Credit rating agency S&P Global Ratings says the reinsurance sector continues to struggle to earn its cost of capital as natural catastrophe losses and other factors mount.

In a new report S&P notes it has a negative view on the reinsurance sector describing its performance over the past five years as "dismal."

Reinsurance, or insurance for insurers, allows insurers to transfer some of their risk to other parties to reduce the likelihood of paying up large for an insurance claim. The sector has experienced a tough few years. In an episode of interest.co.nz's Of Interest podcast in July, Tower CEO Blair Turnbull said they were now "questioning whether they want to be down under."

S&P says the reinsurance industry has a poor track record when it comes to earning its cost of capital, defined as the weighted average cost of capital.

"Reinsurers failed to surpass this hurdle in the past five years (2017-2021), except in 2019, and 2022 looks set to continue this trend. As central banks hike interest rates in sync to tame inflation, reinsurers' cost of capital is also rising, making their job even harder," S&P says.

"In 2017 and 2018, the reinsurance sector generated returns on capital of only 3.2% and 2.0%, below its 7.4% and 7.9% cost of capital, respectively. Natural catastrophe losses, loss creep, and investment market volatility in fourth-quarter 2018 all played significant parts in these results. However, the improved investment returns in 2019 helped the sector earn in excess of its cost of capital. This meant that the gap between the sector's actual return on capital and cost of capital was positive at 2.9 percentage points."

"In 2020, the sector took a major hit from COVID-19 and natural catastrophe losses, as well as significantly lower net investment income relative to the previous year. In 2021, return on capital improved to 7.7% but still did not exceed the relatively higher cost of capital of 9.1%. The trend will likely continue in 2022 because of financial market volatility. Although underwriting performance in property/casualty and life reinsurance is improving in our base case assumptions in 2022-2023, we believe the sector still needs to demonstrate its ability to sustainably earn its cost of capital before we could potentially revise our view to stable from negative," says S&P.

The credit rating agency does say, however, that the global reinsurance sector could finally be facing a turnaround, with price increases persisting for most insurance lines while property catastrophe lines are experiencing a "full-on" hard market environment.

"The question on everyone's mind, though, is will these pricing improvements be enough to combat the endless barrage of headwinds against the reinsurance sector that have muted returns for years? The combined impact of higher frequency and more severe natural catastrophes, untamed inflation across the world, mark-to-market investment losses eroding capitalization, and the Russia-Ukraine conflict all threaten the reinsurance sector," S&P says.

"As a result, S&P Global Ratings' view on the global reinsurance sector remains negative, reflecting our expectations of credit trends over the next 12 months, including the distribution of rating outlooks, existing sector wide risks, and emerging risks. As of Aug. 31, 2022, 19% of ratings on the top 21 global reinsurers were on CreditWatch with negative implications or had negative outlooks, 76% were assigned stable outlooks, and 5% were on CreditWatch positive."

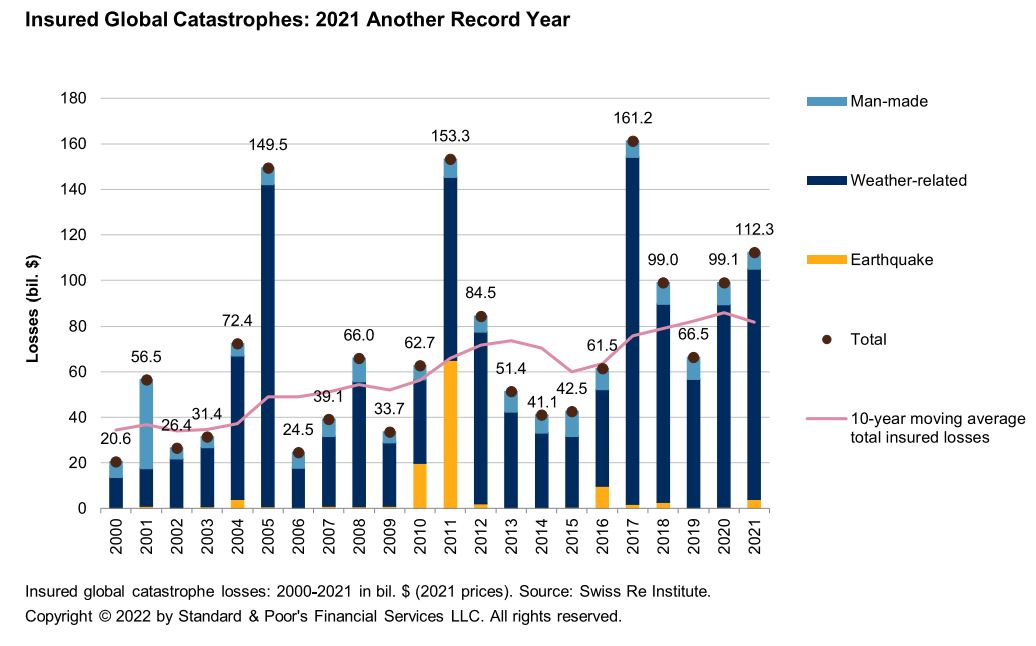

Citing the Swiss Re Institute Sigma report, S&P says in 2021, global economic losses from natural catastrophes were US$270 billion, of which about 40% was covered by the re/insurance industry. These natural disasters caused US$111 billion of insured losses, which were the fourth highest since 1970. S&P also says the top 21 reinsurers are budgeting about US$15.5 billion for natural catastrophe losses in 2022 versus US$13 billion in 2021.

Reinsurers S&P rates include the likes of global giants Munich Reinsurance, Swiss Reinsurance and Lloyd's, plus still significant but smaller reinsurers like Fairfax Financial Holdings, Everest Re Group, China Reinsurance and Qatar Insurance Co.

"This cohort of companies reported US$25 billion in pandemic losses from both property insurance and casualty insurance and life re/insurance in the past two and half years, US$19.1 billion in 2020, US$4.6 billion in 2021, and US$1.3 billion in the first half of 2022. In addition, the top 21 reported US$1.4 billion losses due to the Russia-Ukraine conflict in the first six months of 2022. We believe the situation is still fluid and further losses will be reported in the upcoming quarters," S&P says.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

5 Comments

S&P says the reinsurance industry has a poor track record when it comes to earning its cost of capital, defined as the weighted average cost of capital.

"Reinsurers failed to surpass this hurdle in the past five years (2017-2021), except in 2019, and 2022 looks set to continue this trend.

“There’s no business like insurance business”

According to Warren Buffett the best business in the world is the insurance business. It is the only one with a negative cost of capital. The premium-income collected by the insurance company is put in capital accounts as if it were owned outright. Of course, ultimately that sum is paid out in claims. But in the meantime the insurance company pockets the return to capital $ which is what makes its capital cost negative. Insurance premiums held by the company as reserves before claims are coming in (maturing) is called the ‘float’.In recent years through QE (Quantitative Easing) and ZIRP (Zero Interest Rate Policy) the Fed has succeeded in bankrupting the entire insurance industry. Through a peculiar ignorance of mathematics (in which it is supposed to be eminently strong) the industry has failed to take notice of the capital destruction to which it has fallen victim.

....a rate cut by the central bank destroys the capital efficiency of cash flows. It is no different in the case of the

cash flow of insurance premiums accruing to insurance companies. The latter are hit indiscriminately by QE and ZIRP. Since 2008 the rate of interest has been cut in half several times through the Fed’s open market purchases of government debt. In each instance the capital efficiency of the float has been seriously undermined. As a result the ability of the insurance companies to increase their capital base has been destroyed. The diagnosis is that the industry is a dead man walking. The prognosis is 'sudden death syndrome'. When it becomes known that it has been denuded of capital, the industry will follow Lehman Brothers to Hades (where the god of the dead, Hephaistos, reigns).An ad hominem argument can be made that this scenario is indeed inevitable. The rate of interest is reduced through Fed open market purchases of government debt. Thereafter the account carrying insurance premiums will be compounding at a reduced rate. It will increase more slowly. In addition, the capital efficiency of the industry is ruined. It has to pay more for generating the same premium-income while getting no relief in the form of risk reduction. In effect, the insurance industry is forced to shoulder ever more risks without the possibility of increasing

premium income. Insurance companies are forced by Quantitative Easing, so called, to take ever greater risks just to keep abreast. But there is a limit to this imprudence. At one point the industry will find that it could no longer meet claims. Under ZIRP insurance companies are deprived of any return to assets with no compensation in the form of a reduction of liabilities. Link

ACC announces $8.7 billion deficit for year as interest rates plummet

Similar, but same again next year.:

Falling interest rates

As was the case in 2018/19, interest rates continued to decline, influenced in part by COVID-19. Falling interest rates affect ACC in two keys areas: the valuation of the OCL and investment returns.The OCL is our assessment of the net present value of how much ACC needs today to support already injured clients for as long as they require it. Falling interest rates result in a lower discount rate being applied to our OCL. In 2019/20 this contributed $7.3 billion to our deficit. The single-effective discount rate1 applied to our OCL has an average duration of 20 years. This rate fell to 1.86% at 30 June 2020.

Investment returns for the year were 7.59% ($3.4 billion) after costs. Two-thirds of our investment portfolio is in fixed-interest products. This acts as a partial hedge to the interest rate exposure present in the OCL valuation.

In the past two financial years ACC has recorded $14.6 billion in deficits. These deficits have primarily been driven by economic factors outside ACC’s control. These factors affected the valuation of ACC’s OCL by $16.4 billion.

Although these deficits are not cash losses, they do have impacts on the funding ratio of the levied and Non Earners’ accounts, which in turn affects levy and appropriation requirements. Link: https://www.acc.co.nz/about-us/corporate/

A seriously scary thought if ACC has to take on such risk as noted above. Most of the public doesn't appreciate that the money for the scheme doesn't just come from taxpayer dollars, there are a range of pots of money that service the scheme and which get plucked from.

If reinsurers stop serving 'down under' we're stuffed, EQC is stuffed.

If you don't believe in Climate change effects thats fine.

These guys are on the front line and insurance costs here are ramping at great levels - just getting some insurance is getting harder and very expensive.

Insurance and finance will ultimately cause us all to change as we wont be able to function without a risk cover mechanism.

Reduce your debt asap or face higher interest rates or inability to refinance due to no insurance.

Don't be in high risk natural disaster areas or industries

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.