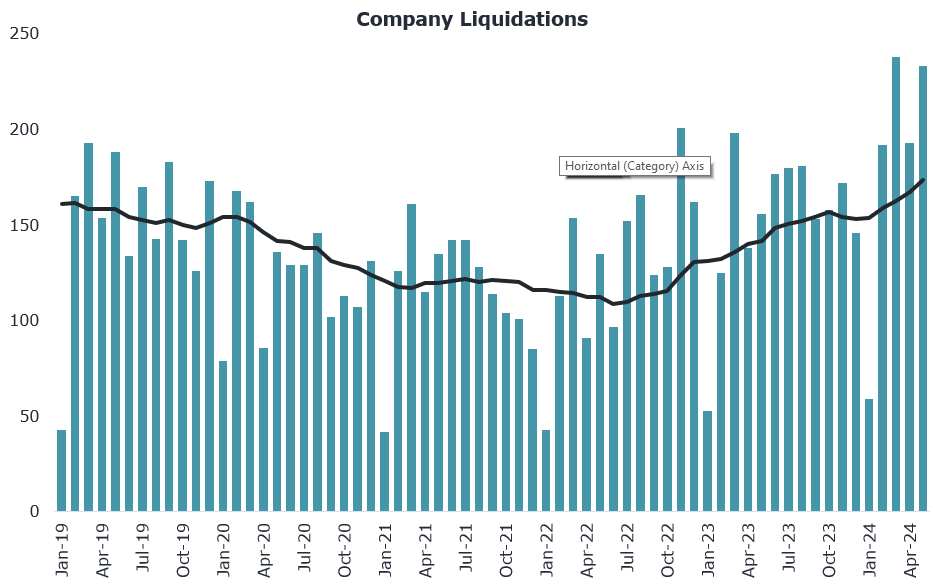

Company liquidations are on the rise, hitting the highest level for a May month in 10 years, according to credit bureau Centrix.

Centrix managing director Keith McLaughlin said in the company's latest monthly Credit Indicator that all sectors have seen liquidations rise with retail trade companies experiencing the largest increase annually, followed by the property/rental and transportation sectors.

In May there were 233 company liquidations around the country, which was up some 49% on the 156 in May 2023.

Looking at the rolling 12-month average, the May figure was up some 22% on the same time a year earlier.

While construction and property companies continued to be the most sizeable contributors to the liquidation numbers - making up collectively nearly 40% of the total, retail trade numbers rose quickly in May.

"Over the last 12 months, retail liquidations have increased by 44% compared to the previous year, with food retailers experiencing the highest volume of liquidations. There were 14 retail companies placed into liquidation in May 2024, the highest monthly since August 2023," McLaughlin said.

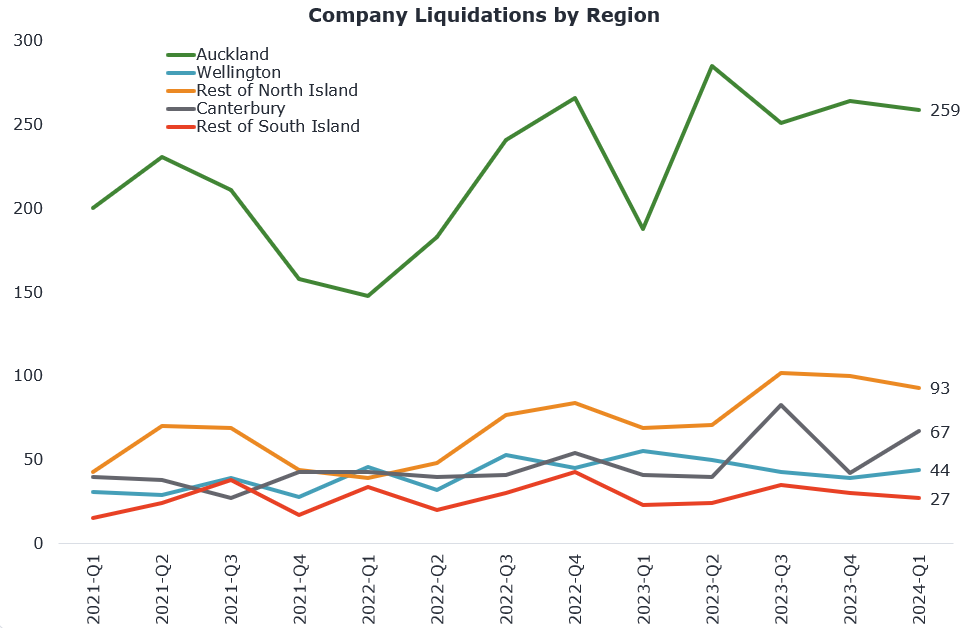

While Centrix has an increase in overall liquidations "across the country", there was "a significant increase" in the rate of South Island companies going into liquidation over the first quarter of 2024 when compared to the same period in 2023, he said.

Over the first quarter of 2024, there were 94 company liquidations in the South Island – up 47% year-on-year and largely driven by the Canterbury region.

There were 259 liquidations in Auckland over the same period (+38% year-on-year) and 137 liquidations across the rest of the North Island (+10% year-on-year).

In April Centrix reported March saw the highest number of monthly business liquidations in nine years with construction companies leading the way, with 238 liquidations the most for any month since 299 in March 2015.

"The challenging economic climate continues to persist," McLaughlin said.

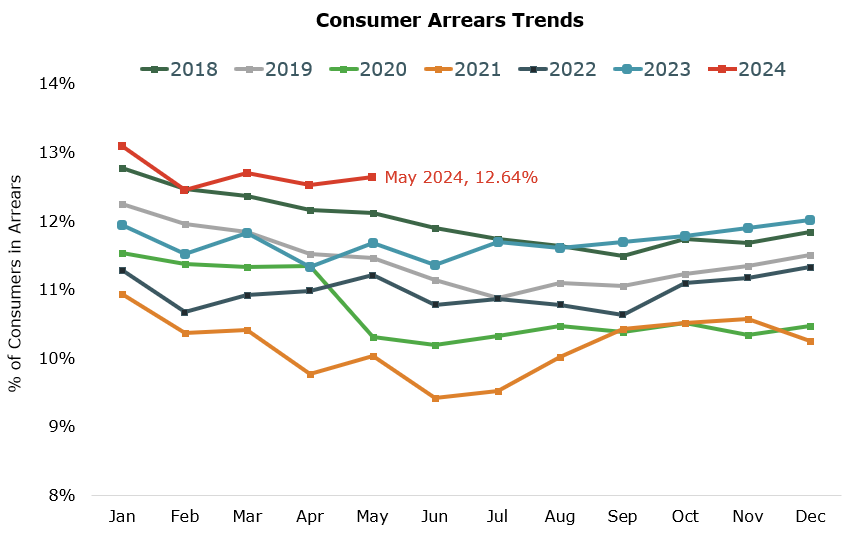

"For example, we saw consumer arrears climb last month– largely driven by telco and mortgage repayments – as pressure from the cost-of-living crisis endures.

The number of consumers falling behind on payments increased by 16,000 in May, with arrears tracking 8.2% higher year-on-year.

Percentage wise, the number of consumers reported in arrears in May rose to 12.64% of the credit active population (up from 12.52% in the month prior), which translates to 474,000 people behind on payments (compared to 458,000 in April).

Of those in arrears, 173,000 consumers are currently 30+ days past due, and 114,000 are at 60+ days in arrears.

"Encouragingly the number of people with non-performing loans (90+ days behind on their payments) has fallen to 90,000, unchanged year-on-year," McLaughlin said.

Business credit defaults have also risen year-on-year, which further points to the overarching economic tension being experienced across the country as weaker consumer demand flows through to impacting businesses, McLaughlin said.

He said mortgage arrears rose slightly in May, with 22,000 home loans now past due - up 12% year-on-year and a return to 2019 pre-pandemic levels. On the other hand, vehicle loan arrears dropped to 5.5% in May (compared to 5.7% in 2023), while credit card arrears fell to 4.7% in May and remain below historical levels.

"There’s plenty of uncertainty about the future, with many anticipating the challenging conditions to persist well into 2025," McLaughlin said.

"For anyone who is feeling the pinch, it’s important to seek advice early to help get through without impacting their future financial wellbeing," he said.

33 Comments

Adrian can see the enemy ( the economy) is bleeding out, but he wants to see it stop twitching before administering first aid, will that be too late? Will it be ICU or the mortuary?

No problem with cutting the OCR to 0% if the LVR on any secondary property is also dropped to that level? That's the problem we have. Any drop in interest rates will go into one area - property. And util that has been stopped, except Adrian to do his job.

So businesses don't use credit, and the high OCR is to nerf property lending, not inflation?

Interdesting

Just as likely, maybe they are thinking that a consumer based society is a sure fire way to go broke fast. In keeping the OCR high, they can bleed off all discretionary spending on trivial material items, and any job that's not an absolute necessity. With this drop in consumption and decline in activity, we will reduce pollution and our impact on the planet, and any new jobs created in such an economically depressed environment will be one of true innovation. With so many extra unemployed bodies, our birth rates will rise again, due to the surplus available childcare (some retirement villages will empty).

Dreams are free.

I've noticed that's the general sentiment around here. People on this forum would rather inflation stay high to justify higher interest rates causing asset price destruction. They get sad everytime the CPI reading is a leg lower.

They somehow think this is a surgical strike, rather than wide reaching.

Insolvencies and unemployment isn't bad enough yet to appreciate the consequences.

As the saying goes, when it's someone else's insolvency or unemployment it's a recession. When it's your own, it's a depression.

DTI rules are in force as of yesterday, I think. That gives us some kind of backstop against property craziness in the event of low interest rates.

Some kind. Not a demonstratively good one, but some kind.

Yes not necessarily enough, but should hold back some of the investor froth, at least for those who already own a leveraged property or two.

It holds back investor and OO froth. Making it harder for those on middle-lower incomes to buy a house at all. And suppresses new dwelling generation, forcing more competition over existing properties.

About the only good thing it does is reduce lending over exposure.

From my memory of the RBNZ DTI stats, it's pretty well targeted at investors despite the higher limit for them - cuts off a much bigger tail of tending for them than other groups.

I'm speaking to how DTIs have generally played out in the past. It has the inverse effect on increasing affordability, both on housing purchases, and rents.

Medicine never tastes nice.

This is why I cannot buy into any of the bank economists growth forecasts. We are still watching the NZ economy contract and sputter along in a downward direction.

.

it's like when winter comes, all the sick or weak trees will just die.

Chapel Bar Ponsonby is in receivership, many more to follow.

That place is always busy, even on Sundays. I wonder if it was just managed poorly?

I think its just a secured creditor who wants their money back..... It will rise again in new name/ownership.

The creditor is also a shareholder. Loaned money to the holding company and put the co in liquidation when it couldn't pay him. He is the proud liquidater of a string of hospo Co's previous to this.

The tide goes out and you see who is naked.

All survivor SMBs (most of the NZ economy) are taking avoiding action. The smart ones with a future will be ruthlessly cutting costs, freezing hiring, and battening down the hatches, which all has a knock-on effect. They don't like to do it, but unlike employees, no-one comes to save them when things get harder, they have to be pre-emptive. They'll still be selling hard though, I salute them.

The smarter ones would've been doing this years ago, and building a cash buffer. Plenty now have been operating on fumes for a couple of years, hoping for market conditions to improve, when instead they're getting worse.

Getting through the COVID years was enough to stuff a lot of SMEs. There's not been much time to rebuild reserves and re-save since then. This is akin to kicking a grown man while he is still down.

If you could see this coming, an SME owner should've restructured 4 years ago to be incredibly lean.

Too many would've thought the trading environment during 2020-2022 would've been sustainable.

A big if given that absolutely no one had any understanding or experience of what a global pandemic business and societal lockdown was going to be like - or that it could even happen.

As soon as the government was paying businesses to retain staff, and basic items started becoming scarce, that should've been the cue.

We have had competitors bought out by large Aussie corporates who are actively squeezing us. We have had to respond by hiring and pushing back hard. Won't make a dime this year but will survive well enough.

"retail liquidations have increased by 44% compared to the previous year, with food retailers experiencing the highest volume of liquidations." Perhaps the double whammy of Covid, high interest rates, and reduced consumer spending has affected marginal businesses ie those who were just keeping their head above water pre-covid when economic times were good. Although sad for employees who have lost their job, the business owner will probably move on or join the dole queue. This is a mopping up of businesses who thought the good times would roll on for a long time and could only survive one major adverse financial event.

I noticed on a trip to Akl over the long week end unnecessary shops like Pascoes and Michael Hill still have branches open in the big mall that I visited. So still a fair amount of money floating around. When I read about them closing branches then I'll say times are getting tough.

Michael Hill closing it's 3rd store due to retail crime https://www.1news.co.nz/2024/06/14/a-sad-day-michael-hill-jeweller-clos….

Perhaps the people you saw in the store were just figuring out how to rob it.

It's just the tip of the spear , Retail and Hospitality that have been holding on by their fingertips wont make it to Christmas.. The slide will eventuate in a Collapse ,, Michael Hill are closing stores , The Warehouse is now looking at closing stores and reducing operating hours

Both May months when Nats in Govt

Nats only stand for the banks & corporates, no one else

Gone by 2026

Forgets that banks announced record profits and record lending all through the Labour-Greens government.

Ditch the partisan coloured glasses and start looking at reality.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.