By Gareth Vaughan

The Reserve Bank of New Zealand (RBNZ) is likely to be participating in stringent pre-Christmas stress tests of Australia's big four banks ordered by the Australian Prudential Regulation Authority (APRA) amid growing concern about the European sovereign debt crisis.

Both APRA and the RBNZ declined to comment on an Australian Financial Review report saying APRA has given the banks a week to model the impact of a worst-case scenario of the European debt crisis causing a global recession and hard economic landing in Australia's key trade partner, China. The scenario reportedly includes a 12% unemployment rate (compared with an official Australian rate of 5.3% in November), 30% fall in house prices and 40% drop in commercial property values.

Spokespeople for both the RBNZ and APRA directed interest.co.nz to previous articles and speeches by the regulators that cover stress testing with APRA's spokesman pointing out it sometimes coordinates stress-tests with both the Reserve Bank of Australia and RBNZ. In its Financial Stability Report released in May this year, the RBNZ discussed an APRA-led system stress testing exercise for the Australasian banking system, which included the four biggest New Zealand banks - ANZ, ASB, BNZ and Westpac - given they're "significant parts" of their Australian parents' balance sheets.

The APRA stress tests come at a time of heightened concern about the Western European banking system and concern Australasia's big banks could potentially be shut out of key overseas wholesale funding markets for some time.

Liquid assets

The major banks also run their own, internal stress tests and sit on billions of dollars worth of liquid assets, including the likes of cash, Treasury bills, bank bills and residential mortgage backed securities with the idea being these can be quickly converted to cash if and when necessary.

The banks detail some of their risk management policies in their general disclosure statements (GDS). In perhaps the most detailed account, ASB says key aspects of its liquidity and funding risk include; That one week crisis net cash flow maturity run-off must be positive by more than NZ$1.5 billion, one month net cash flow maturity run-off must be positive by greater than NZ$1 billion, and its core funding ratio must be at 72.5%, 2.5% above the RBNZ mandated minimum of funding that must meet the definition of stable core funding, - that is this percentage of the bank's funding that must come from retail deposits and/or wholesale sources such as bonds with durations of at least 12 months.

ASB's latest GDS notes liquid assets of NZ$9.6 billion as of September 30, which as a percentage of total funding comes in at 17.08%.

The country's biggest bank, ANZ New Zealand, had liquid assets of NZ$12 billion at September 30. Westpac New Zealand had NZ$11.12 billion, and BNZ had NZ$6.3 billion.

ANZ, BNZ and Westpac, between them, have the thick end of NZ$9 billion worth of bonds guaranteed by the taxpayer through the Crown wholesale funding guarantee scheme with the guarantee covering some of this money into 2014. On top of this, Kiwibank has a A$250 million bond issue guaranteed. See more on the wholesale guarantee here.

Considering what may go wrong

APRA, meanwhile, describes stress-testing as the process of: considering what may go wrong, estimating the resulting outcomes, and determining the actions that could be taken to minimise or avoid outcomes considered to be "outside the institution’s risk appetite." See more here in this speech from APRA chairman John Laker.

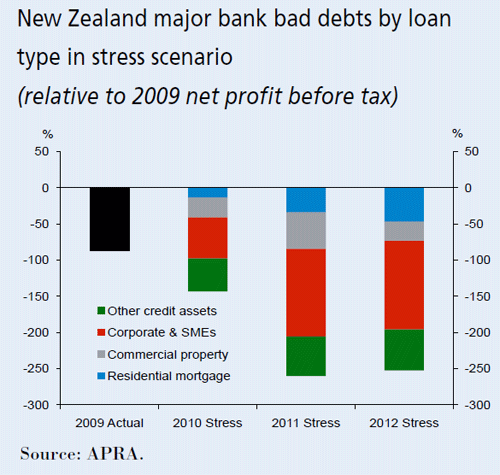

In May's Financial Stability Report, the RBNZ details a previous stress scenario used for New Zealand. This involved GDP contracting by 2.3% in 2009/10, an unemployment rate of 9.8%, and an 11.4% fall in house prices. This improved to GDP growth of 3% in each of 2010/11, and 2011/12 with unemployment down to 9.7% and 8.9%, and house prices falling 6.6% in 2010/11 and rising 0.3% in 2011/12.

The central bank says the big New Zealand banks' return on assets over the three years was near to zero and slightly worse than their Australian parents. (See the chart below from the May 2011 FSR)

"The weak return on assets reflects significant loan losses over the three years. Residential mortgages, which represent about half of all New Zealand lending, are relatively resilient. Losses come more from SME (including farm), corporate and commercial property lending. This is also true in Australia, where overall losses are slightly lower."

This article was first published in our email for paid subscribers this morning. See here for more details and to subscribe.

8 Comments

Plan B – How to loot nations and their banks legally

http://www.golemxiv.co.uk/2011/12/plan-b-how-to-loot-nations-and-their-…

That is an absolute ripper AJ, a must read of the month. It might be length but it is written in such a simple easy flowing style that even a property spruiker could understand it. I would suggest you PM to Bernard.

It really should go hand in hand with Exters Pyramid.

The data is already out there, what you are asking BH for is an opinion.......

The big 4 are exposed IMHO.....the problem is its a mono-culture ie they are the same businesses, exposed to the same risks in the same way....so ppl should move away from the mon-culture risk. Maybe TSB as a NZ bank is way less exposed in the same way as the big 4....maybe....

regards

Read my post in response to AndrewJ above. Great links and reinforces my call to get out of the banking system while you still can.

How about a Stress Test on Borrowers? Invoke the clause in clients mortgage documents and ask them to repay immediately. Do this on, say, 10% of customers - just for fun. This would bring into stark contrast how big that home mortgage really is. And get lots of re-financing going

Maybe they would be more grateful for a nice 30 year term ... with drip feed payments....

Nothing is secure and safe in life, I fail to see why I as a tax payer have to guarantee OAPs income beyond the OAP. Its simple be responsible for yourself....

Otherwise there is a real indication that the RBNZ and Govn is intent on taking away the intrinsic guarantee the Govn has to put behind banks to prevent bank runs....this is supposed to protect voters and tax payers from almost un-limited liability that will kil the economy let alone kill it aka Ireland. Becareful what you wish for because what you want means that the OAP could be cut as NZ has no money to pay it if we have to do like Ireland.

If you want a Govn guarantee then Govn bonds are possibly safer....short term...< 2 years.

I would suggest you open at least 2 bank accounts, say TSB and Kiwibank for instance, and make sure you can do Internet banking betweeen them.

regards

Your funds have never been secure in a bank, just relatively very secure.

The RB regulates the retail and commercial banks but works within the limts set by our elected Govn. This is the successive Govn(s) you voted for, blame yourself.

"finance law" cant determine what you are trying to say,

If you mean the present housing bubble then houses are presently 50% over-valued...if you applied an 80% limit on that 50% then you end up at a 60% deposit.....and you would kill the housing industry dead because first time buyers would cease to exist and send us into a severe resession. Not to mention that these young professionals / workers would bugger off to OZ or anywhere where they have a chance to own theor own home.

So I think not.

regards

"You think you money is not at risk in the banks ? Think again, learn the lesson from MF Global where 400,000 people with accounts have seen their monies vanish into thin air because the small print allowed MF Global to gamble with their client monies despite being in segregated accounts..

So the head of the French Central bank is deliberately trying to push markets attention away from the fact that the crisis has reached a critical point and trying to ignore that both France and Germany are directly responsible for the euro-zone debt crisis because BOTH countries themselves broke the fiscal rules as contained within the Maastrict Treaty right near the very start of the Euro currency and thus gave the green light for others to also go on a borrowing and spending binge on low interest rates.

The risks of a collapse of the banking system most definitely are with a trigger out of the Eurozone and particularly France than the UK, therefore the credit ratings agencies whilst being several years behind the curve are correct to see the credit risk of French debt as being far, far higher than that of the UK for it does pose a severe risk as evidenced by rising French government debt market interest rates.

But what the credit rating agencies appear blind to is the fact that no government would be able to escape the consequences of a collapse of the euro-zone or default of the debts of any major economy, even Greece leaving the euro-zone could be enough to trigger banking system collapse as they would all fall like dominoes one after the other eventually including even the worlds reserve currency holder, the United States, in which case maybe a downgrade of France could be the trigger that starts a cascading collapse of the eurozone which explains the panic in Paris. If France becomes Italy overnight then where does the money come from for all these ever expanding bailout funds? Throw France also in the mix and the bailout pot required would extend to at least Euro 5 trillion which Germany as the last euro man standing is just not big enough to bailout everyone!

So France instead of putting several hundred billions of euros into the bailout pot, may find itself after a credit ratings downgrade seeking several hundred billions in bailout funds itself in a matter of months, especially as it has about as much debt requiring refinancing during 2012 as Italy (about Euro 400 billion)."

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.