The start of a new year is a good time to review how the last year went. That’s true in many things, from health and fitness to relationships and investments.

With all the wars, natural disasters, and cost of living rises, there was much to dislike about 2024. Nevertheless, for Australian investors the financial returns at least were quite respectable.

The three types of investment that dominate the portfolios of most Australians are the Australian share market, superannuation, and residential real estate.

According to CoreLogic, the total value of Australian residential property now exceeds A$11 trillion. That dwarfs the A$4.1 trillion value of Australians’ superannuation balances and the A$3.3 trillion capitalisation of the Australian share market.

But how did the returns on these different investment categories compare in 2024?

Superannuation research house SuperRatings recently provided its estimate of superannuation fund performance last year. It estimates that the return on the median ‘balanced’ super fund option was around 11.5%. (A balanced option is one with a mixed portfolio spread across a range of investments and with 60-75% of its funds invested in growth assets like Australian and international shares and private equity. It is the most popular choice among Australians.)

SuperRatings says that ‘the vast majority’ of balanced funds would have returned over 10% in 2024 with the best performers returning more than 12.5%.

Australian equities produced a comparable result. Taking into account both capital growth and dividend income, the domestic share market was up 11.4%. Obviously, returns varied dramatically between different sectors within the market. Australian banks performed particularly well.

Those Australians with exposure to the US share market last year were big winners. The S&P 500 had another great year which partly explains why in 2024 Australians spent a record $5 billion investing in exchange traded funds focused on US equity markets.

(For those invested, or looking to invest, in Wall St, a fascinating read is ‘On Bubble Watch’, the latest epistle from investment guru Howard Marks of Oaktree Capital.)

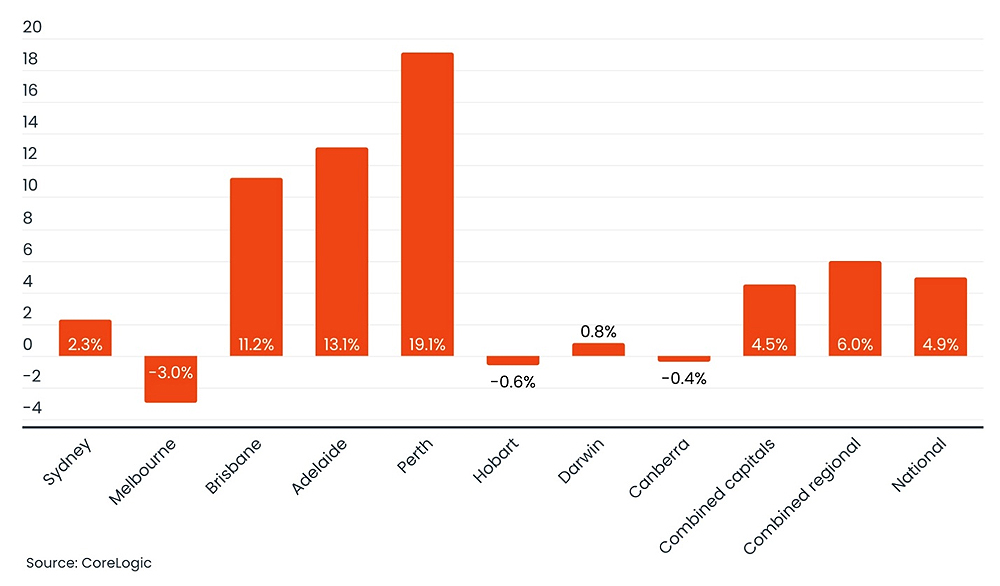

The Australian residential real estate market underperformed both the Australian share market and balanced superannuation in 2024. According to CoreLogic, it returned 8.3%, including both capital value growth and rental yield. That’s still not a bad return and well ahead of inflation of around 3%.

Of course, there were wide variations in housing markets across the country. There was a world of difference between booming Perth with annual growth of 19% and moribund Melbourne that saw a decline of 3%.

CoreLogic Home Value Index - annual change to 31 December 2024

Where to from here for the share and residential property markets?

It’s impossible to know with equities which are historically far more volatile than residential property. Some commentators predict another good year for the Australian share market, based in part on the assumption of interest rate cuts in the first half of the year. But the outcome will ultimately be driven by a range of unknowables including the result of the next federal election and the impact of a Trump presidency on international trade and the Chinese economy.

And if there’s a major correction in US equity markets, the Australian market will follow suit irrespective of what’s happening in the Australian economy.

By comparison, the direction of Australian residential property is easier to predict. Nationally the trend over the last twelve months has been declining price growth which is now tipping over into negative growth i.e. falling house prices.

In other signs of a softening market, nationally both listings levels and selling times are higher than a year ago.

In the words of CoreLogic economist Kaytlin Ezzy

Despite showing some resilience in the first half of the year, the accumulation of stock, and the higher for longer interest rate environment has seen the change in dwelling values slow, and, in some cities, shift into negative territory.

The national decline in December was driven primarily by declines in Sydney (0.6%) and Melbourne (0.7%) but the softening was nationwide.

These results partly reflect the passing of the peak in the housing rental boom. The December quarter saw the smallest rise in rents since 2018.

The biggest single factor for house prices is interest rates. That’s where the Reserve Bank of Australia plays a key role. To date it has resisted lowering the cash rate in order to keep a lid on inflation.

The Labor government of Anthony Albanese faces an election by May and is desperate for the RBA to cut rates before then. There was growing expectation of a rate cut at the next RBA meeting in February, however this week’s employment results may have reduced that prospect. The market was anticipating employment to grow by 15,000 in the month of December but the actual figure was more than 56,000.

With unemployment still at a relatively low 4%, the RBA may decide to wait for clearer evidence that inflationary pressures in the economy are subsiding. The risk is that in the interim a falling Australian dollar will lead to more imported inflation.

For the moment, most analysts are forecasting an RBA rate cut by May at the latest. Assuming that occurs, any downturn in the residential real estate market is likely to be modest. But a repeat of 2024’s positive return of 8.3% is looking increasingly unlikely.

*Ross Stitt is a freelance writer with a PhD in political science. He is a New Zealander based in Sydney. His articles are part of our 'Understanding Australia' series.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.