Having taken on the regulation of retail payments as recently as November 2022, the Commerce Commission is consulting on whether fees set then for using the Visa and Mastercard payments networks are now costing New Zealanders too much.

Although these fees could potentially be heading significantly lower, the Commission's stopping short of advocating abolishing key interchange fees altogether, which I did in 2020.

"We are exploring whether New Zealanders are paying too much to make and receive payments using Mastercard and Visa cards. We think there is potential to reduce these costs to New Zealanders," Commission Chairman John Small says.

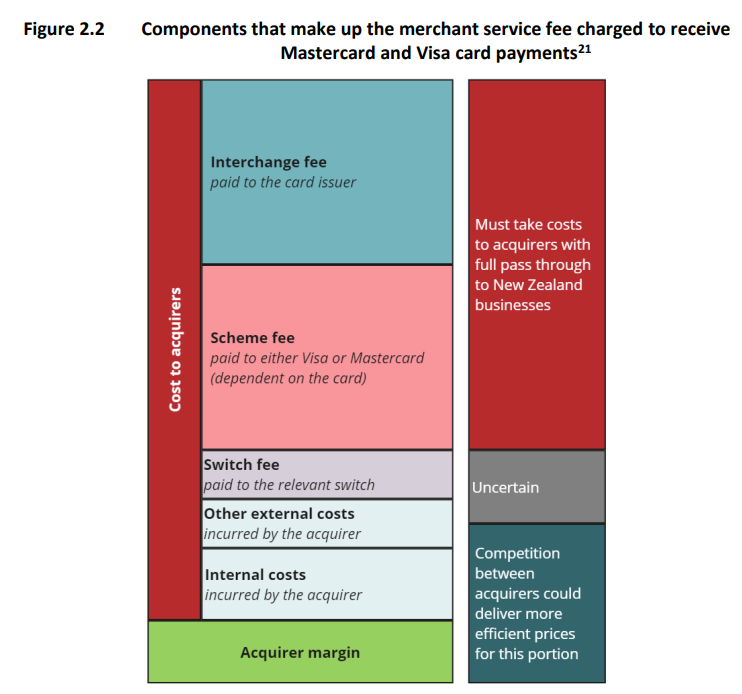

In a new consultation paper the Commission estimates merchant service fees amount to about $1 billion a year, with interchange fees comprising about $600 million, or 59%, of these fees paid for Mastercard and Visa card payments, mostly via banks.

Thus the Commission says further interchange fee regulation could reduce fees substantially. Assuming 90% of these savings are passed through to merchants, merchant service fees could fall by more than $250 million annually, it says. This estimate is based on 0.2% domestic and 1.15% international interchange fee rates, which are lower than current rates.

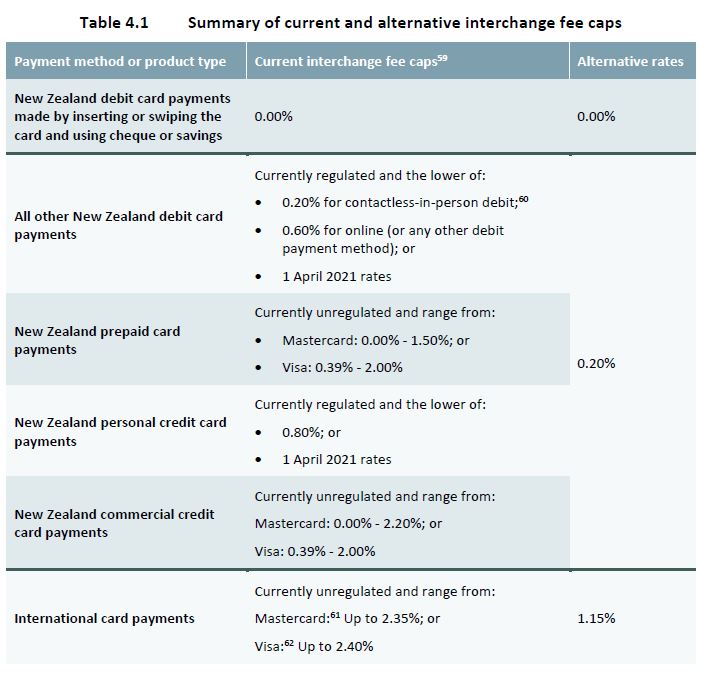

See details of current and alternative, potential interchange fee caps in Table 4.1 at the foot of this article.

Under the Retail Payment System Act, which took effect in November 2022 after being passed by the previous Labour government, the Commission's powers include; issuing merchant surcharging standards, regulating the "designated" Visa and Mastercard credit and debit networks including their participants through network standards and/or directions, and ensuring merchants and consumers pay no more than "reasonable" fees for the supply of payment services.

What are interchange fees?

Interchange fees are charged by the financial institution on one side of a payment transaction to the financial institution on the other side of the transaction. A typical card transaction involves four parties the cardholder, the cardholder's financial institution (the issuer), the merchant and the merchant's financial institution (the acquirer). For most card transactions, the interchange fee is paid by the acquirer to the issuer.

Visa and Mastercard point out interchange doesn't generate revenue for them. However it underpins and grows their networks and is the biggest component of merchant service fees paid by merchants to their banks. Interchange can thus drive up costs for merchants and ultimately consumers too, being reflected in retail prices and surcharges, with some also rebated to card holders as rewards.

They're also complicated. For example, Visa and Mastercard have hundreds of interchange fee categories, impacting the cost and transparency of the merchant service fees paid, merchant service fee pricing and the accuracy of merchant surcharging.

Further regulation would be bad news for bank card issuers for whom Visa and Mastercard relationships are lucrative.

A relic from a pre-electronic payments era?

The Commission notes when a new system's being established, interchange fees might be necessary to rebalance costs and ensure both sides of the market have an incentive to participate. However, this rationale is weaker now the Visa and Mastercard networks are well established.

"We understand card issuers may use interchange fee revenue for a range of matters, including paying rewards, covering fraud losses, supporting anti-fraud investments, paying for [Visa and Mastercard] scheme fees, paying digital wallet fees and covering the cost of interest free periods."

In 2020 I noted in the days of the internet, smartphones and instant communications, interchange is arguably a relic from a pre-electronic payments era.

As the Reserve Bank of Australia put it: "The major card schemes are mature systems, and regulators in many countries have reached the judgement that their cards are ‘must take’ methods of payments – that is, that merchants have little choice but to accept their cards. In practice, with interchange fees being used to incentivise issuers [typically banks] to issue cards from a particular scheme and cardholders to use that card, the tendency has been for competition between mature card schemes to drive up interchange fees and costs to merchants, with adverse effects on the efficiency of the payments system."

And as the Australian Productivity Commission put it: "The case for interchange fees to fund reward programs or to redistribute benefits on a transactions basis from the merchant’s bank to the customer’s bank is feeble."

Problematic issues with interchange

The Commission's paper cites several problematic issues with interchange. These include the interchange fee being a form of horizontal agreement between rivals meaning it "clearly risks" breaching competition law, and different user groups paying fees set at different levels. For example, the initial NZ price regulation set a cap on contactless debit interchange fees of 0.20%, what it was prior to regulation. However, some large businesses pay rates as low as $0.02.

Whilst cardholders generally only have a Mastercard or Visa card with their choice typically made for them by their bank, merchants normally accept multiple card payment networks. This means the card payment networks can exercise market power over merchants and compete for issuers by offering high interchange fees.

"The risk of missed sales leads to merchants perceiving widely held cards as 'must-take' cards. This implies merchants' demand for card use is more inelastic and they are less 'resistant' to increases in merchant fees. All merchants that accept cards face these costs," the Commission says.

The consumer watchdog also references the "merchant indifference test," which seeks to make a merchant indifferent between accepting a payment between different payment methods. It notes applied to NZ, Eftpos could be the appropriate comparison.

"Given an Eftpos payment has no incremental cost for businesses, the test would likely suggest the card networks would not have an interchange fee level above zero."

The Commission also talks of cost-based approaches in Australia and the USA. And it outlines potential for open banking and other new payment options.

In the short-term the Commission says it sees an opportunity for further regulatory intervention to improve the efficiency of the costs faced by merchants and consumers to make and receive payments with Mastercard and Visa. In the medium to long-term, it suggests innovations and new entrants could help to further reduce the direct costs and address the indirect costs, promoting greater competition and efficiency in the retail payment system to the benefit of both merchants and consumers.

It argues open banking payments, progressing at a glacial pace in NZ, and a modernised interbank payment infrastructure, are medium to long-term solutions to improve efficiency within the retail payment system.

"This requires various developments, including all banks to collectively invest and work together before this method of payment is a viable alternative to card payments made in person and online," the Commission says.

"We want to see consumers and businesses benefiting from new ways to pay between bank accounts for online and in-person payments. We recently consulted on a proposal to recommend to the Minister of Commerce and Consumer Affairs [Andrew Bayly] the designation of the interbank payment network. That proposal seeks to confront barriers to new payment options that are likely to be more secure, more convenient and reduce costs for businesses and consumers."

Investment support & the fraud fight

The Commission notes setting interchange fees to zero has been recommended in other jurisdictions, noting the Australian Productivity Commission report cited above. However, it says this hasn't yet been implemented anywhere other than in NZ for contacted, rather than contactless, debit card transactions which is "rooted in the historic development of Eftpos."

A key concern preventing the Commission seeking to abolish interchange fees altogether is it wanting to ensure payment providers can earn revenue from a payment service to support ongoing investment.

"Setting zero interchange fees on the Mastercard and Visa networks may hinder further investment by challenger providers of payment instruments, " the Commission says without citing specific evidence.

It goes on to say not all costs are true costs because the card issuer decides what it chooses to spend interchange revenue on.

"Moreover, the choice of issuers on how to spend interchange fee revenue could be viewed as independent of the level of interchange fee," the Commission says.

"An important 'cost' is the investment in consumer protection in respect of fraud. We consider payment providers should have incentive to invest in fraud reduction techniques so being potentially compensated for fraud losses through interchange fees may reduce this incentive."

Pragmatic approach

The Commission says it'd be hard to determine a reasonable fee level via a cost-based approach, thus suggests a "pragmatic approach" could be using a benchmark method for determining interchange fee levels.

"If we were to use benchmarking, our initial thinking is that the debit rates set in the United Kingdom and European Union could be a reasonable pragmatic basis for our approach. This recognises there is no one definitive method. It also has the advantage that the rates set by other payment system regulators can be observed to allow for a commercially viable product," the Commission says.

"We can also observe that an interchange fee cap of 0.20% is supported by a Canadian study and is a rate in New Zealand for contactless debit card payments for most businesses."

Transactions using commercial credit, prepaid and foreign-issued cards are excluded from NZ's interchange fee regulation. The Commission is, however, considering whether these should be included in regulation.

"We are interested in understanding what the impact would be of using the cap applied in the European Union of 1.15% for all transactions using foreign-issued cards at New Zealand merchants."

Surcharge concerns

The Commission notes some interchange fees in NZ are materially higher than those in other countries.

"We see the potential to reduce a significant component and the complexity of the fees paid by New Zealand merchants to accept payment from Mastercard and Visa payment products. This should also reduce the surcharges faced by New Zealand consumers and/or reduce retail prices or lessen inflationary pressure on businesses to increase prices."

"Currently the average surcharge imposed by merchants is approximately 2% but the average merchant service fee is approximately 1%. Whilst the cost for accepting contactless debit is lower (0.70% for those on unbundled pricing plans), merchants will have higher costs when their customers pay with a more costly payment method (upwards of 2% for international cards) so they may just pick the higher number," the Commission says.

"Interchange fee complexities make it incredibly difficult for a merchant on an unblended pricing plan to understand the cost of accepting different forms of payments. This impacts a merchant's ability to price goods and services, compare and switch acquirers, and surcharge correctly."

The Commission is seeking submissions by 4pm on August 20.

*Table 4.1 and Figure 2.2 below come from the Commerce Commission.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

5 Comments

Have enjoyed all your analysis on this topic over the years Gareth. I think we should slowly wave goodbye to the lucrative rewards/airpoints schemes being offered on credit cards.

Merchants, and ultimately the consumer via higher prices/surcharges etc, should not be funding these rewards schemes. This is an unnecessary cost for consumers, with rewards then typically enjoyed by those more well off in society. If banks want to offer rewards schemes, then fund it out of their bottom line, don't get merchants to fund it.

I do think some retailers have taken the mickey with their ongoing 2% surcharges (something the Commission should investigate as well). You can't charge every customer a 2% surcharge, regardless of card type, simply because on the odd occassion you might have a tourist with an American Express walks into your shop and you incur a 2% interchange fee. Most interchange rates are nowhere near 2%.

If not passed on to the consumer, these fees are a 'cost of sales' largely borne by the vendor. However, given that consumer behaviors are so ingrained and so many live paycheck to paycheck, the banks get to make out like bandits.

I was a big supporter of BNPL, even though it is generally hated and seen as oppressive. Why support BNPL? Because it can lead to a sale where none may exist. It supports the economy. The argument that it encourages people to take on debt they can't manage is a cop out considering the banks already nudge people to live as close to the edge as possible.

I insert the card and pick cheque - never been charged a fee paying that way. Presumably if everyone did the same the fees for debit card Paywave transactions would fall pretty quickly.

So the vendor is paying. Less profit margin or increased shelf price.

If you insert the card and select Cheque or Savings, the transaction is processed over the EFTPOS network, not the Visa/Mastercard network, so the retailer doesn't incur a fee.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.