning of 2016. The following 12 months were very good to our home price evaluation... :) One should buy low, as well as sell high. I've demonstrated success in doing both aspects, how about you? Since our purchase, the official median statistics suggest that our home has increased by about 35%. This is an illusory gain unless one decides to sell without purchasing elsewhere... In order to make a real gain, one has to sell at an appropriate time, as well as buy at an appropriate time.

All the best with that, I’m not going to hazard a guess about what’s going to happen out there. Link to data below.

https://www.landlords.co.nz/housing-statistics/?graphsubmitted=true&fro…

As any investor knows, average sale price has only a casual correlation with house value. If lower value houses are selling a lot, then the average sale price decreases, even if the same home price is static. Similarly, if higher value homes are selling but lower value homes are not, then the average sale price increases even if the same home value is constant. Another aspect is that home size has increased quite a bit in the last decade, which substantially increases the average sale prcie even though a given house price is unchanged. Using average sale price as your metric is silly. Look at HPI for home value instead.

Ramblings of a madman. This is median data, not mean, so that isn’t a problem (which is why this data is used widely). Also, not that many new houses would have been built there between 2006 and 2016. Impact of larger houses would be negligible.

But I acknowledge the gains weren’t good over this period in the region. Still better than renting.

The house we rented was purchased just prior to us moving in, and sold when we left. It's 5% capital gain for that time period is a matter of public record. Sorry that you do not understand fact and logic. Best of luck. BTW, your data shows about 5% capital gain for the same 7 year time period.

Yankiwi 5

Buylowsellhigh 0

Spot on regarding your last statement, I didn't respond to blsh, as you can only reason with sensible people.... he would have just just come back with a bark..

.

Some migrants are wealthy, but most are not

Average by what standards? You have to have a fair amount of cash lying around to up root yourself to a high COL country like NZ. Most of the immigrants I've spoken to from the third world had maids back home. The people driving taxis, making takeaways and manning counters at service stations aren't from poor backgrounds.

I am talking in terms of income here. Many of the minimum or low wage job holders I interact with seem to be esp. south Asian migrants, fresh out of the schools around Queen st. I also see the lack of wage inflation pressure at the lower end as being due to low skilled migrants competing for jobs, but it’s very anecdotal of course. For every remuera there are 5 Sandringham and owairakas.

BuyLowsellhigh, notice you commence name calling when out of your depth. When I see your posts, I'm reminded of a person who only specializes in oily substances like snake oil.

What name calling? I read all of BuyLowSellHigh's posts above and there is no name calling - just the presentation of reasoned arguments based on statistical correlations.

Retired PoOppy

Only one gratuitous misspell name-calling remains from BLSH.

A hint is that some posts have been edited. Note that some responses to BLSH posts are with a timestamp earlier than the BLSH post. That means that BLSH has edited his post. As we do not have a edit history on this site, one cannot show what was posted originally. The timestamp strongly suggests that BLSH edited after reading the post from RP.

Wankiwi, I assure you the edit is a spelling correction.

Kate, it's no big deal. He resorts to this when he'd rather avoid the pending counter arguments and prefer we'd just leave. See above "Boobster & Retired-Poopy" @12:47.

RP, I asked you to see your GP urgently mate, you are really losing it ...

P.S. I hear there are some good anti-hallucination drugs in the market at present !

Shouldn't you and your specuvultures mates follow your advice before dishing out to others..

There is clear evidence of desperation from you lot..

@Kate, Blimey you must be one of a few then. I would suggest that the only others that read BLSH quotes are those that deep down know they have made a big mistake, one that may take them 30 years of misery to get over, but they read because his waffling gives them small a sliver a hope that at least they aren't alone.. Albeit where they really know that the trap, that the banks were allowed to create, has already sprung on them. Akin to being in a prison cell that at least offers a view, even if no chance of escape.

Still flatting, Nic?

Nic, did you eat that time expired ham and mouldy white bread I left in the fridge!? Even though it had my name on it!? You know how I’m saving hard for that first home in pokeno, you’re just not helping....

Can we please talk tomorrow before your paper run....

Sorry about the sandwich but it wasn't me Bobster..

It was that lovely old lady from next door, apparently her stupid son borrowed too much money from Westpac and has kicked her out of the house she was renting from him. Something to do with him not meeting the banks new lending covenants or he'd lose the family home. She was going to give the sandwich to his dog I think... I said that she could come back and sleep in your room tonight - hope that's okay and for her not to worry about the lack of heating, I said you'd keep her warm... We've got to keep saving that deposit Bobster!!!! Focus and take one for the team.

Oh, you mean the p addict? Well, ok, I know we need to make sacrifices so we can afford that 2 beddie in pokeno. Honestly, if I can go without lattes and avocado on toast why can he go without P!? Seriously, he’ll never get his foot back on the ladder......loser

he may well be one of those p-addicts.. addicted to 'property-porn' its such an expensive and costly issue within society, particularly with credit and its availability about to get so much tighter... Good on ya Bob helping an old lady out... Maybe we could see if she wants to buy with us as well? reckon we'll be able to buy a 3 bed pretty soon... way things are going..

Not that you asked me but I'm still flatting. Won't be buying for a couple of years.

Do you think I should be ridiculed for saving hard for a house but not being able to afford a decent one yet? In your mind are people poorer than you to be ridiculed for trying to make their lives better than their parents?

"My key question to both of you - what do you have to say about the very clear correlation in the graph I linked to above, and why do you think now is different?"

I would like to see what the graph would look like extended to the present day. Record immigration over the last 2 years while house prices have stagnated in Auckland. Sure, there's a correlation but it is clearly not the only factor and the two do not march in lockstep. You ask why people think now is different, perhaps because now is different - migration is high, house prices are flat.

There has been an extraordinarily close correlation from 1990 (probably earlier) - 2016, but "now is different".

Like those people who gather on a mountain top year after year because the world is going to end and they are going to be sucked up into outer space by the savior. "This time is different, trust me".

OK, I'll flip the question back onto you. Why have house prices in Auckland barely increased in the last two years while immigration has been running incredibly hot by historical standards if the correlation is so extraordinary?

someone who understands about credit bubbles/availability only could answer that question meaningfully

Take another look at the graph. There are plenty of years where the two don’t align perfectly, but when you take a step back, there is a very close correlation over time. Migration isn’t the only factor, so this isn’t surprising. Can’t just look at 2 years and say it disproves 2 decades. And id still say there isn’t a mismatch really - migration slowing, so is price growth. Discrepancy probably down to affordability constraints and cautious lending.

I agree, like I said there is some kind of correlation but it's clearly not all that is going on. If anything, I would say the graph suggests house price inflation is lagging migration by a year or two, so the fact that house prices flattened well before migration started to reduce give me no confidence that current levels of migration are going to lead to houses rising.

Something else is effectively counter-balancing any price pressure which current migration levels are causing. Like you say, it could be credit availability or that prices have run up too high. If I was looking for when house prices will take off again, I'd be considering these factors rather than assuming a now reducing immigration rate would kick things off again.

I just don’t see the disagreement here, I’m not ignoring other factors, just point out the strong correlation which I think is going to continue more or less.

“I'd be considering these factors rather than assuming a now reducing immigration rate would kick things off again.” Again, I’m not ignoring the other factors or suggesting that migration will “kick things off again”. I am pointing out that net migration remains high by historical standards, which will be putting upward pressure on prices (while other factors exert downward pressure) and I see no reason why the general correlation wont continue on.

I think it is naive to say that demand for housing as accommodation is not a very significant driver of property value.

But you didn't say that. You're inferring that migration is correlated to house price growth. And to some extent, it probably is.

Nevertheless, availability of credit can be a pre-condition for demand. So the availability of credit can drive demand. Without credit, it's possible that no demand would exist, therefore migrants with large amounts of funding at their disposal would be paying lower prices for properties.

rent is determined by what tenants can afford to pay.

Exactly the same as house prices. House prices are determined by what buyers can afford to pay. When credit is freely available and the cheapest in NZ's history, this allows many buyers to afford to pay more for houses.

Whilst foreign buyers have surely added heat, it's the resident buyers competing with each other and foreign buyers that put upward pressure on prices. However, if the credit to these higher prices hadn't been available then no bueno. You can't pay with money you don't have (or can't get access to).

Well, keep your eyes on Sydney and Melbourne, cos they both look like property bubbles that are going deflate (violently or otherwise) due to a reduction in the amount of available mortgage credit. The banks are having a sort of epiphany when they think, “maybe we shouldnt have lent interest only on 8x income to every sentient being who walked in our door”. Without any other change in fundamentals like “migration”.

Good old Aussie banksters!

Bobster is right of course

Low mortgage rates of 1% from China banks also are invested in the obscenely inflated property markets around the world including Auckland.

I just wonder how many kiwis living overseas now will see living back in Auckland as a better option nowadays

At least you’ve got a decent government unlike the US & Jacinda made PBS news here with baby girl tonight

You need to put these movements in the context of changes in interest rate. Changes in rates have a more significant effect that changes in accomodation demand.

And of course our old friend, but somewhat harder to discern - “credit availability”.

Yeah, well said

indeed custard and with migration now dropping (as the specu-vultures depart the country leaving their bad debts and false ID's behind) we may find out that our very gullible banking sector is left facing a new wave of capital losses... Easy come easy go as they say!

One swallow does not a summer make…..and all that sort of thing.

But I’ve been banging on a bit recently about what I perceive as the key drivers of our market – and that nearly all are continuing to being left somewhat weakened over time.

This to me is just another dent in one of arguably the most significant drivers.

No sudden crash, but piece by piece, and bit by bit the drivers are reverting back towards more historical norms.

Do the banks respond and throw cheap credit around like drunken sailors once again – probably not.

They may find they need to hold a little more of depositors funds in reserve.

Could the irony be less depositors funds being available to various external factors (upwards interest rates + exchange rates pressures) siphoning more out of the economy?

Custard pie

So true everyone’s forgotten about credit availability

The 2 best examples of credit availability I’ve witnessed was to corporate NZ in the 80’s and US residential property in the early to mid-2000’s.

The ability of ultra-loose credit to blow up a market is incredible.

Equally incredible is how few actually see it while it’s happening, including many quite bright and intelligent people – somehow for the majority of players it all makes sense – pricing all quite rational thank you very much.

I’ve never forgotten the power of credit availability – and its intoxicating effects on a market thirsty for a drink.

I think we’d need to see an overlay of interest rates and rents over the same periods. For eg, I would say the principal cause of prices increases post GFC were the rapid interest rate cuts, not immigration. Rents would be the best indicator of the effect of increased migration on accommodation, stripped of credit growth. Is that something you could work on over the weekend? Thanks in advance

I’ll take a punt – but I’ll talk Auckland.

From memory the market was doing a bit of a sideways dance until around 2013 – then up, up and away.

Just wondering – what else started to happen around 2013 – which was also then up, up and away?

And a final late Friday afternoon throw it up in the air – perhaps it wasn’t so much the number of immigrants – but more the intent and raison d’etre of some that created such unusual market behaviour.

If you don't like the housing situation in NZ you can vote with your feet and move to another country - thank God Australia still takes us Kiwis.

American was looked at by many of its "founders" as a giant marketplace. Americans could decided education was too expensive in one state and move to another. After graduating they might look for job opportunities in another state. After saving money, that same American might look to yet another state to purchase their home.

Hopefully wise Kiwis are leaning to treat NZ, Australia, UK and Canada as such a marketplace. Most Millennials (including myself) have no patriotism towards NZ.

I know few close friends who are lucky enough that they are done with EOI step and no longer affected by the immigration policy changes. https://www.immigration.govt.nz/about-us/media-centre/news-notification…

And once you are granted with RV, you have a year before moving to NZ. So I am expecting that the arrival will continue to be stable until the end of the year until we see a sudden drop.

Also those on temporary visas without prospects of ever transitioning into permanent one will eventually leave. That may be the reason behind an increase in Asian departures.

It's either up or down so what's the fuss?

DGZ, no fuss. Its hard to ignore a downward trend likely to continue for years to come as the economy slows. Boom-over-Rover!

A appropriate song for the end of the week. Last one out turn off the lights!

Hallelujah….

A winter solstice miracle!!

We are none the poorer for this drop. We could well be better off. The policy arguments for New Zealand’s immigration flood have never been articulated. Perhaps because they’re economically and socially all but indefensible.

New Zealand’s immigration policy is predominantly the result of the agricultural sector moo-ing to previous governments about ‘the need’ to lower its costs of production to compete with other global producers. New Zealanders are increasingly unwilling or financially unable to take the low-waged, low-salaried jobs demanded by the sector. So foreign workers are ‘needed’. Other sectors see the same argument. All the way down to restaurant owners. The policy is there to be taken advantage of by anyone, and people notice when the incentive to collapse business costs is staring them in the face.

And so New Zealand has plummeted into an increasingly low-value, often nakedly exploitative, economy. Infrastructure of every sort is all but overwhelmed, GDP per capita rests with its wheels spinning in a polluted ditch, and the families of ordinary employees in our larger cities depend on food-banks. Many others, of course, welcome the pressure on housing, and congruent asset value inflation.

And houses for our now indispensable highly-skilled immigrants? We need more indispensable highly-skilled foreign workers to knock these together. Where are we going with all this? Who knows? Certainly not towards an added-value, inclusive, highly rewarded economy and society.

The regulatory and monetary easing post-GFC triggered a change in NZ's economic landscape where even these unproductive businesses could access easy debt and cheap imported labour to make healthy profits.

We might see a large number of these low-value companies drop out of the market as minimum wages, fuel prices, input costs and debt-servicing expenses start to increase over the next few years.

yes workingman. It was always a daft idea that keeping wages down was a path to an improved New Zealand.

The agricultural sector? Maybe one component, but last time I looked they don't employ chefs and cooks, retail workers and age care workers which make up the bulk of the "skill shortage" intake.

Doris, lobbying by the agricultural sector to drive down costs of production via imported low-cost labour has been the prime and most influential driver of NZ's immigration policy. Every other sector you name and many more have used the same 'can't get NZers to fill the role' argument to bring in low-cost labour.

You want a reason for the wide open immigration door? Growth (or the illusion thereof)

"We are none the poorer for this drop"

I think we are, because the drop is not so much because we're getting less immigrants in, it's because more kiwis are leaving, see quote below.

"The slowdown in the net gain is mainly due to increasing numbers of people leaving the country, while arrivals are more stable"

Workingman, do you really think letting a lot of asians in and losing kiwis is a good thing?

But might not many of these leavers be ex migrants themselves, who having got their passport head off to where they really want to go, which is Australia?

No ifs or butts, Boobster! Your ancestors were ex migrants themselves weren't they?? ^^LOLdgz^^

I suspect many migrants use a nz passport as a back door to Aussie, which is really where they want to be. We seem to be a much softer touch, hence why the Aussie are clamping down on nz passport holders rights in aussie. I think that esp goes for ethnic Chinese. Just a hunch

Excellent news!

How is letting a lot of asians in and losing more kiwis a good thing?

Because he likes Asians and yummy Asian cuisine especially sweet sour pork and yum-cha - who doesn't?? ^^LOLdgz^^

Are you speaking for yourself or do you have telepathy?

Well, I like Asian food too, but now that we have the recipes........?

You're able to get really good western food in asia - cooked by asians. I'm sure whitey could figure out northern chinese dumplings or pad thai.

That is very true indeed. Yan can cook, so can YOU! ^^LOLdgz^^

Maybe there is hope that GDP per capita may start to improve from the miserable 0.1% last quarter.

That can only happen if the migrant skills are better matched with our industry requirements.

Construction output has peaked due to capacity constraints and so could not contribute to economic growth in the last two quarters, so if more experienced construction workers and civil engineers were to replace the cooks and tour guides migrating to NZ in droves, we could lift our GDP per capita just as well.

One of the most significant drivers in migration is economic.

After a period of sustained buoyant economy the increase in the number of emigrants - along with subdued GNP and business outlook - could be an early signs that the economy may be perceived as cooling.

Another driver is policy, and National's changes to the rules are still working through the system.

https://www.interest.co.nz/opinion/93368/david-hargreaves-says-tweaks-n…

No.

Read the article: "The slowdown in the net gain is mainly due to increasing numbers of people leaving the country, while arrivals are more stable".

I thought leaving the country was simply free-will to do so as I not aware of any policy by neither National nor Labour directly related to ability to emigrate.

Put aside political bias and ask; "Why are more people deciding to leave?"

From the article I linked:

"The fact that a March-month record number of non-New Zealanders (over 3,000) left the country long term last month tells you what is happening. People are reaching the end of the road on visas and having to leave."

People do not always leave the country because they want to.

edit: anecdotally I know a couple of people in this situation who have not been able to obtain residency permits and are running out of work permit options

Finally, the smart ones are realising that isn't a piece of greener grass. It's just cheap astro tuff!

We can carry on debating till the cows come home, as to what property prices are doing, but my mantra and still is, is: ...."A PROPERTY IS ONLY WORTH WHAT IS WRITTEN ON THE SALE AND PURCHASE AGREEMENT" not what someone says what "they" think it's worth...so until the money is in YOUR bank, that is what it's worth.

And I agree with Bobster and that it's "cheap and loose credit" and what the property bulls fail to understand is that those days are now gone.

As I have said before "who controls the money, controls the market", so if you bought into all the recent BS about prices "constantly and consistently" increasing ....best of luck to ya mates !! ps they don't call it "negative" gearing for nothing !

you could post this a 100 times and I bet there a many who will fail to understand what you're inferring to ....

huh what? But my mortgage broker said that prices always went up. He even smiled when I signed the agreement with Westpac for $1,000,000 mortgage... Always go up he said again.. He's such a handsome young man as well.. Always go up...

Always go up

Always go up

Always go up.

Say it enough and even I'm starting to believe it.... Nah, perhaps not. I wonder what the commission is on a $1,000,000 dollar mortgage loan? Always go up, Always go up, Always go up....

Nah still not working.

Ha-ha-ha-ha :)

Get's the commission from selling the mortgage, but when it all goes tits up "not my problem bro LOL".

For immigrants from developing countries, it is brutal economics. Which countries will let me in? How much do I need to pay under and over the table to get in? How long will I need to agree to be exploited to establish myself in that new country? Will I and my present or future family be better off in the medium to long term if I move to that country? If New Zealand on balance offers the best package overall they get the immigrants. We need to decide what the optimum number is and then cap at that. Allocate a certain number to each visa type. If the number for one visa type is not reached the excess can be allocated to the other visa types on ProRata % basis. But the overall agreed cap is not exceeded.

I'd go further and say we need to have a conversation about what our optimal population is. 5, 10, 20 million, what is the target?

Personally, I'd be happy with 5 million. I'd rather not lose what makes this small country unique.

But we're not allowed to have this conversation. As soon as you start, you get shouted down as xenophobic or whatever.

"More New Zealanders are continuing to leave the country permanently or long term than are arriving back after extended stays overseas, with a net loss of 1386 New Zealand citizens the 12 months to May."

I wouldn't call it an exodus or brain drain of the past, but I would throw a wild guess out there and say that this is the start of a trend that is driven by the high cost of living. Kiwi's will seek a better income to house price/debt balance elsewhere (look at the exodus of Aucklander's to the regions). Less are returning too, what's the point if you can't afford to live comfortably back home, may as well stay put.

Living costs are the same in equivalent countries - I'm in one now. And I suspect the conversation, inter-generationally, is the same in them too. Not much point in migrating to the same problem, but there's probably an argument that it is easier to survive on home turf.

As to the question of population, 5 million is probably too many, ex fossil fuels. The sustainable figure is probably 2 million or so. Better less. The indigenous population drew down protein on the hoof (moa), ate each other post battle - and never made 2 million........

Well, given there is plenty of reputable view that the world is really on capable of sustainably supporting a maximum of about 3 billion of us, 2 million here looks about right.

I had often been thinking about the pops problem and wonder if lower head count is better for surviving in a region with limited resources allowed, then why is there not a group of people going it already in some remote part of the world??? Then it hit me that is because with lower pops you might get wiped out by other invading human groups with higher head count. So while is nice that if nobody invades anybody then yeah low pops is the way to go but..... with the world as it is, it may be just wishful thinking that we in nz will not get invaded in an all out war. Anyway not that we matter against the other big world powers anyway :)

OK – let’s throw it to the wind - if we annualized May’s number we get around 28,000 pa net gain – although quite what we are “gaining” could be open to debate.

So we are in Labours target range all things being equal – and all things being somewhat simplistic.

So next stop – Winnie’s 10,000 just around the corner?

Election promises ticked!

Labour have got no immigration target. The drop is mostly due to more kiwis leaving, much less so because of fewer immigrants arriving. Please read the article

Oh dear oh dear - clearly the comment is in jest.

Speaking of reading articles before commenting - how did you go with that April 1st one - I recall someone enthusiastically posting without obviously reading the article or prior comments.

Most fessed up - but the someone didn't catch on for some time, and then rewrote their piece.

^^LOLdgz^^

Sold this week 2 Pere Street, Remuera $4,250,000 http://www.boulgarisrealty.com/listings/18863198/

In the market this week 2 Arney Road, Remuera CV $8,800,000

https://www.bayleys.co.nz/1751563

I knew you wouldn’t let down......you certainly know how to please...

#sadpropertypornaddict

Just for you Boobster ^^LOLdgz^^

You certainly know how to please me.....don’t you dare stop!

#sadpropertypornaddict

Yesterday was Xiazhi (夏至 Summer Solstice) in Chinese. Ancient Chinese believed that the sweating days of summer only came after this day. Does it still hold true for you Boobster?

https://buff.ly/2tdhdeM

Look, let’s not pretend I’m in this for your conversation, I’m only here for your property porn....so yummy

#sadpropertypornaddict

Ok grumpy here it is...

https://rwremuera.co.nz/auckland/remuera/9a-komaru-street-19168707/

^^LOLdgz^^

Sign..... more property porn from you know who -.-

https://edition.cnn.com/travel/article/chengdu-hotpot-all-you-can-eat-c…

Is this the real reason you are back?

No Matter how you Slice it , The fact that there is a net gain of 66,000 people pa means more demand on housing , be that rental or ownership.

This simply means that the pool of available houses will not cope with increasing immigration and organic growth.

The additional 350 extra houses pa that Fletcher intends to build next year from prefab ( some labeled as KB) is a piss in the sea -- Auckland alone might require an additional 3000 units by then to accommodate last year's arrivals !!

At the current intake rate, and the lack of serious action by this Gov ( let alone pissing existing landlords and developers off) we will have a real housing crisis at the end of this CoLs' term in 2020.

These are the products of our immigration growth thus far ^^LOLdgz^^

Auckland's filthiest food joints revealed with stomach-churning photos

https://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=12076007

Special mention:

Wan Fu Yuan, Howick

Wong Kok Café & Bar, Auckland CBD

Chinese Claypot Rose, Auckland CBD

Smith and Wong Chinese Takeaway, Massey

Jiale Bun Shop, Northcote

Do they smell 'immigration' to you Boobster, HO my friend?? ^^LOLdgz^^

Half must be owned by your mates/contacts...

Hopefully you don't bring more along

Hopefully I'll bring all my filthy immigrant mates to live next to you ^^LOLdgz^^

Are you already sick of living with them..

That would explain your eccentricity

I am now back in the country HO my friend. More importantly, back to Double Glamour Zone ^^LOLdgz^^

Ah that is a coincidence you arriving and filthy people.. wow

What is double glammar zone? Seriously, I don't understand what your user name is all about.

I mean nowhere in Auckland strikes me as that glamourous, save a small slice of Takapuna I guess.

Certainly not Queen Street where a pickpocet tried to steal my phone this week.

If pickpockets are active there should be notices warning of the risk.

My goodness – the quality of interest.co.nz has certainly reached new heights.

The owners and advertisers must surely be delighted.

This is high calibre stuff indeed – well done.

These headlines are cruel to the math illiterate - the immigrant population is STILL GROWING.

The problem is we have very low Gdp growth, low productivity, yet we continue to allow high immigration.

All we are doing is dividing our wealth between more and more people.

AndrewJ the problem with your argument is that to achieve certain things as a nation we need to get to “critical mass”. With auckland population at 1million rapid transit is not an option, at 5million its a necessity. Productivity gains follow. Same philosophy applies to all manner of things. The flip side of the argument, is do we want this for NZ? I would say yes. However many (especially those on interest.co.nz) kiwis appear to not want change.

I just don’t buy this “critical mass” argument. Copenhagen has 600,000 people, Amsterdam has less than 1mill, this doesn’t seeem to have held these places back? I suppose you can argue about cities vs metropolitan centres, but both these places run rings around Auckland as urban centres. They have fewer people than us but better ideas

Just been on a see Europe holiday and was impressed by:

Frankfurt 763,000

Basel 175,000 (great rapid transit by the way)

Lucerne 81,000

Toulouse 466,000

I have lived in London and New York and visited Manila - my preference is for a small city. Plenty of evidence that most citizens prefer a large town / small city; maybe students like to live like termites but families prefer something smaller.

To make it as simple as possible the bigger Auckland becomes the less I like the place, the wealthier as a home owner I become and the productivity per capita goes down. Maybe Auckland is unique in having a minimal agglomeration productivity effect; other international cities do far better (compare with Leeds for example).

And if I am wrong they why not scrap all immigration rules and let Auckland reach 50 million (5 milion is way too small in the modern world - Shanghi, Mexico, Bombay, Manila).

Living costs are not the same. Your purchasing power goes far further in a white collar job in Melbourne, Sydney, Brisbane even London than it ever does in Auckland its well documented.

Living costs are not the same. Your purchasing power goes far further in a white collar job in Melbourne, Sydney, Brisbane even London than it ever does in Auckland its well documented.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.