NZ finance companies face cash squeeze, S&P warns (Update 1)

8th Apr 10, 11:42am

by

New Zealand's non-bank deposit taking sector will continue to face challenges for a while yet, as they struggle to deal with a lack of new investment and the need to raise cash from maturing loans, credit rating agency Standard and Poor's (S&P) said. (Update 1 includes S&P ratings list from release.) Here is the press release from Standard and Poor's:

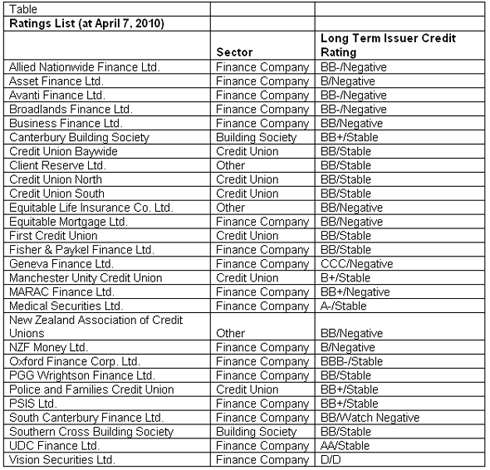

Melbourne, April 7, 2010—Standard & Poor’s Ratings Services said today New Zealand’s non-bank deposit taker (NBDT) sector will continue to face challenges for a while yet, mainly due to its susceptibility to liquidity and funding risks. This is according to a commentary titled “For New Zealand’s Non-Bank Deposit Takers, Liquidity Is Still A Primary Credit Concern,” published today. Standard & Poor’s credit analyst Peter Sikora said that while the sector’s asset quality problems are showing signs of having peaked and regulatory oversight has improved, most NBDTs have limited or no back-up external liquidity in the form of committed bank or other funding lines. “To meet liquidity requirements, most NBDTs are forced to rely heavily on loan principal and interest inflows and the active management of new lending outflows,” said Mr. Sikora. “Many also have material liquidity gaps in their maturity profiles that will need to be carefully managed to avert liquidity pressure in the future. These liquidity gaps also make some NBDTs even more sensitive to the emergence of any new industry or company-specific credit pressures.” Mr. Sikora also notes that when the Crown Retail Deposit Guarantee Scheme was introduced October 2008, it played a critical role in averting the sector’s total collapse after a sharp drop in debenture reinvestment. Although some NBDTs have attracted debenture investments beyond the initial guarantee period (which was to Oct. 12, 2010) most maturities continue to fall within the guarantee period. This underpins our refinancing-risk concerns for the sector. The scheme has now been extended to Dec. 31, 2011, with new eligibility criteria and fee structures, and we expect this will support the liquidity and funding profiles of NBDTs covered through the extension period. The NBDTs most vulnerable to liquidity and refinancing risks are those not covered by the deposit guarantee scheme through the extension period, either because they are not rated or they are rated below ‘BB’ (see list below). Reinvestment rate success beyond the October 2010 expiry date represents a critical rating and credit factor for these entities. Our concerns are reflected in the negative outlooks we have on most NBDTs rated below ‘BB’. “We note, however, that many lower rated finance companies continue to have long-established debenture investor relationships and there is evidence that debenture investors may continue to support them even if they’re not covered by the deposit guarantee scheme,” said Mr. Sikora. In the short-to-medium term, the modest business-risk profile of most NBDTs limits the potential for ratings to be raised—even if there were a sustained moderation to some financial risks. Specifically, most NBDT are small, geographically highly concentrated, and have a narrow business focus. Although many have good business positions across certain asset classes, the operating environment remains competitive and these market niches provide little competitive advantage. We are somewhat comforted by evidence that most NBDTs have sought to fortify their capital positions and buffer against possible losses on problem loans. That said, liquidity and refinancing vulnerabilities continue to trouble our view of the sector’s creditworthiness and are likely to result in further company failures and consolidation.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.