Overall spending on cards fell by 0.6% or $40 million in June on a seasonally-adjusted basis, according to new figures from Statistics NZ.

Core retail spending which doesn’t include fuel and vehicles fell by just 0.1% or $5.7 million on a seasonally-adjusted basis last month as well.

During June, cardholders made a total of 157 million transactions across all industries, averaging $55 per transaction, resulting in electronic card expenditure of $8.5 billion.

It’s the fifth fall in retail spending in five months. In that period, total retail spending figure movements have fallen by, in order, 0.8%, 0.7%, 0.4%, 1.1% and now 0.6%.

Stats NZ said seasonally-adjusted specific movements by retail spending category in June 2024 included:

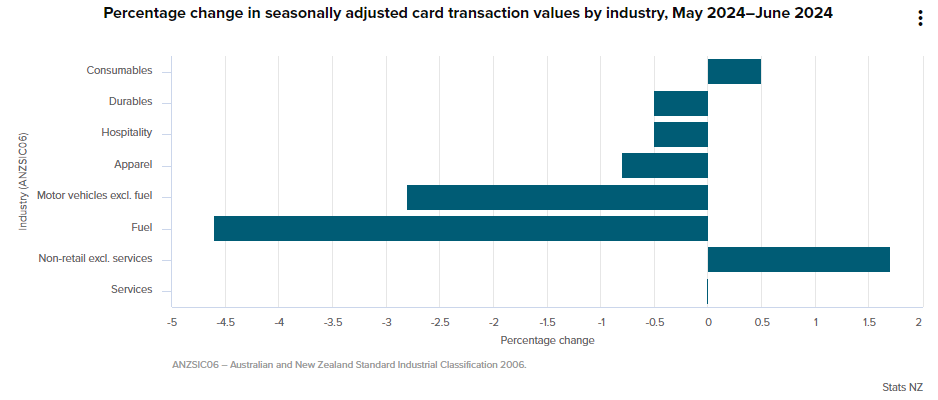

- fuel, down 4.6% or $24 million

- durables, down 0.5% or $8.2 million

- hospitality, down 0.5% or $6.6 million

- motor vehicles (excluding fuel), down 2.8% or $5.3 million

- apparel, down 0.8% or $2.4 million

- consumables, up 0.5% or $12 million

In the month of June, the non-retail sector (excluding services), which includes medical and health care, travel and tour arrangements, postal and courier services, and other non-retail industries, grew by 1.7% or $38 million.

Stats NZ said services spending which covers repair and maintenance, personal care, funeral services, and other personal services, remained unchanged from May when it was down 5.8% or $22 million.

Overall electronic card spending, incorporating both non-retail categories, declined by $45 million (0.5%) from May 2024.

When comparing the June quarter with the March quarter, total retail spending dropped by 3.7% or $740 million, while core retail spending declined by 2.3% or $410 million on a seasonally adjusted basis.

During the June quarter, the non-retail sector (excluding services) rose by 1.4% or $91 million and the services sector rose by 1.8% or $19 million.

However, the total value of electronic card spending spent during the June quarter, including both non-retail categories, fell by 1.1% or $302 million compared to the March quarter.

Household squeeze

Westpac senior economist Satish Ranchhod said in a note that the downturn in retail spending was deepening and June’s 0.6% spending drop was higher than the retail bank had expected.

Westpac had anticipated a 0.2% drop in retail spending during June.

“Over the past year, households have seen their spending power squeezed by the continued rise in living costs and the related increases in interest rates,” Ranchhod said.

“Those pressures have been compounded by the softening in the labour market. Against that backdrop, consumer confidence has fallen to low levels, with nervousness about the economic outlook meaning that many households are keeping their wallets firmly shut.”

Ranchhod said the Government’s new income tax cuts which will be applied from the 31st of July may give spending a boost through the back half of the year.

“However, with lingering pressure on household budgets and the labour market continuing to weaken, we expect spending will remain soggy for some time yet,” he noted.

ASB senior economist Kim Mundy said the latest electronic card transactions painted a bleak picture.

“The cumulative impact of past monetary policy tightening and growing job insecurity fears are playing out clearly in the retail space,” she said.

Mundy added that ASB had long maintained that consumer spending held up well against initial Reserve Bank of New Zealand (RBNZ) tightening due to high household savings, population growth, and strong income growth from a tight labour market.

“But the change we’re seeing in the labour market is consistent with consumers taking an even more cautious approach to spending. We expect challenging conditions in the retail sector will prevail, in part driven by our expectation that the unemployment rate will peak at around 5.5% in mid-2025,” she said.

ANZ’s merchant card spending for the month of June also came out on Friday and painted a similar story to Stats NZ’s data.

The bank’s chief economist Sharon Zollner said annual spending growth fell under 1% year-on-year in June, which suggested that sales volumes are still falling.

She noted that year-on-year decline in durables spending “continues to deepen.”

Seasonally-adjusted tourism-related spending also saw a “particularly sharp fall” during June with monthly spending falling 4.7% and annual spending decreasing by 1.9%.

The only categories that showed year-on-year growth were miscellaneous services, miscellaneous goods – including supermarkets – and utilities and repairs, she said.

83 Comments

The economy is falling off the cliff.

The RBNZ should have already cut the OCR, but if they don’t cut it by at least 75 BPs by end of 2024, and 150 BPs by mid 2025, the economy will be even worse in 2025 than 2024.

NZ has too much private debt, quick lower rates so we can take on more debt.

NZ = total basket case.

Giz some more cheap credit so we can buy some more imported goods.

This is much of the West though.

Madcap economist Hugh Hendry's counter is there's a tax on mercantilists' goods that gets placed into sovereign wealth funds, to allow for infrastructure and development spend.

Although governments would likely just blow it on operating costs and lollies.

I recall making a comment many years ago on here - that the low rates were the opportunity to get rid of debt, not take on more.

So we did what?

I now we wonder why we are in the doo dooo

Blackbeard: "NZ has too much private debt, quick lower rates so we can take on more debt."

What about the billions that are being sucked out of the economy (and overseas!) by the high interest rates being paid?

With no increase in debt - none whatsoever - NZ Inc would be trucking along. Or put another way, the interest being paid on the existing debt would be reduced and people would have more to spend on local businesses like hospo. And the government would clip the ticket by picking up GST which would help balance their books.

Sorry BB, I get sick and tired of nonsense like this. Lowering on interest rates does NOT automatically imply more debt.

It's more likely than not.

If it's nonsense, it's probable nonsense.

Pa1nter: "It's more likely than not."

Prove it.

Or I'll call it more folksy wisdom.

In your reply please reference what would happen if LVR and DTI ratios were ratchetted up and/ or the RBNZ used the other credit creation controls at their disposal (that they've largely forgotten about). You may also like to mention where good debt could be encouraged.

Name calling is about the only thing you're good at.

Why would I base my view around some uber optimal Death Star trench run lending practice that doesn't exist? Far more reliable to base your views on how things actually are, than how you'd hope they'd be.

It does in NZ, we are addicted to the property drug. The government needs to address that. In my opinion, rates need to stay where they are. If our economy can’t survive on these low-ish rates, then we have major fundamental issues.

Austrian business cycle theory - Wikipedia

Read the "Mechanism" section of that wikipedia and tell me it doesn't sound remarkably what NZ and the world has been going through since 2008.

The final part is of great interest to me in particular:

According to Ludwig von Mises, "[t]here is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as a result of the voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved".

Central bank are attempting the "voluntary abandonment of further credit expansion" option. Remains to be seen if they can stick to it in face of inescapable recession (I think it is doubtful for political reasons and rates will be reduced). Then we will move onto "currency collapse" option.

Buy crypto.

Sounds like a huge flip flop from HouseMouse again...

Changing your stance in the face of new circumstances or evidence is not a bad thing. And circumstances are undoubtedly very different to 12 months ago.

The question is - is it actually bad that we're destroying our joke of an economy? Isn't it actually a very good thing that we're killing the unproductive credit-harvesting arms of the economy that have been squeezing out productive enterprise? Bye bye housing market, the "bits tacked on" will survive and finally be able to take their rightful place at the heart of a healthy economy that works for all.

You're assuming whatever rescue plan will exclude housing and whatever tenuous commercial enterprises are still standing.

Isn't it actually a very good thing that we're killing the unproductive credit-harvesting arms of the economy that have been squeezing out productive enterprise?

Yes, I agree. A genuinely productive business will survive. i.e. we will still export xyz that ultimately pays for our imports. Even if a farm goes under due to excessive debt, it will still continue under a new owner as there is a market for its produce.

Maybe we should jack up interest rates more, let the banks take a haircut on their loan book and the new business owners produce the same but with less debt. Effectively sucking back some of those billions we've sent offshore in bank profits. Productive jobs would remain - that would be an eye opener to many who think they currently hold one.

We have all forgotten that recessions are a normal part of the economic cycle, occur every 7-10 years, and operate as a kind of brush fire - clearing out dead wood making way for new growth, and most importantly, preventing the build up of conditions that would cause a major destructive fire down the road. Its only recently that central bankers have decided that recessions are to be avoided at all costs, even if this means kicking the can down the road so far all that's left in the economy are debt riddled, zombie companies and governments, and a handful of mega caps that stifle investment and innovation into anything that threatens their revenue streams. Capitalism is a great system, if its allowed to work properly.

In what respect? I was more accurate than most in picking the economy to tank.

Yet, inflation is subsiding quicker than I and almost everyone thought it would.

Yes because the economy has stalled and is now falling to the ground short of the runway....

Ah right maybe you haven't flip flopped, you've just been making wildly inaccurate predictions on this for sometime. A quick search brought this up from someone who took note of your predicitons lol...

By printer8 | 29th Nov 23, 10:29pm

Hi House Mouse

Which ones are you going to revise / flip-flop on?

- OCR 1.75% max this cycle

- Inflation: Done and dusted 2022 I think from late 2022 through to late 2023 it could still be in the 3-4% range.

- Mortgage Interest: back to 2 to 3% by early 2024

- My pick is unemployment above 5% by early 2023. And above 6% by May 2023 . . . . and I stand by that. I suspect it could be at least 7-8% by mid-2023

- CPI inflation sub 4% by May 2023

I really loved the 1.75% OCR max when ANZ were calling 5% - what did you call them. That's right "fools". It looks like you are the fool.

You will deny these as honesty and integrity aren't one of your traits. Be careful, I'm happy to back these up. :)

Now don't get triggered.

This sucker is going down.

The retail market has the bouyancy of a common item of fishing tackle.

Notice the recent headlines about how food prices are falling. Might be cheaper than a year ago but they've actually been rising for the last few months.

Is that just seasonal variation?

That's right - it's a mixed bag. Groceries are still going up, meat is going sideways, and vegetables are going down.

Hi Jfoe. According to Stats NZ you are correct but according to my eyewitness account every category is up strongly in my local (Whakatāne) supermarkets. (All 3 of them !!).

And those totals are with an extra how many people to our population over the last year?

At Burger Fuel yesterday and it cost me $29.30 for a normal burger, fries and a drink, so a burger combo.

Many people simply can’t afford to go out any more, especially those with kids.

There is no value in a lot of this spending so it’s going to sink further. It’s a downward spiral.

Was over 20 bucks yesterday for a double mediocrity burger with cheese combo at Maccas.

People will likely pay over the odds for convenience for a while to come.

Was over 20 bucks yesterday for a double mediocrity burger with cheese combo at Maccas.

Price of a Big Mac set in Japan will cost you 480 yen. That's <NZD5.

That's nice. I'd also earn 1/4 as much (actually even less, some of my income isn't possible in Japan at all).

Good opportunity for income arbitrage for those that can do it.

That's nice. I'd also earn 1/4 as much (actually even less, some of my income isn't possible in Japan at all).

Japanese shoppers are also paying up to 35% less for Aussie beef, despite an import tax of 27% and a logistics cost of AUD1 per kg. One of the key reasons is that the Japan retail sector is far more competitive.

https://www.beefcentral.com/news/comparison-suggests-aussie-beef-retail…

Some things are cheaper in Japan, yeah.

They're also cheaper again other places.

But much of the underpinnings are circumstantial, rather than by design.

Conversely, many items now have global pricing. I can walk into an Adidas store in Delhi, Bangkok or Seoul and they're the same (or more) than in NZ.

Finding somewhere that the balance between incomes and expenses is significantly better for your average employee is pretty rare. Just looking at currency converted price tags doesn't tell you much.

Some things are cheaper in Japan, yeah.

The beef example is mind-blowing. Most things pertaining to daily living are cheaper in Japan than in Western countries. Some key reasons:

1. The Japanese govt intervenes in markets to preserve purchasing power

2. Japan`s domestic industrial structure is much more cut-throat competitive

Quoting Jesper Koll:

The net result of this seeming contradiction – government intervention going hand in hand with extraordinary competition – is a much lower inflation equilibrium here in Japan compared to what we get in the less interventionist and more oligopolistic US economy. There, a few producers and distributers are price-leaders and effectively control the market.

https://japanoptimist.substack.com/p/whos-afraid-of-inflation-not-japan

At almost every point you choose to ignore the day-to-day realities for the Japanese citizen. Their incomes are going nowhere and their currency has them increasingly less capable of spending outside of their own ecosystem.

It only looks good if you're viewing it from your income perspective, not theirs.

Their incomes are going nowhere and their currency has them increasingly less capable of spending outside of their own ecosystem.

Which is why the Japanese govt implements the policies described above. I highly recommend you read the article if this is of interest to you.

As for JPY being spent outside Japan, it's also unlikely you will find people using NZD outside NZ, except in the Pacific Islands and Aussie.

Japanese can use JPY in places such as Guam, Hawaii, and South Korea. And of course, all ecommerce platforms will accept JPY.

Im talking about what their currency can afford outside Japan, not where it's accepted.

Go basically anywhere now, and ask the locals how fewer Japanese they encounter.

I highly recommend you read the article if this is of interest to you.

Things are cheaper in Japan and many of the reasons aren't relevant to NZs context.

I can get a good meal in Sri Lanka for $1-$2 but I can't import their conditions here, nor would I want to.

Im talking about what their currency can afford outside Japan, not where it's accepted.

Naturally. But I don't think you understand it well.

1. What would happen if capital were repatriated to Japan? What would happen to JPYAUD / JPYNZD?

Despite the interest rate differential, JPYAUD+NZD soared during the GFC. The moves were dramatic. NZD fell from JPY95 to 52.

2. If JPY keeps weakening, what do you think happens to CNY?

How is that good for anyone sitting in Springfield in the Anglosphere? More importantly, who buys the USDT?

We could have an endless discussion about potential global hypotheticals. Our accuracy there is probably as good as blindfolded darts.

But we're discussing the realities that've actually occured, or exist today.

But we're discussing the realities that've actually occured, or exist today.

1. The current state of JPY is the "reality".

-- Weak JPY is putting immense pressure on CNY. China and Japan are direct export competitors. The only thing that matters is price. If CNYJPY exchange rate rises, China’s export competitiveness is hurt.

https://www.forexlive.com/centralbank/pboc-is-alarmed-by-the-weakness-o…

2. If the BOJ raised rates to narrow the dollar-yen interest rate differential, domestic regulated capital (banks, insurance companies, and pension funds) would buy JGBs. To do this, these entities would sell their foreign dollar-denominated assets, mostly USTs and US stocks.

This is a bad outcome because the Japanese private sector would sell trillions of dollars worth of USTs and US equities.

The CNY has been intentionally suppressed for decades, and you'd have to question how much of Japan's production can now be repatriated.

If the BOJ raised rates to narrow the dollar-yen interest rate differential, domestic regulated capital (banks, insurance companies, and pension funds) would buy JGBs. To do this, these entities would sell their foreign dollar-denominated assets, mostly USTs and US stocks.

"If". They'd struggle to service the higher interest costs. Maybe they can sell some treasuries to try and cover that, but this is only a short term fix.

The CNY has been intentionally suppressed for decades

The BOJ-MOF have also worked in tandem to keep JPY competitive for export purposes.

But you're missing the point. F'more, Japan cannot compete with China on low-cost manufacturing production. Their more sophisticated production can of course happen domestically - to some extent.

But you're missing the point

Yes I am. You started again to point out how consumer goods are cheaper in a much larger economy, with much lower wages, situated in closer proximity to a huge market, as if it means much, and now we're crystal balling currency shifts.

Painter does not understand the implications of the carry trade, here is an example

Frucor is owned now owned by Suntori.... perhaps purchased and funded by cheap debt from japan, vs good yield in NZ... carry trade.

Borrow cheap and invest where yield is high, Japan has become a massive source of cheap funding, but as JPY strengthens, there is more debt to repay... companies DO NOT hedge all there fx exposure... why?

Because the carry trade has been around forever so why spend the dosh, until its not and every one rushes to the door at once, NZD could fall 10 big figures on an unwind. What happens to imported inflation.

Great. You get it. And as the mighty Audaxes also pointed out before, Tokyo is also an important source of the Eurodollar.

Japan's government is engaged in a massive $20 trillion "carry trade" - the funding of loans and foreign assets by borrowing low-cost yen - that could bring unexpected risks if the central bank tightens policy, Deutsche Bank analysts warn.

Using research by the San Francisco Federal Reserve and International Monetary Fund, Deutsche's head of currency research George Saravelos analysed a consolidated balance sheet of the Japanese government including the government-run pension fund GPIF, the Bank of Japan (BOJ), and state-owned banks, showing the asset-liability mix of its $20 trillion debt.

https://www.business-standard.com/economy/news/japan-s-20-trn-carry-tra…

If kiwis were paid 850-1000 yen per hour our burgers would be cheaper too.

The minimum wage for fast food workers in California is $20 USD an hour.

That's more than the average Japanese salary.

Fast food chains in the US are struggling because prices are perceived as unaffordable. They're having to resort to value meals to get people through the door.

“What’s happening now in the burger category is a race to the bottom, with all these companies discounting to try to retain market share,” says BTIG analyst Peter Saleh. “This isn’t a profitable venture.”

According to a study from LendingTree, 78% of respondents said they now see eating fast food as a luxury and 65% were shocked by the price of their orders.

https://www.barrons.com/articles/fast-food-mcdonalds-inflation-price-wa…

And fast food reatuarnats are closing fast in Calipornia thanks to Governor new some (but not much) and the exodus to Texas and Florida of people and business will exacerbate the diminihsing tax base like it is in NY and many other democratic states - spot a link?

Priorities. Many have no problem spending $50/week on beers... Or upgrading the iPhone every year. Or the car every 4 to 5 years.

I'd say there's a lot of fat to be cut still.

I think you’ll find each of those categories are absolutely are tanking.

Just like the GFC period, it’s going to be trendy to not spend money for a while and people are ok to talk about it.

Too bad they weren't thinking that way over COVID.

Looks like the ramifications of interest rates on spending greatly eclipse those of global pandemic and shutdowns.

Ahh humans, always thinking 30 seconds ahead.

If people stop spending, nobody will have jobs. We need people to spend. We just need to stop borrowing to spend (other than houses and major assets etc).

Yep, it might be possible to spend and have a functional economy if circa 50% of an individual's take home income wasn't spent on paying off the bank's or the landlord's house.

I'll add being able to afford a family to that as well.

NZ likemany other countries is in deep dodo with population as current birthe per female are now 1.64 below replacement rate of 2.11 and below 1.9 which historically has been the lower limit at which a population recovers.

But people borrowing to spend = growth. Bringing forward income from the future into today, so that businesses can post profit growth.

Yes and it will accelerate and spread to many other items of discretionery soending.

Another one to suit the “cut” narrative.

The number of push to cut articles are going to come thick and fast over the next few weeks. There is zero resilience in the NZ economy, businesses here will start dropping like flies.

There's definitely some resilience.

Plenty of people here seemed to think everything would crap itself as soon as rates got hiked.

Don't worry everybody is saving their money to buy a house instead.

/endsarcasm

Great to see Luke from "Keep the Change" floating around these forums.

Doing a lot of great work around financial education on the socials for those who aren't as literate. Definitely a hunger in the public space for education to get through these times, definitely don't getting it on the news/anywhere else!

Random shoutout/promo...#ad?

Not at all mate, don’t know him from a bar of soap. Stumbled on his stuff and he’s got screenshots of interest.co.

Great info when times are tough and wallets are shut as above.

"hunger in the public space for education", lol that is actual hunger you are mistaking. Whatever people want in NZ sadly for most the populace, especially those coming down the pipe, education is rarely the most desired or valued. Just look at how the STEM fields are being stripped. To the point many graduating teens and youth cannot many do simple sums or understand simple concepts (like what a percentage is) even using a calculator. It is not education which is desired the most and for most we, as a nation, have been steadily devaluing the lessons of it for the past 20 years. To the point a sharp reset is needed even to save those starting now.

What people need most is the base needs to survive first, then a sense of purpose, justice & community, then a larger series of goals & cultural fulfillment to strive for. Instead we have it upside down and are failing badly with much worse wellbeing outcomes the result. We think by fulfilling the least functional and least essential fields that people can survive without base needs for shelter, safety, medical care & food. It does not happen that way and you don't need much of an education through human history & physiology to see why. Education is essential for all communities to survive as a whole and for people to understand key factors in their lives. But as much as it is a key factor in the later levels NZ still cannot provide an environment to satisfy the essential needs, medical needs, and long term safety.

If you think people suffer without financial education you are right but a person can live a lot longer without knowing how to do basic math then they can without food & shelter (as NZ so keenly proves in our poorest & vulnerable). However for too long we have focused support solely on a racial basis rather then a socioeconomic one (where collective ownership managed by limited people does not translate to equitable wellbeing... on many levels). So many essential needs and social supports are denied to those who are in socioeconomic need. Much the same way we also discriminate heavily by age for financial benefits & social supports. We do not target those who need support. Rather we fund more wealthy groups with very low levels of need and deny any support to those who are denied essentials. We think this makes us more egalitarian but instead we have only become more inequitable, and more ageist (more likely to also have a growing level of harm towards those who are destitute).

Like the incredibly wasteful funding for mandatory budgeting courses that run up against the same problems for those denied social support: you cannot budget key medical care when you have zero available income. You cannot even budget for survival in those conditions and so many don't survive. We knowingly have people die before retirement age with conditions that do not affect lifespan and are treatable. Hence these ill planned financial education & budget courses are worse then wasteful. They are actively harmful, financially wasteful, often traumatic and result in removal of funds from initiatives that could have helped instead.

Even targeting of funding for services is incredibly out of touch and inequitable. Of over 100 providers of medical support services nationwide we have only one (which unlike the others is restricted to no contact with people to save funds) to cover all ethnicities, ages, abilities (although it cannot even support those most able most the time), and so we do not even cover the majority 80% of people with medical support. Especially noticeable in unmet need studies when we have stats to prove the majority of need is in the excluded 80% and that most people are going without essential care. Is it a surprise really that financial education is one of the least important things when such exclusion of basic needs occurs.

This plays out in most of our services. E.g. lets take one branch where financial & maths education can help the most say gambling prevention support; even gambling in stocks, currencies, high risk ventures etc. Education can help identify the clear harm, provide easily teachable ways to loss prevention, clear actionable goals and results tracking, (where financial education & immunization against behavioral targeting tricks helps incredibly). Yet for gambling addiction there is practically no available support services in most areas. There is not even services or supports to help recover and access private gambling support physically in any region. Since the addictive harm can be closer then arms reach now there is far more harm out there & sadly there is even far less addiction support then we had 20 years ago. Financial education is worthless in such cases as it is without the medical support and fails to understand and counter the psychological tricks inducing gambling. Knowing the odds of loss are far greater does not stop addiction. Neither does telling people high risk speculation or "investments" is money down the drain. It requires key social and medical support as well to help with the addiction and NZ has defunded MHS to more then 80% of the population.

NZ is sick but sadly the idea that a quickie slapdash cheap budget & investment tricks education will suffice as a cure is actively harmful dialog to most, especially for those who are suffering.

Like all wealthy chartered accountants Luke shows they are completely ignorant of simple costs, basic budgets when in destitution. When accountants reach a point of destitution (often when they decide to take a long term holiday at the age of 65 to just sit on a benefit on the couch or some other normal life event) they cry blue murder at how impossible it is to get by without the funding for essential living needs and medical care. Even in cases of financial investment supporting long term living they fail to account for the time that is required to enable that, ironically since time is key in equations, and then fail to understand that it will never work for those unable to survive without essential needs in that time. Knowing intimately the mindset and education of accountants it is easy to see the simple failings & mathematical errors. There is a reason they can only go up to a certain level of mathematics education and not beyond. Why even though a budget template is replicated more then hundreds of millions of times it has not worked for most cases of poverty and destitution and in fact we have growing levels of inequity while at the same time more access to these cheap fatally flawed and mathematically irrelevant tables.

It is like Luke has never heard of unforeseen costs in life at all; the thing that is the downfall of most accountants as their significant partner leaves them, a flood washes out their home with insurance limited or their kid gets sick & they lose everything in an effort to have them live (that is if they were the sort of accountant with an ounce of humanity but then many don't). There is a reason why yet another cheap budget table & patronizing irrelevant advice that only works for those already wealthy is not going to help much for those in real need. Why it does not even class as education at all but yet more vaporware. See even the examples above. Oh and when his partner and family do decide to split, (easy to see why given the website content and tone which gives big abusive & controlling relationship vibes with many lines a word for word copy from the worst scams & relationship abuse recognition guides), here is a tip: don't do the accountant thing, instead follow legal advice first & support the family as a whole to emotionally process the change.

Sadly most accountants don't have the mathematics and financial education to weather significant life events without a lot of support from outside. Then they wonder why those without the initial wealth don't weather life events that have occurred to them much sooner in their lifetimes. I would have loved to see some of these accountants go through Lake Alice or Marylands etc and finally understand why their advice does not meet the needs of people and it is not an education gap when real medical harm, significant abuse and real neglect of essential needs is present. Not that I would want anyone to be put in those positions again, we had so much damage & eugenics occur to much of the population from our "care" & school facilities for those who were destitute. But it does show most accountants in NZ have significant education gaps even with understanding simple equations. I get that it is from a place of primarily ignorance and not malice but given the language used on Luke's site, he is pushing far closer to include malice as well then most. Most likely he is setting up to grab some of that free grant cash handed out for the wealthy wastes of time then anything else.

The work of a chartered accountant is mostly work providing how you can best avoid tax and claim incentives for things. It is little more then a get out of jail free card for financial matters. Even for payroll we have other solutions that are more realistic in budgeting and predictions. But a chartered accountant, they can help reduce the tax paid and increase the amounts you claim. Which can be best boiled down to they have a limited set of advice that can be easily replaced by reading a national guideline of tax laws. When it comes to budget & financial education they have less understanding then many of the materials out there you can copy and they are less applicable to most of the population. It is a matter of limited education & training for accountants in which we have unfortunately denied them more comprehensive education in their field. Even for financial investments accountants often resort to really simple mathematics and limited options. They really like property but cannot understand the generational harm etc. Hence as we favored the wealthy with benefits many accountants are useful in working our how to maximize milking the public teat while reducing the social responsibility and now the chickens are coming home to roost. I really hope it serves them well in retirement when they cannot get an ambulance for a heart attack and the medical services are collapsing and there is no social workers or carers for them to help when they are elderly and more disabled recovering after a stroke (if they survive).

I'm in a 20 minute line at Kmart, for their 15 checkouts... other shops at Bayfair mostly empty.

Check what people are buying though, probably much more necessities now compared to a year ago.

Yup.

Scented candles and a dinosaur costume for a Jack Russell it is then.

I don't knock what gets you in the mood but sex is one of those markets that still does high levels of business regardless of recession.

For my partner and I a decent amount of sterilizing solvents and electrical repair tools are a necessity (for about 50+ other living needs as well) although we had to delay a 3D printer due to unexpected medical costs & having to travel long distance over days for treatment (NZ not having a functional medical system in many regions).

Also markets that do well when people are poor are faith & ways to alleviate hopelessness & lives of destitution (why gambling does better against poorer people in turn alongside churches).

The economy is toast. By the time RBNZ realises it will be too late to save it.

They know it more than most of us.

People seem to think maintaining everyone's lifestyles is part of the RBNZs mandate.

This is another step. First we needed both parents to works. This is the next phase of having nearly zero discretionary spending.

Inflation has eaten your annual holiday, your car upgrade etc.

Did we need both parents to work or did cultural norms change, and the almost doubling of the labour force have a depreciating effect on incomes?

Probably a bit of both.

Card spending in real terms is back to 2017 levels (2014 levels if you use per capita).

Great work everyone! Presumably the next CPI release will be around minus 10%, right? Or do we still need to get more on the dole first? That's also going great guns by the way - we're comfortably exceeding RBNZ and Treasury targets, I mean forecasts.

"Ranchhod said the Government’s new income tax cuts which will be applied from the 31st of July may give spending a boost through the back half of the year"

My tax cut is about equivalent with the rise of my district- and regional council rates, co-funding my medicines, the allowed increase in electricity lines charges and my increase in car rego's. With the increase others like insurance I doesn't believe I will have a boost in spending!

And what tools does the RBNZ have to reduce these non tradable inflationery increases - hint is begins with a Z. Orr is determined to create a deep recession to preserve his record of being wrong on everything every time by being to little too late or too much too soon but at least he gets a mention the history book as the worst BanK Govenror ever alongside the othe worst politicians ardern and robbers son.

Spending down, net migration turning negative, HPI down, building materials decreasing. Are enough signals flashing red on the RBNZ dashboard yet?

Sorry, annual inflation still at 4.0 percent. Better keep our foot on the throat of the economy until it stops twitching.

And then once it stops twitching they'll send for the AED and crank it up to 11 to try to shock it back into life...

Yeah cos OCR has a massive effect on non tradable inflation /s

Nup, she's not poked enough yet.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.