By Juan Caballero and Wolfgang Fengler*

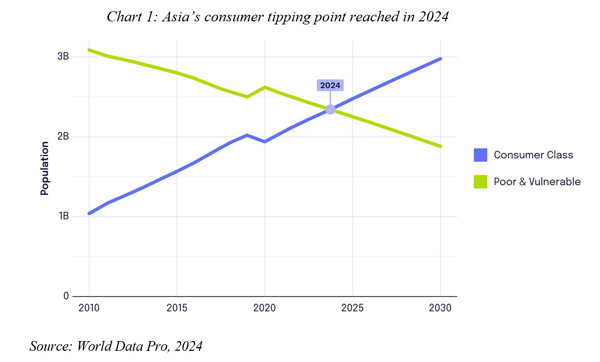

With market turmoil recently capturing headlines, it is easy to lose sight of the long-term forces which have been shaping Asia’s development. While Asian markets, especially the Nikkei, experienced sharp losses in recent weeks, a positive tipping point has been reached as well: for the first time ever, over half of Asia’s 4.8 billion people are part of the global consumer class, defined by the World Data Lab as those spending more than $12 per day in purchasing power parity prices.

The importance of this milestone can hardly be overstated. It marks the transition from poverty to a more typical middle-class lifestyle, where individuals start engaging in discretionary spending on items like motorcycles, gas stoves, and beauty products.

The dominance of Asians in the global consumer class is a relatively recent development. Until 2000, the global consumer class was predominantly Western, totaling 1.7 billion people. In 1980, over 70% of the consumer class was in wealthy OECD countries. World Data Lab estimates that today, almost 60% of the global consumer class is Asian. Asia currently has 2.4 billion consumers and will add one billion more in the next decade, implying that it will account for 65% of the global consumer class. But the Asian consumer is mostly an entry-level consumer, spending on average $20 per day. This means that Asia’s total spending power is currently $19 trillion, roughly 30% of global consumer spending.

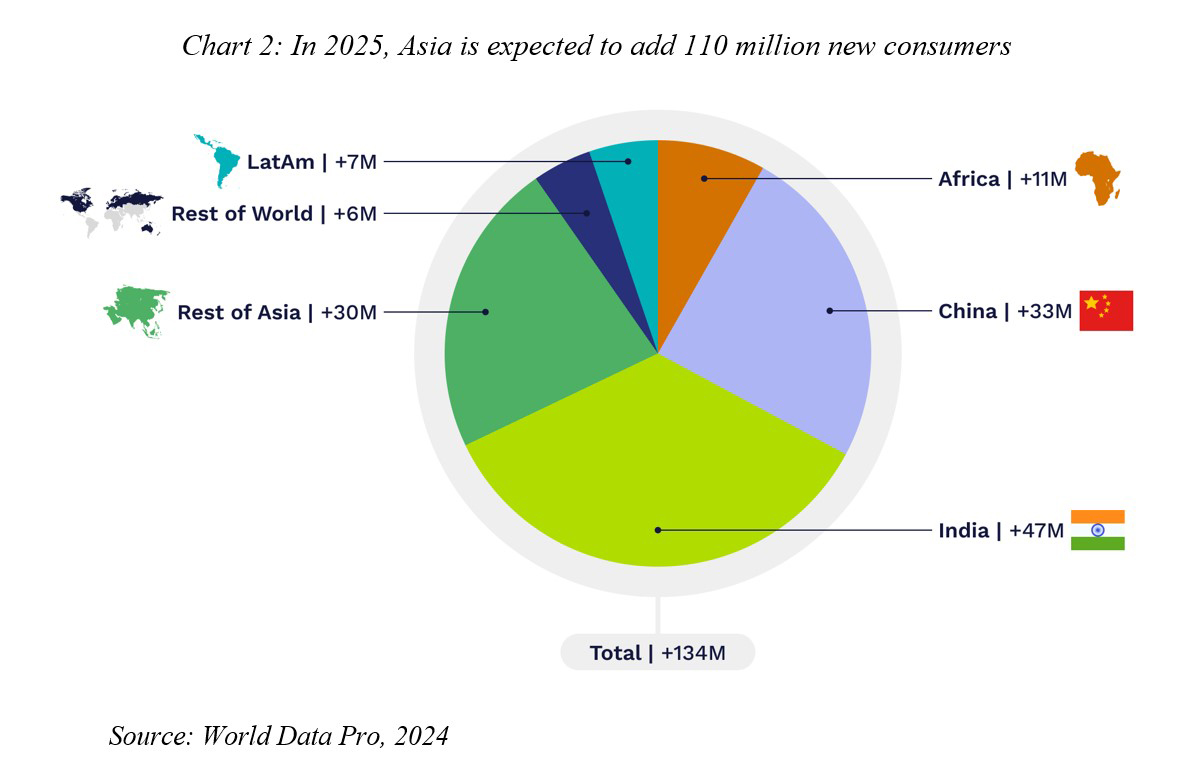

The dichotomy of rapid growth in Asia’s consumer class and only moderately strong growth in consumer spending will continue. In our latest World Consumer Outlook, we project that Asia will continue to lead global consumer class growth, contributing 110 million of the 134 million new consumers expected next year. Additionally, one-third of every additional dollar spent globally will come from Asia.

World Data Lab projects that India will surpass China in adding people to the consumer class next year, with India contributing 47 million new consumers compared to China’s 33 million (Chart 2). Following them are five often overlooked Asian economies: Indonesia (+6 million), Bangladesh (+4 million), Vietnam (+4 million), the Philippines (+3 million), and Pakistan (+2.5 million). In Olympic terms, Asia will dominate the top seven positions among the global consumer class leaders for 2024, followed by the United States, Brazil, and Egypt, respectively.

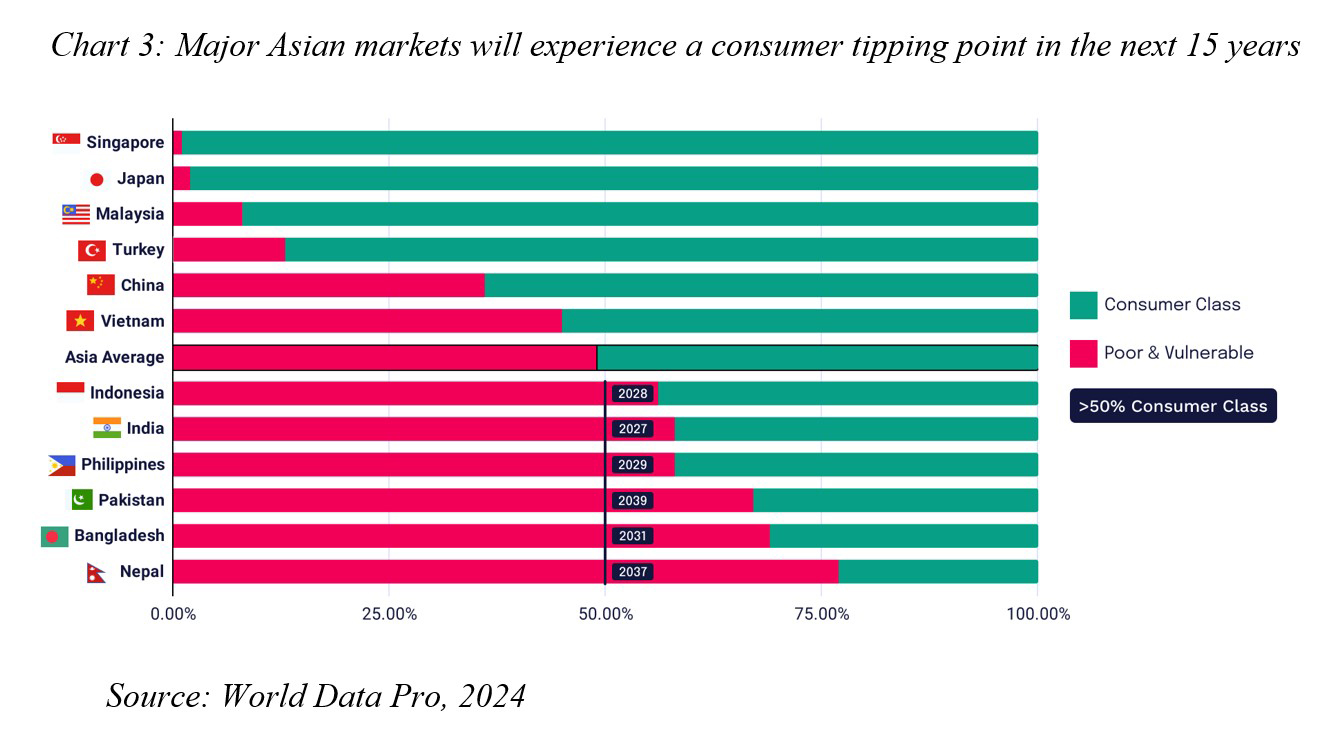

There are still 2.4 billion people in Asia who have yet to enter the consumer class, along with an additional 330 million newborns by 2034. This represents more than half of the world’s future consumers. World Data Lab projects that Asia will add one billion new consumers and $15 trillion in additional consumer spending by 2034. Most countries in emerging Asia, however, have yet to reach the tipping point. China and Vietnam did in the last decade, and World Data Lab projects that India, Indonesia, and the Philippines will soon (in 2027, 2028, and 2029, respectively). Bangladesh, Pakistan, and Nepal will become majority consumer markets only in the 2030s (Chart 3).

While the growth momentum of Asia’s consumer class is strong, the current economic environment is volatile. Recent market turbulence in Asia has raised concerns about investor confidence and the stability of financial markets in the region. But these risks are likely only to delay, rather than derail, the expansion of Asia’s consumer base. Like the COVID-19 pandemic, which similarly interrupted the growth of Asia’s consumer class, these challenges will not stop Asia’s long-term rise in consumer power. The underlying factors driving this growth – longer life expectancy, better education, urbanization – have been put in place over the last decades, and these long-term shifts will influence Asia’s trajectory more than any short-term shock could undo.

Trendlines will prevail over headlines. It is safe to say that China will remain the world’s largest consumer market for seniors, currently at 122 million and growing to 178 million by 2030. By contrast, India will be the largest market for young Gen Z consumers, growing from 150 million today, about as large as in China, to 215 million in 2030. Global consumer goods companies should bet on Asia. If you bet against demographics, you typically lose.

Juan Caballero is a senior data scientist at World Data Lab, where he leads the Insights and Analytics team. Wolfgang Fengler, a former lead economist at the World Bank, is CEO of World Data Lab. Project Syndicate, 2024, published here with permission.

1 Comments

Id bet against demographics

"The underlying factors driving this growth – longer life expectancy, better education, urbanization – have been put in place over the last decades .."

No

the underlying factor driving growth is ever more fossil fuel consumption

All those future consumers wont have the means to pay ...

https://www.stuartmcmillen.com/comic/energy-slaves/#page-1

https://www.stuartmcmillen.com/comic/peak-oil/#page-1

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.