New Zealand's a country where storms, high winds, heavy rain, sea swells, earthquakes and volcanoes are all too well known. With a growing population, some housing and other buildings in dicey locations, and soaring insurance premiums, could there be better - or at least additional - insurance options?

Two major international bodies, the International Association of Insurance Supervisors (IAIS) and the Bank for International Settlements (BIS), the central banks' bank, are making a case that there are.

They set this out in a new paper, Uncertain waters: can parametric insurance help bridge NatCat protection gaps? (NatCat being short for natural catastrophe).

In NZ this is against a backdrop of hugely costly extreme weather events last year. According to the Insurance Council of New Zealand (ICNZ), by June 1 this year some 112,746 of 118,037 private insurance claims from the 2023 Auckland Anniversary weekend floods and Cyclone Gabrielle were fully settled at an estimated total cost of $3.8 billion.

Meanwhile, rising insurance premiums have made a notable contribution to the high inflation of the past couple of years. According to Statistics NZ data, dwelling insurance premium costs rose 22.2% in the September year, contents 19.6% and vehicle insurance premium costs climbed 19.5%.

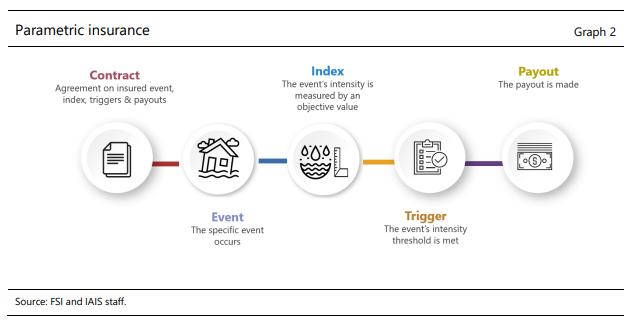

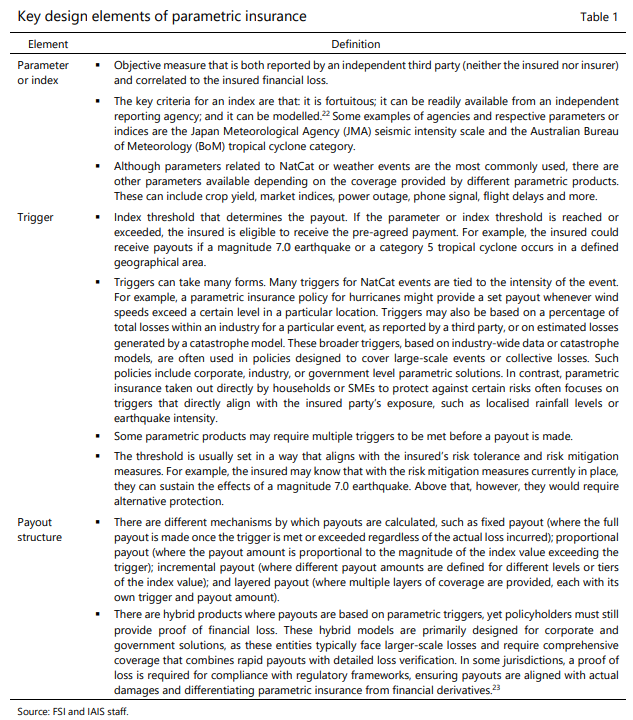

Parametric insurance first came to my attention in an Of Interest podcast with David Hall, Climate Policy Director at Toha, hot on the heels of last year's Auckland floods. It's a type of insurance contract that insures a policyholder against the occurrence of a specific event by paying a set amount based on the magnitude of the event, as opposed to the magnitude of the losses as with a traditional indemnity policy.

It came up in another podcast a few months later, this time with Tower Insurance CEO Blair Turnbull. Tower, he said, believed parametric insurance could be useful in NZ in areas with; "higher propensity for flooding and cyclones and where traditional comprehensive insurance may become too expensive for some households and communities. We would like to explore the option for offering parametric cover."

The IAIS and BIS paper comes on top of another one from the IAIS; A call to action: the role of insurance supervisors in addressing natural catastrophe protection gaps. NZ's insurance supervisor/regulator is the Reserve Bank (RBNZ).

The IAIS and BIS suggest parametric insurance, or index-based insurance where payouts are determined by an index such as average rainfall or crop yields over a specified period or region, can be useful. As can disaster microinsurance such as products targeted at vulnerable industries like fishing in South East Asia. They suggest the likes of the RBNZ can help by creating regulatory sandboxes, or pilot project frameworks, where insurers can test new insurance products on a limited scale.

'Limitations'

So does the RBNZ think parametric insurance is a good option for NZ?

"Whether or not parametric insurance is subject for prudential supervision [by the RBNZ] depends on its design. It may be a good option in certain contexts, for example crop insurance against well-understood weather risks. However, it also has limitations, such as the potential for under or over-insurance, and the variation in indemnity effectively provided from one property to the next," a RBNZ spokeswoman says.

And what about disaster microinsurance in a NZ context?

"Having a diverse range of insurance products that suit a range of needs is desirable. The prudential rules do not favour one type of product over another, and seek to ensure that our regulations are flexible enough to apply to a range of products and business models, while ensuring a base level of financial soundness."

And is the RBNZ up for creating regulatory sandboxes?

"We do not have plans to consider a sandbox for prudential requirements. Rather we have elements of proportionality in place (weaker, simpler requirements for smaller insurers), and proportionality will be a key consideration as we progress the review of the Insurance (Prudential Supervision) Act and prepare advice for the Government," the RBNZ spokeswoman says.

'I wouldn't say it's imminent'

And what about the insurers themselves?

Tower, which pioneered risk-base pricing in NZ for the likes of floods, earthquakes, landslide and coastal hazards, is also working on parametric insurance in the South Pacific.

Tower launched a cyclone response cover parametric insurance product in 2022, now available in Fiji, Samoa and Tonga. Tower Chief Underwriting Officer Ron Mudaliar says whilst the insurer sees potential for parametric insurance for the likes of cyclones, heavy rainfall and possibly drought in Fiji, Samoa and Tonga where it has worked with the United Nations Capital Development Fund, there are key differences between the insurance market there and in NZ.

In NZ, in excess of 90% of people insure their homes via traditional indemnity insurance, Mudaliar, says, while in Fiji this is 10% with only 3% or 4% having cyclone cover for their homes. In the Pacific Tower says parametric insurance offers a lower-cost alternative providing a level of cover for communities that may not benefit from traditional insurance.

"I wouldn't say it's imminent [Tower offering parametric insurance in NZ]. So we'd be doing a whole lot of work this year for the background stuff and we might come up with a product later next year. I'm not guaranteeing that, but it's definitely not in the first half of next year," Mudaliar says.

"There's a bit of work for us to do to complete the Pacific in terms of where we're at ... and then for us to think about how we bring a product in, what is that product, how do we price it, and then we've got to put them [products] to the scalable platform."

Tower has been talking with a couple of iwi groups, he adds, starting from the basic point of what is their need for insurance.

In terms of regulatory sandboxes, Mudaliar says Tower doesn't need need any help from the RBNZ.

"No, we don't really need the RBNZ. Obviously we want to be very transparent in what we're doing and we want to do the right things for any product development."

"So we need to think about what we do. But it's not in our interest or the public interest for the RBNZ to make innovation too easy either," says Mudaliar.

NZ needs to 'improve how we manage our natural hazard risk'

A spokeswoman for IAG NZ says at the moment, the best protection it can provide is via the insurance products it currently offers.

IAG NZ is NZ's biggest general insurer through the AMI, State, NZI, NAC, Lumley and Lantern brands, plus the general insurance products sold by ASB, BNZ, Westpac and The Co-operative Bank.

The most important thing NZ can do, she says, is improve how we manage our natural hazard risk.

"The country’s approach to natural hazards favours response and recovery over investing in risk reduction and resilience, and this approach is not keeping pace with the growing risk. The result is watching some of our most exposed communities being repeatedly devastated by natural hazards. While these communities show great resilience, the emotional toll that these events take on New Zealanders is all too apparent," the IAG NZ spokeswoman says.

"As these risks grow, we are also thinking about how our insurance products need to evolve – including the role that possible new products, like parametric insurance, might complement what we already offer. We will share more with you about any possible new initiatives as new offerings come to market."

Reducing risk in our most hazard prone communities "is the only way to keep people and property safe and insurance affordable."

"We are advocates for targeted and practical steps that will reduce risk, including stronger, more consistent planning rules and greater investment in infrastructure," the IAG NZ spokeswoman says.

"Our annual Climate Change Poll shows that 45% of New Zealanders believe that risk-based pricing is the fairest way to price home insurance, 8% think that community pricing is fairest and a further 40% say that a mix of the two is fairest."

"Most insurers currently use a combination of the two approaches when setting premiums for home insurance. However, as the cost of natural hazards grow, insurers will increasingly apply a risk-based pricing approach. This will increase premiums for people in high-risk locations and reduce them for people who live in low-risk locations. This is why it is important that we put more focus and resources into reducing natural hazard risk. This will not only keep people safe but also help to keep insurance affordable."

A recent report from Parliament's Finance and Expenditure Select Committee recommends a national climate adaptation framework establish a “clear mandate” for local and central government when it comes to adaptation resourcing and financing arrangements. It says a proactive approach is needed, with “all actors” incentivised and able to act on climate adaptation.

'We’re conscious of the impact of these cost increases on our customers'

A spokeswoman for Suncorp NZ, which includes Vero Insurance, Vero Liability Insurance and AA Insurance, says inflation and rising reinsurance costs have put pressure on premiums across the insurance industry.

"We’re conscious of the impact of these cost increases on our customers and are focussed on mitigating these where possible, including working with brokers and partners to design and test potential solutions, including parametric alternatives. Customer reaction to these products has been mixed, due to factors including concerns about coverage limitations or policy exclusions," the Suncorp spokeswoman says.

"At this stage we are working with and encouraging the industry to work with, local and central government on resilience building measures, mitigation of natural hazards and not building in inappropriate places in an effort improve the NZ Inc risk profile."

"As part of Suncorp Group, we’re able to access reinsurance at a greater scale and help spread our risk across perils, and a larger customer base. These steps help us to mitigate premium increases while continuing to deliver a high standard of coverage. While there is no silver bullet, we will continue working on new options to support our customers and promote enhanced insurance affordability," says the Suncorp spokeswoman.

'Indemnity reinsurance is currently the best match for NZ’s specific situation'

In comments attributed to its Chief Executive Tina Mitchell, the Natural Hazards Commission, formerly the Earthquake Commission, says a purpose of the natural hazards insurance scheme is to manage the Crown's financial risk from natural disasters. Having the scheme in place also supports the availability of catastrophe insurance for residential buildings for New Zealanders, more generally, says Mitchell.

"The Treasury is responsible for advising the Government on these types of systemic issues. The Natural Hazards Commission Toka Tū Ake (NHC Toka Tū Ake ) advises the Treasury on the likely cost of providing natural hazard insurance now and over the coming years. This cost is influenced by our evolving understanding of the risks we cover, as well as changing costs."

Mitchell notes the Natural Hazards Commission issued a catastrophe bond in 2023.

"We continue to look at developments in the broader reinsurance market to determine whether there are products that would help NHC Toka Tū Ake. For example, between 2016 and 2019 we put in place an 'aggregate cover' which allowed NHC Toka Tū Ake to group together all losses incurred over the three-year period. Once a pre-specified limit had been reached, NHC Toka Tū Ake was then able to claim for any further losses," says Mitchell.

"We have also looked closely at the potential role for parametric reinsurance but have concluded that indemnity reinsurance is currently the best match for New Zealand’s specific situation, as it mirrors the way in which our legislation responds to events and how it determines we settle claims."

*This article was first published in our email for paying subscribers first thing Tuesday morning. See here for more details and how to subscribe.

13 Comments

Insurance is becoming unaffordable and changing the payout in relation to premiums collected will not make it any more affordable....essentially this is even less protection (ability to return to the previous state) than the current model. As that ratio continues to move more in favour of the ICs (to keep them viable) less and less will see any advantage in purchasing their 'product'...unless of course required by statute, but then that wont fulfill its intended purpose of insurance either, unless the purpose is the survival of the IC shareholders.

Insurance companies aren't considering parametric insurance out of the goodness of their hearts - they've seen a gap in the market that could be profitable to fill. Parametric insurance would make building in unwise places less financially risky. It could inadvertently increase costs to New Zealand in the long run by providing incentives not to retreat from or reduce investment in high-risk areas.

Risk based pricing gives a price signal to the market - as premiums go up, the value of properties in high-risk areas goes down. That is as it should be. An alternative is for the taxpayer to be on the hook for managed retreat from a property the price of which does not account for the hazard versus one that is worth little because of the hazards present.

I prefer risk-based pricing.

*edit for clarity

I doubt anyone thinks ICs operate out of the goodness of their hearts (do they possess one?)....rather my comment was to question whether parametric policies make the concept of insurance any more viable than the current offerings....I would suggest not.

You missed my point. I was asking Qui bono? Not New Zealand, so it's not something to get excited about at the macro level. I was agreeing with you.

Upon rereading I now see....had misunderstood your preference statement.

we have (or had) an EQC levy applied to help fund the chch earthquake, it feels like the same thing but obviously far less targeted.

The main problem is that insurance companies are demanding bigger and bigger profits. Major catastrophes are calculated into their premiums but when they don't occur and claims don't swallow up the premium income, the remainder is raked off as profit when most at least, should be squirrelled away to provide for the times when the rare, major events do occur.

In short insurance has become a rip off, not a service that benefits society. Governments should rigorously regulate the industry.

Insuring a policyholder against a specific event is great idea - dropping baggage from travel insurance drops the premium by about 80%. Why pay for baggage loss fraud when you don't have to?

Which destinations do you travel to without baggage?

Take it, just don't insure it.

The funeral parlour?

Surprised that you can omit baggage from your travel insurance if travelling overseas.

For a house you certainly can' t omit items like sheds and decks. I'd even risk not insuring a separate standalone garage.

More excuses for large insurance companies and major underwriters to increase their profits even more.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.